Boston - Earlier this summer, we blogged our view that bond investors will have to adapt to a new regime very different from the one they've grown used to in recent years.

The decade after the financial crisis has been marked by low inflation and investment spending, lagging income growth and a strong U.S. dollar. We expect these trends to reverse direction and potentially surprise investors who aren't prepared.

In this post, we'll focus on an important theme that could be bonds' strongest headwind in coming years, and one that many don't expect to materialize.

That risk is rising inflation.

Our view of rising inflation is based on several factors. They include:

- Governments focusing more on fiscal policies and spending to maintain economic growth.

- Trade wars and tariffs that are already driving price increases.

- Expectations of wage growth as the labor market continues to tighten.

- Companies' apparent confidence they can pass along higher costs to consumers.

- Expectations of higher housing costs.

- Expectations of a weaker U.S. dollar.

The sleeping dragon

It's not surprising that most investors have a ho-hum attitude on inflation risks. The runaway inflation that many forecast in response to massive quantitative easing (QE) from central banks, of course, hasn't materialized.

Year-over-year changes in the Consumer Price Index (CPI), which tracks the cost of goods and services, remain modest. Core CPI, which strips out volatile food and energy prices, has averaged year-over-year growth of about 2% so far in 2018. However, under the surface, inflation in goods is very tame, while the costs of services and transportation are rising faster.

Therefore, we think that inflation is percolating, and could be a major headwind for income-focused investors. After all, inflation plays the role of the primary villain for bond investors.

What's changing?

We already listed the reasons why we think inflation is poised to move higher.

Regarding the dollar, the U.S. appears to be looking more inward, while perhaps being less concerned about the dollar's status as the world's reserve currency. Meanwhile, rising fiscal spending and tax cuts could weigh on the dollar.

The market's inflation expectations have been moving higher, based on inflation break-even rates. Also, the U.S. 10-year Treasury note yield is again threatening to break out above 3%, seen as a key psychological level. So, capital is in motion, but we still think many investors are underestimating inflation.

We mentioned governments moving to fiscal policy, and relying less on central bank QE policies, in order to foster growth. But, this fiscal stimulus is coming in what appears to be the later stages of the cycle, following years of low yet sustained growth. Adding fuel to the fire at this point might trigger unintended consequences.

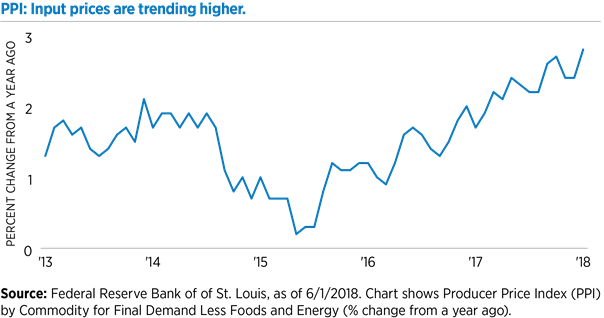

Already, input prices have been trending higher since about mid-2015.

Now, with tariffs in the headlines, more companies in second-quarter earnings statements and calls are hinting at price increases. For example, Procter & Gamble is raising prices of diapers by 4%, and raising prices of toilet paper and paper towels by 5%. The company cited rising commodity and transportation costs. So, some companies are positioning for inflation, even if many investors are not.

We also expect home prices will continue to move higher, mainly due to an ongoing lack of supply, particularly for starter homes. In fact, some homebuilders are shying away from building more affordable homes because rising materials and labor costs are making it less profitable.

Finally, we think wage pressures are building and that wages will rise. Earlier this week, the Labor Department said U.S. employment costs rose 2.8% in the second quarter from the year-ago period - the biggest increase in about a decade. That's another tail wind for inflation and is likely a reason why companies are confident they can pass along higher input costs to consumers.

Bottom line: For bond investors seeking returns in coming years, we believe inflation will be their biggest challenge.

Before investing in any Eaton Vance fund or unit investment trust (UIT), prospective investors should consider carefully the investment objective(s), risks, and charges and expenses. For open-end mutual funds and UITs, the current prospectus contains this and other information. To obtain a mutual fund prospectus or summary prospectus and the most recent annual and semiannual shareholder reports, contact your financial advisor or download a copy here. Read the prospectus carefully before you invest or send money. For closed-end funds, you should contact your financial advisor. To obtain the most recent annual and semi-annual shareholder report for a closed-end fund contact your financial advisor or download a copy here. To obtain a UIT prospectus, contact your financial advisor or download a copy here. Before purchasing any variable product, consider the objectives, risks, charges, and expenses associated with the underlying investment option(s) and those of the product itself. For a prospectus containing this and other information, contact your investment or insurance professional. Read the prospectus carefully before investing.

Not FDIC Insured. No Bank Guarantee. May Lose Value.

Eaton Vance does not provide tax or legal advice. Prospective investors should consult with a tax or legal advisor before making any investment decision.

The information on this Web page is for U.S. residents only and does not constitute an offer to sell, or a solicitation of an offer to purchase, securities in any jurisdiction to any person to whom it is not lawful to make such an offer.

© 2018 Eaton Vance Distributors, Inc. | Member FINRA / SIPC | Two International Place, Boston, MA 02110 | 800.836.2414 | eatonvance.com

© Eaton Vance

Read more commentaries by Eaton Vance