Weighing the Week Ahead: Should Investors Worry about the Yield Curve?

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsLast Week Recap

In my last edition of WTWA I previewed the annual Fed Jackson Hole symposium. I provided the material for your own party bingo card on what to expect from the punditry. Many of the suggestions were covered early in the week and all of them by Friday. I noted that many would leave after the release of Powell’s speech. The chart for the week (below), shows a flat line for the rest of the day.

Finally, and most importantly, the news continues to be framed in terms of when the bull market will end and what will cause it. How different it would be if experts were asked about the key market drivers and whether they were still working. As always, Alan Steel’s commentary is clever, humorous, and accurate. Here is a tidbit:

Some two-thirds remain neutral to bearish by the American Association of Individual Investors’ (AAII) reckoning – unwilling to leave the March 2009 dour sentiment party gathering of anoraks, recessionistas, safety-seekers and economists (does that spell ‘arse’?).

Millions stand steadfast in that nine-year-long line, taking in turn their opportunity to swing the Trump, Turkey and trade war baton at the stock market pinata; a torn and battered beast yet stuffed and sturdied with stable economic indicators despite the unyielding headline assaults.

The Fear and Greed Trader also notes the deceptive framing of issues:

Not a week goes by when someone doesn’t appear and make one or both of these comments. “We are late in the cycle” and “stocks are expensive”. The statements are made as a matter of fact and no one seems to challenge them.

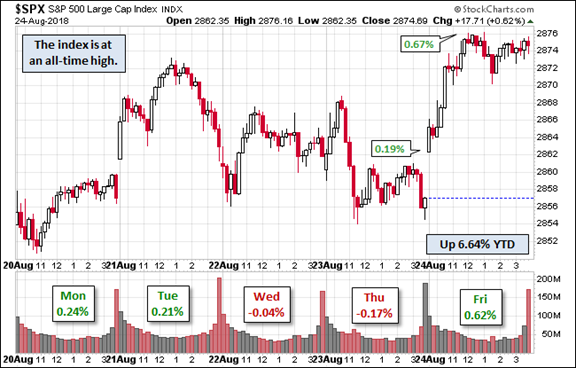

The Story in One Chart

I always start my personal review of the week by looking at a great chart. I especially like the version updated each week by Jill Mislinski. She includes a lot of valuable information in a single visual. The full post has even more charts and analysis, including commentary on volume. Check it out.

The market gained 0.88% on the week and has reached a new all-time high. The chart reflects variation, but the scale is one again a narrow one. The weekly trading range was less than 1%. I summarize actual and implied volatility each week in our Indicator Snapshot section below. Volatility remains well below the long-term range.

The News

Each week I break down events into good and bad. For our purposes, “good” has two components. The news must be market friendly and better than expectations. I avoid using my personal preferences in evaluating news – and you should, too!

When relevant, I include expectations (E) and the prior reading (P).

The Good

- FOMC minutes and Powell’s speech. The market seems comfortable with the planned, gradual pace of rate hikes.

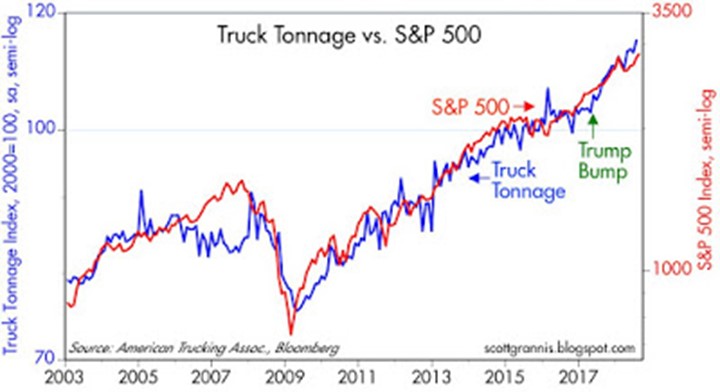

- Trucking growth continues. Steven Hansen (GEI) follows this with a special emphasis on the CASS index rather than the ATA data. Scott Grannis agrees, calling it one of the most bullish charts in his inventory.

- Initial jobless claims for the week were only 210K. E 217K P 212K. (Bespoke)

- Earnings estimates move higher. Some of the punditry have noted that estimates are not following the normal declining path at this point in the year. Brian Gilmartin analyzes the data objectively, suggesting a note of caution.

- Mortgage delinquencies decline to the lowest levels since March 2006. (Calculated Risk).

- New Deal Democrat’s long leader indicators have returned to neutral. The “nowcast” and short-leading forecasts remain quite positive.

The Bad

- Durable goods orders declined 1.7%. E -0.6% P 0.7% (revised down from 1.0%). Steven Hansen (GEI) analyzes the data, emphasizing the need to do some smoothing. The results are still encouraging with a three-month rolling average.

- New home sales reached a 9-month low. Existing home sales are at a two-year low. New Deal Democrat has charts and analysis. Avondale, monitoring earnings calls, notes a housing warning from Redfin about homes getting tougher to sell. Calculated Risk notes that sales are up 7.2% through July when compared to last year. As the comparisons get more difficult in the next few months, the growth may be tougher to maintain. Bill notes that builders need to offer some smaller, less expensive homes if the gap from distressed sales is to be closed. This is a good historical look.

The Ugly

Ebola, again. Exacerbated by conflict among the bordering nations. (Washington Post).

And Hawaii, with Hurricane Lane and flooding.

The Week Ahead

We would all like to know the direction of the market in advance. Good luck with that! Second best is planning what to look for and how to react.

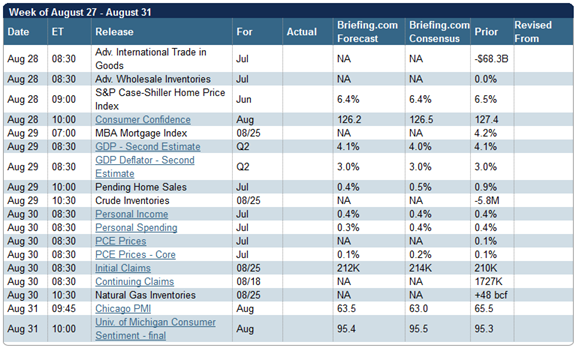

The Calendar

The calendar is a modest one and many are on vacation. We can once again expect early departures as market participants plan to extend their Labor Day weekend. The calendar features personal income and spending and the Fed’s favorite inflation measure, PCE prices. We will also get updates on both the Conference Board and University of Michigan sentiment indicators.

Briefing.com has a good U.S. economic calendar for the week (and many other good features which I monitor each day). Here are the main U.S. releases.

Next Week’s Theme

Another slow week opens the door for plenty of political news. These stories have come to dominant financial press and TV whether there is a market implication or not.

Sticking with my announced plan, I will continue to use WTWA to focus on important issues. In the quest for new worries, the most recent hot topic is the yield curve. This formerly arcane and nerdy subject is now the buzz almost everywhere. Even those who had never heard of this concept a few months ago are now self-proclaimed experts! The average investor is urged to worry about a yield curve inversion, since that will mean a recession. Anticipating the inversion arrival is a daily accounting of the flattening of the curve and the implied slowing of the economy.

When you begin with the wrong question, you are far less likely to get the right answer. A better framing of the issue is the following:

Should investors worry about the yield curve?

In a departure from custom, I will analyze the topic in this section, rather than putting it all in the final thought. I’ll look first at what people are saying, next at why they are saying it, what investors should really be thinking, and a final snapshot of the current situation.

Current Commentary

The bull market is long in the tooth and so is the economic cycle. Nicely analyzed by Cullen Roche: “…we are masters at creating interesting sounding narratives based on statistics that are mostly meaningless.” And Morningstar cites various sources suggesting that there may be several years left – with few signals of an end.

Is there a declining “margin of safety” in the yield curve spread? (The Capital Spectator). And will it force a change in Fed policy?

Will the Fed invert the curve? Leading Fed expert Tim Duy analyzes commentary from Atlanta Federal Reserve President Raphael Bostic, who says he will fight this.

The flattening curve signals slowing growth. Wrong, says Tim Duy.

An inversion is coming, and the Fed will speed it along.

Motives

I invite readers to take a closer look at any source exaggerating the yield curve story. You will probably find someone from the following list:

- Those selling bonds.

- Those selling “structured products.”

- Those selling annuities.

- Those selling real estate.

- Those selling gold, silver, or bitcoin.

- Those selling page views or ratings.

Larry Swedroe has a nice article on this topic. Readers occasionally suggest that pushing back on these themes implies that you are selling stocks. That is certainly true of some representatives of equity funds. What do you expect to hear from the manager of a small cap fund, an emerging market fund, etc.?

This bias is less likely for independent investment advisors (like me) with a fiduciary role and a willingness to work with assets of all types.

A Simple Lesson in Yield Curve Inversion

The yield curve compares interest rates for a short-term instrument with one of a longer term. While various comparisons could be used, the 2-year and 10-year notes are a common choice. Normally, longer terms command higher rates, so the curve slopes upward.

The Fed controls the short end of the market. This directly relates to Fed Funds but is highly influential on the two-year.

Long-term rates reflect several factors:

- The compounding of short-term rates, referred to as the term structure.

- Expectations for inflation.

- Supply and demand for the underlying instruments

- During QE the Fed acquired debt in this range, adding to demand and lowering rates. The best estimate of the total QE impact is about 1% on the ten-year. This can only be estimated through modeling, since there is no “counterfactual.”

- Arbitrage with debt from other countries. This is often ignored, but it has been a major factor. Investors are used to US debt being the “funding currency” for a carry trade. The arbitrageur borrows in the funding currency and buys higher yielding instruments. This can be a leveraged trade and involves currency risk. (Burton Malkiel, WSJ). The big recent change is that US rates are higher than those in Europe. That means that the arb involves borrowing in Europe and investing in the US.

- Informal arbitrage, as foreign investors prefer the dollar and the yield in the US.

The relationships provide a challenge in causal modeling. Higher long-term rates frequently reflect inflation and stronger economic growth. Short-term rates, especially when out of the accommodative range, reflect Fed concerns about an overheating economy and incipient inflation. The yield curve inverts when the Fed quashes inflation fears and effectively puts the brakes on the economy.

Right Now?

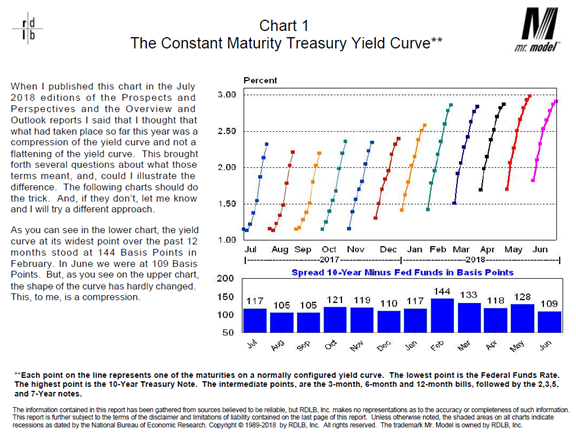

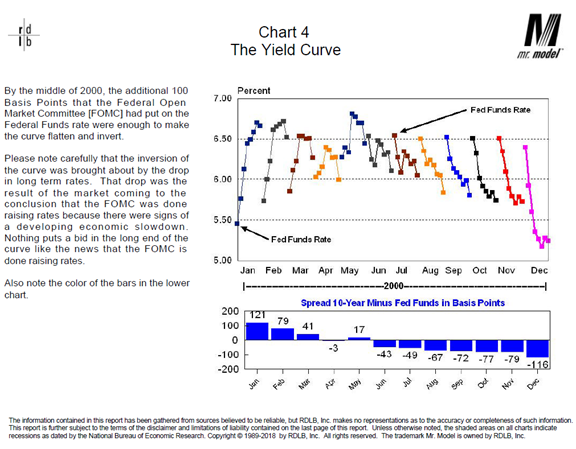

The long end of the curve does not reflect weak growth; the data show the opposite. The Fed is not worried about inflation. Dr. Robert Dieli who has decades of experience on this topic emphasizes a pattern where the Fed stops increasing rates and the long end of the curve declines. His business cycle forecasting includes (now and always) a measure of the economy as well as the yield comparison. He also employs plenty of confirming data in his monthly analysis of this topic.

Bob describes current trading as a “compression” not necessarily the start of an inversion. Here is his look at the current picture, with a chart you have probably never seen before. The yield spread is the length of the various lines while inversion comes from the shape.

And here is an example of the time surrounding the 2001 recession:

Bob’s subscribers have his full report covering several past recessions.

I have some additional personal observations in today’s Final Thought.

Quant Corner

We follow some regular featured sources and the best other quant news from the week.

Risk Analysis

I have a rule for my investment clients. Think first about your risk. Only then should you consider possible rewards. I monitor many quantitative reports and highlight the best methods in this weekly update.

The Indicator Snapshot

Short-term trading conditions continue at highly favorable levels. Actual volatility has moved even lower. While many point to the low historical level of the VIX, it remains higher than realized volatility.

Some readers have requested a retrospective indicator snapshot from 2008. Others have suggested a standalone article as well. I will provide 2008, but this project is a bit bigger than I thought. Some of the key warnings came in 2007. My plan is a separate article with a couple of past time frames and then a regular link from WTWA.

The Featured Sources:

Bob Dieli: Business cycle analysis via the “C Score.

Brian Gilmartin: All things earnings, for the overall market as well as many individual companies.

RecessionAlert: Strong quantitative indicators for both economic and market analysis.

Doug Short and Jill Mislinski: Regular updating of an array of indicators. Great charts and analysis.

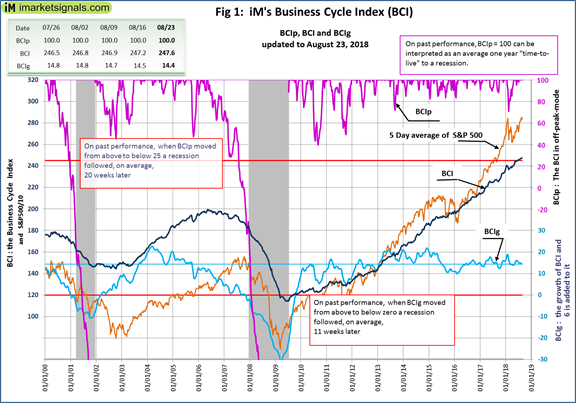

Georg Vrba: Business cycle indicator and market timing tools. None of Georg’s indicators signal recession. Here is the latest chart on the Business Cycle Index.

Insight for Traders

Check out our weekly Stock Exchange post. We combine links to important posts about trading, themes of current interest, and ideas from our trading models. This week we discussed the issues involved in trading news flows. It was another good question for traders, and we incorporated the expected expert commentary along with some examples. Our ringleader and editor, Blue Harbinger, took up one of the week’s picks, Tesla (TSLA) for a more detailed discussion. We provide picks as examples and a starting point for your own research, not expecting people to follow. We make many trades and cannot always cover the exits. That said, I want to report that we have sold our TSLA position. Felix highlighted the S&P 500 and Oscar ranked the high-liquidity ETFs.

Insight for Investors

Investors should have a long-term horizon. They can often exploit trading volatility.

Best of the Week

If I had to pick a single most important source for investors to read this week it would be The Bull Market Can Run for Years, by Shareholders Unite. From his perspective in the Netherlands, the experienced academic author is somewhat insulated from the “liberal versus conservative” economics. While originally skeptical of the impact of the Trump tax cuts, he is carefully watching data on a positive increase in business investment and productivity.

There are several good lessons from this post:

- Don’t get caught up in politics when doing your economic and investment analysis;

- Be willing to change your mind when you see new data;

- Use your analytical skill to ferret out what is most important – business investment in this case;

- Take a realistic look at the related economic factors;

- Let your conclusions reflect the wider range of possible outcomes.

Stock Ideas

Interested in China? Chuck Carnevale finds seven stocks with high growth and a reasonable price.

Altria (MO). A “dividend growth machine trading at a discount” says Colorado Wealth Management.

Bet you haven’t tried this comparison: Ollie’s (OLLI) versus Amazon (AMZN). Peter F. Way’s unique analytical method shows that the big real-money players are more worried about taking short positions in…?

Looking for a rebound? Marc Gerstein analyzes American Axle (AXL). GM changes hurt, but China and Europe are supporting growth

Personal Finance

Seeking Alpha Senior Editor Gil Weinreich’s Asset Allocation Daily considers a wide range of sources as well as his own take on an important issue. It is interesting to financial advisors as well as the DIY investor. This week he highlights possible retirement disaster scenarios. This week he hits on our theme of the extended bull market, considering some pluses and minuses. He highlights John M. Mason, who takes up the extended troubles of the “bond king,” Bill Gross. This is a history worth reading.

There is discussion of the choices involved in two posts this week he considers the trade-offs in purchasing an annuity or long-term care insurance. Read the entire series for more great discussions.

Abnormal Returns is an important daily source for all of us following investment news. His Wednesday Personal Finance Post is especially helpful for individual investors. This week’s typical selection of great articles included several good posts on retirement. The post from Pete the Planner covers a topic important to many – how couples should take Social Security to receive maximum benefits.

Watch out for…

Yield traps. Morningstar analyzes FTSE 100 candidates yielding over 4%, but the conclusions and reasoning are relevant for all yield seekers. Watch out for high concentrations in popular stocks along with a low dividend cover ratio.

Lowe’s (LOW). Stone Fox Capital suggests that you “wait for a summer clearance.” This is an interesting analysis of the duopoly in this sector. They also warn about Novavax (NVAX) – making progress but needing a partner.

Exact Sciences? (EXAS) Kirk Spano has been long and right about this company, willing to take on noted short-seller Citron Research. While not bearish on the stock, he feels the easy money has been made. Investors might join him in selling (or avoiding) the stock at the high end of the range. There may yet be another opportunity here.

Final Thoughts

This week’s post has been a challenge. It is an important topic, frequently discussed, but is quite technical. The recommended conclusion is deceptively simple. The problem is to simply a tough question without making the answer simplistic. I can hardly believe how poor the commentary is on this one – and my expectations are generally low.

Saying that the Fed might start a recession by inverting the yield curve is like saying that you can warm up a cold day by holding a match under your thermometer!

The yield curve is not a cause of recessions. It is an indicator that sometimes reflects other causal factors.

Compare the knowledge needed to understand this topic with what the average person knows (Visual Capitalist).

The result is an opportunity for the intelligent WTWA reader: Take the opposite side of the “public” trade. With everyone worried about an incipient recession you can enjoy gains from cyclical names like (non-FANG) technology, financials, construction, energy, and discretionary consumer names. These are all currently undervalued when compared to the FANG and yield-chaser names. This is not a short-term trade. It can profit for years before this cycle actually ends.

[Overloaded in expensive names? Can’t find cheap stocks? This is a crucial time for investment decisions. If you are flying solo, you might want to request my papers on risk or the top pitfalls for individual investors. If you are concerned that you do not have a good risk/reward portfolio, or one suited to your needs, feel free to ask us for an analysis. For any of these just email main at newarc dot com].

I’m more worried about:

- Impeachment turmoil. This is a repeat from last week. There was plenty of push back from those suggesting that conditions were unlike past such controversies. Nonetheless, it has become more likely and represents a disruption. Eddy Elfenbein has a clear-headed assessment.

- North Korea. It is difficult to quantify the investment effect. A reader asked why I even bother to classify this, but I am trying to highlight what is on my radar. The scheduled conference has been canceled in the face of lack of progress on denuclearization.

I’m less worried about:

- North American trade. There seems to be some real progress. This is the most important of the trade matters.

Membership required

Membership is now required to use this feature. To learn more:

View Membership Benefits