The Best Time to Prepare Is While the Bull Runs

Membership required

Membership is now required to use this feature. To learn more:

View Membership Benefits

In case you couldn’t tell from the ubiquitous political ads and yard signs, midterm elections are right around the corner—46 days from now, to be exact. Historically, volatility has increased and markets have dipped leading up to midterms on uncertainty, but afterward they’ve outperformed.

Of especially good news is that we’re entering the three most bullish quarters in the four-year presidential cycle, according to LPL Financial Research. The fourth quarter of the president’s second year in office, which begins next month, and the first and second quarters of the third year have collectively been the best nine months for returns, based on 120 years of data.

It makes sense why this has been the case. Following midterms, the president has been motivated to “boost the economy with pro-growth policies ahead of the election in year four,” writes LPL Financial.

Government Policy Is a Precursor to Change

Should Republicans manage to hold on to both the House and Senate—which Wells Fargo analysts Craig Holke and Paul Christopher estimate has a 30 percent probability—it’s likely they’ll try to pass “Tax Reform 2.0,” with an emphasis on the individual tax side. We can also probably expect to see additional financial deregulation.

Cornerstone Macro is in agreement, writing that “the better Republicans do in the election, the more confidence investors will have that [President Donald] Trump could be reelected and the business-friendly regulatory practices will remain in place.” A GOP Congress, the research firm adds, would be supportive of banks and energy, specifically oil, gas and coal. Since Trump’s inauguration, the Dow Jones U.S. Coal Index has climbed nearly 60 percent, double the S&P 500’s performance.

The more likely outcome, according to Holke and Christopher, is a divided Congress, with Democrats taking control of the House. In such a scenario, financial deregulation would slow, but Trump, who’s pushed hard for aggressive infrastructure spending, might find the support he needs for a bill from Democrats. This would help increase demand for commodities and raw materials, but “additional stimulus in an economy already near capacity may result in higher inflation, negatively affecting fixed income,” Holke and Christopher write.

On the other hand, higher inflation has historically meant higher gold prices. After climbing for 12 months, year-over-year change in consumer prices cooled in August to 2.7 percent, from July’s 2.9 percent.

Government policy is a precursor to change, as I often say. It’s not the party that matters but the policies, and there are ways for investors to make money however the midterms unfold.

Money Managers and Banks Are Adding Safe Havens at a Faster Pace

With the bull run now the longest in U.S. stock market history, there’s a lot of talk and speculation about when the next major pullback will happen. I’ve discussed a number of possible catalysts with you already, from record levels of global debt to the flattening yield curve. Last week, I shared with you that Goldman’s bull/bear indicator hit its highest level in nearly 50 years.

Even as markets closed at fresh all-time highs, essentially ignoring the intensifying U.S.-China trade war, Bank of America Merrill Lynch (BofAML) called the bull run “dead” this week, due to slowing global economic growth and the end of monetary stimulus. “The Fed is now in the midst of a tightening cycle, ignoring structural deflation, focusing on cyclical inflation,” writes BofAML chief strategist Michal Hartnett.

Against this backdrop, a growing number of money managers hold a dim view of continued economic growth. September’s Bank of America Merrill Lynch Fund Manager Survey found that a net 24 percent of fund managers believe global growth will slow over the next 12 months. That’s the highest percentage of managers with such a view since December 2011, the height of the European debt crisis. Reasons given for this bearishness are the U.S.-China trade tensions and, again, the end of central bank accommodation.

Fund managers are raising their cash levels, Hartnett says, as well as their exposure to fixed income, which has been used as a safe haven in times of uncertainty. In July, the most recent month of Morningstar data, bond funds attracted the greatest amount of any asset class in the U.S., with taxable and municipal bonds seeing a collective $28.5 billion in inflows. U.S. equity funds, meanwhile, collected a little under $3 billion, and in fact have seen $11 billion in outflows in the 12 months through July 31.

Getting even more specific, U.S. actively-managed ultrashort bond funds were the biggest winner, attracting over $6 billion in July, according to Morningstar.

Gold demand among central banks has also accelerated this year. According to the World Gold Council (WGC), banks added a net 193.3 metric tons of gold to their reserves in the first half of the year, an 8 percent increase from 2017. This was the most purchased in the first six months since 2015.

The Next Crisis Could Be Triggered by Passive Indexing

One of the biggest risks right now, I believe, is the explosion in passive, “dumb beta” indexing. Trillions of dollars have poured into products that track indices built not on fundamental factors like revenue, cash flow and return on invested capital (ROIC), but on simple market capitalization. A piling on effect has occurred, whereby multibillion-dollar funds are buying more and more of the most expensive stocks. This has resulted in overinflated valuations.

The big risk is when these funds rebalance, which could happen as early as the beginning of next year. Last year, junior mining stocks got crushed after the VanEck Vectors Junior Gold Miners ETF (GDXJ) restructured its portfolio. Imagine what could happen if all passive index funds did the same simultaneously.

This week I wrote more in depth about the risks passive indexing poses. If you didn’t get a chance to read it, I invite you to do so by clicking here.

Index Summary

- The major market indices finished mixed this week. The Dow Jones Industrial Average gained 2.25 percent. The S&P 500 Stock Index rose 0.85 percent, while the Nasdaq Composite fell 0.29 percent. The Russell 2000 small capitalization index lost 0.55 percent this week.

- The Hang Seng Composite gained 3.29 percent this week; while Taiwan was up 0.96 percent and the KOSPI rose 0.90 percent.

- The 10-year Treasury bond yield rose 6 basis points to 3.06 percent.

Domestic Equity Market

Strengths

- Materials was the best performing sector of the week, increasing by 2.30 percent versus an overall increase of 0.89 percent for the S&P 500.

- Brighthouse Financial Inc was the best performing stock for the week, increasing 10.66 percent.

- Tilray is set to be the first Canadian cannabis company to export legal weed to the United States. Its shares soared 28.95 percent Wednesday after receiving approval to ship medical cannabis for a study in California. Shares have gained more than 800 percent since the initial public offering priced at $17 in mid-July.

Weaknesses

- Utilities was the worst performing sector for the week, decreasing by 1.53 percent versus an overall increase of 0.89 percent for the S&P 500.

- Copart Inc was the worst performing stock for the week, falling 18.79 percent.

- Oracle shares dropped more than 5 percent in after-hours trading Monday after the business-software maker announced revenue from its cloud services and license support unit was up 3.2 percent to $6.61 billion in its fiscal first quarter. This was missing the $6.71 billion that was expected by analysts surveyed by Reuters.

Opportunities

- Aston Martin is seeking a $6.7 billion valuation for its initial public offering in October. The luxury car maker set a price range of around $10 to $30, Reuters says.

- Salesforce's newest product, Einstein Voice, is an artificial intelligence (AI) similar to Amazon's Alexa that is meant for use in the workforce. The assistant tool within Einstein Voice can interpret voices, allowing it to capture spoken memos and log that information into Salesforce.

- Amazon may open 3,000 cashierless, physical locations by 2021, Bloomberg reports. Jeff Bezos is also experimenting with different formats for “Amazon Go.”

Threats

- The U.S. Department of Justice has reportedly asked Tesla for documentation after CEO Elon Musk tweeted about having “funding secured” for taking the company private. The automotive company is under investigation due to Musk’s statements on social media about taking Tesla private, according to Bloomberg.

- The European Union (EU) has begun its preliminary investigation into whether Amazon has violated antitrust laws. Competition commissioner Margrethe Vestager explained that “[w]e haven't formally opened the case, but we are trying to make sure that we get the full picture.” Vestager has overseen investigations which ended in substantial fines for both Google and Apple.

- The new Apple Watch is now on sale. Preliminary reviews, however, are not positive for the gadget, claiming that the features are overshadowed by its hefty price tag. This is the first major redesign since the Apple Watch was initially released in 2015.

The Economy and Bond Market

Strengths

- The Conference Board announced this week that its leading economic index rose by 0.4 percent in August, after climbing by a revised 0.7 percent in July. "The leading indicators are consistent with a solid growth scenario in the second half of 2018 and at this stage of a maturing business cycle in the U.S., it doesn't get much better than this," said Ataman Ozyildirim, Director of Business Cycles and Growth Research at the Conference Board.

- The number of Americans filing for unemployment benefits unexpectedly fell last week, hitting near a 49-year low, in a sign that the job market remains strong. Initial claims for state unemployment benefits fell by 3,000 to a seasonally adjusted level of 201,000 for the week ended September 15, according to the Labor Department. This is the lowest level since November 1969.

- The Philadelphia Fed Manufacturing Business Outlook Survey rebounded strongly in September, rising 11 points to 22.9. Over 38 percent of the manufacturers surveyed reported increases in overall activity this month, while just 15 percent reported decreases.

Weaknesses

- On Monday, President Trump ordered another round of tariffs of 10 percent on $200 billion worth of Chinese goods. This means that more than half of all goods coming into the U.S. from China will be subject to import duties of some level.

- Sales of previously owned U.S. homes held steady in August after a stretch of weakness in the housing market. Existing-home sales were flat in August from the previous month at a seasonally adjusted annual rate of 5.34 million, the National Association of Realtors reported on Thursday. Economists surveyed by The Wall Street Journal had expected sales to notch a 5.38 million annual rate. Compared with this time a year ago, sales in August declined by 1.5 percent.

- The Empire State manufacturing index fell to 19 in September, down from a 10-month high in August of 25.6. Economists had forecast the index to come in at 23, according to a survey by Econoday.

Opportunities

- After years of weak growth, global bond yields are beginning to react as wages are finally starting to rise in several developed countries. The yield-to-worst on the Bloomberg Barclays Global Aggregate Bond Index is at the highest level in more than four years. U.K. basic wages rose the most since July 2015, gains in U.S. average hourly earnings reached a post-recession peak in August and cash earnings in Japan are rising at a pace not seen for about 20 years. Should wages continue climbing, it would suggest even higher yields as central banks react to inflation. This scenario presents an opportunity for investors looking for fixed-income exposure to get in at attractive yield levels that haven’t been seen in years.

- When the Federal Reserve gathers next week, markets likely will be looking past a widely expected rate hike and toward the direction the central bank will chart ahead. A quarter-point increase in the Fed's benchmark funds rate is highly expected. That will take the funds target from 2 percent to 2.25 percent, where it last was more than a decade ago. For now, the conclusion of most investors is that the Fed will continue the path of steady and gradual rate hikes and a continued unwinding of the balance sheet.

- Ahead of next week’s U.S. GDP data release, Nomura analysts’ outlook stated that strong August housing starts and some upward revisions to the previous months imply better residential investment growth in the third quarter. As such, their real GDP tracking estimate for the third quarter remains unchanged at a robust pace of 3.4 percent quarter-on-quarter.

Threats

- The release of personal consumption expenditure data next week is forecasting a dip from 0.4 percent to 0.3 percent. After the strong summer spending season, it could be a sign of slower consumption ahead.

- With consumer sentiment at all-time highs, next week’s release of the University of Michigan Consumer Sentiment Survey is at risk of disappointing, especially after the increased trade talk hostility between the U.S. and China.

- Durable goods orders have been choppy and trending lower lately. Next week’s release is at risk of continuing the downward trend.

Gold Market

This week spot gold closed at $1,198.78 up $5.28 per ounce, or 0.44 percent. Gold stocks, as measured by the NYSE Arca Gold Miners Index, ended the week higher by 4.39 percent. The S&P/TSX Venture Index rose 0.67 percent. The U.S. Trade-Weighted Dollar Index ended the week down 0.77 percent.

| Date | Event | Survey | Actual | Prior |

|---|---|---|---|---|

| Sep-17 | Eurozone CPI Core YoY | 1.0% | 1.0% | 1.0% |

| Sep-19 | Housing Starts | 1240k | 1282k | 1168k |

| Sep-20 | Initial Jobless Claims | 210k | 201k | 204k |

| Sep-25 | Conf. Board Consumer Confidence | 132.0 | -- | 133.4 |

| Sep-25 | New Home Sales | 630k | -- | 627k |

| Sep-26 | FOMC Rate Decision (Upper Bound) | 2.25% | -- | 2.00% |

| Sep-27 | Hong Kong Exports YoY | 8.5% | -- | 10.0 |

| Sep-27 | Germany CPI YoY | 2.0% | -- | 2.0% |

| Sep-27 | GDP Annualized QoQ | 4.2% | -- | 4.2% |

| Sep-27 | Durable Goods Orders | 1.8% | -- | -1.7% |

| Sep-27 | Initial Jobless Claims | 210k | -- | 201k |

| Sep-27 | Caixin China PMI Mfg | 50.5 | -- | 50.6 |

| Sep-28 | Eurozone CPI Core YoY | 1.1% | -- | 1.0% |

Strengths

- The best performing metal this week was palladium, up 7.80 percent, scoring an eight-month high of $1,053.40 on Thursday, due to stockpiling by China, writes Kitco News. The World Gold Council reported this week that central banks added a net total of 193.3 tonnes of gold to their reserves in the first six months of 2018, representing an 8 percent increase from the same period in 2017 and the strongest first half of the year since 2015. The report notes that it is encouraging “to see several central banks utilize gold as an active asset to access liquidity or generate returns.” Russia, Turkey and Kazakhstan alone accounted for 86 percent of the central bank purchases for the time period.

- The Perth Mint Physical Gold ETF saw big inflows this week. Investors added a net $13.2 million into the fund on Tuesday, increasing the fund’s assets by 41 percent to reach its highest level since inception just over a month ago. Bloomberg writes that the ETF has attracted net inflows of $44.4 million since August 15.

- After several months of negotiations, labor groups representing more than 60 percent of workers at AngloGold Ashanti Ltd have signed a three-year wage deal with the major South African gold producer, reports Bloomberg. Negotiations between South Africa’s largest gold companies and labor unions began in July as producers are struggling to cut costs. The agreement between three unions and AngloGold is for a 6.5 percent pay raise for the first year and increases at the same rate or rate of inflation for each of the following two years. This is positive news for the South African gold industry, which has faced numerous challenges in recent years.

Weaknesses

- The worst performing metal this week was gold, still up 0.44 percent. Cobalt miners in the Democratic Republic of Congo are facing another round of bad news. The government is set to declare cobalt as a strategic metal, which will trigger a 10 percent royalty tax. This is far higher than the current 3.5 percent tax on cobalt produced in DRC and means a further cost increase for miners after a new mining code was implemented in June.

- Gold has continued to trade in the $1,200 per ounce range for the past month, even as assets fall in bullion-backed ETFs. The yellow metal has struggled to gain traction so far this year due to a stronger U.S. dollar. Ole Hansen, head of commodity strategy at Saxo Bank A/S, said that gold’s narrow trading range “does indicate that some underlying demand has begun to emerge, but in order for the price to progress to a point where short sellers begin to worry, it needs additional support from a combination of a weaker dollar and lower stocks.” Gold appears to be trading sideways as conflicting stories reported that the yellow metal was both up and down on the news of additional tariffs on Chinese imports to the U.S.

- Goldman Sachs released a report on Thursday revising its three-, six- and 12-month forecasts for gold that are all around $100 less than before. Kitco News reports that Goldman expects gold to be at $1,250 per ounce in the next three months and at $1,325 in one year. Although the group lowered its forecasts, it expects gold prices to gradually rise on the back of renewed emerging market demand.

Opportunities

- Gold is now around 85 times more expensive than silver per ounce as the gold/silver ratio hit a high not seen since 1995, according to Bloomberg data. Both precious metals have been falling so far in 2018 due to a stronger U.S. dollar, among other factors. ETF holdings backed by gold have fallen 1.3 percent this year, while those tracking silver have climbed 2.3 percent. Carsten Fritsch, an analyst at Commerzbank AG, told Bloomberg in a phone interview that “smart investors and long-term investors are seeing a lot of value in silver at these levels” and that “silver prices are low in both relative and absolute terms”. This rising ratio could attract more investors to silver.

- Gascoyne Resources released incredibly strong drill results near the Dalgaranga Gold Project in Western Australia. The company reported gold grades up to 1,450 grams per ton within an eight meter wide zone that has visible gold mineralization. Nighthawk Gold also reported strong drill results at its Colomac Gold Project in Canada with 16 of the 18 drill holes intersected with gold mineralization. Drill results include intersects of 84.30 meters of 2.91 grams per ton of gold and 24.55 meters of 5.05 grams per ton of gold. Lastly, Cardinal Resources said that it has a strong business case to move the preliminary feasibility study at the Namdini Gold Project in Ghana to being a definitive feasibility study after strong drill results.

- Ross Norman, CEO of Sharps Pixley, wrote this week that precious metals lease rates are tightening. Norman says that “just as buying and selling affects prices, borrowing and lending affect lease rates. If a market is undersupplied then it follows lease rates will rise, which can have a knock-on effect on prices.” Since precious metal markets are tightening, that could put pressure on large speculative short positions in gold and silver, which could lead to higher prices.

Threats

- Chile’s congress is reviewing a proposal for an additional royalty payment for copper and lithium miners operating in the country as a way to bolster the development of the regions around miners and deposits. The initiative proposes a 3 percent tax on the nominal value of extracted metals and would apply to copper miners producing more than 12,000 tons of the red metal a year and 50,000 tons of lithium. Chile is the world’s top producer of copper.

- The government of India is attempting to curb gold imports in an effort to check the fall in the rupee’s value and control its current account deficit, writes the Press Trust of India. Reports show they will attempt to use policy changes to curb imports, rather than raising customs duties, which can lead to an increase in smuggling activities. India saw gold imports jump by 93 percent in August, with demand expected to continue rising as the wedding season and Diwali celebrations near. The rupee has fallen around 6 percent since August and India’s trade deficit hit a near five-year high in July.

- Bloomberg reports that companies repatriated $169.5 billion to the U.S. in the second quarter of this year, according to data from the Commerce Department, up from $34.9 billion a year earlier. This could lead to a stronger dollar, if the money wasn’t already held in dollars. A stronger dollar historically is a headwind for the price of gold. More repatriations are expected as the tax overhaul signed into law by President Trump in December gives companies incentives to bring money back to the U.S. by lowering the tax rate to just 15 percent, down from 35 percent.

Blockchain and Digital Currencies

Strengths

- Of the cryptocurrencies tracked by CoinMarketCap, the best performing for the week ended September 21 was Bob’s Repair, which gained 311.26 percent.

- Cryptocurrency hedge funds continue to open up despite the downward fall in many digital assets, reports Bloomberg, with some of the more established names also expanding. BlockTower Capital, for example, was co-founded a year ago by former Goldman Sachs investment manager Matthew Goetz, and just last month the hedge fund opened a second office in New York, the article continues, now employing 13 people. According to researchers, nearly 100 cryptocurrency hedge funds have opened up in 2018 alone.

- Coinbase has announced the hiring of a new chief legal officer as it moves to grow its leadership team, reports Coindesk.com. “Brian Brooks, a former executive vice president, general counsel and corporate secretary at Fannie Mae, will now serve as the top attorney at the exchange, where he will help interact with regulators and oversee other issues,” the article reads. In addition to the hiring of Brooks, Coinbase announced it will be hiring over 100 new employees for its newly-opened New York office over the next year.

Weaknesses

- Of the cryptocurrencies tracked by CoinMarketCap, the worst performing for the week ended September 21 was BitcoinDark, which lost 36.33 percent.

- According to the New York State Attorney General’s office, it seems as though cryptocurrency exchanges aren’t doing much to stop manipulation, particularly because they don’t have the standard consumer protections that established financial markets have, reports Seeking Alpha. “The industry has yet to implement serious market surveillance capacities, akin to those of traditional trading venues, to detect and punish suspicious trading activity,” reads the report from Attorney General Barbara Underwood’s office.

- Zaif, a cryptocurrency exchange in Japan, is the latest to be hacked, according to Seeking Alpha, with losses of bitcoin and two other digital currencies totaling an estimated $60 million. This incident comes on the heels of another high-profile theft earlier in the year at Coincheck in Tokyo, where $530 million in coins was compromised. The Coincheck theft was “one of the world’s biggest cyber heists that forced regulators to step up risk management protocols,” the article reads.

Opportunities

- Despite cryptocurrencies losing more than 80 percent so far in 2018, Josh Fraser, co-founder of Origin, an open-source blockchain platform, believes that growth in the technology sector should allow digital currencies to end this year on a brighter note. “We’re seeing a shift toward development in the blockchain and crypto space, which is extremely important because some of the key pain points in the space are usability and pricing,” Fraser wrote in an email to MarketWatch. “People who have written off crypto as a result will only be drawn back in when they see real utility, versus speculation. This will help stabilize prices and is why building usable systems is critical.”

- Switzerland-based startup Eidoo announced plans to create a digital token tied to the price of gold, reports Coindesk.com. According to the company, the ERC-20-compatible token, or “the ekon,” will sit alongside its multicurrency wallet and decentralized exchange. “But perhaps more notable, each token will be redeemable for one gram of 99.9 percent fine gold, which the startup says will be stored in its vaults and audited every 90 days,” the article reads.

- During the CoinDesk Consensus conference in Singapore this week, Binance founder and CEO Zhao Changpeng indicated to attendees that he wants to launch cryptocurrency trading platforms on nearly every continent, reports Coindesk.com. Ideally, two exchanges per continent, the article clarifies. Currently Binance, which is the world’s largest crypto exchange by trading volume, is planning to roll out an exchange in Singapore that supports local fiat-to-crypto trading services.

Threats

- Bitmain, the Chinese maker of crypto mining rigs who controls close to half of the world’s bitcoin mining power, has seemed to forgotten an important lesson from the California Gold Rush, reports Bloomberg, which is to be the one selling shovels. Various leaks of the company’s financials have shined a light on its business model, (which doesn’t focus on selling shovels, per say). “What pops out at everyone who reads that initial slide is that while Bitmain is making and selling a lot of crypto shovels, it’s getting paid in digital gold, i.e. bitcoin and its offshoot bitcoin cash,” writes Bloomberg. Bitmain held less than 3 percent of its assets in cash at the end of March, compared with $1.17 billion in different digital currencies.

- Hackers are illegally targeting cryptocurrencies like Monero and bitcoin, reports Bloomberg, by exploiting a software flaw that was leaked from the U.S. government. In fact, in a report released last week by Cyber Threat Alliance, data shows that detected cases of illicit crypto mining have surged 459 percent in 2018, compared to a year ago.

- The Administrative Council for Economic Defense, Brazil’s antitrust watchdog, is investigating whether major banks in the country worked together to close off access to cryptocurrency services, reports Coindesk.com. Allegedly, the banks in the probe shut down accounts that belong to crypto traders and brokerages, although the banks deny these claims. Rather than allegedly abusing their power, the banks claim that these accounts were shuttered due to missing client data.

Energy and Natural Resources Market

Strengths

- Natural gas was the best performing major commodity this week, rising 7.77 percent. The commodity posted its best weekly gain since January after weather forecasts suggest winter may be coming earlier than expected. In addition, current inventory levels are sitting 18 percent below 5-year averages as the summer saw lower builds than anticipated.

- The best performing sector this week was the FTSE 350 Mining Index. The index rose 10.47 percent, tracking an advance in most major industrial commodities, after China unveiled additional fiscal measures to avoid an economic slowdown amid the trade spat with the U.S.

- The best performing stock for the week was Hudbay Minerals Inc. The Canadian base metals miner rose 12.20 percent after it was upgraded to a buy by market analysts citing better commodity price forecasts and the company’s current low valuation.

Weaknesses

- Lumber was the worst performing commodity this week. The commodity dropped 18.57 percent amid mounting concerns on the U.S. housing sector. U.S. housing data has corrected this year as a result of higher mortgage rates and increased raw materials costs.

- The worst performing sector this week was the S&P 1500 Paper & Forest Products Index. The index dropped 3.66 percent after sector analysts downgraded equities in the sector citing a worsening outlook for the U.S. housing sector.

- The worst performing stock for the week was Canfor Corp. The Canadian producer of lumber products dropped 12.39 percent after the paper and forest sector received analyst downgrades.

Opportunities

- China’s demand for copper is alive and humming. China is the world’s largest consumer of the red metal and has seen soaring demand for physical copper despite the threat to growth posed by the worsening trade war with the U.S. Premiums paid to secure physical metal rose to the highest in almost three years. Similarly, inventories in warehouses tracked by the Shanghai Futures Exchange have more than halved in the past six months.

- Goldman Sachs and Barclays agree that commodities are a good bet for the remainder of the year. Goldman argued that investors have factored in an extended trade war and are returning to markets like oil and copper. Its view is bolstered by stronger than expected manufacturing growth in the U.S., as well as the lack of a material slowdown in the EU, China or India. Barclays suggested copper prices may rally 5 percent in the fourth quarter.

- JPMorgan believes crude prices may rise further as supply risks continue to mount. The bank raised its fourth quarter West Texas Intermediate (WTI) price estimates to $75.83 per barrel, adding that prices could rise even further if the U.S. accelerates its monitoring of Iran-sanctioned oil buyers.

Threats

- President Trump imposed a 10 percent tariff on $200 billion worth of Chinese imports. The rate is set to increase to 25 percent in 2019, which means that U.S. consumers will only feel the effects of the change after the country’s November midterm elections.

- Trade war retaliation from China could cut 0.4 percentage points from U.S. gross domestic product in 2019, according to Oxford Economics. The impact for China is said to be 0.7 percentage point cut to 2019 gross domestic product, according to UBS and JPMorgan.

- Confidence among Asian companies slumped to the weakest in almost three years. Companies cited fear of a blowback from a worsening global trade war, according to Reuters. The data showed the steepest decline in confidence since the survey began in 2009, and could signal an upcoming economic slowdown, said Reuters.

China Region

Strengths

- China’s Shanghai Composite surged back by 4.37 percent this week, with Hong Kong’s Hang Seng Composite Index jumping 3.29 percent over the same time.

- The top gainer in the Hang Seng Composite Index (HSCI) for the week was Sinotruk Hong Kong Ltd. (3808 HK), which soared 43.57 percent over the last five days amid a broader China rebound and as the company announced a joint venture for a new heavy-duty truck in China.

- Materials constituted the top-performing sector in the HSCI for the week, rising 6.17 percent in that time, just barely nudging out consumer services, which rose 6.04 percent.

Weaknesses

- India’s SENSEX and NIFTY Indices dropped 3.26 and 3.22 percent respectively, and the Philippines Stock Exchange Index fell by 41 basis points for the week.

- Indonesia’s exports rose only 4.15 percent for the August measurement period, below analysts’ anticipated growth rate of 10.0 percent.

- Utilities constituted the worst-performing sector in the HSCI for the week, and notably the only one in the red in that time frame. The sector dropped 14 basis points over the last five trading days as investors put money back into riskier sectors.

Opportunities

- Despite all talk of trade wars and economic concerns, it remains worth noting that—as we have pointed out in recent weeks—China’s economy continues to chug along and grow at an enviable rate, and particularly so when viewed from a longer-term perspective.

- Officials from China, Japan and South Korea are pushing for quicker negotiation of a free-trade agreement between the three countries. Although not impacted evenly by global trade tensions, these Asian countries all have incentive to lock down an agreement promptly. “As the promoters of free trade, joint efforts to push forward to build a China-Japan-South Korea FTA … would also help to jointly resist the impact of turbulence in external markets,” said deputy director Yang Zhengwei of the Chinese Ministry of Commerce.

- Hong Kong and mainland China will now be even more connected thanks to an $11 billion train. The Guangzhou-Shenzhen-Hong Kong Express Rail opens on Sunday and will connect—even more tightly—the global financial and trade hub Hong Kong with the major southern Chinese cities of Guangzhou and Shenzhen. Travel time from the island to mainland will be cut in half and is part of an ongoing effort to foster more economic integration within the region. Government estimates show they expect 80,000 daily passengers.

Threats

- Trade war concerns remain an ongoing threat, although it remains a positive that, despite the latest round of rhetoric and perceived lack of progress toward resolutions of the U.S.-China spat, markets increasingly seem to be adjusting, as evidenced by the overall strength amongst some of the world’s largest major economies.

- On Thursday, Washington invoked new sanctions against the Chinese defense ministry’s Equipment Development Department (EDD) for purchasing surface-to-air missiles and fighter jets from Russia. The intent of such sanctions is to deter further arms purchases from Moscow, but analysts doubt if the Asian superpower will be impacted enough to alter its behavior. Last year, China was the third-largest purchaser of Russian weaponry, according to the Stockholm International Peace Research Institute, with around $859 million of arms deals. While China might not be deterred by these sanctions, Russia’s other clients may be more vulnerable to America’s pressure, especially if the Trump administration escalates further as a result of China’s refusal to change.

- Investor concern over any broad slowdowns or emerging market foreign exchange (FX) risks could continue to have outsized effects upon countries deemed to be at risk.

Emerging Europe

Strengths

- Turkey was the best performing country this week, gaining 3.4 percent. This week, the Turkish government released its medium-term plan, revising growth forecasts for 2018 and 2019 down to 3.8 percent and 2.3 percent, respectively. Finance Minister Berat Albayrak also announced a $10 billion spending cut in order to lower the budget deficit. The plan lacked details regarding how the government will help banks troubled by the collapsing lira and non-performing loan portfolios.

- The Russian ruble was the best relative performing currency this week, gaining 2.4 percent against the dollar. The ruble was supported by last’s week 25 basis points rate hike and higher oil prices. The central bank of Russia halted its weekly foreign currency purchases, which will most likely not restart before the end of the year.

- Information technology was the best performing sector among eastern European markets this week.

Weaknesses

- Hungary was the worst performing country this week, losing 1.3 percent. The European Union’s discussions about potentially imposing sanctions on Hungary continues to put pressure on equities.

- The Turkish lira was the worst performing currency this week, losing 1.9 percent against the dollar. Some investors lack confidence that government’s latest announced measures will support country’s falling currency and improve economic situation.

- Consumer discretion was the worst performing sector among eastern European markets this week.

Opportunities

- Despite the Trump Administration imposing tariffs on additional $200 billion of Chinese goods, equities trading around the world moved higher this week. Some investors believe that the tariffs and subsequent retaliation have already been priced in. According to CornerStome Macro Economic Research Team, a 10 percent tariff on $200 billion worth of goods, scheduled to go into effect next week, is worth 0.10 percent of U.S. gross domestic product. A tally of all U.S. and Chinese tariffs – both those currently imposed and those still under consideration – amounts to roughly 0.3 percent of Global GDP.

- Since the FTSE Russell and Deutsche Boerse AG’s STOXX upgraded Poland to “developed,” Polish equites will join the developed indices next week on September 24. That will likely boost interest in Polish stocks.

- The Five Star and the Laguge, two populist parties in Italy, have each asked for €9 billion to enable them to start implementing the economic programs promised before the elections. However, Italian Prime Minister Conte wants next year’s budget deficit to be lower than 2 percent of gross domestic product, keeping its spending plan in line with European budget rules. EU Economics Commissioner Moscovici highlighted that, in order for Italy to remain a credible country in the Eurozone, debt must be under control.

Threats

- Turkey’s financial crisis could affect European banks, especially those exposed to Turkish banking sector. The depreciating lira, which lost 25 percent it its value in August, makes it harder for debt holders to repay their foreign exchange (FX) loans. Corporates could start to default, raising the amount of non-performing loans for Turkish banks and their owners. Spain’s BBVA, Italy’s UniCredit, France’s BNP Paribas, Dutch bank ING and Britain’s HSBC are the most exposed to Turkey according to The Irish Times, making them vulnerable to its free-falling currency.

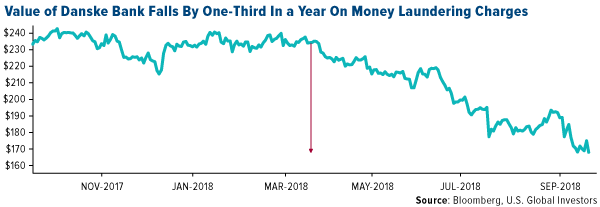

- Danske Bank CEO Thomas Borgen will resign on allegations that the bank was involved in money laundering through its Estonian unit, especially in Russia. The Wall Street Journal has reported that the United States is investigating the case, as many of the transactions were processes in dollars. The U.S. earlier this year accused Latvia’s ABLV of covering up money laundering. As a result, the bank was denied U.S. dollar funding, which led to its collapse.

- The U.S. added 33 Russian citizens to the federal government’s sanction list, which tracks defense and intelligence agencies connected to 2016 election interference. China entity Equipment Development Department and its director Li Shangfu were also subject to U.S. sanctions purchasing military equipment from Russia.

© US Global Investors

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All