NewsLetter September 2018

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsWHOOPS

Retirement isn’t the sort of thing you can just jump into. Rather, it requires thoughtful planning and a modest amount of basic knowledge. Unfortunately, Americans seem to be sorely lacking in this regard. GOBankingRates recently found that, shockingly, only 2 percent of respondents were able to pass a quiz on basic retirement knowledge.

SOBERING

From the Retirement Income Journal

If no action is taken, Social Security will be able to pay only 75 percent of its promised benefits after 2034. To solve that problem today, the government would have to raise payroll taxes (to about 15 percent from 12.4 percent), cut benefits across the board by 17 percent, or implement some combination of the two. It could also generate more revenue by raising the cap on the amount of earned income—currently the first $128,400—on which the payroll tax is levied.

FREE AT LAST!!

CBS News

After more than a century behind bars, the beasts on boxes of animal crackers are roaming free.

Mondelez International, the parent company of Nabisco, has redesigned the packaging of its Barnum’s Animal Crackers after relenting to pressure from People for the Ethical Treatment of Animals

A MUST-READ

If you’re remotely in striking distance of qualifying for Medicare, my partner, Josh Mungavin, has a most excellent reference book. You’ll note the attractive price—$0—as Josh prepared this amazing effort as a public service and simply wants to make it available to as many people as possible.

Click here to download it now.

THE FIGHT CONTINUES

Posse of top cops from 17 states dresses down SEC, demand same fiduciary standards for broker-dealers and RIAs and cite other ‘egregious’ deficiencies in proposed son of DOL rule

“… the state attorneys general’s remarks carry particular weight because of their regulatory powers and ability to sue the government if the rule falls short of its intended goals. Judging from their comments, they’re mad as hornets at the proposed measure.

The SEC’s proposed rule purports to impose a ‘best interest’ standard on broker-dealers while requiring additional disclosures; however, the proposed rule fails to require broker-dealers to act as fiduciaries for their clients, as is required of investment advisers—meaning retail investors are not assured unbiased advice from all their financial professionals,” the group asserted in a statement.

What’s more, “the proposed rule fails to ban even the most egregious of broker-dealer conflicts, like sales contests, which elevate the broker-dealer’s financial interest above that of the customer.”

Click here to read the full article.

OUCH!

Following up on the theme of retirement health care…

A Couple Retiring in 2018 Would Need an Estimated $280,000 to Cover Health Care Costs in Retirement, Fidelity® Analysis Shows

A 65-year-old couple retiring this year will need $280,0001 to cover health care and medical expenses throughout retirement, according to Fidelity Investments’ 16th annual retiree health care cost estimate. This represents a 2 percent increase from 2017 and a 75 percent increase from Fidelity’s first estimate in 2002 of $160,000.

For individuals retiring this year, using the same assumptions and life expectancies used to calculate the estimate for a 65-year-old couple, a male will need $133,000 to cover health care costs in retirement while females will need $147,000, primarily due to the fact that women are expected to live longer than men.

Click here for the full article.

OTHERS WITH TROUBLES

Luxury Apartment Sales Plummet in New Your City

Sales of such properties costing $5 million or more fell 31 percent in the first half of the year, pushing sellers to cut asking prices.

Click here for the full article.

SOME SURPRISES

At least for me … 10 Highest-Paid Professions in America

From Investment News

| Median base salary | |

| Software Architect | $105,329 |

| Nurse Practitioner | $106,962 |

| Software Engineering Manager | $107,479 |

| Physician Assistant | $108,761 |

| Software Development Manager | $108,879 |

| Corporate Counsel | $115,580 |

| Enterprise Architect | $115,944 |

| Pharmacist | $127,120 |

| Pharmacy Manager | $146,412 |

| Physician | $195,842 |

Click here for the full article.

RIGHT DIRECTION

Trends in Financial Advisor Compensation from WealthManagement.com

| 2004 | 2018 | |

| Fee Only | 31% | 52% |

| Commission Only | 21% | 3% |

| Combination | 10% | 28% |

NO COMMENT

For Online Daters, Women Peak at 18 While Men Peak at 50, Study Finds. Oy.

From the New York Times

WISE WORDS

- “The wise man, even when he holds his tongue, says more than the fool when he speaks.” Yiddish proverb

- “What you don’t see with your eyes, don’t invent with your mouth.” Yiddish proverb

- “A hero is someone who can keep his mouth shut when he is right.” Yiddish proverb

- “Don’t be so humble—you are not that great.” Golda Meir (1898-1978) to a visiting diplomat

- “Intellectuals solve problems; geniuses prevent them.” Albert Einstein

- “You can’t control the wind, but you can adjust your sails.” Yiddish proverb

- “I’m not afraid of dying—I just don’t want to be there when it happens!” Woody Allen

- “Not everything that counts can be counted, and not everything that can be counted counts.” Albert Einstein

- “Two things are infinite: the universe and human stupidity; and I’m not sure about the universe.” Albert Einstein

HOW LONG?

How long will $1 million last you in retirement? Report says it depends on the state

CNBC/USA Today

Mississippi: 25 years, 11 months, 30 days

Oklahoma: 24 years, 8 months, 24 days

Michigan: 24 years, 7 months, 14 days

Arkansas: 24 years, 7 months, 4 days

Alabama: 24 years, 7 months, 4 days

Hawaii: 11 years, 8 months, 20 days

California: 15 years, 5 months, 27 days

New York: 16 years, 3 months, 22 days

Alaska: 16 years, 8 months, 6 days

Maryland: 16 years, 8 months, 29 days

Click here for the full article.

TOO GOOD TO BE TRUE

From Financial Advisor magazine

Five Florida Brokers Sued By SEC In Alleged $1.2B Ponzi Scheme

Five unregistered Florida brokers are in hot water for funneling investors into a $1.2 billion Ponzi scheme. Woodbridge allegedly bilked 8,400 investors out of $1.2 billion in an elaborate Ponzi scheme in which high-pressure sales agents were used to prey on investors, who were told they would be repaid from high rates of interest on loans to third-party borrowers, the SEC said.

In reality, the borrowers were LLCs owned and controlled by Woodbridge’s leadership, according to the SEC, and investor funds were used to pay $64.5 million in commissions to sales agents … the five brokers were among the top revenue producers for Woodbridge, selling more than $243 million of its securities to more than 1,600 retail investors…

The SEC claims that the defendants told investors that the Woodbridge securities were “safe and secure” using various channels of communication. Klager pitched the investments via newspaper ads, while the Kornfelds allegedly solicited investments through seminars and a “conservative” retirement planning class taught via a Florida university and Costa recommended them on a radio program, the SEC said. Robbins allegedly used radio, television and internet marketing.

The moral is true: If it’s too good to be true, it’s not true.

HANDY TIP

From The Points Guy (@thepointsguy)

If you travel at all, I hope you have TSA PreCheck. If not, get it—it will save you tons of time and hassle at the security gate. What I didn’t realize is that if for some reason your known traveler number (KTN) doesn’t make it onto your reservation, your ticket may not reflect your qualification for PreCheck.

By streamlining security and cutting down on wait times, the program helps make travel a less stressful experience. However, it only does so when you actually use it, so we strongly encourage you to double-check your frequent flyer accounts and make sure your KTN is saved on your profile

Here’s how to do that for the major airlines in the US once you’ve logged into your account:

Alaska

- Visit Profile and tier status

- Click on Traveler profiles

- Click on Edit my information under International Travel Information

- Enter your KTN, then click Save

American

- Click on Your account

- Click on Information and password

- Enter your KTN, then click Save

Delta

- Click on Go to My Delta

- Click on View my profile

- Find Basic Info, then click Open

- Click Edit in the Secure Flight section

- Enter your KTN, then click Save Changes

JetBlue

- Click on the TrueBlue icon at the top right

- Click on Profile

- Click the pencil icon next to TSA PreCheck

- Enter your KTN, then click Yes, Update

Southwest

- Click on My Account

- Under My Preferences, click Edit

- Enter your KTN, then click Save

United

- Click on View account

- Under Profile, click on Edit Traveler Information

- Expand the KTN/Pass ID section, enter your KTN, then click Continue

AND ANOTHER HANDY TIP

From my partner Brett

Are you getting a lot of spam email? Instead of clicking “unsubscribe” at the bottom of the email, which tells companies your email is legit and then you get even more spam email, use the Rules feature in Outlook.

- Click on Rules, Create Rule

- Go to Advanced Options

- Click the checkbox that says “with “” in the subject or body” for Step 1

- Below that, under Step 2, click on the blue link and type in the company name or some unique identifier (be careful not use to a word like JPMorgan or anything else that could inadvertently filter out good emails)

- Click next and then click the checkbox “move a copy to a specified folder” for Step 1

- Below that, under Step 2, click on the blue link and select Junk email

- Click Finish

WORTH READING

Two most excellent articles from one of my favorite practitioner authors, Larry Swedroe, from Advisor Perspective via Bob Veres’ most excellent newsletter.

The Danger in Private Real Estate Investments

“Should clients invest in private deals as an alternative to publicly-traded REITs? Swedroe examines the evidence, in the form of a private investment database compiled by Cambridge Associates. It contains historical performance of more than 2,000 fund managers, more than 7,300 funds, and the gross performance of more than 79,000 investments underlying venture capital, growth equity, buyout, subordinated capital, and private equity energy funds.

The database shows that for the 25-year period ending in 2017, private funds returned 7.6% a year, on average, while comparable REITs returned 10.9%. The private investments were also taking on much more risk, in the form of leverage above 50% of the value of the underlying properties. One research report summarized more than a dozen academic studies across various time periods, and all of them reached the same conclusion: REITs outperformed private deals.”

The Problem with Focusing on Expense Ratios

“The evidence is clear that investors are waking up to the fact that, while the past performance of actively managed mutual funds has no value as a predictor of future performance, expense ratios do—lower-cost funds persistently outperform higher-cost ones in the same asset class.

That has led many to choose passive strategies, such as indexing, when implementing investment plans because passive funds tend to have lower expense ratios. Within the broad category of passive investment strategies, index funds and ETFs tend to have the lowest expenses.

Most investors believe that all passively managed funds in the same asset class are virtual substitutes for one another (meaning they hold securities with the same risk/return characteristics). The result is that, when choosing the specific fund to use, their sole focus is on its expense ratio. That can be a mistake for a wide variety of reasons. The first is that expense ratios are not a mutual fund’s only expense.”

THERE’S HOPE

From my friend Dianna

At age 23, Tina Fey was working at a YMCA.

At age 23, Oprah was fired from her first reporting job.

At age 24, Stephen King was working as a janitor and living in a trailer.

At age 27, Vincent Van Gogh failed as a missionary and decided to go to art school.

At age 28, J.K. Rowling was a suicidal single parent living on welfare.

At age 30, Harrison Ford was a carpenter.

At age 30, Martha Stewart was a stockbroker.

At age 37, Ang Lee was a stay-at-home-dad working odd jobs.

Julia Child released her first cookbook at age 39, and got her own cooking show at age 51.

Vera Wang failed to make the Olympic figure skating team, didn’t get the editor-in-chief position at Vogue, and designed her first dress at age 40.

Stan Lee didn’t release his first big comic book until he was 40.

Alan Rickman gave up his graphic design career to pursue acting at age 42.

Samuel L. Jackson didn’t get his first movie role until he was 46.

Morgan Freeman landed his first major movie role at age 52.

Kathryn Bigelow only reached international success when she made “The Hurt Locker” at age 57.

Grandma Moses didn’t begin her painting career until age 76.

Louise Bourgeois didn’t become a famous artist until she was 78.

Whatever your dream is, it is not too late to achieve it. You aren’t a failure because you haven’t found fame and fortune by the age of 21. Hell, it’s okay if you don’t even know what your dream is yet. Even if you’re flipping burgers, waiting tables, or answering phones today, you never know where you’ll end up tomorrow.

Never tell yourself you’re too old to make it.

Never tell yourself you missed your chance.

Never tell yourself that you aren’t good enough.

You can do it. Whatever it is.

FRAMING—80% FAT-FREE SOUNDS MUCH BETTER THAN 20% FAT

From Morningstar’s optimistic review of active manager performance: Active vs. Passive Fund Management: Our Research on Performance

80% Fat-Free

“4 takeaways about active vs. passive fund management from our year-end 2017 report

- S. stock pickers’ success rate increased sharply in 2017, as 43 percent of active managers categorized in one of the nine segments of the Morningstar Style BoxTMboth survived and outperformed their average passive peer. In 2016, just 26 percent of active managers achieved this feat.

- The turnaround was most pronounced among small-cap managers. In 2016, the combined success rate of active managers in the small blend, small growth, and small value categories was 29 percent. In 2017, 48 percent of small-cap managers outstripped their average index-tracking counterparts.

- Value managers saw some of the most meaningful increases in their short-term success rates. Active stock pickers in the large-, mid-, and small-cap value categories experienced year-over-year upticks in their trailing one-year success rates of 15.0, 20.2, and 34.2 percentage points, respectively. “

How I read these statistics:

20% Fat

57 percent of active managers underperformed their average passive peer.

52 percent of small-cap underperformed

For value managers, 85 percent of large-cap, 79.8 percent of mid-cap, and 65.8 percent of small-cap underperformed.

And that was the good news.

“Although 2017 marked a clear near-term improvement in active managers’ success rates, many of their long-term track records leave much to be desired. In general, actively managed funds have failed to survive and beat their benchmarks, especially over longer time horizons.

Click here for the full article.

HARD TO BELIEVE THIS IS REAL

Top Magician—Israel’s Got Talent

COSTCO, ANYONE?

18 Kirkland Products You Should Buy at Costco

Tips from Kiplinger

READ BETWEEN THE LINES

Before I start this “story,” I want to emphasize that I am NOTrecommending any of the investments discussed below and E&K has not and does not currently invest in any of them.

It’s a very popular theme today to critique mutual funds for being expensive closet indexers (and I agree) and to suggest that a far better solution is to search for managers who have a high “active share,” i.e., a high percentage of a portfolio that differs from the index (I’m a skeptic). What I teach my class is to be agnostic and do your own research. I recently came across a story about the Baron Fifth Avenue Growth Fund that seemed to make the case for such a manager.

The Art of High-Conviction Investing

Financial Advisor

For over seven years, the Baron Fifth Avenue Growth Fund was a fairly typical large-company growth vehicle with a diversified portfolio of over 100 stocks, lots of benchmark index companies, and so-so performance.

That changed pretty quickly when Alex Umansky, who had been a large-cap growth manager at Morgan Stanley for many years, assumed control in November 2011. Within a relatively short time he had whittled the fund down to fewer than 40 carefully chosen stocks and gave the best ideas ample room to run…

“The fund’s old portfolio was structured to guard against volatility,” says the 46-year-old Umansky. “I guard against over-diversification. If you have a portfolio of 100 names, you’re really just providing exposure to an asset class. We’re in the business of finding mispriced securities and adding alpha.”

MarketWatch also had a quite glowing story

Opinion: Baron Funds money manager goes all in to beat the stock market

Click here to read full article.

So I decided to look beyond the “story.”

Simply looking at a comparison of the fund performance to an appropriate investable index (iShares Russell 1000 Growth) since December 2011, when Mr. Umansky took over, didn’t seem to support the argument.

Next, I looked at what I consider to be the real test—risk-adjusted return. The basic measure for that is the Sharpe ratio, a number that according to Investopedia “ … is the average return earned in excess of the risk-free rate per unit of volatility or total risk.” What I found was that although Baron’s return did indeed beat the index by a percent or two, on a risk-adjusted basis, it lagged. Bottom line, Baron’s looks like a fine alternative if you’re looking for a mega large cap actively managed domestic stock fund, but iShares Russell 1000 Growth, at least today, looks a bit better. The moral: research and don’t just read—read between the lines.

WOULD BE A GOOD START

SEC Chairman Calls for End of Sales Contests

“As the SEC goes over the public comments it received on its proposed Regulation Best Interest and holds roundtables to hear from investors, the commission’s chairman says some of the feedback has ‘resonated’ with him, according to a statement published on the regulator’s website. Namely, Jay Clayton is adamantly opposed to ‘high-pressure, product-based sales contests’ and wants them eliminated entirely, he says in the statement.

‘In these circumstances, I do not believe it is possible for an investment professional to say with credibility that the investment professional is not putting his or her own interests ahead of the interests of the customer,’ he says, referring to the sales contests.”

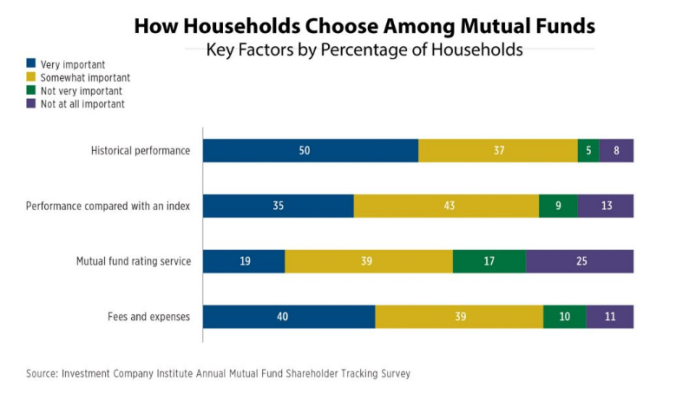

INTERESTING RESULTS

From the ICI Annual Mutual Fund Shareholder Tracking Survey as reported by ThinkAdvisor

Although 81 percent and 84 percent respectively reported a fund’s investment objective and risk profile were important considerations, only 36 percent said it was very important.

My ranking for Very Important would be:

- Investment Objective and Risk Profile

- Performance Compared to an Index

- Fees and Expenses (already included in the “performance”)

- Mutual Fund Rating Services wouldn’t even make the list

PUNCTUATION IS POWERFUL

From my friend Dianne on Facebook

An English professor wrote these words on the blackboard and asked his students to punctuate it correctly:

“A woman without her man is nothing”

All of the males wrote:

“A woman, without her man, is nothing.”

All the females in the class wrote:

“A woman: without her, man is nothing.”

Punctuation Is Powerful!

FOREWARNED IS FOREARMED

SEC Chairman Jay Clayton’s statement on Cryptocurrencies and Initial Coin Offerings

“The world’s social media platforms and financial markets are abuzz about cryptocurrencies and ‘initial coin offerings’ (ICOs). There are tales of fortunes made and dreamed to be made. We are hearing the familiar refrain, ‘this time is different.’

The cryptocurrency and ICO markets have grown rapidly. These markets are local, national and international and include an ever-broadening range of products and participants. They also present investors and other market participants with many questions, some new and some old (but in a new form), including, to list just a few:

- Is the product legal? Is it subject to regulation, including rules designed to protect investors? Does the product comply with those rules?

- Is the offering legal? Are those offering the product licensed to do so?

- Are the trading markets fair? Can prices on those markets be manipulated? Can I sell when I want to?

- Are there substantial risks of theft or loss, including from hacking?

The answers to these and other important questions often require an in-depth analysis, and the answers will differ depending on many factors. This statement provides my general views on the cryptocurrency and ICO markets and is directed principally to two groups:

- ‘Main Street’ investors, and

- Market professionals—including, for example, broker-dealers, investment advisers, exchanges, lawyers and accountants—whose actions impact Main Street investors.

Considerations for Main Street Investors

A number of concerns have been raised regarding the cryptocurrency and ICO markets, including that, as they are currently operating, there is substantially less investor protection than in our traditional securities markets, with correspondingly greater opportunities for fraud and manipulation.

Investors should understand that to date no initial coin offerings have been registered with the SEC. The SEC also has not to date approved for listing and trading any exchange-traded products (such as ETFs) holding cryptocurrencies or other assets related to cryptocurrencies. If any person today tells you otherwise, be especially wary.”

AND THEN THERE IS MARKET RISK

After the Bitcoin Boom: Hard Lessons for Cryptocurrency Investors

Tony Yoo, a financial analyst in Los Angeles, invested more than $100,000 of his savings last fall. At their lowest point, his holdings dropped almost 70 percent in value. Pete Roberts of Nottingham, England, was one of the many risk-takers who threw their savings into cryptocurrencies when prices were going through the roof last winter. Now, eight months later, the $23,000 he invested in several digital tokens is worth about $4,000, and he is clearheaded about what happened.

“I got too caught up in the fear of missing out and trying to make a quick buck,” he said last week. “The losses have pretty much left me financially ruined.”

Mr. Roberts, 28, has a lot of company. After the latest round of big price drops, many cryptocurrencies have given back all of the enormous gains they experienced last winter. The value of all outstanding digital tokens has fallen by about $600 billion, or 75 percent, since the peak in January, according to data from the website coinmarketcap.com.

HEADLINES

From my friend Peter. You can’t make this stuff up.

IT’S 100 DEGREES IN LUBBOCK BUT IT COULD BE WORSE

As one might expect, the desolate and remote East Antarctic Plateau is home to Earth’s coldest temperatures. What is surprising, however, is that these bitter temps are even colder than previously thought—reaching nearly -148 degrees Fahrenheit (-100 degrees Celsius).

I ALSO LOVE GETTING OLDER

From my friend Judy. Always a good source of interesting tidbits.

- My goal for 2018 was to lose 10 pounds. Only 15 to go!

- I ate salad for dinner. Mostly croutons and tomatoes. Really just one big round crouton covered with tomato sauce. And cheese. FINE, it was a pizza. I ate a pizza.

- I just did a week’s worth of cardio after walking into a spider web.

- I don’t mean to brag, but I finished my 14-day diet food in 3 hours and 20 minutes.

- A recent study has found women who carry a little extra weight live longer than men who mention it.

- Kids today don’t know how easy they have it. When I was young, I had to walk nine feet through shag carpet to change the TV channel.

- Just remember, once you’re over the hill you begin to pick up speed.

NOT SO HUMBLE

Harold Evensky to receive FPA’s highest award

AND

GOOD STUFF

From my friend Alex.

HOW OLD IS GRANDMA?

One evening, a grandson was talking to his grandmother about current events. The

grandson asked his grandmother what she thought about the shootings at schools,

the computer age, and just things in general.

The grandmother replied, “Well, let me think a minute.”

-

- I was born before:

- Television

- Penicillin

- Polio shots

- Frozen foods

- Xerox

- Contact lenses

- Frisbees

- The Pill

- There were no:

- Credit cards

- Laser beams

- Ballpoint pens

- Man had not yet invented:

- Pantyhose

- Air conditioners

- Dishwashers

- Clothes dryers (clothes were hung out to dry in the fresh air)

- Man hadn’t yet walked on the moon

- In my day:

- “Grass” was mowed

- “Coke” was a cold drink

- “Pot” was something your mother cooked in

- “Rock music” was your grandmother’s lullaby

- “Aids” were helpers in the principal’s office

- “Chip” meant a piece of wood

- “Hardware” was found in a hardware store

- “Software” wasn’t even a word.

- Until I was 25, I called every man older than me “sir.”

- And after I turned 25, I still called policemen and every man with a title “sir.”

- We were before gay rights, computer dating, dual careers, day care centers, and group therapy.

- Our lives were governed by good judgment and common sense.

- We were taught to know the difference between right and wrong and to stand up andtake responsibility for our actions.

- Serving your country was a privilege; living in this country was a bigger privilege.

- We thought fast-food was what people ate during Lent.

- I was born before:

- Draft dodgers were those who closed front doors as the evening breeze started.

- Time-sharing meant time the family spent together in the evenings and weekends, notpurchasing condominiums.

- We never heard of FM radios, tape decks, CDs, electric typewriters, yogurt, or guys wearing earrings.

- We listened to big bands, Jack Benny, and the president’s speeches on our radios.

- If you saw anything with “Made in Japan” on it, it was junk.

- The term “making out” referred to how you did on your school exam.

- Pizza Hut, McDonald’s, and instant coffee were unheard of.

- We had 5-and-10-cent stores where you could actually buy things for 5 and 10 cents.

- Ice cream cones, phone calls, rides on a streetcar, and a Pepsi were all a nickel. And if you didn’t want to splurge, you could spend your nickel on enough stamps tomail one letter and two postcards.

- You could buy a new Ford Coupe for $600, but who could afford one?Too bad, because gas was 11 cents a gallon.

- We volunteered to protect our precious country.

- No wonder people call us “old and confused” and say there is a generation gap.

How old do you think I am?

Are you ready?

This woman would only have to be 66 years old. All this is true for those of us born any time before late 1952. Gives you something to think about.

Depressing, as I’m lots older.

WHY WE NEED A FIDUCIARY STANDARD

Why Conflicting Retirement Advice is Crushing American Households

From Forbes

It is a well-documented fact that American workers are financially underprepared for retirement. For example, in a recent Government Accountability Office Report that examinedthe retirement savings of households in the 55 to 64 age group, researchers found that 55% of households had little to no retirement savings. Additionally, the remainder in that range that had saved for retirement saved a median of approximately $104,000. Even with Social Security, it seems the average American worker will have limited financial resources to generate income during retirement.

When you look at the savings data, this shortfall is not a surprise, as the U.S. consistently under-saves its peers. Data sourced from the Organization for Economic Co-operation and Development (OECD) spanning over a decade of savings rates ending in 2008 shows that the U.S. has historically come up short. Canada, France, Germany, Italy, Japan and the U.K. all reported generally better national savings rates during that time period. Although the retirement preparedness of the average American worker is distressingly bad and the savings trends and figures are of great concern, the focus of this article will be on the cost of conflicting advice on retirement preparedness.

The effects and financial impact of conflicting advice on American families is of consequence. In a 2015 report by the Council of Economic Advisers, the authors estimate that “the aggregate annual cost of conflicted advice is about $17 billion each year.” This conflicting advice comes from individuals and institutions that are “compensated through fees and commissions that depend on their clients’ actions. Such fee structures generate acute conflicts of interest.”

Unfortunately for the American family seeking “professional” financial advice, the choices are few. Just a small percentage of financial professionals are able to offer financial advice without facing the conflicts outlined by the Council of Economic Advisers. In a recent article (paywall) penned by Dr. Kent Smetters, he suggests that out of the roughly 285,000 financial advisers in the U.S., few are “fee-only advisers who follow a true fiduciary standard that prohibits commissions on products recommended to clients and legally requires the advisers to always put their clients’ interests first.”

It is challenging at best to determine which advisers, brokers, agents and mutual fund companies are able to act in your best interests as most say they will.

The effects and financial impact of conflicting advice on American families is of consequence. In a 2015 report by the Council of Economic Advisers, the authors estimate that “the aggregate annual cost of conflicted advice is about $17 billion each year.” This conflicting advice comes from individuals and institutions that are “compensated through fees and commissions that depend on their clients’ actions. Such fee structures generate acute conflicts of interest.”

WELLS FARGO PUSHED WEALTH ADVISORS TO USE HIGH-FEE PRODUCTS, CROSS-SELL

From Yahoo Finance

For almost two years, Wells Fargo has been under near-constant fire. It all began, of course, with the revelation that employees in bank branches, who faced immense pressure to sell, had opened fake accounts for customers. Then, the bank agreed to pay a $1 billion fine to settle allegations of abuses in its auto lending and mortgage businesses.

In the spring, the bank also disclosed that its board was conducting a review of “certain activities” within the bank’s wealth management unit, which filings describe as including fee calculations of fiduciary accounts.

In mid-July, Yahoo Finance reported on increasing sales pressure in the wealth management sector of Wells’ Private Bank. Late last month, the Wall Street Journal also reported that four Wells Fargo advisors had sent a letter to the Justice Department and the Securities and Exchange Commission, detailing “long-standing problems” in the wealth management business.

In addition, the Journal reported that the broad class of Wells Fargo advisors were encouraged to funnel wealthier clients into the Private Bank’s wealth management area because the fees were higher. A former senior executive in this area and multiple former Wells Fargo brokers expressed that to Yahoo Finance as well.

MERRILL LYNCH PAYS $8.9 MILLION TO SETTLE CONFLICT OF INTEREST CHARGES

From Financial Advisor

“Merrill Lynch’s equity research arm has agreed to pay approximately $8.9 million to settle Securities and Exchange Commission charges that it failed to disclose a conflict of interest to more than 1,500 of Merrill’s retail advisory accounts who were sold approximately $575 million in products as a result.

Investors continued to be sold the products managed by a U.S. subsidiary of a foreign multinational bank despite concerning management changes because of the fees the banks paid to be on Merrill’s advisory platforms and its broader financial relationship with the wirehouse, the SEC found.

‘By failing to disclose its own business interests in deciding whether certain products should remain available to investment advisory clients, Merrill Lynch deprived its clients of unbiased financial advice,’ said Marc P. Berger, director of the SEC’s New York Regional Office. ‘Retail clients must feel confident that their advisors are eliminating or disclosing such conflicts and fulfilling their fiduciary duties.’

Merrill’s decision to continuing offering the U.S. subsidiary’s products violated both its due diligence and disclosure policies and violated its own ADV requirements.

According to the order, Merrill put new investments into these products on hold due to pending management changes at the third party. As part of the decision, Merrill’s governance committee planned to vote on a recommendation to terminate the products and offer alternatives to investors.

The third-party manager sought to prevent termination by contacting senior Merrill executives, according to the order, including making an appeal to consider the companies’ broader business relationship.

Following those communications, and in a break from ordinary practices, the governance committee did not vote and chose instead to defer action on termination, the SEC found.”

If you’re in doubt regarding the legal relationship you have with an advisor, have them sign the simple mom-and-pop “fiduciary oath” (it doesn’t even have the word “fiduciary” in it). If you’d like a copy, call (305-448-8882) or send an email ([email protected]) and we’ll send you one.

Hope you enjoyed this issue, and I look forward to “seeing you” again in a couple months.

Harold Evensky

Chairman

Evensky & Katz / Foldes Financial Wealth Management

© Evensky & Katz / Foldes Financial Wealth Management

© Evensky & Katz / Foldes Financial Wealth Management

Read more commentaries by Evensky & Katz / Foldes Financial Wealth Management

Membership required

Membership is now required to use this feature. To learn more:

View Membership Benefits