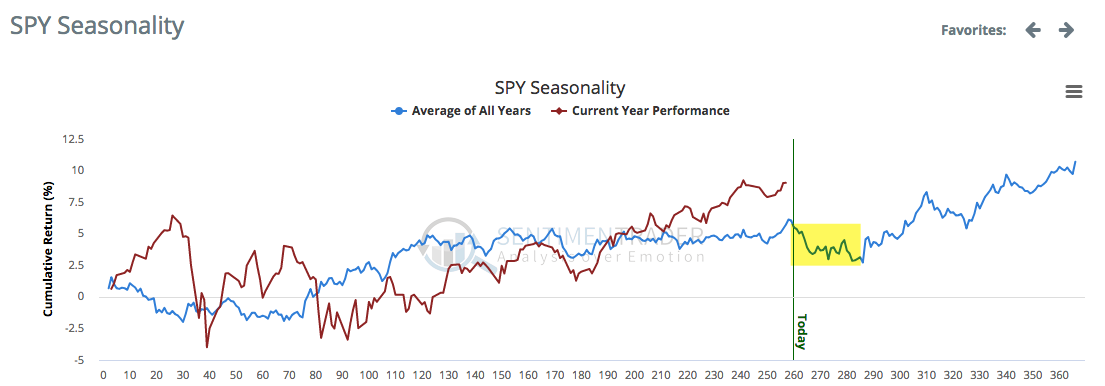

Summary: Mid-way through September, US equities are flat to lower for the month. The longer term trend is positive but the near-term outlook is unfavorable. It seems unlikely that any equity weakness will be substantial or long lived, but investors should remain on alert to heightened risk over the next several weeks. We believe that will be a good set up for gains into year end.

Mid-way through September, US equities are flat to lower for the month (table from alphatrends.net). Enlarge any chart by clicking on it.

Our perspective two weeks ago was that:

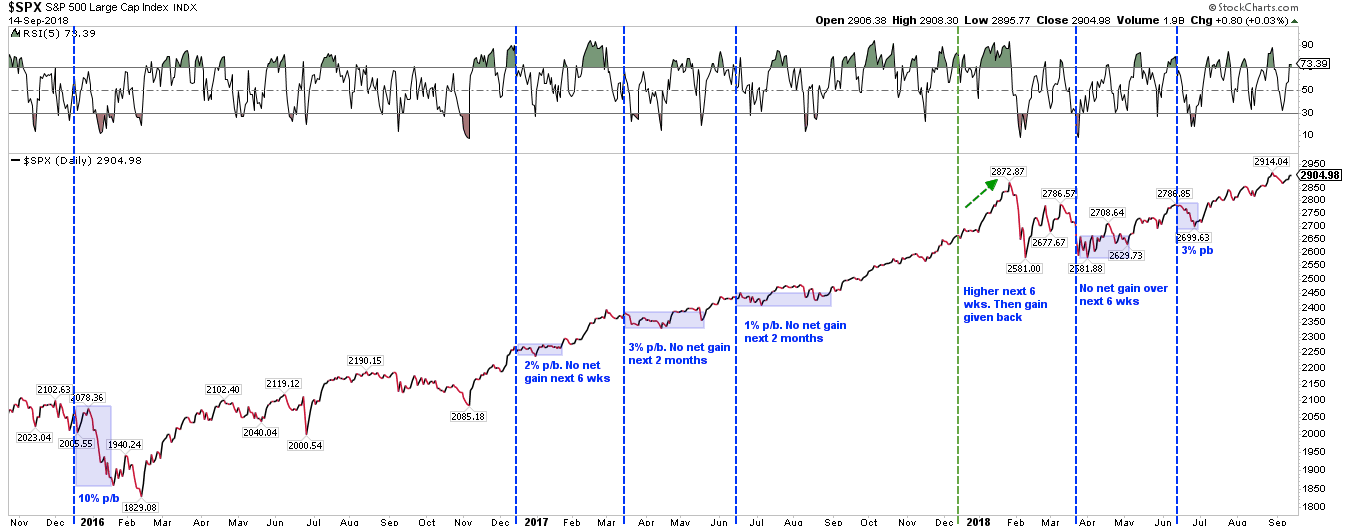

Years like 2018, where the SPX is up 5 months in a row and up between nearly 10% through August, have a strong propensity to continue higher to the end of the year. That view is supported by long term measures of sentiment and positive economic fundamentals

If there is a reason for caution, the risk is mostly short-term (within the next month). Strong Augusts have a propensity to trade lower in September, a view further supported by short-term measurements of complacency (like the put/call ratio)

That perspective has not changed. Data supporting this view can be found here.

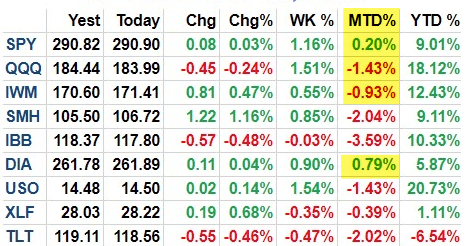

Among the major US indices, the Dow Industrials has been the weakest. SPX, the Nasdaq and both the Russell 2000 and 3000 have all made new all-time highs (ATH) in the past two weeks. DJIA has not yet exceeded its January high. But the pattern is constructive and last week DJIA traded to a new 8-month high (from IBD Investors; for a trial subscription, please use this link).