Executive Summary

Emerging equities are more volatile than developed market equities. This owes little to the volatility of emerging stock markets in local terms and much more to the strong positive correlation between their local stock markets and movements in their currencies. The spring of 2018 was a classic example of this, with US dollar strength driving significant emerging weakness. Emerging markets do exhibit momentum, so it would not be odd for the weakness to persist for another quarter, although after transaction costs the momentum effect is probably not capturable. Our analysis of the underlying fundamentals for emerging markets, on the other hand, gives us confidence that the assumptions behind our forecasts are sound and emerging value stocks represent the most attractive asset we can find by a large margin, and in the longer term we believe valuation is much more predictive of returns for emerging than momentum is. Our models do not take into account the potential effects of a trade war, but while a trade war is presumably a negative for emerging assets, it should arguably be at least as negative for US assets and seems unlikely to change much about the relative attractiveness of emerging markets in global portfolios.

Emerging markets had a really lousy second quarter. This was true for pretty much any index with “emerging” in the name, regardless of whatever other words were there along with it. MSCI Emerging Equities (EM) was down 8%. The JP Morgan EMBI Global Diversified Bond Index (EMBI) hard currency bond index was down 3.5%. The JP Morgan GBI-EM Global Diversified+ local debt index (GBI-EM) was down 10.4%, and the JP Morgan ELMI Plus emerging currency index (ELMI) was down 5.8%. With the S&P 500 up 3.4% for the quarter and MSCI EAFE down a tame 1.2%, it was therefore a pretty tough quarter for our asset allocation portfolios given our large bias toward emerging securities and against US equities.1 Whenever we have a quarter like this we react by looking at what happened, why it happened, and whether it poses a challenge to the assumptions that caused us to have the biases in our portfolios in the first place. In this case our analysis suggests that what has happened is not particularly out of line with other historical events in emerging markets. The event shows starkly the distinction between emerging and developed markets and is a demonstration of why we consider emerging markets to be riskier than other assets that we invest in. Momentum has historically mattered in emerging markets, so there is some reason to expect that there may be more pain to come in the short term. However, nothing that has happened in the markets or to the underlying fundamentals causes us to doubt our longer-term thesis that emerging markets are the best investment opportunity available today by a substantial margin.

So what happened last quarter, and why were emerging markets hit so hard? Simply put, it was a very strong quarter for the US dollar (USD), with the DXY dollar index up 5%.2 That is a 1.1 standard deviation event, which makes it a little out of the ordinary, but not a true outlier. It probably comes as no surprise that when the USD rises, the US stock market outperforms non-US markets. But what makes emerging markets unique is the fact that this doesn’t simply occur due to the currency translation effect. This quarter, for example, the currency basket of MSCI Emerging fell by 4.8%, precisely the same as the fall for the currency basket of MSCI EAFE. In other words, while some specific emerging currencies fell a lot in the quarter – the Turkish lira fell 13.4% and the Brazilian real fell 10%, for example – you’d be hard-pressed to call this a general case of emerging currency weakness so much as USD strength. But while MSCI EAFE rose 3.5% in local currency terms, slightly outpacing the rise in the S&P 500, MSCI Emerging fell 3.5% in local currency terms. This is par for the course. It is only a mild overstatement to say that the basic difference between the developed world and the emerging world is that when a developed world country has a declining currency, all else equal that is good for that country’s stock market, whereas when an emerging country has a declining currency, all else equal that is bad for that country’s stock market.

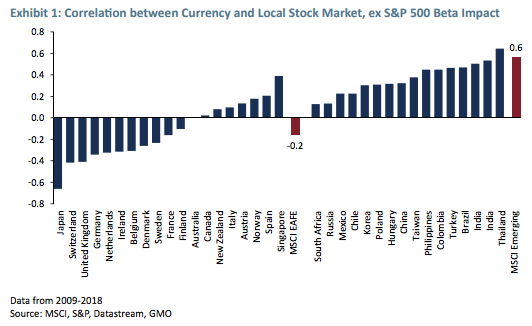

This is true over and above the fact that emerging market currencies tend to have a positive beta – that is they tend to rise when global stock markets are rising, and fall when stock markets are falling. Some developed market currencies, like the Australian dollar, also show a positive beta, although other “safe haven” currencies like the Japanese yen and Swiss franc tend to do well when global stock markets are falling. Exhibit 1 shows the correlation between currency and local stock market movements for 35 developed and emerging markets after we remove the effect of co-movement with the S&P 500.3

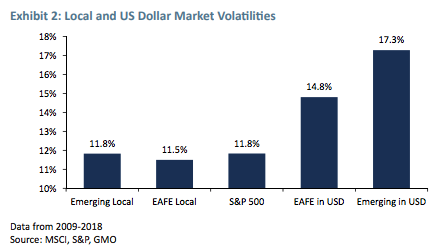

Two-thirds of developed currencies have a negative correlation with their local stock markets, and the figure for EAFE as a whole is -0.2, whereas every single emerging market of those listed above has a positive correlation, and the figure for MSCI Emerging is 0.6. This correlation is arguably the reason why emerging markets are more volatile than developed markets in the first place, as we can see in Exhibit 2.

In local terms, MSCI emerging has been almost exactly as volatile as the US or EAFE markets since the end of 2009, but due to the strong positive correlation between the local returns and the return to emerging market currencies, the volatility in US dollars is significantly higher than for the S&P 500 or EAFE.

But while this explains the riskiness of emerging at a surface level, it doesn’t do much to tell us why the correlation is so positive or whether that volatility is a symptom of truly greater fundamental risk or not. Carl Ross, a senior member of GMO’s emerging debt team who leads our sovereign market analysis, notes four channels in which a falling currency could plausibly have an impact on the local economy or stock market, and these are summarized below.

Debt service channel

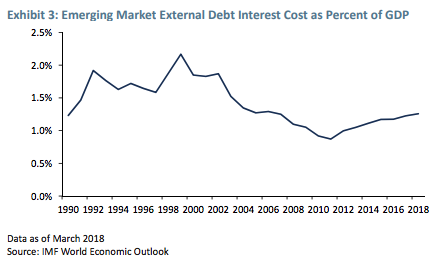

Insofar as a country has debt denominated in US dollars or other hard currencies, a falling currency can make debt service costs more onerous, hurting the economy or corporate cash flow directly. This is not a material issue in the developed world, as the vast majority of debt in developed economies is denominated in the local currency. But emerging countries do borrow in foreign currencies. The trouble with this explanation is that the interest on that debt is just not that high as a percent of GDP, as we can see in Exhibit 3.

At a current interest cost of 1.2% of GDP, a large 20% devaluation would have an impact of about 24 basis points of GDP – not completely immaterial to be sure, but a small fraction of the volatility of emerging GDP growth. When you take into account the impact of foreign currency revenues from exports, which will have increased in local terms given the devaluation and helped cash flow, as well as the generally large foreign exchange reserves of many emerging countries, it is hard to see this as a particularly material impact.

Trade channel

A lower exchange rate will make exports more globally competitive and imports more expensive. While you would expect some winners and losers across companies from this shift, in aggregate the corporate sector should be a net beneficiary, while the household sector would be more of a casualty. The corporate sector produces the bulk of exports whereas households consume a large fraction of imports, so the corporate sector benefits and households are worse off. This is the effect that appears to predominate in the developed world, driving negative correlations between stock markets and currency movements. In principle it should also exist in the emerging world, although it goes in the opposite direction of the effect we see. One possible issue that impacts emerging countries with this channel is that if the country acts simply as an “assembler” – putting together devices such as smartphones or computers – the import content of exports is very high and the local value-added is small as a percentage of exports. But even in such a case, a lower currency should certainly improve the competitive position of whatever value-added is produced locally.

Monetary policy channel

A falling currency will, all else equal, cause inflation to rise in that country due to rising import prices and likely price rises from domestic companies that compete with imports. In a country with well anchored inflation expectations this inflationary kick would probably seem like a one-off event that a central bank can safely ignore.4 But inflation expectations are less well-anchored in the emerging world, and a central bank may well feel forced to tighten monetary policy to protect against rising inflation or simply to bolster the currency itself, despite the fact that the falling currency was probably a sign of a weakening economy in the first place. This pro-cyclical monetary shift would tend to make downturns worse than they otherwise would be, because central bank orthodoxy holds that monetary stimulus is the appropriate response to economic weakness. Given stock markets generally do poorly in times of economic weakness, this effect works in the direction we see empirically.

Portfolio channel

A falling currency can cause both local investors and foreign investors to flee a market. In the case of foreign investors, this is a fairly simple case of investors acting like momentum traders. The falling currency means foreign investors are experiencing losses measured in their home currency, and many investors react to losses by increasing their estimate of the riskiness of the investment that just lost money and decreasing their expected returns to the investment. Higher risk and lower return are obviously a bad combination, and as a consequence we see selling after currency losses. Local investors, who Carl points out in many cases measure their wealth in USD terms in the first place, can react negatively to the perceived loss of wealth and try to get money out of the country into “safer” investments.

In aggregate, this leads to a somewhat mixed picture where it’s easy to imagine that emerging currencies and stock markets should be less negatively correlated than developed markets, but frankly it doesn’t seem to justify the strong positive correlation we actually see.

But what does this mean for the future?

Clearly, if the USD continued to strengthen, it would be a negative for emerging markets. Will it happen? It is hard to dismiss the possibility. A strong US economy and rising interest rates are more likely to be associated with an expensive USD than a cheap one. But on that front, it’s worth recognizing that the USD is already pretty expensive, as we can see in Exhibit 4.

After last quarter’s rally, the USD is 0.8 standard deviations overvalued on a trade-weighted purchasing power parity basis.5 Over the last 20 or so years, it has gotten more overvalued than that on two occasions, peaking out at about 1.5 standard deviations expensive, or about 9% higher than its current level. If that were to happen, we believe you might expect it to cost emerging equities another 15% in total performance as a bear case scenario.6 On the other hand, even with relatively high interest rates to buoy it, 0.8 standard deviations is reasonably far above fair value, and we would expect weakness from here to be more likely than strength.

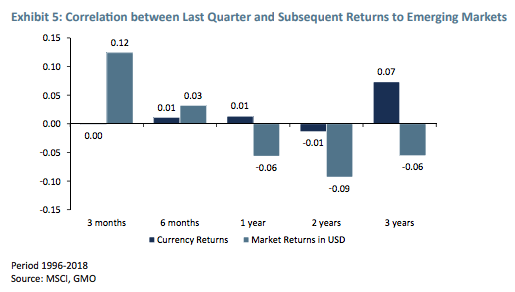

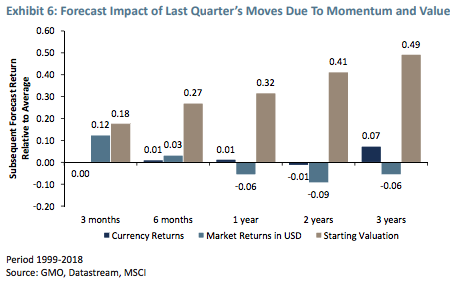

What else can we say about the potential future for emerging based on last quarter’s events? Exhibit 5 shows the correlation between currency movements and stock market returns in the previous quarter and following period returns for emerging markets.

Currency returns themselves seem not to matter at all, with a correlation of effectively zero out to two years. So, there is no reason to believe that the currency moves from last quarter tell us much. Total returns for emerging do have some power, however. There is evidence of short-term momentum in emerging markets with a correlation of 0.12 between last quarter’s return and next quarter’s. For an 8% move such as we saw last quarter, the momentum effect suggests next quarter’s return could be about 1% worse than average. Given that the round-trip trading cost for an emerging market portfolio is somewhere in the realm of 50 to 200 basis points, that’s an interesting effect, but not obviously an exploitable one. When we look at the correlations for a simple valuation metric, however, you can see why we tend to be more enthusiastic about value as an asset allocation tool. This is shown in Exhibit 6.

Over one quarter, value7 is mildly more powerful than momentum in predicting future returns, but whereas momentum quickly dissipates as a predictor as the time horizon lengthens, value chugs along with ever-improving correlations. Last quarter’s return was about a 1 standard deviation negative event from a momentum perspective, and made emerging about 0.25 standard deviations cheaper than it was before. Exhibit 7 shows the expected return versus average given a 1 standard deviation negative momentum event and a 0.25 standard deviation positive value shift to predict returns over the next three months to three years, given emerging’s history.

Over three months, the momentum move should matter more, and the expected impact is slightly negative. As the period gets longer, it wouldn’t even be a contest, as the power of valuation continues to grow while momentum completely dissipates. In a world of zero transaction costs it might be tempting to trade on momentum, although the returns wouldn’t be extraordinary. In the real world, where trading costs real money, it seems very difficult to argue for selling any emerging equities today. Emerging equities are cheaper than they were three months ago, and history shows that when these assets are cheaper, they perform better over time.

But how has emerging been doing fundamentally?

A more important question to our minds is about how the fundamentals of emerging have been doing. Our forecasts, which are more involved than a simple cyclically-adjusted P/E, assume that the underlying fundamentals for emerging stocks will grow solidly over time. Specifically, we assume that the sum of dividends and per share growth in capital should be approximately 6% real, as those two pieces make up the long-term return to stocks.8 It turns out to be more complicated calculating this quantity than you might think, and we have two methods that over time should form upper and lower bounds for the quantity even if there is some volatility in each of them year by year.9 Exhibit 8 shows two different ways of calculating the “fundamental return” of emerging annually since 1996.

The two estimates do bounce around year by year, but the averages for both estimates are entirely in line with our assumption, which is shown in the dashed black line. This analysis is not hiding any problem with a collapsing return on capital for emerging markets, as we can see in Exhibit 9.

We assume the return on economic capital in emerging will average 6% over time. Recent years have been eerily consistent with this assumption, and the recent data, if anything, shows improvement, which we assume will eventually reverse and return on capital will fall back to 6%.

Forward-looking concern: What about a trade war?

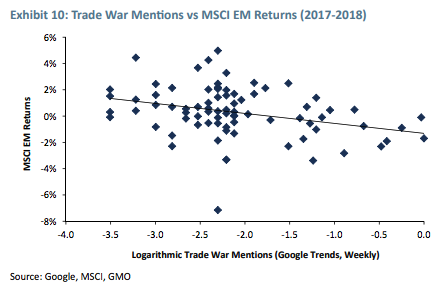

So there is no reason we can see for concern that the backward-looking fundamentals for emerging have been worse than our models assume they should have been. That doesn’t mean that there couldn’t be problems in future. In particular, the looming prospect of a broad trade war weighs very heavily on emerging market countries. We can see that directly in their performance over the past 18 months. My colleague John Pease put together Exhibit 10, which shows the relationship between Google searches for “trade war” and performance of emerging countries.

The more the topic “trade war” gets mentioned, the worse the performance is for emerging markets. A doubling of the share of searches that mention “trade war” leads to returns 0.8% worse on a weekly basis for MSCI Emerging. From a fundamental perspective, emerging countries really do have a lot to lose if the world were to retreat from global trade. Trade is a large percentage of GDP for many emerging countries, but even beyond that, the industries that produce exports are the industries that are capable of the strong productivity growth that is necessary for emerging economies to get richer. Further, many emerging companies are parts of the supply chain for global multinationals. Without a strong brand or differentiated intellectual property of their own, they can be particularly vulnerable should tariffs or quotas change the attractiveness of doing business in a particular country.

It is appropriate, therefore, to be concerned about escalating trade tensions. But it is also worthwhile to keep them in perspective. At this point, the trade war that is in the offing is very much “US versus the world,” instead of “everybody versus China” or “everybody versus everybody.” This is an important distinction, because while the US is the world’s largest economy at about 25% of global GDP as of 2016,10 it is one of the most closed economies in the world, such that US exports are only about 12% of the global total and imports about 15% of the global total.11 If the US were to actually follow all the way down the current path and put tariffs on 100% of all US imports, with the rest of the world responding with tariffs of their own, the result would impact 12% to 15% of trade for the rest of the world and 100% of trade for the US. While 15% of trade isn’t immaterial, it’s hard to see how it fundamentally alters a lot of the calculus of who builds what where. On the other hand, 100% of trade can have fairly profound impacts, as we’ve already started seeing in the earnings reports of US companies, particularly those that are significant users of steel or aluminum products. Exhibit 11 shows what has happened to the local price of cold rolled steel coil in the US, China, and Europe from January until June of this year.

US steel costs have risen by 18% relative to prices in Europe and by 30% versus Chinese prices. The US steel tariffs have unquestionably been a boon for US steel producers, but any company producing goods using steel now has a pretty good reason to avoid producing those goods in the US. If the US were to start imposing tariffs on all goods using steel in order to protect US goods producers, it could protect those US companies competing with imports from the impact of the nasty cost shock they have just experienced, but even that would do absolutely nothing to restore their competitiveness outside of the US, which has just taken a similar hit. The US can wall itself off from the world in some sort of misguided spirit of autarky, but as has generally been the case with protectionist policies by governments throughout modern history, this will make US industry less, not more, competitive with the rest of the world.

In short, tariffs are generally bad for business, and all else equal they are probably worse for emerging market companies than developed market companies given their place in the supply chain. But all else is not equal, and so far it seems likely that the impact of the US imposing tariffs on the rest of the world and the rest of the world responding in kind is likely to be worse for the US than everywhere else. The generally domestically-focused nature of the US economy means that the economic impact of all the tariffs might not be that severe, but it is worth remembering that the US stock market is an awful lot more globally exposed that the overall economy. Price action so far makes the US look like a haven from trade war fears, whereas emerging countries look like the major victims. But it seems likely the reality of a trade war, should it occur, will prove otherwise.

Conclusion

Emerging assets had a lousy quarter of the classic variety. In the face of falling currencies, local stock markets moved lower as well. This is par for the course for emerging equities, even if it is not obvious that the fundamentals support such a correlation. While the currency fall predicts nothing about future returns for emerging assets, the stock market declines do suggest there may be some more short-term pain to come, given the historical power of momentum to predict emerging returns. On the other hand, both emerging stocks and currencies are cheaper than they were three months ago, and historically cheaper valuation has been a plus in both the short and long term. Exhibit 12 shows the margin of superiority for our favorite asset relative to our next favorite asset through time on our asset class forecasts. Emerging market value stocks are the best asset we can find, by a margin that is just off of the largest we have ever seen.12

This large margin of superiority warrants a large position in emerging value stocks, and that is what we have in asset allocation portfolios where allowed. There is no question that positioning was painful last quarter. Given that we have a large position in emerging equities, we are particularly vigilant about events in the emerging world to ensure we are not missing something important that would cause emerging assets to be less attractive than we believe them to be. As of now, we can see nothing in the recent or longer-term fundamentals for emerging equities that causes us to question the assumptions that underpin our forecasting models. On a forward-looking basis, there are risks. There are always risks to emerging equities. That is what it means to be a risk asset, and emerging equities are one of the riskiest risk assets out there. But as for the most talked-about risk today – a trade war – it is not obvious that emerging equities are truly in the crosshairs given that what is currently unfolding is not a truly global trade war, but the US taking on the rest of the world. Despite the size and strength of the US economy, and despite the rhetoric coming out of the US administration, a single country trying to take on the world is extremely likely to create more problems at home than it does abroad. In the longer run, whatever the US does, we believe emerging markets should be just fine. With luck, the US will be as well, but that seems a riskier bet.

Ben Inker. Mr. Inker is head of GMO’s Asset Allocation team and a member of the GMO Board of Directors. He joined GMO in 1992 following the completion of his B.A. in Economics from Yale University. In his years at GMO, Mr. Inker has served as an analyst for the Quantitative Equity and Asset Allocation teams, as a portfolio manager of several equity and asset allocation portfolios, as co-head of International Quantitative Equities, and as CIO of Quantitative Developed Equities. He is a CFA charterholder.

Disclaimer: The views expressed are the views of Ben Inker through the period ending August 2018, and are subject to change at any time based on market and other conditions. This is not an offer or solicitation for the purchase or sale of any security and should not be construed as such. References to specific securities and issuers are for illustrative purposes only and are not intended to be, and should not be interpreted as, recommendations to purchase or sell such securities.

Copyright © 2018 by GMO LLC. All rights reserved.

1 More specifically, our asset allocation portfolios have a large bias toward emerging value stocks, not emerging stocks in general. In this quarter, though, growth versus value was not a material driver. Value did underperform broad emerging by 1%, but compared to the fall in emerging generally, it was a small effect.

2 DXY is a common index for describing the performance of the USD. The thing about measuring currency returns is that you have to measure a currency against something else for there to be a return. Measured in US dollars, the USD doesn’t move. The DXY measures the performance of the USD against a basket of the euro, Japanese yen, British pound, Canadian dollar, Swedish krona, and Swiss franc. Frankly, at this point it is a slightly odd basket relative to trade flows or global GDP, but it remains the most commonly quoted USD index, and does a decent job of capturing what the USD is doing.

3 To be clear, removing the S&P 500 beta effect decreases the gap between emerging and developed markets rather than increasing it, because in addition to the effect shown in Exhibit 1, almost all emerging currencies have a positive beta to the S&P 500 whereas most developed currencies do not.

4 We have seen the Bank of England look through depreciation-related inflation increases repeatedly in the face of periodic drops in the pound over the last decade, as an example.

5 Purchasing power parity models value currencies by comparing the prices of baskets of goods and services in different countries. If the basket is more expensive in one country than another at prevailing exchange rates, that country’s currency is deemed overvalued.

6 That 15% comes from 9% dollar appreciation and a further 6% fall in emerging market stocks in local terms given their beta over time.

7 The value metric I am using here is price/5-year earnings. It is a shorter version than standard CAPE because we have limited history for emerging stocks and I wanted to capture as much of the history we have as I could. Our forecasts use a 10-year version of CAPE as one of the inputs.

8 You can break down returns to stocks in multiple ways, but we do it into four pieces: P/E change, return on capital change, capital growth, and dividends. Together they fully describe returns. Neither P/Es nor return on capital can trend forever, so in the long run, returns need to be driven by capital growth and dividends. This is true despite the fact that changes to P/Es and return on capital drive most of the shorter-term volatility in stock returns.

9 The short version of why this is tricky is that changes to index composition impact the aggregate fundamentals of the index. In 2016, when Tencent, Alibaba, and Baidu were added to MSCI Emerging, this had the effect of reducing the aggregate sales, book, earnings, etc., for the index because these stocks were trading at significantly higher valuations than the rest of the index. In Method 2, that shows up as negative growth, which it isn’t. Method 1 ignores the impact of index changes, which is probably too friendly. Truth almost certainly lies somewhere in between the two.

10 Source: World Bank, BEA.

11 Source: WTO. Global total excludes intra-EU trade.

12 It may seem counterintuitive that the margin of superiority for emerging value fell in the second quarter given that emerging equities had such a lousy return. The second best asset on our forecasts is hard currency emerging market debt, and that forecast actually rose a little faster, although the gap between the two is still very large.

© GMO

Read more commentaries by GMO