Weighing the Week Ahead: Asking the Right Questions

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsThere is a big economic calendar featuring the most important monthly reports – employment, ISM manufacturing, ISM services, and auto sales. In normal times we would be analyzing the data and the implications for corporate earnings and interest rates. There will be some of that, of course, but the “real” market news seems to be taking a back seat. With the media focused on non-market events, it allows investors to ask the right question:

Where can some additional work provide a big payoff?

Today’s WTWA will provide four insightful ideas that can boost your investment results – if you are able to ask the right questions.

Last Week Recap

In my last edition of WTWA I urged investors, bombarded with stories about the anniversary of the financial crisis, to quit fighting the last war. My objective was to provide useful information rather than guessing the twists and turns of the Washington news. I am taking the same approach this week. Readers have been receptive to this, and I appreciate it.

The Story in One Chart

I always start my personal review of the week by looking at a great chart. I especially like the version updated each week by Jill Mislinski. She includes a lot of valuable information in a single visual. The full post has even more charts and analysis, including commentary on volume. Check it out.

The market declined .99% on the week. The weekly trading range was about 1.1%, still very low. I summarize actual and implied volatility each week in our Indicator Snapshot section below. Volatility remains well below the long-term average.

Personal Note

I enjoyed my week away from the office and will travel home tomorrow. I saw some interesting and important ideas in my vacation reading, so I’m taking some time to pass them along.

The News

Each week I break down events into good and bad. For our purposes, “good” has two components. The news must be market friendly and better than expectations. I avoid using my personal preferences in evaluating news – and you should, too!

When relevant, I include expectations (E) and the prior reading (P).

The Good

- FOMC rate decision was expected and accepted by the markets.

- High-Frequency Indicators remain positive, although the long-leading group is just above neutral (New Deal Democrat).

- Durable goods orders rose 4.5% E 1.8% P -1.2% revised from -1.7%. Ex-transportation, the results were a little soft.

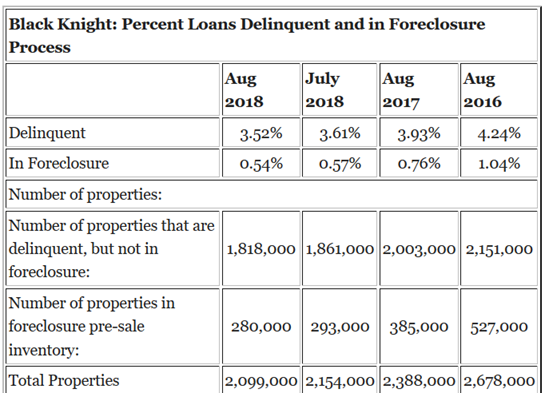

- National mortgage delinquencies decreased in August, with the rate down to 3.52. The table below from Black Knight (via Calculated Risk) shows the improvement over the last two years.

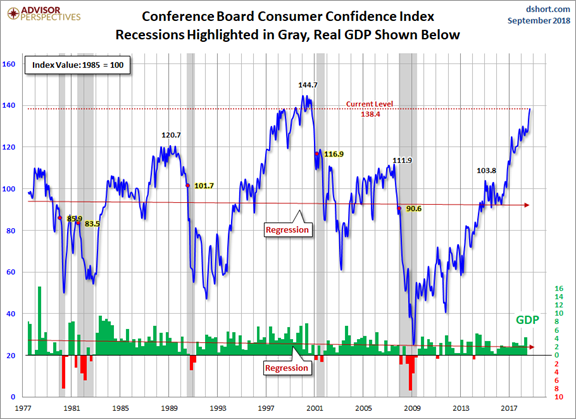

- Sentiment remained high (100.1) on the Michigan survey and hit a fresh high of 138.4 on the Conference Board measure E 131 P134.7. Jill Mislinski has the best charts on this subject, showing the relationship with the market and the economy.

The Bad

As has been the recent case, some of the “bad” news consists of indicators slightly off the best levels.

- Initial jobless claims rose to 214K E 209K P 202K

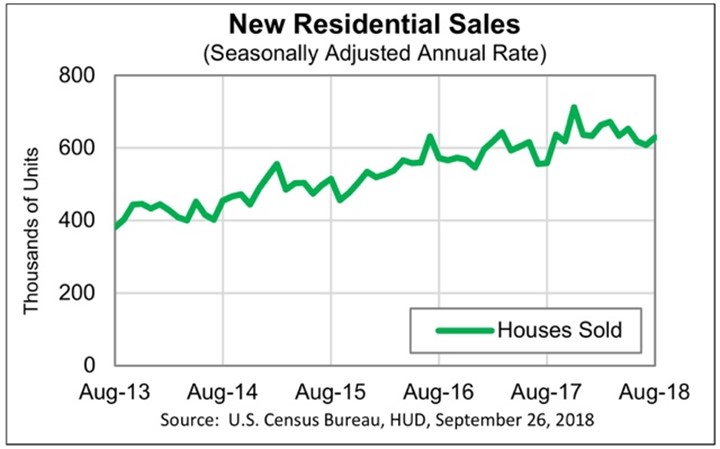

- Pending home sales declined 1.8% E a gain of 1.8% P -0.8%. New home sales were in line with expectations with a gain of 629K (SAAR). New Deal Democrat, however, notes signs of “rolling over.”

- Personal income increased 0.3% slightly missing expectations of 0.4% but equaling the prior of 0.3%

-

Personal spending increased 0.3% meeting expectations but missing the prior of 0.4%.

The Ugly

I am taking a week off from ugliness.

The Week Ahead

We would all like to know the direction of the market in advance. Good luck with that! Second best is planning what to look for and how to react.

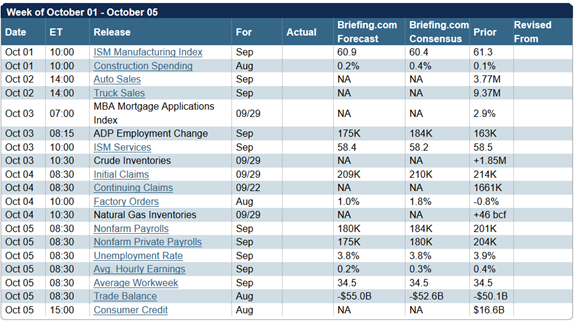

The Calendar

When the trading week starts with the first of the month, we get a big economic calendar. The employment reports will garner the most attention. The ISM manufacturing and services indexes provide a timely look at business activity. Auto sales round out the top reports.

Briefing.com has a good U.S. economic calendar for the week (and many other good features which I monitor each day). Here are the main U.S. releases.

Next Week’s Theme

There is a lot of important economic news, but that has not been very important in recent weeks. A solid economy and a gradual pace for the Fed seem to be reflected in the markets.

The emphasis on Washington “stories” is understandable, but not profitable for investors. The confirmation of a Supreme Court Justice is, of course, very important. The link to investing is tougher to find. The attraction as a news story is clear-cut. The issues are those where there are no real experts and everyone’s opinion is equal. Everyone wants to watch, form their own opinion, and discuss with friends.

It represents something of a pause in the normal give-and-take of market issues. I want to take advantage of that by raising important questions, overlooked by most. We should be asking:

How can investors ask the right questions – those most salient for future results?

The most important require some study and thought, but the results will pay off.

- How should investors plan for the mid-term elections? David Templeton (HORAN) looks at the Presidential cycle. He notes that the historical period matters as does the time increments studied. This year the history seems especially unhelpful, since September has been the worst month. This week’s Barron’s roundtable, the cover story, reviews the range of possible outcomes. The expert panel focuses on what to expect from each scenario, not which scenario to expect. Ben Phillips, CEO of EventShares, sponsor of a policy-related ETF (PLCY), is especially helpful in revealing specific stock ideas related to various election outcomes.

-

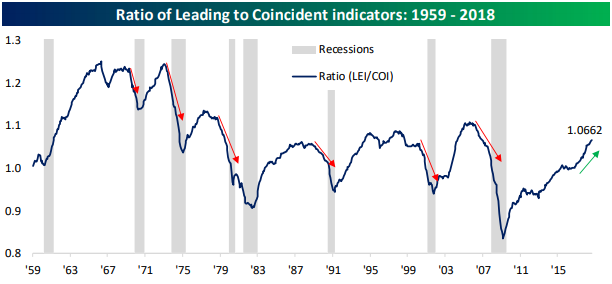

Dr. Ed Yardeni raises a question on the minds of many: With so many apparent bear traps, why does the market continue to charge ahead? His post includes a comprehensive review of worries including helpful charts. He notes five corrections and six “panic attacks.” All were followed by rebounds. Dr. Ed concludes as follows:

So what will it take to snare the bull in the bear traps? It will take a recession. That’s all there is to it. While Goldman and everyone else is on the lookout for this event, both the Index of Leading Economic Indicators (LEI) and the Index of Coincident Economic Indicators (CEI) rose to new record highs during August (Fig. 11). The LEI did so even though the yield curve spread, which is only one of this index’s 10 components, has been narrowing fairly steadily since 2013, but remains positive. It only subtracts from the LEI when it is negative. So it is still contributing positively to the LEI, though to a lesser extent. History shows that the CEI, which is a good monthly proxy for quarterly real GDP, falls when a financial crisis occurs, triggering a credit crunch and a recession. There’s no sign that scenario is about to play out again anytime soon.

- Eddy Elfenbein directs attention to The Silent Bear Market. Those who focus on the averages and some headline stocks may be missing some real opportunities. The emphasis on tech may be changing. [And congratulations to Eddy on the second anniversary of his innovative ETF, CWS. It is performing well and provides easy access to his choices].

The Wall Street Journal notes that stocks like Harley-Davidson, Whirlpool, Stanley Black & Decker and Caterpillar haven’t done much of anything. The list also includes consumer staples like General Mills and our own, J.M. Smucker. Apple and Amazon make up 30% of the S&P 500’s gain so far this year.

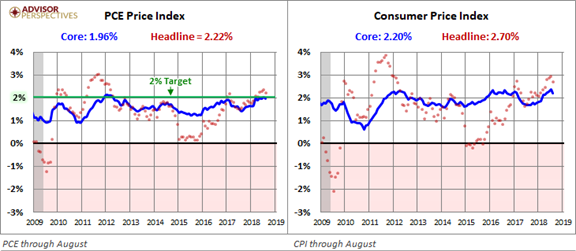

- Why isn’t the Fed more concerned about inflation? Most people feel that their own costs are rising significantly. Jill Mislinski provides a helpful comparison between the CPI and the price index for personal consumption expenditures, the PCE. Understanding these differences will help in understanding the Fed.

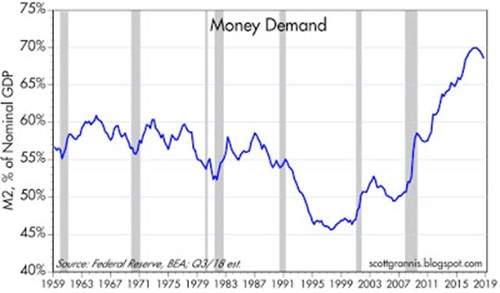

- Should we worry about the impending reduction in the Fed’s balance sheet? Scott Grannis explains that the original expansion satisfied demand for safe assets. This is why M2 growth was modest despite the expansion in the monetary base. The velocity of money slowed significantly but is now increasing. Here is the key chart from his post.

Scott observes:

Chart #5 is the main exhibit. This shows the ratio of M2 to nominal GDP. To understand this chart, think of M2 as a proxy for the amount of cash (or equivalents) that the average person, company, or investor wants to hold at any given time. Think of GDP as a proxy for the average person’s annual income. The ratio of the two is therefore a proxy for the percentage of the average person’s or corporation’s annual income that is desired to be held in safe and relatively liquid form (i.e., cash or cash equivalents). In times of uncertainty, it stands to reason that most people would want to hold more of their assets in cash, and in times of optimism they would want to hold less.

In today’s Final Thought, I’ll add some comments for each of these great questions.

Quant Corner

We follow some regular featured sources and the best other quant news from the week.

Risk Analysis

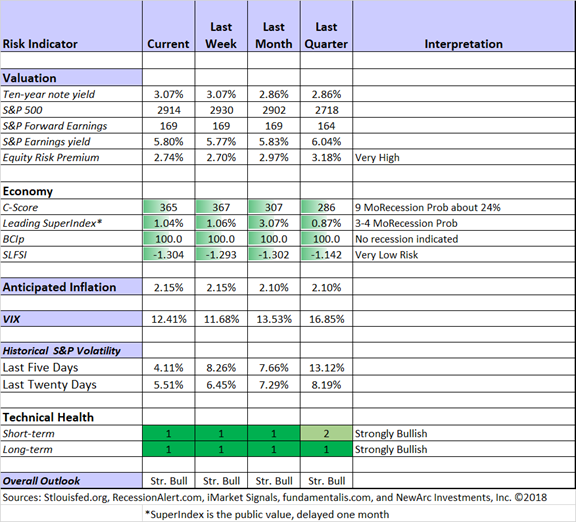

I have a rule for my investment clients. Think first about your risk. Only then should you consider possible rewards. I monitor many quantitative reports and highlight the best methods in this weekly update.

The Indicator Snapshot

Short-term trading conditions continue at highly favorable levels. Actual volatility remains very low. While many argue that the low VIX level is a sign of complacency, it remains higher than realized volatility. Those selling volatility are making money. The 3% yield has been exceeded; some see this as a precursor to a new trading range for the ten-year note.

My team has been working on the historical indicator snapshot project while I have been vacationing. I’ll try to post something soon.

The Featured Sources:

Bob Dieli: Business cycle analysis via the “C Score.

Brian Gilmartin: All things earnings, for the overall market as well as many individual companies.

RecessionAlert: Strong quantitative indicators for both economic and market analysis.

Georg Vrba: Business cycle indicator and market timing tools. None of Georg’s indicators signal recession. Here is the latest chart on the Business Cycle Index.

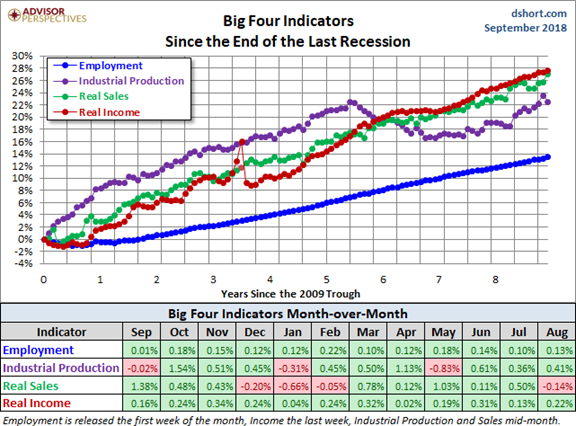

Doug Short and Jill Mislinski: Regular updating of an array of indicators. Great charts and analysis. It is time for an update of their key summary of the Big Four economic data points.

Guest Commentary

Mark Hulbert (Barron’s) analyzes the strategy of using the 200-day moving average as a buy/sell signal for the market. Ironically, it worked better when trading costs were higher. Check out the entire post for the explanation. [Jeff – I wonder. I am always suspicious of “explanations” formed after a relatively small number of instances. But the change in a long-heralded indicator is certainly interesting].

Bespoke analyzes the strength in the Leading Economic Indicators, noting the relationship with (eventual) recessions. This is yet another approach providing reassurance on the recession front.

Insight for Traders

Check out our weekly Stock Exchange post. We combine links to important posts about trading, themes of current interest, and ideas from our trading models. This week we explored the possible foundations for a trading approach. To highlight this theme, we were delighted to have expert commentary from Avi Gilburt and his team. We shared advice by top trading experts and discussed some recent picks from our trading models. Our ringleader and editor, Blue Harbinger, provided fundamental counterpoint for Avi and the models, who are all of the technical persuasion.

We have been getting good results from the models. Some of them fit a risk/reward profile that is attractive for retirement investors. Check out the weekly post (including results) and write to us at main at newarc dot com if you want more information or a consultation.

Insight for Investors

Investors should have a long-term horizon. They can often exploit trading volatility.

Best of the Week

If I had to pick a single most important source for investors to read this week it would be Aswath Damadoran’s analysis of Apple (AAPL) and Amazon (AMZN). The leading expert on stock valuation reviews the history of each company and past valuations. The article provides a detailed illustration for those wishing to learn how to do an expert fundamental valuation. And finally, of course, he provides some practical conclusions about these two popular stocks.

I have always operated on the premise that if you value companies, you should be willing to act on those valuations. In the case of Apple and Amazon, that would suggest that the next step that I should be taking with each company is to sell. With Apple, a stock that I have held for close to three years and which has served me well over the period, that would be accomplished by selling my holding. With Amazon, a stock that I have not held for more than five years, that would imply joining the legions of short sellers. Like an Avengers’ movie, I am going to leave you in suspense until my next post, because I have two loose ends to tie up, before I can act. The first is to grapple with the uncertainties that I have about my own stories for the two companies, and the resulting effects on their valuations. The second is what I will mysteriously term “the catalyst effect”, which I believe is indispensable, especially when you sell short.

Stock Ideas

Chuck Carnevale once again combines a great lesson in stock valuation with some practical advice. The key? The value investor should focus on the value of the business. Let the “market player” worry about the price of the stock. FedEx is the example, but the analysis is universal and timeless.

Stone Fox Capital analyzes Citigroup ©, explaining the importance of tangible book value. Anyone investing in banks should read this.

Jae Jun observes that some stocks seem to be getting all the attention. He finds three “boring companies” that represent both value and potential.

Personal Finance

Seeking Alpha Senior Editor Gil Weinreich’s Asset Allocation Daily is consistently both interesting and informative. This week I especially liked his explanation of a startling fact: The median retirement investor has nothing saved – nothing at all. Gil describes the sources of data on this subject and why it is not right to emphasize retirement accounts. He also cites Marc Gerstein on how to reduce risk while remaining invested. Marc combines an interesting analysis of how to use past performance along with the results of a “quality” screen. If you think it might be time to place greater emphasis on lower volatility rather than momentum, this is your kind of list!

Abnormal Returns is an important daily source for all of us following investment news. HisWednesday Personal Finance Post is especially helpful for individual investors. As always, there are many great links on various topics. I especially liked Ben Carlson’s identification of four important pieces of investment advice – and the reminder that small stuff is small. (See also Tony Isola below).

Watch out for…

Complicated insurance products. Tony Isola explains what to watch for.

Airlines. Morningstar’s updated analysis of the four major carriers shows them to be fairly valued.

Final Thought

My week in a community of expert bridge players from all over the world was surprising in one way. No one from any country mentioned US policy, international issues, or our President. I competed against teams from France, Israel, China, Indonesia, Italy, and Japan – among others.

Here are some additional thoughts on the five questions for the week.

- It is still too soon for a good read on the mid-term elections. There are so many new events each week that the situation remains fluid. Like the Barron’s panel, I prefer to plan and prepare rather than to guess the outcome.

- I strongly agree with Dr. Ed. The market is trading on economic fundamentals and earnings expectations. In the absence of a recession, equities remain attractive. This is, of course, why we monitor these indicators so closely in each installment of WTWA.

- Eddy (and Marc Gerstein) shine a light on some of the many inexpensive stocks in the current market.

- It is easy to complain about the Fed and the cost of living. Feel free to do so when having drinks with friends. In your investing it is more important to understand the Fed than to fight it through disagreement.

- The Scott Grannis post is crucial for your investment outlook. Those who misunderstood the effects of the Fed QE policies will also be wrong about the unwinding. The post is clearly organized and explained, but it is still not easy material for most. It is worth reading twice.

I do not expect this week’s questions to be on the lips of the punditry in the week ahead. Willingness to ask the right questions gives us an advantage over others!

I’m more worried about:

I have enjoyed a week without a focus on worries and financial media. No TIVO to do recaps! I’ll look for worries again on Monday morning. Meanwhile, the delicate balance is holding. The strength in the economy and corporate earnings has trumped (sorry – on my mind for the last week) the political news.

Membership required

Membership is now required to use this feature. To learn more:

View Membership Benefits