The economic calendar is light, and many are already on vacation. Even actual economic news has not competed with the ‘what can we talk about on a slow Friday’ story over the last few weeks. The real news this week begins with the FOMC minutes on Wednesday and ends with Chairman Powell’s speech Friday morning. Many traders would prefer a two-day week! It might seem like that. Expect the punditry to be asking:

Will there be a message from Jackson Hole?

Last Week Recap

In my last edition of WTWA I warned that there were many efforts to hijack the financial news agenda – and your ears and eyeballs along the way! In particular, I barely mentioned the Turkey non-story, which I described as a headline lacking substance. Just as I suspected, Turkey was the focal point of every market blip – but only for a few hours. What would be the “contagion?” intoned some newly-created Turkey experts, who looked up a few facts in an almanac. I was prepared to write the entire summary (before I put “mute” back on) but Bill Kort did such a clever and humorous version, we should just read his post. He recounts the various media flashes and stories. Here is an example:

Contagion is a favorite word the media uses when brewing up a crisis in your mind. Yes, there could be other countries that could be swept up in the current frenzy over Turkey’s finances. This, too, would not be the end of the world. Since this run in stocks began over 9 years ago (the S&P 500 has almost quadrupled) there have been multiple potential contagion stories – Greece (2 or 3 times), the PIIGS (Portugal, Ireland, Italy, Greece and Spain) and Cyprus. CNBC even takes this into account in the headline for an August 13, post– ‘What happens in Turkey won’t stay in Turkey’: Why this debt crisis could be different. They just won’t let this story go. Here is another post from this AM – “Charts of past currency crises show Turkey may have a lot more pain to face.”

This is exactly why I warned people not to fall victim to those framing the news. Usually I focus on what to watch. Last week it was about what to ignore.

Warning: This paragraph contains some optional OldProf humor, not approved by Mrs. OldProf. Feel free to skip to the next section. Somehow it seemed like a good example. I need to have a little fun while writing, so please provide a little slack.

Yes, the idea was sparked by Turkey. In this case we were going to consume turkey at a family gathering in Wisconsin. Mrs. OldProf is an excellent cook, but she had the ‘help’ of her two sisters. From my writing corner, I noted a disagreement among the sisters – never good, and not something that invites more participants. With a vested interest in dinner, I discerned that there was disagreement about thawing, cooking times, and turkey weight. The disparate views seemed extreme to a non-expert like me. I have expertise, but it is specialized in recognizing and enjoying a great turkey dinner.

Here is the strange point of connection with last week’s market, which merely happened to involve Turkey. Decades ago I realized that I could never be an expert at everything. By learning how to learn I could become expert at finding experts. When someone comes on CNBC or has a print article, I check out their background, references, possible policy biases. All “experts” are not equal, and some are purely imposters. This week we will see the Turkey experts remove the Groucho masks and become Fed experts.

But back to dinner. I dialed a number on my phone. When it was answered, I handed it to the nearest sister. She heard, “Butterball hotline. May I help you?”

I will never know whether my efforts made any difference to the cooking time decision, but dinner was delicious.

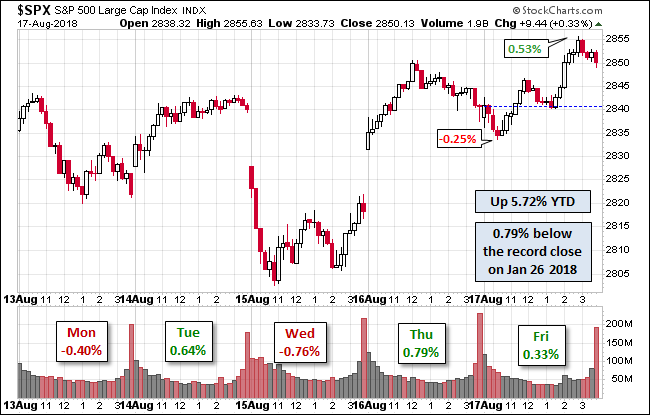

The Story in One Chart

I always start my personal review of the week by looking at a great chart. I especially like the version updated each week by Jill Mislinski.She includes a lot of valuable information in a single visual. The full post has even more charts and analysis, including commentary on volume. Check it out.

The market gained 0.59% on the week and is less than one percent from the all-time highs. The chart reflects opening gaps from news events while US markets were closed. The range for the week was about 1.9%. I summarize actual and implied volatility each week in our Indicator Snapshot section below. Volatility remains well below the long-term range.

The News

Each week I break down events into good and bad. For our purposes, “good” has two components. The news must be market friendly and better than expectations. I avoid using my personal preferences in evaluating news – and you should, too!

When relevant, I include expectations (E) and the prior reading (P).

The Good

-

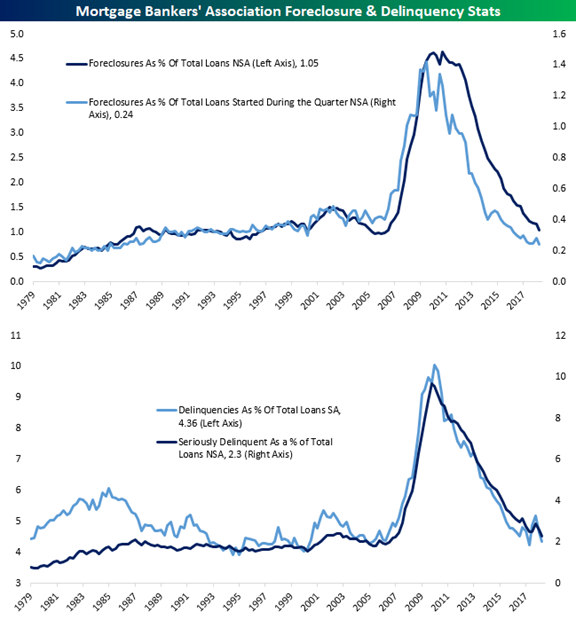

Mortgage delinquencies at multi-decade lows (Bespoke).

-

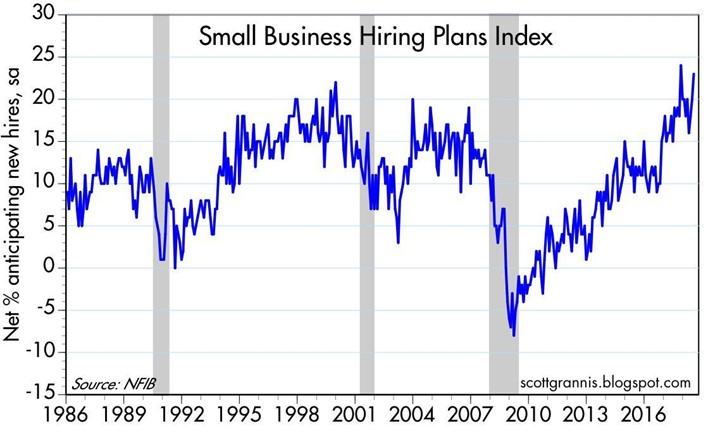

Small Business Optimism as measured by the NFIB Index up ticked again to 107.9. Supply-side economist Scott Grannis notes the crucial role business investment plays in moving economic growth to a higher level. While he does not mention my “delicate balance” terminology, he does acknowledge tariffs as a current but temporary roadblock. Instead of showing the entire index, let’s look at the hiring plans component.

-

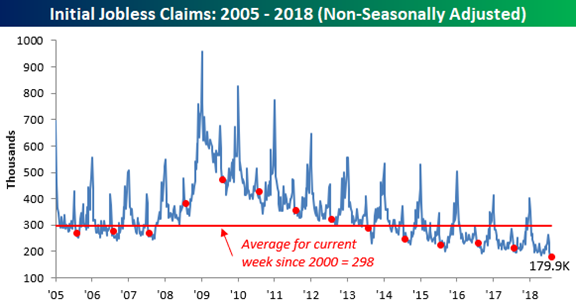

Initial jobless claims declined to 212K, although the four-week moving average edged higher. Bespoke has several great charts and historical perspective. Here is a look at the non-seasonally adjusted series. The most recent report was the lowest on record for this week of the year.

-

Retail sales increased 0.5%. E 0.1% P 0.2% but revised down from 0.5%.

-

Productivity increased 2.9%. E 2.0% P 0.3%.

-

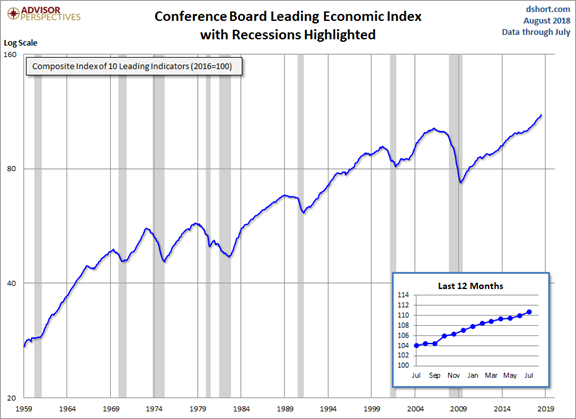

Leading indicators from the Conference Board increased 0.6% E and P both 0.5%. (Jill Mislinski)

The Bad

-

Industrial production increased only 0.1%. E 0.4% P 1% revised up from 0.6%. Capacity utilization continues to run at about 78%. To the casual observer, this may seem just fine. I have not seen recent research, but typically I have associated this level with inflationary pressures. Something new for the research agenda!

-

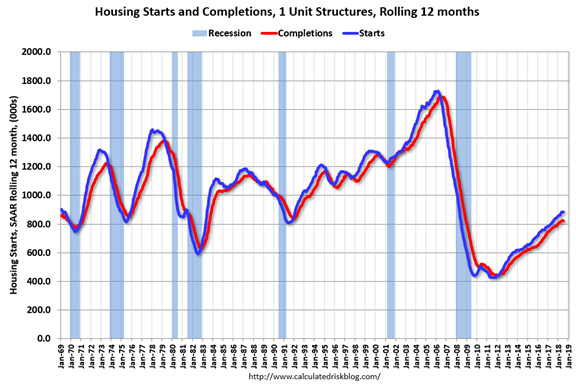

Housing starts grew by only 1168K (SAAR). E 1256K P 1158K. Building permits were in line. Calculated Risk notes the second consecutive disappointment and the relative strength of the single-family data. Bill still expects a continuing sideways move with a general increase over the next two or more years. His post has charts, links to key data, and his recent summaries. This is a great place to catch up if you are concerned about the housing market.

-

New Deal Democrat’s regular weekly review of high-frequency indicators remains positive overall but has turned negative for those in the long-term forecast. This is the first such reading since 2009, but not enough to start a recession watch, he reports.

-

Michigan sentiment registered only 95.3 on the August preliminary reading. E 97.8 P 97.9. Jill Mislinski has charts and details.

The Ugly

What about the chances for hacking the electrical grid? FiveThirtyEight describes the difficulties faced by hackers as well as the advances in current security measures.

The Week Ahead

We would all like to know the direction of the market in advance. Good luck with that! Second best is planning what to look for and how to react.

The Calendar

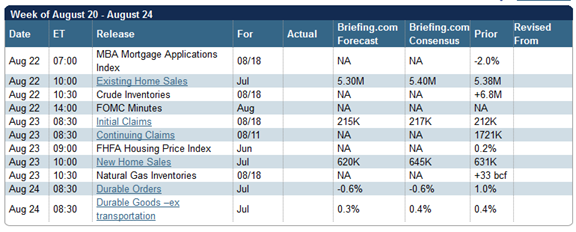

The calendar is even lighter than those of the last few weeks. Earnings season is ending. Many are on vacation. By mid-week we can confidently expect a focus on Fed policy. Until then we must depend upon tweets and soap-opera style news.

Briefing.com has a good U.S. economic calendar for the week (and many other good features which I monitor each day). Here are the main U.S. releases.

Next Week’s Theme

The fact that there is little to talk about does not mean that there will be little talking! Weeks like this are a field day for the punditry. Stories that would not get published or appear on the air in most weeks are suddenly candidates for your eyeballs.

It is easiest to hijack the agenda when there is little competition. It is fruitless to guess what will claim attention during the first part of the week, but things will change beginning on Wednesday.

The FOMC minutes from the last meeting will be released. On Thursday the KC Fed will release the schedule for the annual Jackson Hole Symposium – speakers and titles. At the moment, we know only the general topics, which are so broad that they could be about anything. Friday morning will see the presentation by Fed Chairman Powell. While more will follow, market participants will start checking train schedules, as Art Cashin often says.

As the week wears on, the punditry will be asking:

Will there be a message from Jackson Hole?

The timing is clear. The implications are not. Expect some variant of the following and be prepared for some newly-minted Fed experts!

- The Fed has been too soft for too long.

- It is now too late to catch up since high levels of inflation are now “baked in.”

- It is too late to catch up since the economy has weakened. The Fed “missed its chance to hike back when we pundits said they should.

- The Fed will not be able to unwind the balance sheet.

- No one wants to buy US bonds and trade wars increase the vulnerability.

- Quantitative tightening will flood the market with unwanted paper.

- The Fed is increasing rates too quickly, threatening economic growth and Administration policy successes.

- The Fed, by not raising rates quickly enough, has no room to ease during the next recession – which might happen any day now.

- The Fed will create a recession by inverting the yield curve. Haven’t they followed all the news on this subject?

- And of course, the all-time favorites – in a box, painted into a corner, rock and hard place or some other variant.

- While we may not be sure of the reasons, we can be pretty sure that this will all end badly.

I could publish a party bingo card based on this list. You will hear it all. And everyone will be interested in Powell’s first Jackson Hole speech as Chairman.

I have some personal observations and an alternative approach in today’s Final Thought. Feel free to join in with suggestions of more species of framers.

Quant Corner

We follow some regular featured sources and the best other quant news from the week.

Risk Analysis

I have a rule for my investment clients. Think first about your risk. Only then should you consider possible rewards. I monitor many quantitative reports and highlight the best methods in this weekly update.

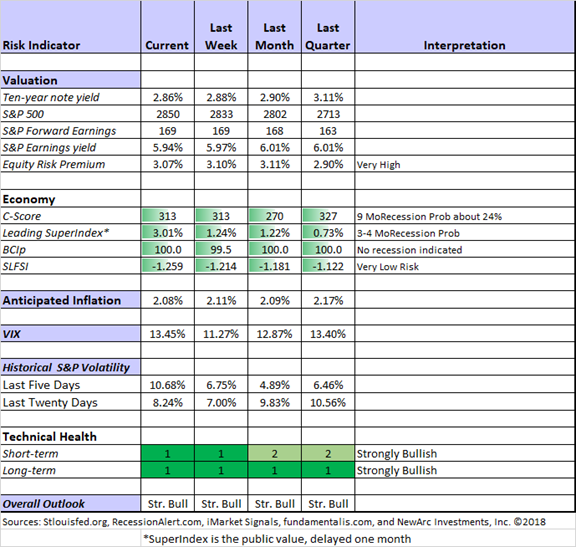

The Indicator Snapshot

Short-term trading conditions continue at highly favorable levels. Actual volatility remains low. The VIX (despite a post-January low) is once again higher than reality.

Some readers have requested a retrospective indicator snapshot from 2008, and we are working on that project.

The Featured Sources:

Bob Dieli: Business cycle analysis via the “C Score.

Georg Vrba: Business cycle indicator and market timing tools. None of Georg’s indicators signal recession.

Brian Gilmartin: All things earnings, for the overall market as well as many individual companies.

RecessionAlert: Strong quantitative indicators for both economic and market analysis.

Doug Short and Jill Mislinski: Regular updating of an array of indicators. Great charts and analysis.

Insight for Traders

Check out our weekly Stock Exchange post. We combine links to important posts about trading, themes of current interest, and ideas from our trading models. This week I suggested a theme that WTWA readers should recognize: What happens when you are leaning the wrong way? It was a good question for traders, and we incorporated the expected expert commentary. Our ringleader and editor, Blue Harbinger, provided data about many funds that might be caught offside. [Mrs. OldProf prefers the latter analogy]. As always, we described a few of the current ideas from the models. Felix highlighted the Russell 2000 and Oscar ranked the high-liquidity ETFs.

While the series emphasizes trading, investors might profit from a look. The methods reduce risk through diversity and (for most people) are appropriate for those needing a boost in returns in their IRA. This week’s theme will soon be featured again on WTWA, this time with an investor emphasis.

Insight for Investors

Investors should have a long-term horizon. They can often exploit trading volatility.

Best of the Week

If I had to pick a single most important source for investors to read this week it would be Marc Gerstein’s post on small cap value stocks. This may seem like an unlikely subject for this recognition, so let me elaborate my reasons. I hope you will then read the post carefully and add Marc to those whom you follow.

- Marc combines great intelligence with creativity, experience, and a disciplined approach. While I have not met him personally, I have participated in some advisor conference calls with him, as well as reading his work for years. He is the real deal.

- Marc’s work is never data-mining, where you can prove nearly anything. He always includes the following

- An initial hypothesis

- Reasonable investigatory criteria

- Understanding of fundamental precepts

- Suspicious skepticism of initial results.

- This post begins with the analysis of value investing – cast aside by those who are avoiding the ‘cold’ factor. He writes:

Value investing works. It always worked in the past. It works now. It will always work in the future. To suggest otherwise would be to deny human nature, the tendency to buy something at a lower price and to bypass an offer from one who sells the exact same product or service at a higher price. A rational buyer will pay a higher price for something only if there is a particular reason to do so (better service, more convenient method of shopping, better buying experience, better warranty, not knowing of a cheaper alternative, etc.).

- He builds on a foundation of prior work with large-cap value stocks, highlighting both similarities and differences.

- He concludes with a list of candidates – and they are just that. Marc understands that screens are usually the basis for building watch lists and doing further work. They are a source of ideas, not a list of conclusions.

Even the astute WTWA reader will need to take a little more time with this post. You need to understand why it is good before reading it, and then read it a second time.

Stock Ideas

The FANG stocks are a hot topic, both in terms of attractiveness as individual investments and in the continuing role in current markets.Chuck Carnevale provides a valuable take on this controversy via his wise, data-based analysis. Some of the points are covered in this post, but watching the video is even better. Here is a key theme:

Furthermore, it’s important to consider and recognize the difference between justifying historical valuations versus justifying current and future valuations. Historical information – if garnered from a credible source – is typically accurate and reliable. Future information requires making forecasts into the unknown and, therefore, less likely to be accurate and/or reliable. This is a real conundrum for investors, because we can only invest in the future. We can learn from the past, but we cannot purchase it retroactively.

Synaptics? (SYNA) A low valuation in the face of current smartphone and IoT challenges. Shareholders Unite expects shares to recover.

General Dynamics? (GD) William Stamm cites the big defense stock as a solid choice in the terms of his interesting portfolio guidelines.

Oil stocks? Kirk Spano sees oil prices as at or near the bottom of a trading range, offering “a strong intermediate-term outlook for oil stocks.” An attractive feature of his analysis is that he looks at the whole picture, beginning with the economics of supply and demand, instead of just making a list of possible influences.

Personal Finance

Seeking Alpha Senior Editor Gil Weinreich’s Asset Allocation Daily considers a wide range of sources as well as his own take on an important issue. It is interesting to financial advisors as well as the DIY investor. This week he highlights possible retirement disaster scenarios. There is discussion of the choices involved in two posts this week he considers the trade-offs in purchasing an annuity or long-term care insurance. Read the entire series for more great discussions.

Abnormal Returns is an important daily source for all of us following investment news. His Wednesday Personal Finance Post is especially helpful for individual investors. This week and an array of great articles, featuring important retirement questions. Among this list of winners, my favorite was Ten Commandments from Richard Quinn of Humble Dollar. There is a lot of practical advice in this post. If you are personally weak on any item, make a note and check back in a few months.

I also recommend Ben Carlson’s careful analysis of real estate investing. Like Ben, I see many investors tempted by apparent steady cash flows and risks that are poorly recognized.

Watch out for…

Walmart (WMT). A great quarter, but big challenges remain. Valuentum does a nice job analyzing both strengths and weaknesses. Also worth reading is their post on Clorox (CLX), “a fantastic company with solid brands.” Yes, there is a ‘but’ coming….

Brokers who pay unfair rates on cash. Seeking Alpha CEO and Editor-in-Chief Eli Hoffman analyzes the wide variation in payments by brokers, some of whom are giving you 0.1% while collecting 1.9%. Since we will all sometimes have cash, this question is of widespread interest. Read the entire post for Eli’s full analysis. Hint: Pick the right broker. His choice (and ours) is Interactive Brokers.

Leveraged loans (WSJ). Most do not understand the relationship with junk-rated bonds. Nearly every “reach for yield” requires very careful investigation.

Final Thoughts

Fed punditry is a great employment opportunity. No experience is required. Everyone understands about money, of course, so you can speak to the masses. The very language of the Fed process – money printing, massive debt, bloated balance sheets – lends itself to connecting with a mass audience. In 2013, Using the Fed as a Fig Leaf, I described how the Fed was being used as an excuse by everyone who had been wrong about the market. The new arguments, listed in that post, proved no more accurate.

There is an interesting post-election change. Many of the loudest critics have switched sides, now cheering for a very different monetary policy. Any party in power wants low interest rates. The “out’s” always find Fed policy fertile ground for economic posturing.

Regular readers know that I think the Fed has done well, both in reacting to the Great Recession, the willingness to use innovative policies, and the measured withdrawal of stimulus. Like everyone else, I am interested in whether changed leadership will imply changed policy.

My biggest disappointment with the “modern” Fed has been the effect of greater transparency. Neither Bernanke nor Yellen were great with the press conferences. Providing more information for the markets seems only to provide more grist for critics. Providing more explanation, showing more forecasts and dot plots, and earlier release of minutes has increased neither confidence nor understanding. Why not?

Market participants always seek a business-like analogy. They want to see leadership, consensus on forecasts, accountability for missed projections, and a single voice in support of agreed policy. They will never get that from the Fed. The issues are inherently complex. A range of viewpoints is very healthy, especially when made public.

There could be plenty of news from Jackson Hole, but it is unlikely to provide the policy buzz most observers seek. The best move for investors is to ignore the Fed blame game and enjoy some family time!

[This is a crucial time for investment decisions. If you are flying solo, you might want to request my papers on risk or the top pitfalls for individual investors. If you are concerned that you do not have a good risk/reward portfolio, or one suited to your needs, feel free to ask us for an analysis. For any of these just email main at newarc dot com].

I’m more worried about:

- Impeachment turmoil. Newsweek has a lead article on the changing odds. This is another example of concerns that are difficult to quantify, in terms of both probability and impact.

I’m less worried about:

- Trade policy extremes. David Kotok has a simple explanation of what tariffs do to U.S. exports, even without any retaliation. As I did a few months ago, he suggests that GOP feedback will lead to a realignment of Administration personnel and policies.

© NewArc Investments, Inc.

Read more commentaries by NewArc Investments, Inc.