In the title of his quarterly message at the beginning of this year, our outgoing president Sam Stewart referred to a popular rumination of baseball legend Yogi Berra: Seems Like Déjà Vu, All Over Again. Sam also observed that, “For just about any market force that might normally be expected to derail the status quo of continuing growth, an opposing force has emerged to keep the expansion on track.”

Over the six months since that message, and particularly during the second quarter, we’ve seen plenty of factors with the potential to cool off long-term global economic growth. We’ve also had multiple instances of that vague déjà vu sensation of having been here before—because these factors haven’t had overly significant impacts on the resilience of the economy and the financial markets.

Economic indicators and market action in recent years serve as reminders that assuming worst-case scenarios is usually a mistake. Neither President Trump’s most-controversial actions, nor the tensions surrounding the Brexit referendum, nor other geopolitical events have put the brakes on generally strong world-wide economic growth and stock prices. So while disturbances like the recent fractured political situation in Italy and the intensifying international trade spats have created some volatility and may continue to do so, we believe that the largely synchronized global growth trends are still on track.

Therefore, I’ve adapted the déjà vu theme for this quarterly message—our first message since Sam signed off in April. The adaptation I’ve used here, Déjà Vu Squared, is a tribute to Sam’s essential theme over the past several years: expect more of the same, at least in the near term—but stay keenly alert for potential trouble spots. For our part, we think such trouble spots will have more to do with overvaluation and/or faltering fundamentals in specific investments, rather than with the macro events we’re likely to see in the news.

In a broad sense, what we mean by “more of the same” is we expect ongoing economic expansion and continued opportunities in world-wide financial assets, despite geopolitical uncertainties and the long tenure of the current bull market. In this quarterly message, I share our thoughts on the economy and the markets. Going forward, other members of the Wasatch investment team will rotate in to write our quarterly messages—providing you with additional perspectives.

ECONOMY

While there was some nervousness in global financial markets during the second quarter of 2018, world-wide economic news was generally positive. In the U.S., the news was particularly good. The unemployment rate has trended downward for several years, and at about 4% in June the rate was close to the lowest level in 50 years. Other favorable trends included modestly rising wages and inflation. As a result, consumer confidence stayed relatively strong—even among lower-income Americans. Moreover, corporate earnings broke record levels on a widespread basis. And what we heard anecdotally from corporate management teams matched up with the economic indicators.

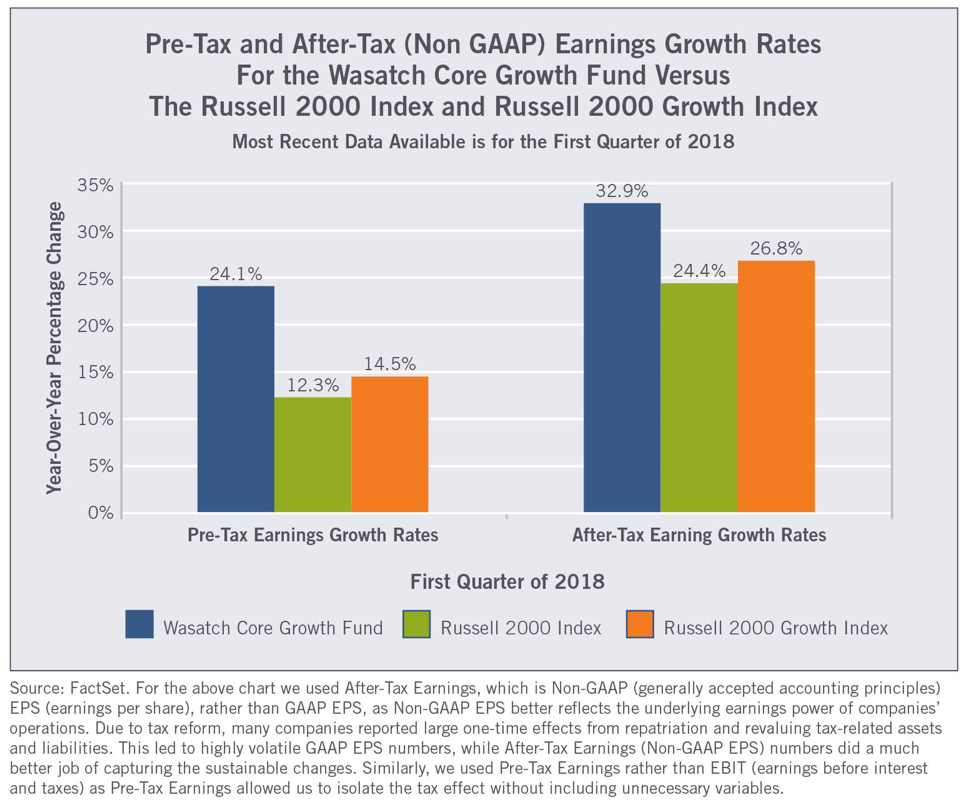

Even more important was the earning growth we actually saw in our Funds. For example, the following chart presents the pre-tax and after-tax earnings growth rates for the companies in the Wasatch Core Growth Fund versus the companies in the Fund’s primary and secondary benchmarks. The purpose of this chart is to look at the growth in after-tax earnings compared to what we believe is the more-important growth in pre-tax earnings—which shows the true, underlying earnings power of companies because the one-time effects related to the Trump tax reforms aren’t included.

As the chart indicates, the Fund’s holdings achieved higher earnings growth than the benchmarks’ holdings on both a pre-tax basis and an after-tax basis. Please note that the differences in the Fund’s bar heights compared to the benchmarks’ bar heights are more pronounced for pre-tax earnings growth—suggesting that we are, indeed, zeroing in on companies with earnings potential that goes well beyond the shorter-term, macro-level tax-reform effects enjoyed by companies generally.

Chart 1

Coming back to our comments about the economy, U.S. gross domestic product (GDP) grew at an annualized rate of 2% in the first quarter of 2018. While this increase was lower than expected, other recent quarterly increases were much higher. And the second quarter of 2018 showed signs of a very significant reacceleration, perhaps to a rate over 4%. Apparently, the Federal Reserve (Fed) felt comfortable with the economic progress and hiked interest rates for the second time this year. Fed Chairman Jerome Powell said U.S. growth looked robust enough to support the central bank’s continued normalization of monetary policy. And two more rate hikes are still expected before year-end.

At least so far, monetary policies haven’t created any major economic problems in the U.S. The yield curve has flattened somewhat, which means that short-term interest rates have risen more than long-term rates. But we’re not seeing signs of a recession, which might be more likely if short rates were to actually rise above long rates.

Regarding U.S. fiscal policies, we haven’t seen the kind of excessive spending that often leads to overinvestment by corporations and, eventually, to economic retrenchment. It’s important to remember that an economy doesn’t weaken based on some arbitrary timeframe. An economy weakens when imbalances get too large. And the current U.S. economy seems both relatively stable and strong—geopolitical factors aside.

For the most part, we’re also sanguine regarding Europe, where economies have been strong enough for the European Central Bank to begin tapering monetary stimulus. Japan, on the other hand, is still in easy-money mode. But Japan’s inflation rate remains extremely low, corporations are doing remarkably well, and we’re witnessing a vibrant environment for small businesses and initial public offerings (IPOs). Overall, Europe and Japan appear to be just several years behind the U.S., but on similar economic paths.

As for emerging-market countries, they were out of favor with investors during the second quarter, at least partially as a result of higher U.S. interest rates and a stronger dollar. But at the individual-company level, we see plenty of reasons for optimism—among them, reasonable valuations and enormous headroom for growth. Given the solid prospects of emerging-market companies, we think the aggressive flows into the U.S. dollar are probably overdone.

MARKETS

Toward the end of the second quarter, the threat of a U.S.-China trade war seemed to rattle the U.S. stock market. But overall, investors basically shrugged off the heated rhetoric setting fire to Twitter and emblazoning newspaper headlines. As with any high-stakes negotiation—the U.S.-North Korea nuclear summit also comes to mind—it’s hard to know what is simply bluster that will resolve itself with less drama than pundits predict.

In our view, the smart approach to addressing geopolitical risks is to stick with a well-thought-out, time-tested investment discipline. As bottom-up investors, our discipline emphasizes individual companies’ prospects. Of course, those prospects are affected by what’s happening in a broader context. For this reason, we may identify themes that are broader than a single company—for example, retailers that are somewhat insulated from the “Amazon effect.” But ultimately, any theme we identify is simply a collection of similar observations that play out at an individual-company level.

And here’s what we’re seeing among the individual companies in our Funds: growth. As described above, based on the most-recent quarterly data available, companies in the Russell 2000 and the Russell 2000 Growth indexes grew both pre-tax and after-tax earnings at double-digit annualized rates. Moreover, companies in the Wasatch Core Growth Fund grew earnings even faster.

Consistent with the generally positive news regarding the American economy and corporate earnings, stocks in the U.S. mostly traded up during the second quarter. The large-cap S&P 500® Index advanced 3.43%. The technology-heavy Nasdaq Composite Index gained 6.61%. The Russell 2000® Index of small caps rose 7.75%. Growth-oriented small caps performed extremely well too, with the Russell 2000 Growth Index up 7.23%. Value-oriented small caps in the Russell 2000 Value Index were even bigger winners at 8.30%—although this performance appeared to be an anomaly, as value stocks across larger market capitalizations generally lagged growth stocks by wide margins.

Consistent with fairly modest moves in interest rates during the second quarter, U.S. bond markets were relatively flat. The intermediate-term Bloomberg Barclays US Aggregate Bond Index lost -0.16% and the long-term Bloomberg Barclays US 20+ Year Treasury Bond Index returned 0.35%. Going forward, unlike many market pundits, we’re not necessarily bearish on U.S. bonds because we think extremely low interest rates overseas may keep U.S. interest rates from rising too dramatically.

International stock markets, for the most part, didn’t fare as well as those in the U.S. The MSCI World ex USA Index lost -0.75% and the MSCI Emerging Markets Index fell -7.96% for the second quarter.

So why did stock markets around the world perform as outlined above? Regarding U.S. small caps versus large caps, investors favored smaller companies probably because these companies tend to be more domestically focused, and therefore more insulated from international trade tensions and the higher value of the dollar. A longer-term indication of the health of small caps was that, according to financial-data provider Dealogic, 2018 year-to-date IPOs occurred at the fourth-busiest rate on record.

As mentioned, to the surprise of many pundits, growth-oriented stocks continued a longer-term trend of generally outperforming value-oriented stocks. The reason may have to do with investors recognizing the propensity of growth-oriented companies to implement the most-innovative business models and technologies that will be necessary to support expansion in an economy that’s already seeing close to full employment. This trend favoring high-quality, growth-oriented companies has mostly worked to our advantage at Wasatch Advisors.

Regarding U.S. markets compared to international markets, we think the recent outperformance by the U.S. was the result of a massive “risk-off trade” in which geopolitical events caused investors to view the U.S. as a safe haven—with heightened challenges in other developed markets and even greater challenges in emerging markets. There were also some hiccups in world-wide economic progress. But, as already discussed, we think many international economies—both developed and emerging—are on economic paths similar to that of the U.S., just several years behind.

Where do we go from here? Our assessment is that although U.S. valuations are relatively high, well-chosen companies are priced roughly consistent with realistic growth expectations. And valuations in international developed countries are generally more attractive, although selectivity is essential because economic growth is less consistent. As for emerging-market countries, differences from one economy to the next are even greater, but—for investors who are willing to put boots on the ground—companies with the most-compelling valuations and the largest prospects for growth can be found in emerging markets.

In terms of potential trouble spots, we agree with the likes of Warren Buffett in that we don’t spend much time worrying about macro risks—whose effects are very difficult to predict and whose challenges are often resolved without the permanent destruction of capital. Just consider some of the biggest macro events of our generation. Now think about whether or not you could have really predicted them ahead of time. Even more important, if you had predicted them, would that have told you where the markets would be a year, five years or 10 years later?

At Wasatch, what we’re more concerned about are the risks of overpaying for stocks whose valuations aren’t justified by the fundamentals of the underlying companies. And in an environment of generally elevated stock prices like we have today, those company-specific risks are higher than normal. This is why we believe bottom-up research, including discussions with management teams and on-site visits, is more important than ever.

With sincere thanks for your continuing investment and for your trust,

JB Taylor

RISKS AND DISCLOSURES

Mutual-fund investing involves risks, and the loss of principal is possible. Investing in small-cap funds will be more volatile, and the loss of principal could be greater, than investing in large-cap or more diversified funds. Investing in foreign securities, especially in frontier and emerging markets, entails special risks, such as unstable currencies, highly volatile securities markets, and political and social instability, which are described in more detail in the prospectus.

An investor should consider investment objectives, risks, charges and expenses carefully before investing. To obtain a prospectus, containing this and other information, visit www.WasatchFunds.com or call 800.551.1700. Please read the prospectus carefully before investing.

The Wasatch Core Growth Fund’s primary investment objective is long-term growth of capital. Income is a secondary objective, but only when consistent with long-term growth of capital.

Wasatch Advisors is the investment advisor to Wasatch Funds.

Wasatch Funds are distributed by ALPS Distributors, Inc. (ADI). ADI is not affiliated with Wasatch Advisors, Inc.

Information in this document regarding market or economic trends, or the factors influencing historical or future performance, reflects the opinions of management as of the date of this document. These statements should not be relied upon for any other purpose. Past performance is no guarantee of future results, and there is no guarantee that the market forecasts discussed will be realized.

© 2018 Wasatch Funds. All rights reserved. Wasatch Funds are distributed by ALPS Distributors, Inc. WAS004735 Exp: 10/30/2018

Wasatch Advisors

Read more commentaries by Wasatch Global Investors