In the past few years, the London interbank offered rate (LIBOR) has faced well-publicized challenges. LIBOR was intended to reflect the cost at which large banks could borrow from each other and for decades was a benchmark for numerous private-sector rates. However, the credibility of LIBOR was eroded after evidence of manipulation, leading the UK Financial Conduct Authority to call for its eventual phasing out. US financial authorities, recognizing the need for a replacement benchmark with greater transparency, recently launched the secured overnight financing rate (SOFR). We believe SOFR is an improvement over LIBOR because it is based on interest rates charged in actual lending transactions. In contrast, LIBOR is based on submissions of interbank lending rates by major banks that don’t have to be tied to actual transactions, making it more susceptible to manipulation.

The search for a LIBOR replacement

Given the importance of LIBOR as a financial market reference rate, US financial authorities sought to identify a new, more transparent benchmark. The Board of Governors of the Federal Reserve (Fed) and the Federal Reserve Bank of New York convened the Alternative Reference Rates Committee (ARRC) in 2014 to find a replacement.

The committee considered several alternatives, including repurchase agreement (repo) rates. A repo agreement is an agreement to sell securities one day and buy them back the following day. The following three repo rates were considered:

- The Tri-party General Collateral Rate (TGCR). Based on trade-level, tri-party data collected from the Bank of New York Mellon.

- The Broad General Collateral Rate (BGCR). Calculated using the TGCR and the General Collateral Financing (GCF) repo rate as reported by the Depository Trust & Clearing Corporation.

- The Secured Overnight Financing Rate (SOFR). Based on BGCR and bilateral repo rates cleared by the Fixed Income Clearing Corporation (FICC).

After three years of careful study, the ARRC identified SOFR — the broadest of the three repo rates — as its preferred alternative to LIBOR, and established 2021 as the target date for LIBOR’s phase-out. On April 3 of this year, the Federal Reserve Bank of New York began daily publication of SOFR.

What is SOFR?

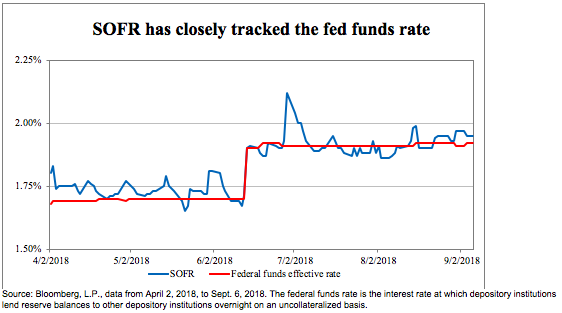

SOFR is a secured, overnight funding rate based on a broad range of repo transactions collateralized by Treasury securities. It is considered one of the most robust indexes available since it is based on a high volume (approximately $800 billion) of daily overnight transactions.1 Its calculation is derived from the TGCR, the GCF repo rate and the FICC-cleared bilateral repo rate. SOFR (along with the TGCR and BGCR) provides market participants with greater transparency into an important segment of the US financial system - the Treasury repo market.

Dynamics impacting the volatility of SOFR

We expect some volatility in the SOFR benchmark due to factors that typically cause volatility in Treasury repo markets. These include changes in Treasury bill supply, dealer balance sheet management and excess cash flows of government-sponsored enterprises into and out of funding markets, to name a few.

How has the market responded to SOFR?

In late July, the Federal National Mortgage Association (FNMA) became the first entity to issue a floating rate security benchmarked to SOFR — a meaningful step in the transition away from LIBOR. The market response appeared positive, as the deal was well oversubscribed. On the heels of the FNMA transaction, the World Bank became the second notable issuer to generate a funding deal pegged to SOFR. Several private sector firms have recently followed suit. The Chicago Mercantile Exchange also launched SOFR futures contracts in May 2018.

In an important acknowledgement, Standard & Poor’s called the benchmark an “anchor money market reference rate” in its principal stability fund ratings methodology, which makes the SOFR index eligible for purchase by money market funds rated by the agency. And with the implementation of the SOFR futures market, investors now have a framework for forward-looking expectations and values of the benchmark.

Why is the transition important to investors?

LIBOR is the reference rate currently driving funding costs on a huge volume and variety of financial products. The transition to SOFR therefore represents a major change for global financial markets.

The transition from LIBOR to SOFR will be especially relevant for investors in floating rate debt and for issuers seeking variable rate funding. Because coupons on floating rate notes have historically been set as a percentage amount, or “spread,” over LIBOR, a reliable and credible LIBOR alternative is essential. One question yet to be resolved is how floating rate notes that mature after 2021 will be impacted. Because some of these notes are currently being issued with maturities that extend beyond this date, Invesco Fixed Income hopes to see more floating rate note issuance based on SOFR going forward.

Another important consideration is pricing. For investors to receive the same floating rate yield as LIBOR-based notes, they must demand a higher spread over SOFR to compensate for SOFR’s generally lower yields. This differential is due to some important differences in what these rates represent — SOFR is a secured overnight rate, while 3-month LIBOR is longer-term and unsecured.

Looking ahead

Although the market is still a few years away from completing the transition from LIBOR to SOFR, we believe the success of recent deals suggests that SOFR will be a welcome replacement. Over the course of the next year, we anticipate increased adoption and issuance of securities based on SOFR, which would help provide depth to the market. As we approach 2021, investors may be wary of LIBOR-indexed securities as questions and concerns arise over whether LIBOR contributors will continue their voluntary submissions, which could lead to volatility of the LIBOR index.

Potential key benefits and challenges related to SOFR

Potential benefits

- The SOFR index provides a fallback rate as LIBOR is phased out.

- SOFR is a robust benchmark supported by substantial transactional data for the issuance of floating rate securities.

- Increases in repo rates (due to increased Treasury supply, for example) should be reflected in the SOFR index.

- SOFR should automatically reset when the Fed raises rates, providing a quick update to securities pegged to the reference rate.

Challenges

- SOFR is expected to experience some volatility, which is typically seen in repo markets.

- Because SOFR is tied to overnight repo rates and Treasury collateral, falling repo rates (due to a credit event that causes a flight to quality, for example) would likely reduce yields on floating rate securities pegged to the index.

- Because SOFR is a relatively new index, markets will likely require an adjustment period to gauge its liquidity, determine its pricing and understand its potential performance versus other established indices, such as the overnight bank funding rate, interest on excess reserves and the federal funds rate.

Conclusion

Because the SOFR index is based on a high volume of transactional data in the repo market, we believe it provides a robust replacement for LIBOR. The recent issuance and acceptance of funding transactions benchmarked to SOFR represent the beginning of the monumental transition away from LIBOR, which has historically served as the reference rate for most floating rate securities.

Going forward, Invesco Fixed Income expects greater adoption of SOFR by a broad range of issuers as entities collect data points tracking its volatility and liquidity, determine its performance versus other indices and establish the internal systems and procedures necessary to issue and price securities to the SOFR benchmark.

1 Source: Bloomberg, L.P., as of Sept. 13, 2018.

Important information

Blog header image: Kiev Victor/Shutterstock.com

LIBOR (London Interbank Offered Rate) is a benchmark rate that some of the world’s leading banks charge each other for short-term loans. US LIBOR represents LIBOR denominated in US dollars.

The repo (or repurchase) rate is the rate at which the central bank of a country lends money to commercial banks in the event of any shortfall of funds. The repo rate can be used by monetary authorities to control inflation.

Justin Mandeville

Portfolio Manager

Justin Mandeville joined the Invesco Global Liquidity team in January 2015 as a Portfolio Manager, and is involved with the management of short-term Treasury, agency and repo securities.

Mr. Mandeville began his career with Vanguard’s client relationship management group before transitioning to Vanguard’s Fixed Income and Money Market team.

Mr. Mandeville earned his BS degree in business administration from Pennsylvania State University, and his MBA, with a concentration in finance, from Drexel University

Jacob Habibi

Senior Analyst

Jacob Habibi is a Senior Credit Analyst at Invesco Fixed Income. He is responsible for conducting fundamental credit research and making investment recommendations on US and Canadian domiciled corporate bonds and credit default swaps in the banking, brokerage and finance sectors in both the investment grade and high yield credit markets. He also contributes to developing investment strategies for the US investment grade market.

Mr. Habibi joined Invesco in May 2001 as a credit research assistant, providing research and financial model support to the US IG Corporate Credit team. In April 2003 he transitioned to a role as an investment application analyst, assessing the business needs of investment professionals and developing web-based applications to support many of Invesco’s fixed income investment products including interest rates, MBS, ABS, CMBS, currencies, investment grade credit, high yield credit, and emerging markets. In June 2007 he returned to the Investments team as a fixed income investment associate, spending 10 months in a rotational program with Quantitative Research, Government Bond Trading, Corporate Credit/Trading and Mortgage & ABS Credit/Trading. In March 2008, he joined the US IG Credit Research team as a credit analyst, where he continues to serve in this capacity.

Mr. Habibi earned his MS degree in banking and financial services from Boston University, graduating with honors. He also earned a BS degree in business administration with a double major in finance and computer information systems from the University of Louisville, graduating magna cum laude. He holds the Chartered Financial Analyst® (CFA®) designation.

This does not constitute a recommendation of any investment strategy or product for a particular investor. Investors should consult a financial advisor/financial consultant before making any investment decisions. Invesco does not provide tax advice. The tax information contained herein is general and is not exhaustive by nature. Federal and state tax laws are complex and constantly changing. Investors should always consult their own legal or tax professional for information concerning their individual situation. The opinions expressed are those of the authors, are based on current market conditions and are subject to change without notice. These opinions may differ from those of other Invesco investment professionals.

NOT FDIC INSURED | MAY LOSE VALUE | NO BANK GUARANTEE

All data provided by Invesco unless otherwise noted.

Invesco Distributors, Inc. is the US distributor for Invesco Ltd.’s retail products and collective trust funds. Invesco Advisers, Inc. and other affiliated investment advisers mentioned provide investment advisory services and do not sell securities. Invesco Unit Investment Trusts are distributed by the sponsor, Invesco Capital Markets, Inc., and broker-dealers including Invesco Distributors, Inc. Each entity is an indirect, wholly owned subsidiary of Invesco Ltd.

©2018 Invesco Ltd. All rights reserved.