Weighing the Week Ahead: All About Jobs!

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsThere is a huge economic calendar in a holiday-shortened week. The mid-term elections impend, so politicians will be on the stump. With Labor Day setting the stage and the week loaded with key employment reports, expect plenty of attention to employment issues. Much of this will be confusing and unproductive spinning. Financial news pundits could provide a better focus by asking:

What investment opportunities are provided by the employment debate?

Last Week Recap

In my last edition of WTWA I expected plenty of discussion of the yield curve, with most asking the wrong question – would it invert? My analysis showed that the current yield curve action was better described as “compression” and had nothing to do with the strength of the economy. As expected, the determined economic and market bears ignored these arguments and presented the same tired charts showing yield curve inversions before recessions.

Yes! I agree, as does leading business cycle expert Bob Dieli, who has made the yield curve part of his model for decades. But he is more sophisticated in its application, which provides an advantage for those who really understand the fundamentals. The indicator is an indicator, not a cause! And as Bob stresses, we should not try to forecast the indicator.

It was a good theme for last week, especially illustrated by the upbeat economic news about the Mexico trade deal.

The Story in One Chart

I always start my personal review of the week by looking at a great chart. I especially like the version updated each week by Jill Mislinski. She includes a lot of valuable information in a single visual. The full post has even more charts and analysis, including commentary on volume. Check it out.

The market gained 0.93% on the week and has reached a new all-time high. The chart reflects variation, but the scale is one again a narrow one. The weekly trading range was about 1.3%, still very low. I summarize actual and implied volatility each week in our Indicator Snapshot section below. Volatility remains well below the long-term average.

Noteworthy

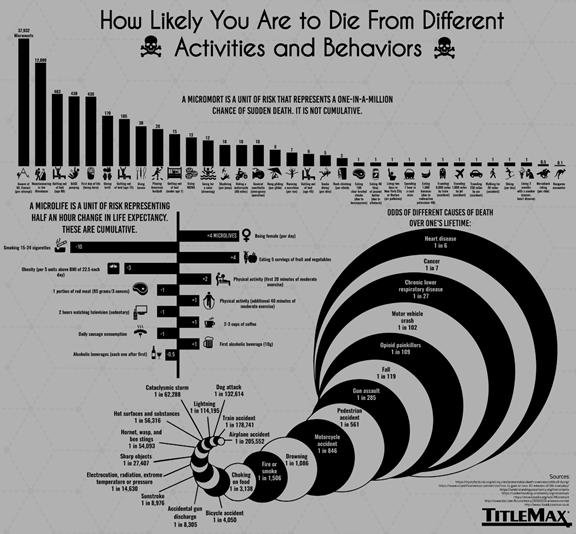

Have you ever heard of a micromort? Or a microlife? These measures help in comparing the various causes of death, in both frequency and magnitude. The entire article, from Visual Capitalist, also provides some links to perception versus reality in causes of death. This is yet another illustration of how newsworthy items create elevated perception of likelihood. One micromort corresponds to a one in a million chance of sudden death. Traveling 6000 miles by train or 230 miles by car reflect one micromort. Riding a motorcycle costs ten.

The News

Each week I break down events into good and bad. For our purposes, “good” has two components. The news must be market friendly and better than expectations. I avoid using my personal preferences in evaluating news – and you should, too!

When relevant, I include expectations (E) and the prior reading (P).

The Good

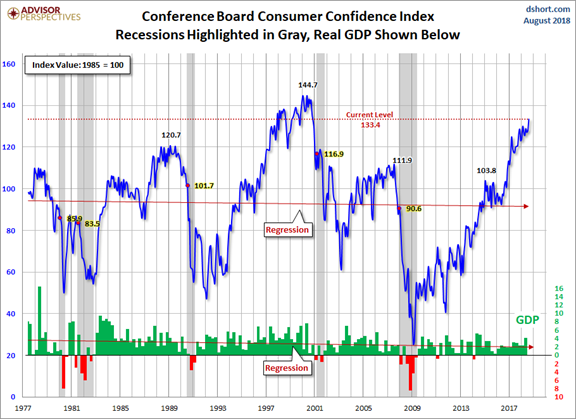

- Consumer confidence reaches new highs. The Conference Board version tabbed 133.4 (E 126.5 P 127.9). Michigan’s consumer sentiment was 96.2 (E 95.5 P 95.3). Jill Mislinski’s update notes that the Michigan version is a bit off the highs and cites comments from the Survey Director Richard Curtin on future conditions, which do not reflect concern about inflation.

- Q2 GDP edged higher in the second estimate, a gain of 4.2% E 4.1%.

- Company earnings calls remain positive — good growth, low inflation, and a sense that the bias may be even better. (Avondale).

- Chicago PMI registered 63.6 E 63.0 P 65.5. This has the greatest interest when coming out on a Friday, since some use it as a proxy for the ISM index. Friday’s report did not seem to have much impact.

- Trade agreement with Mexico is more likely. Markets reacted positively to the news despite the lack of specifics.

The Bad

- Trade negotiations with Canada and China showed little (if any) progress. (MarketWatch).

-

Long-term, high frequency indicators turn negative – again, reports New Deal Democrat. He reports that this is worth watching, but not an immediate recession indicator, suggesting the following criteria:

I will require two events before this translates into a “recession watch” for over 12 months later: (1) The weekly reports must remain negative consistently for at least one full month, and (2) they must be reflected in a reliable monthly measure where available.

- Pending home sales decreased 7% in July. Calculated Risk.

- Personal income increased only 0.3% (E 0.4% and P 0.4%). Personal spending was in line, as was the personal consumption price indicator. Brian Wesbury (First Trust) calls it a healthy start to the quarter, taking note of the 0.4% increase in wages and salaries.

-

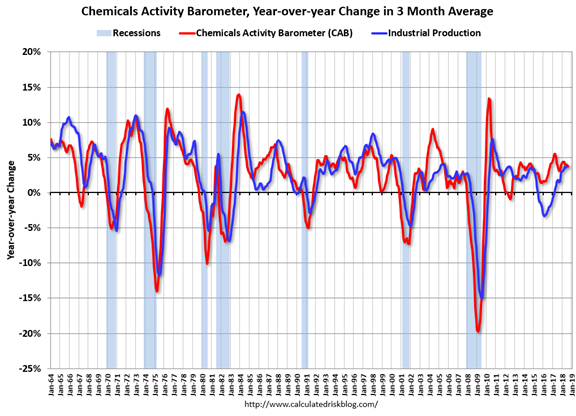

The Chemical Activities Barometer softens. Calculated Risk follows this indicator closely and suggests that it signals continuing growth at a slower pace.

The Ugly

Chicago incidents and a possible pattern. Here are three events from the last week.

- One community funds a mural by a well-known local street artist. Within a few days, someone complains that it is graffiti. It was then removed by the Department of Streets and Sanitation.

- A water treatment plant partially collapses after an explosion. Eight workers were injured, some seriously. Firefighters were at risk while conducting the rescue. The workers lit a torch while doing some repairs, igniting methane gas – a natural byproduct of the process. The workers were not using their mandatory test equipment.

- A terrible fire leads to the death of ten children in a residence. Later reports show that the building in question had a history including dozens of code violations, including smoke detectors and exits.

Obviously, these range widely in seriousness. To most people they may not seem related. To me, they are all situations that could have been avoided by the effective administration of existing public policy. In the time since the great recession there has been a significant reduction in government jobs at all levels. The consequences are difficult to determine – a few more students per teacher, fewer police for a district, fewer inspectors.

We all want lean and efficient government, but we also want the effective delivery of services.

The Week Ahead

We would all like to know the direction of the market in advance. Good luck with that! Second best is planning what to look for and how to react.

The Calendar

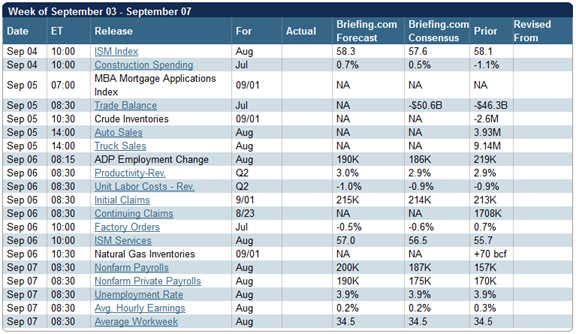

The calendar is loaded with news and the week is short. The ISM indexes and auto sales are important reads on the economy, but the focus will be employment news.

Briefing.com has a good U.S. economic calendar for the week (and many other good features which I monitor each day). Here are the main U.S. releases.

Next Week’s Theme

A holiday-shortened week is loaded with important economic news. Labor Day and associated political campaigning begin the week, while the employment situation ends it. While there is plenty of news in between, it may seem like the week is all about jobs.

Employment data provide many angles for analysis and even more opportunity to spin the conclusion. The result is both a challenge and an opportunity for investors.

The right question for this week is the following:

What investment opportunities are presented by the debate about jobs?

There will never be a perfect employment report. Even those described as “Goldilocks” or “just right” have disappointments on various criteria. There may be plenty of apparently good news, but there is also always something wrong.

Dimensions of Employment Analysis

- The size and pace of job growth. This might seem to provide a consensus for agreement. Wrong!

- Growth that is too fast will be criticized as a basis for Fed tightening;

- Should we expect the pace of growth to slow? (New Deal Democrat).

- Politicians can argue about the starting point for periods of growth;

- Different measures – payroll survey, population survey, ADP survey, non-seasonally adjusted data – often suggest differing conclusions. Survey sampling error is also different for each approach.

- The quality of jobs.

- Full-time or part-time. Are some forced to take part-time jobs? Or multiple part time jobs, perhaps not getting benefits.

- Wage growth, lagging through the current economic recovery. Have companies kept an excessive share of the economic expansion?

- Labor force participation. This is measured in terms of those seeking work, but that might not be sufficiently inclusive. (Steven Hansen, GEI).

- A possible shortage of workers. This is certainly true in some jobs (Western Farm Press) and might be related to changes in immigration policy.

- The analysis and collection process itself. Periodically critics complain that the BLS reports are subject to undue political influence, or even completely contrived.

This is not an exhaustive list, but it illustrates the breadth and depth of the challenge. Participants in the employment debate often have clear political motives – defending or attacking a record, or the implications of specific policies. Some have economic motives, with conclusions linked to their products or services.

In today’s Final Thought, I’ll provide some suggestions about untangling these arguments and finding some investment opportunities.

Quant Corner

We follow some regular featured sources and the best other quant news from the week.

Risk Analysis

I have a rule for my investment clients. Think first about your risk. Only then should you consider possible rewards. I monitor many quantitative reports and highlight the best methods in this weekly update.

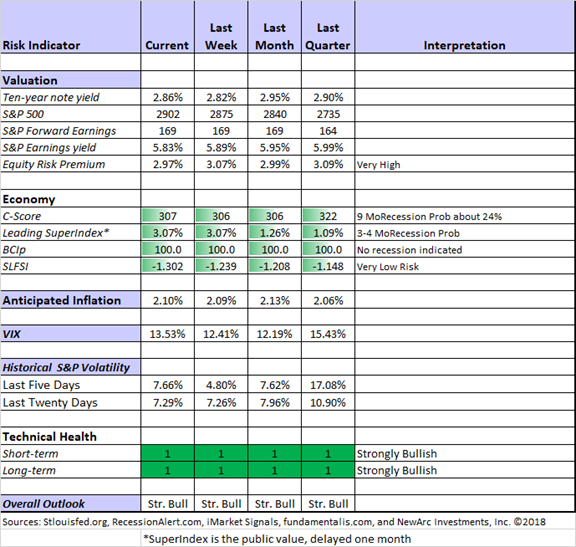

The Indicator Snapshot

Short-term trading conditions continue at highly favorable levels. Actual volatility remains very low. While many point to the low historical level of the VIX, it remains higher than realized volatility.

Some readers have requested a retrospective indicator snapshot from 2008. Others have suggested a standalone article as well. I will provide 2008, but this project is a bit bigger than I thought. Some of the key warnings came in 2007. My plan is a separate article with a couple of past time frames and then a regular link from WTWA.

The Featured Sources:

Bob Dieli: Business cycle analysis via the “C Score.

Brian Gilmartin: All things earnings, for the overall market as well as many individual companies.

RecessionAlert: Strong quantitative indicators for both economic and market analysis.

Doug Short and Jill Mislinski: Regular updating of an array of indicators. Great charts and analysis.

Georg Vrba: Business cycle indicator and market timing tools. None of Georg’s indicators signal recession. Here is the latest chart on the Business Cycle Index.

Guest Commentary

James Picerno reviews the data and several of the GDP nowcasts, concluding that “US Recession Risk is Low.”

Insight for Traders

Check out our weekly Stock Exchange post. We combine links to important posts about trading, themes of current interest, and ideas from our trading models. This week we discussed whether one can earn an income from trading. We provided educational advice on how to do it right, and one spectacular example of what happens when you do it wrong! As always, we provided some recent ideas from the trading models. Our ringleader and editor, Blue Harbinger, provided fundamental counterpoint for the models, who are all of the technical persuasion.

Insight for Investors

Investors should have a long-term horizon. They can often exploit trading volatility.

Best of the Week

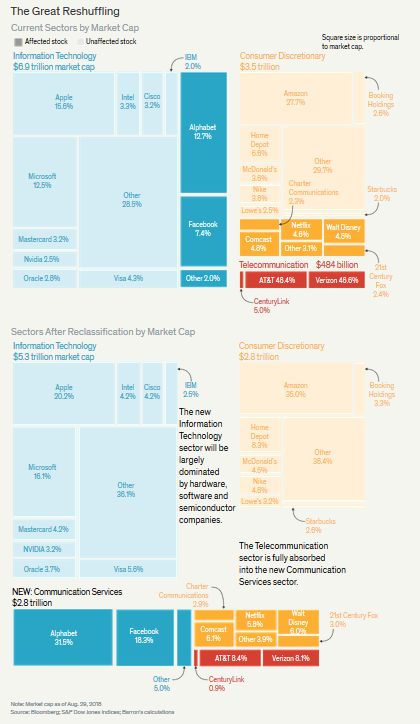

If I had to pick a single most important source for investors to read this week it would be the cover story and related articles from Barron’s, A Market Shakeup Is Pushing Alphabet and Facebook Out of the Tech Sector.

Daren Fonda’s article is interesting and informative in ways not typically seen in mainstream media. Many ETFs use sector classifications as the basis for their tracking. For starters, let’s look at this excellent graphical representation of what will happen.

With the shifts in mind, the challenge is clearly stated for the investor. We know that some funds will be selling stocks in some sectors and moving to others. Others will be changing allocations. Some other sector members will go along for the ride. Will AT&T (T) and Verizon (VZ) trade the same way when combined with Alphabet (GOOG) and Facebook (FB)?

The companion articles provide some ideas for your own analysis, but the answers are not easy.

Stock Ideas

Ten cheap, high-quality stocks with growing yields. (Morningstar). We own some of these and sell near-term calls against them.

How about the Nasdaq – not the index but the stock. Howard Lindzon makes an interesting case.

REITs are better choices when externally managed. (Brad Thomas).

A top, high-yield dividend aristocrat? The Dividend Sensei calls Exxon Mobil (XOM) one of the best.

Microsoft (MSFT) is at an attractive price point compared to other software stocks, says Peter F. Way.

Dale Roberts compares dividend aristocrats and non-aristocrats.

Trump trades?

The improved outlook for a US/Mexico trade deal helps a railroad which derived over 48% of Q2 revenue from Mexico. (Tomi Kilgore, MarketWatch and Avi Salzman, Barron’s).

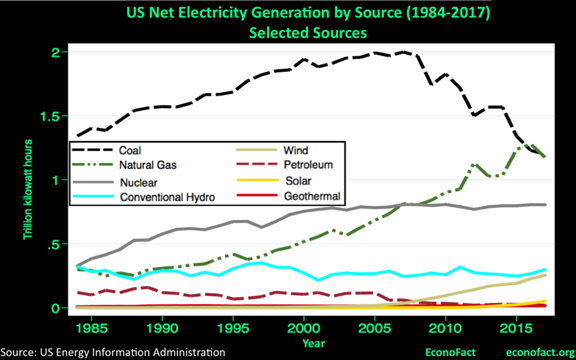

Improved outlook for coal and nuclear, based upon Trump administrations proposals to provide economic relief? Stefan Koester (Econofact) concludes that these policies will be “expensive and ineffectual.”

Outlook

Avi Gilburt notes the circularity of doom-and-gloom arguments linked to trade or impeachment.

The Math Investor provides a summary of doomster forecasts.

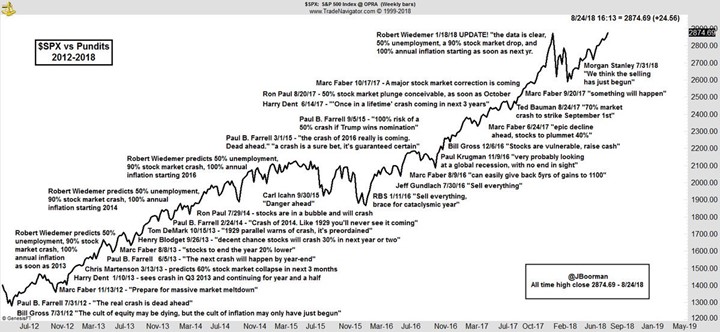

Jon Boorman of Broadsword Capital did a summary of past bearish calls that made the rounds in chart form. Shawn Langlois (MarketWatch) has a nice, balanced account, including the chart.

Personal Finance

Seeking Alpha Senior Editor Gil Weinreich’s Asset Allocation Daily considers a wide range of sources as well as his own take on an important issue. His posts are always interesting, but I especially liked his discussion about who is really managing your account. As we also did in our Stock Exchange installment this week, he notes the SEC decision against a big firm that relied on “an inexperienced, junior analyst.” Gil observes:

I have observed many times in the business world that the bigger, snazzier, slicker team beats out the leaner, meaner team. What’s always bothered me about this (having observed this from the vantage point of the smaller, losing team) is that some mid-level exec at the choosing firm ends up impressed with the brochures, PowerPoint presentations and meetings with the bigwigs, who then, after winning the contract, turn over the actual work to somebody just out of college, when the firm could have benefited from the gray eminences at the smaller firm.

This certainly resonates with me! My “marketing budget” consists of watching what the big firms advertise. I figure that their budgets allow them to find the most important avenues. One firm, for example, frequently advertised that you could “talk to Chuck.” My response was that he was tough to get on the line. It is very important that the real choices come from your advertised investment team.

Abnormal Returns is an important daily source for all of us following investment news. His Wednesday Personal Finance Post is especially helpful for individual investors. This week’s typical selection of great articles includes two important warnings.

- Watch out for brokers or advisors with questionable beliefs and dubious pasts. Josh Brown has some good examples of what not to do.

- Tony Isola explains why timeshares are the “variable annuities of real estate investing.”

Watch out for…

Walmart. Jae Jun has an interesting value perspective combined with some personal information about being a supplier for the company.

Restoration Hardware (RH). Morningstar’s Jaime M. Katz does a thorough job on recent strategic changes, the housing market, company financials, and technical considerations. Overall? A normalized rate of growth, higher expenses, and lower operating margins. This is a good example for readers who want to see what is included in a professional report.

Final Thoughts

Getting the most from employment data begins with some knowledge of how to interpret results.

- All the results, even when the underlying methods are sound, have a margin of error from the survey samples. Revised versions do not “fix” sampling error.

- Interpretation should be based upon trends and multiple data points, not a single release.

- The analysis is performed by experienced, non-partisan career professionals.

Next, we must see the probable political biases.

- Those committed to stronger limits on immigration are unlikely to acknowledge labor shortages.

- When job growth is solid, those out of power are left to criticize the quality of the jobs. Of this means looking at a single report, not trends.

- When unemployment seems to be low, critics will cite “discouraged” workers. This concept is defined as one of the unemployment measures, but some extend it to include grandma!

- If wage growth versus profit growth is the question, expect those backing corporate tax reductions to argue that both will be helped.

These examples are natural, normal, and not a feature of a specific political party. It is more a question of “ins” versus “outs” than one party versus another.

Investment Implications

Here are some ideas to illustrate. Please add your own in the comments.

- Criticism of the employment situation contributes to a near-perpetual skepticism about the strength of the economy. If your analysis of multi-month trends shows strength, use the information to select stocks and sectors that will reflect this growth.

- Suppose you believe that inequality is a key public policy issue and that slow wage growth is one of the causes. You might believe that corporate profits reflect some unfair advantages. As an investor, you should still buy the stocks of companies with strong pricing power and good profit margins. Do not allow your personal opinions to be a factor. If you cannot do this, you should buy a mutual fund and pay no attention to what the manager buys!

- Suppose you believe that homebuilders or farmers face higher costs because of a shortage of workers. You should use your opinions in voting or talking politics with your friends. As an investor, find choices that benefit from higher home or food prices.

In the week ahead, expect the employment debate to provide some good investment opportunities.

Untangling politics and economics in search of investments is both challenging and fruitful.

I’m more worried about:

- Polarizing issues in the mid-term elections. Disagreement about policy is essential. Continuing confidence in the US economy is important for continuing growth. Loss of confidence is a vicious circle.

I’m less worried about:

- Impeachment issues. There was plenty of news, and the market took it in stride. I don’t expect any serious discussion until after the mid-term elections. Barry Ritholtz notes that when it comes to impeachment, Markets Don’t Care.

Membership required

Membership is now required to use this feature. To learn more:

View Membership Benefits