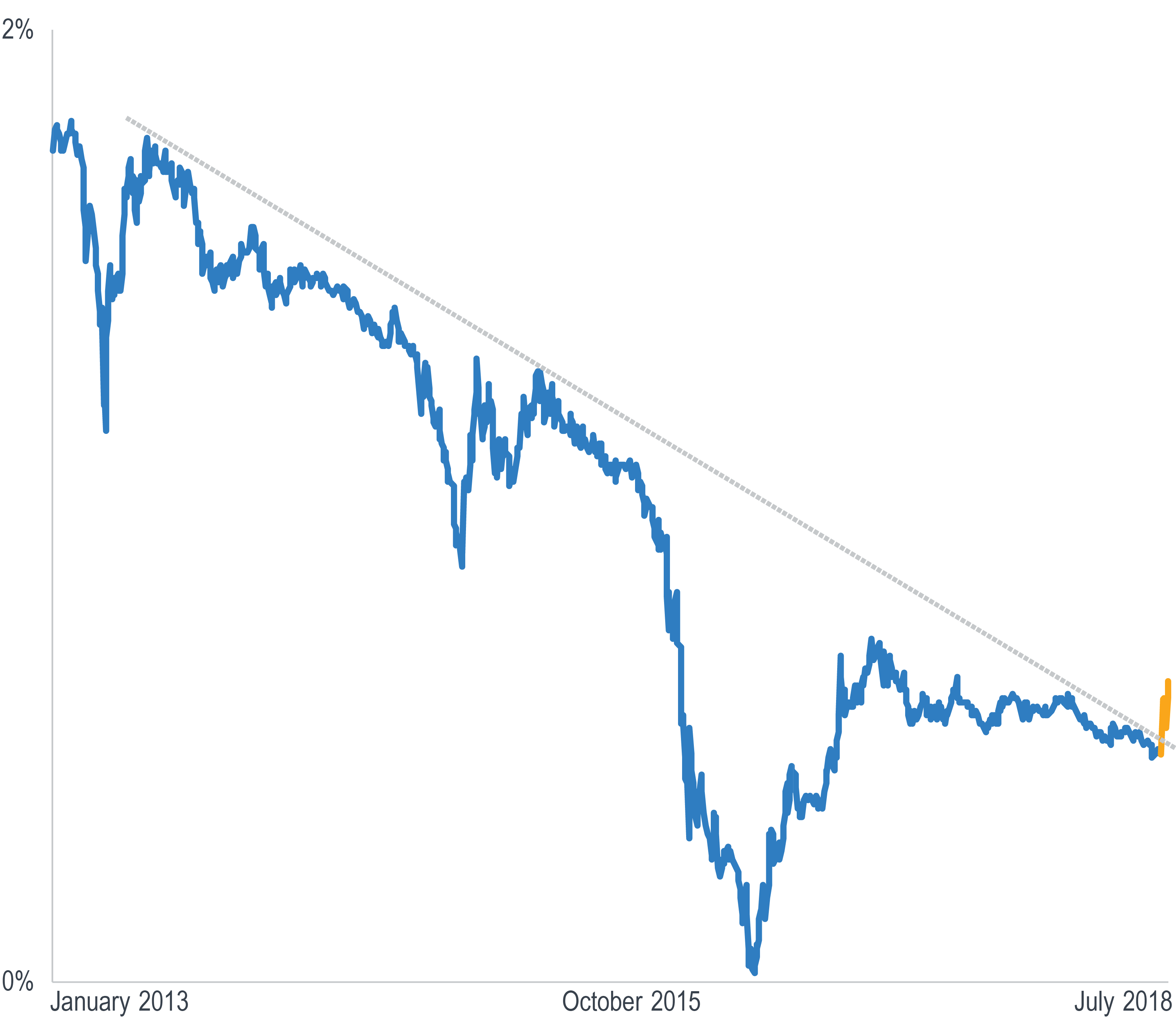

Japan 20 Year Government Bond Yield (%).

In its July 31, 2018 statement, the Bank of Japan noted that it decided to “strengthen its commitment to achieving the price stability target by introducing forward guidance for policy rates, and to enhance the sustainability of ‘Quantitative and Qualitative Monetary Easing (QQE) with Yield Curve Control’”.

With respect to Yield Curve Control, the bank indicated it would continue buying 10-year Japanese government bonds (JGBs) so that the 10-year yield remains around zero percent.

In spite of this being unchanged from their statements over the past 18 months, this time around, the market seems to be interpreting it differently.

As recently as July 20, 2018, the yield on the 20-year JGB was 48 bps. By August 2, it had broken sharply above its trend line, jumping to 63 bps, an increase of 32%.

Ultimately only time will tell, but with rates in the US, now two years off their lows, this breakout may be signaling that Japan is the next domino to fall as rates around the globe revert back to their pre-crisis norms.

Unless otherwise noted, data is sourced from Bloomberg.

Recipients must make their own independent decisions regarding any strategies or securities or financial instruments mentioned herein.

The products or services described or referenced herein may not be suitable or appropriate for the recipient. Many of the products and services described or referenced herein involve significant risks, and the recipient should not make any decision or enter into any transaction unless the recipient has fully understood all such risks and has independently determined that such decisions or transactions are appropriate for the recipient.

The results shown are historical, for informational purposes only, and do not guarantee future results.

Any discussion of risks contained herein with respect to any product or service should not be considered a disclosure of all risks or a complete discussion of the risks involved.

The recipient should not construe any of the material contained herein as investment, hedging, trading, legal, regulatory, tax, accounting or other advice. The recipient should not act on any information in this document without consulting its investment, hedging, trading, legal, regulatory, tax, accounting and other advisors.

The materials in this document represent the opinion of the authors and are not representative of the views of Milliman, Inc. Milliman does not certify the information, nor does it guarantee the accuracy and completeness of such information. Use of such information is voluntary and should not be relied upon unless an independent review of its accuracy and completeness has been performed. Materials may not be reproduced without the express consent of Milliman.

Data included in this document has been sourced from providers that Milliman FRM believes to be reliable from information available publicly or with consent of the provider of the source material. To the fullest extent permitted by law, no representation or warranty, express or implied is made by Milliman FRM as to the accuracy or completeness of the source data or any other information in this document.