Do not put your faith in what statistics say until you have carefully considered what they do not say. ~William W. Watt

In a 2014 NYU study almost every participant rated their own driving skills as “above average.” It is, of course, impossible for the majority to be “above average.” Averages can be misleading, particularly when they are applied to complex systems. Think of the weather — how many days actually have high temperatures that are the exact long-term average number? Very few. Capital markets are a perfect example of this type of system, where the distribution of outcomes is broad and the shape of the curve exhibits “fat tails” — a higher probability of more extreme results than a normal distribution.

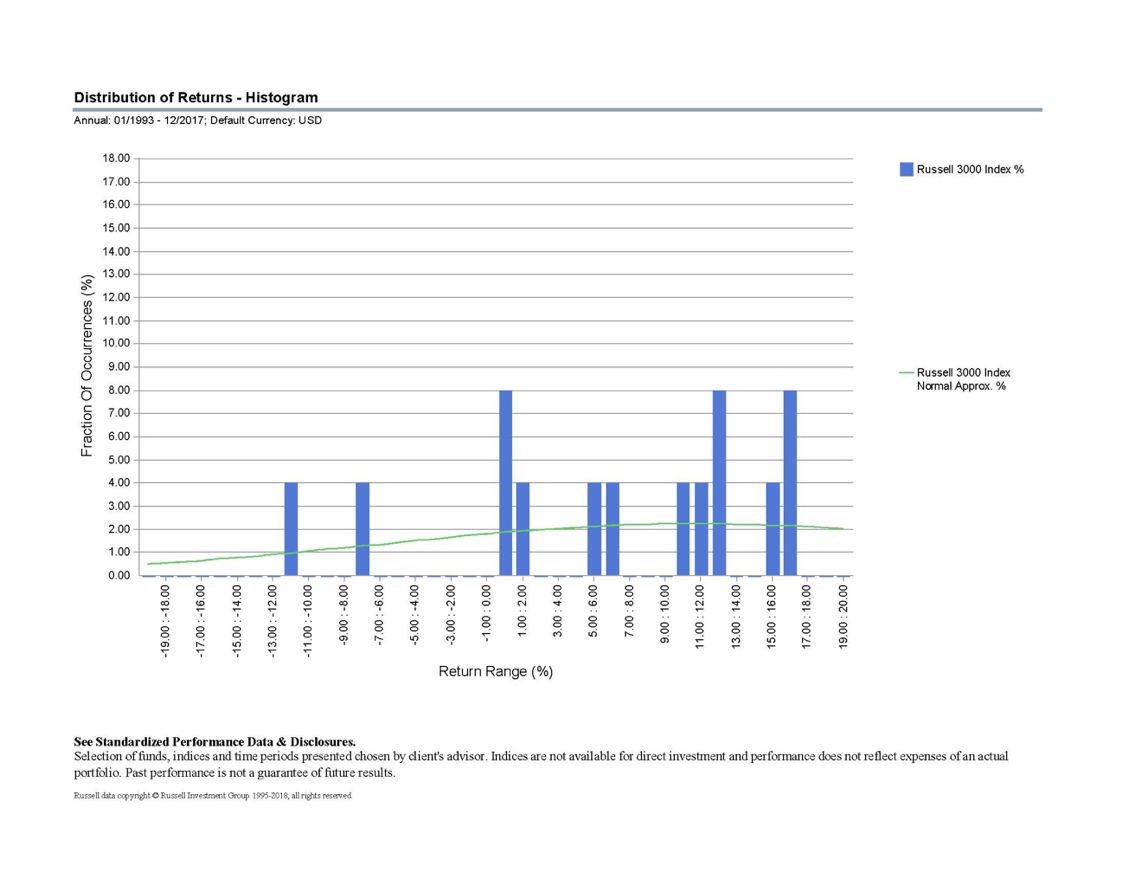

The Russell 3000 Index is a market cap-weighted index of the 3,000 largest stocks in the U.S. They represent about 98% of the investable U.S. equity market. Over the past 25 years (1993-2017, inclusive), the average annualized return for the index has been 9.72%. So, how many annual periods would we expect to cluster around that number? How many times did the index return fall between 9% and 10% during any year? Zero, zip, nada. It never happened. In fact, the most common result was between 0% and 2%. This is the fallacy of examining an average with only a small number of data points and of using arbitrary calendar-year periods.

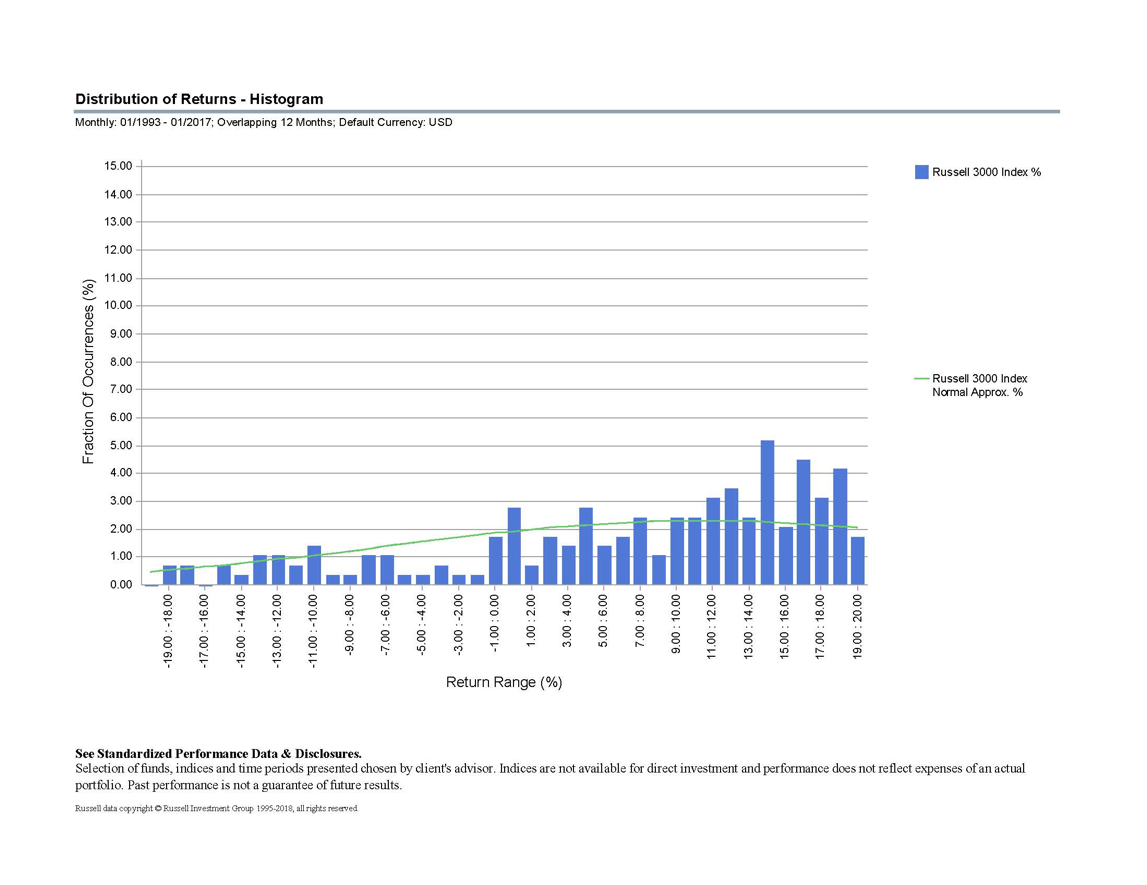

So, what happens if we look at more data? Let’s examine rolling 12-month time periods. There are now 289 observations, and we find the annualized return falls within 9% and 10% a bit more often — about 2.4% of the time. Still, likely a lot less than what most of us would expect — and, the distribution of returns still looks nothing like a bell curve.

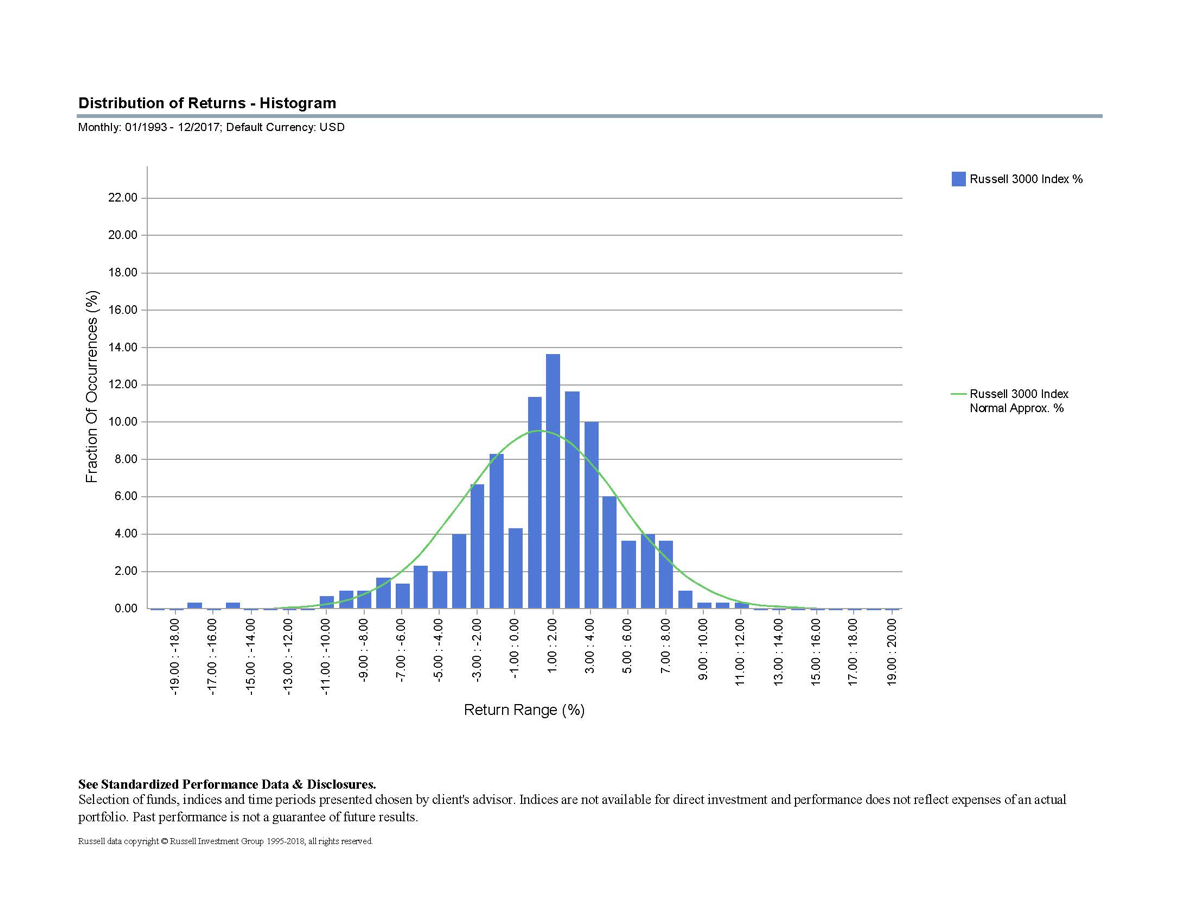

Let’s look at monthly returns. The average over the time period is 0.86%. Now, using more granular data, the bell curve starts to become apparent — with just more than 10% of the monthly returns falling within the 0% to 1% range. But, it’s also notable that the returns still vary quite significantly from the normal distribution, exhibiting much more frequent returns in the 0% to 4% range than expected. We also see that about 0.7% of the returns are below -15%, where we would expect to see less than 0.01% in a normal distribution.

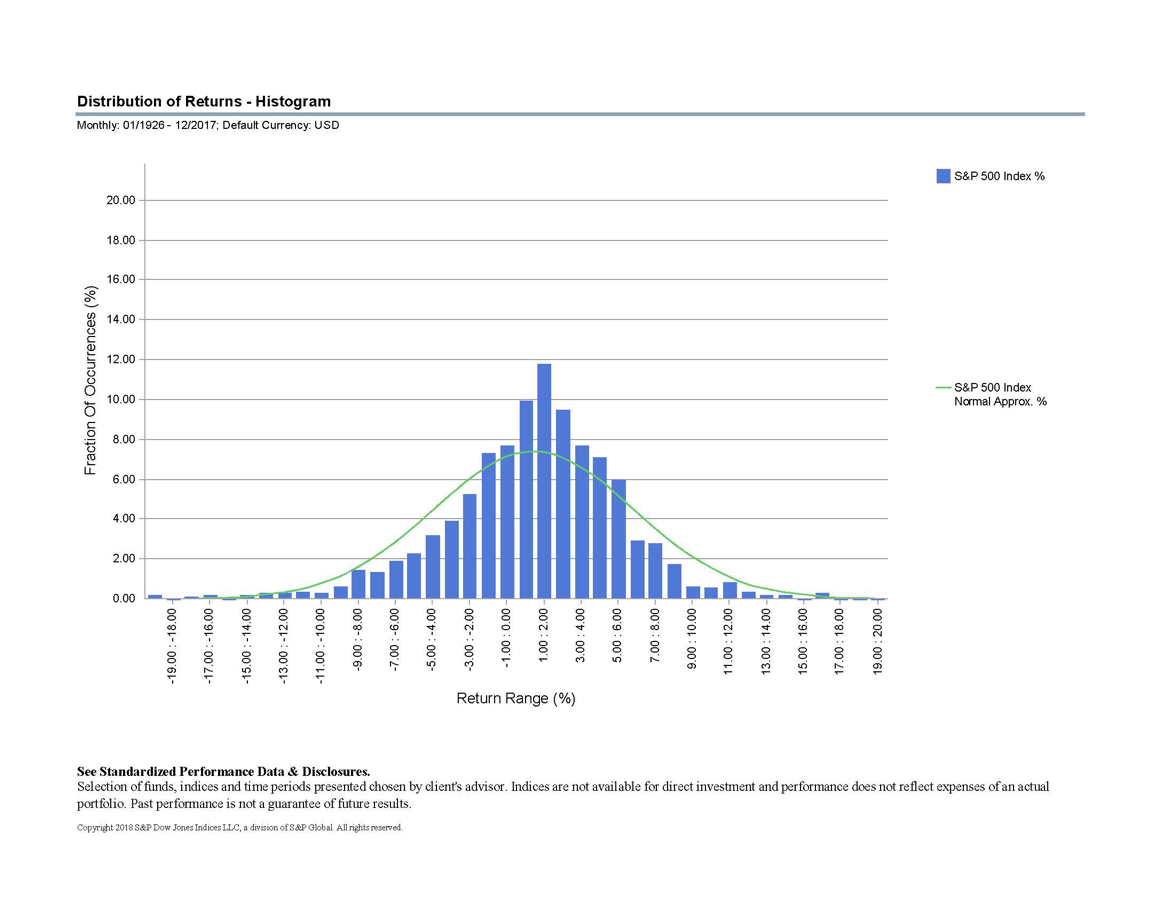

Perhaps, a longer time frame will produce a something that looks more like a normal distribution. We have data on the S&P 500 going back to 1926. That provides us with 1,104 monthly data points and, if a normal distribution is representative of stock market behavior, we should see it. The results are obvious — a much more pronounced peak around the average and the presence of fat tails again. A monthly return in the 18% to 19% range should happen 0.00564% of the time, but it happens 32 times more often than the normal distribution predicts.

What is going on here?

Benoit Mandelbrot, Sterling Professor Emeritus of Mathematical Sciences at Yale University, puts it this way “Extreme price swings are the norm in financial markets – not aberrations that can be ignored. Price movements do not follow the well-mannered bell curve assumed by modern finance; they follow a more violent curve that makes an investor’s ride much bumpier.” Or, to quote Fama and French, “Distributions of daily and monthly stock returns are rather symmetric about their means, but the tails are fatter (i.e., there are more outliers) than would be expected with normal distributions. The message for investors is: expect extreme returns, negative as well as positive.”

Forewarned is forearmed.

© Talis Advisors

Read more commentaries by Talis Advisors