Although markets were less turbulent in the second quarter than the first, volatility persisted as investors shifted their focus from improving U.S. growth data to trade, currencies and diverging monetary policies. As we enter the second half of the year, the U.S. economic expansion continues, supported by an upbeat consumer, strong corporate earnings, contained inflation, deregulation and tax reform. Outside the U.S., the softening economic data and signs of rising credit risk call for added caution but do not preclude investment opportunities. Our positioning reflects the following beliefs:

- Fears of an imminent U.S. recession are premature; tax policy and a more business-friendly regulatory environment provide long-term catalysts for the economy.

- Although conditions outside the U.S. are less encouraging, positive global growth should continue, albeit with growing divergence among countries.

- Mid-term elections, trade concerns, more normalized U.S. interest rates, and a higher level of global economic uncertainty will fuel volatility into the autumn. This turbulence does not signal the end of the bull market in equities.

- The risks to watch most closely include continued tightening of global liquidity conditions, heightened escalation in trade uncertainty, and building political pressures in the EU.

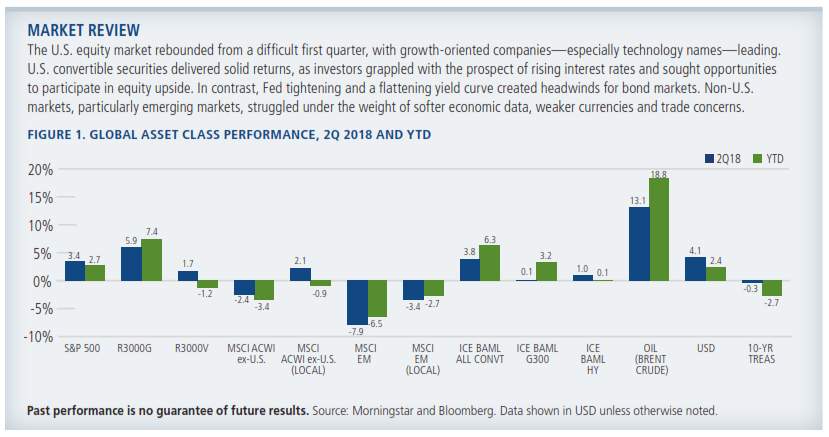

Figure 1: Market Review

United States

Propelled by the tailwinds of deregulation and tax reform, the U.S. economy is positioned for continued growth. Encouraging employment data, rising home prices, healthy consumer activity, and improving sentiment in manufacturing are among the factors that support our positive outlook through the remainder of the year, and likely longer. Small and mid-size businesses, a key engine of economic activity, are also in growth mode. Wage growth has been subdued and inflation is within expectations. The Fed’s course to normalizing monetary policy has been gradual and largely expected. We expect corporate earnings announcements to be strong over these next weeks, as well as through the second half of the year. Higher oil prices, wages and tariffs should push up inflation modestly, but not to extremes.

Many investors have questioned how much longer this current expansion can last, as it has already run for more than nine years. For much of this period, growth has been unusually shallow, only shifting into higher gear more recently. As a result, we believe this expansion can be sustained further. (For more on this, see our recent post.) Although interest rates are rising, credit risk is still contained in the U.S., which supports our view that the end of the economic cycle is not imminent. As middle and lower income consumers strengthen their footing, they can help extend the current expansion. The full impact of tax reform and deregulation will be reaped over time, providing long-term growth catalysts for large and small businesses.

Nonetheless, we expect market volatility to increase as the cycle ramps up and the Fed continues tightening. Trade policy will be a key source of worry for investors, but we remain hopeful that what we are seeing now is setting the stage for more free and equitable trade over the long term. There may be near-term disruptions as policy takes shape, and we are closely monitoring corporate announcements to gauge the potential impact of tariffs on the earnings of specific companies and industries. As mid-term elections approach, market turbulence will grow. However, we could well see a post-election autumn rally as market participants shift their focus back to economic fundamentals.

Global and International Strategies

Trade, monetary policy and political uncertainties clouded the global equity markets during the quarter, and the near-term risks have increased. However, the skies could clear quickly. We are not ruling out a rebound this year, and the longer-term growth opportunities in global markets remain fully intact. In this environment, we have sought to reduce downside risk exposures without sidelining our strategies from participating in a near-term rebound. We maintain our emphasis on secular growth and cyclical growth areas, with less exposure to defensive areas. As always, we are seeking out the best bottom-up opportunities—those with quality fundamentals and accelerating growth characteristics. Emerging markets, including China, remain well represented in our portfolios, but we have brought down our allocations from higher levels earlier in the year.

Several factors have contributed to our current positioning. The softening in non-U.S. economic data in the second quarter, rising geopolitical tensions in Europe and very public trade negotiations occurred as the U.S. economy began to surprise on the upside again. Also, the Fed has diverged from the more accommodative European Central Bank and the Bank of Japan, and the impact of U.S. dollar repatriation from tax reform is beginning to play out. As a result, global financial conditions have tightened, putting pressure on risk assets, particularly outside the U.S. The U.S. dollar’s strength is evidence of some of these stresses and highlights the vulnerability of some developing economies that are more reliant on capital flows for funding. Additionally, recent Fed comments have signaled that it may implement monetary policy with less regard for international financial stability than markets have grown to expect.

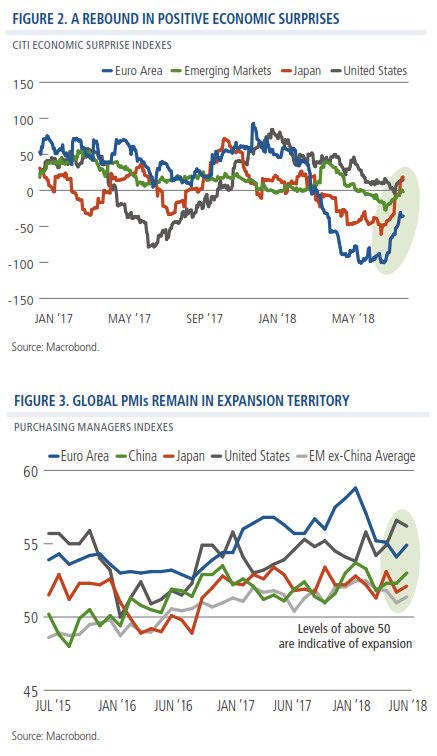

However, there have been early fundamental signals that the European and Chinese economies are reaccelerating. Economic surprises have ramped up again and PMI data has returned to a favorable trend (Figures 2 and 3). Further improvements in economic data over these next weeks would indicate that the recent weakness was an “air pocket,” similar to what we’ve seen several times during the U.S. recovery. This could buoy the global markets rapidly, particularly if trade tensions deescalate.

Figures 2 and 3

Convertible Securities

We believe this growth environment sets up well for our actively managed convertible strategies. For one, convertibles can benefit in an advancing but volatile equity market. (The embedded option to convert to common stock becomes more valuable as stocks rise, while bond characteristics provide potential downside protection when stocks decline.) Further, thanks to their equity characteristics, convertible securities have performed well versus bonds during periods of rising interest rates—including this most recent period.

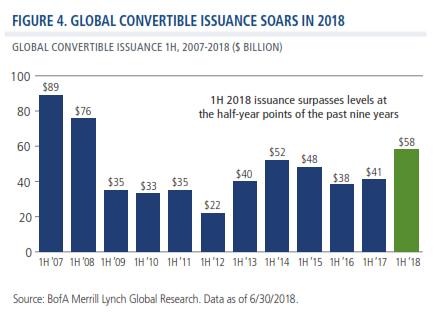

Convertible issuance has soared this year as companies have sought growth capital in a still-expanding economy. Rising interest rates and changes to U.S. tax laws have also made convertible securities a more attractive choice for issuers versus non-convertible debt. At $58 billion, global issuance for the first half of the year is running at the fastest pace since 2008 (Figure 4). U.S. companies have led the way, bringing more than $34 billion to market. There has also been a dramatic upswing in Asia ex-Japan issuance, where companies issued $12 billion.

This impressive issuance has given us opportunities to rebalance and enhance the risk/reward profiles of our portfolios. As we have discussed in the past, convertibles vary in their characteristics, which is why active management is so important. In 2018, more convertibles have come to market with structures that offer better potential downside protection during market corrections, which expands the opportunity set in the balanced portion of the convertible universe we favor. Additionally, the majority of convertible issuers have continued with the common practice of foregoing third-party credit ratings. Because we utilize a proprietary, comprehensive research process tested over decades, we do not see this as an obstacle. From a sector standpoint, we maintain an emphasis on companies in the technology, industrials, and consumer discretionary sectors and an underweight to defensive areas.

Figure 4

Fixed Income

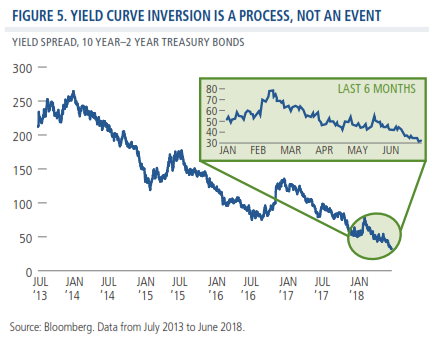

We expect the Federal Reserve to maintain its gradual tightening as the U.S. economy extends its growth phase, with short-term rates likely to rise at least three more times to reach 2.5% by next year. The yield curve has continued to flatten and is now approaching inversion, which has created agitation in some circles and raised fears of recession. While it is true that inverted yield curves have typically preceded recessions, yield curve inversion is better thought of as a process rather than a single event. As we explained in a recent post, the yield curve has been moving toward inversion for many years now, and the economy has kept going while the pressures have built. Once the curve inverts, historically we have seen lags of months—and at times, more than a year—between inversion and recession. So, an inverted yield curve does not toggle the economy from growth to recession overnight.

We are closely monitoring many other factors, in addition to Fed policy and the yield curve. These include tariff escalations (which have recently contributed to flight to quality), global oil production, and U.S. dollar strength and its impact on emerging market economies. In the economically sensitive high yield space, issuer fundamentals are attractive, but market dynamics have become more challenging. In contrast, in the more rate-sensitive investment grade market, we see supportive technicals and a less compelling fundamental picture. Much of the new corporate investment-grade issuance has been in BBB tier where the overall risk/reward characteristics hold less appeal. Further, in recent years, a number of investment-grade corporate issuers have experienced credit downgrades as they pushed their credit metrics to pursue strategic actions (such as buybacks).

Against this backdrop, active management and rigorous fundamental analysis are more crucial than ever. Across the bond market, we believe our core competency in credit analysis will be especially advantageous. Presently, our analysis has led us to favor asset-backed and corporate credits over Treasury bonds and mortgage-backed bonds. Within high yield, the team continues to build meaningful overweights in “best idea” issuers with improving fundamentals and debt-service capabilities. Our bond-by-bond, bottom-up portfolio approach includes a process for selecting preferred individual issues among those available from a “best idea” issuer dependent on bond structure and yield curve positioning. From a sector standpoint, this has led us to emphasize consumer non-cyclicals and energy credits.

Figure 5

Conclusion

The need for active risk management has increased at this point of the economic cycle. However, with appropriate attention to downside, there are ample reasons to maintain a well-diversified portfolio as the global growth story runs its course. We will continue to combine our understanding of the investment cycle, our proprietary research, and long experience investing through a variety of market settings. We believe this will allow us to properly position our clients for the environment ahead.

--

Indexes are unmanaged, not available for direct investment and do not include fees and expenses. The U.S. Dollar Index measures the value of the U.S. dollar relative to a basket of foreign currencies, including Euro Area, Canada, Japan, United Kingdom, Switzerland, Australia, and Sweden. The Russell 3000 Growth Index and Russell 3000 Value Index measure U.S. growth and value equities, respectively. The S&P 500 Index is considered generally representative of the U.S. equity market. The MSCI All Country ex U.S. Index represents the performance of global equities, excluding the U.S. The MSCI Emerging Markets Index is a measure of the performance of emerging market equities. The ICE BofAML U.S. High Yield Index is an unmanaged index of U.S. high yield debt securities. The ICE BofAML All U.S. Convertible Index (VXA0) is a measure of the U.S. convertible market. The ICE BofAML G300 Index measures the performance of 300 global convertibles. Oil is represented by current pipeline export quality Brent blend.

Purchasing Managers Indexes measure manufacturing sector strength. The Citi Economic Surprise Indexes are objective, quantitative measures of economic news that measure the difference between actual releases and the median of Bloomberg survey data. Dovish refers to economic policy that supports low interest rates to keep inflation in check. ICE Data: Source ICE Data Indices, LLC, used with permission. ICE permits use of the ICE BofAML indices and related data on an `as is’ basis, makes no warranties regarding same, does not guarantee the suitability, quality, accuracy, timeliness, and/ or completeness of the ICE BofAML Indices or data included in, related to, or derived therefrom, assumes no liability in connection with the use of the foregoing and does not sponsor, endorse or recommend Calamos Advisors LLC or any of its products or services.

Opinions, estimates, forecasts, and statements of financial market trends that are based on current market conditions constitute our judgment and are subject to change without notice. The views and strategies described may not be suitable for all investors. References to specific securities, asset classes and financial markets are for illustrative purposes only and are not intended to be, and should not be interpreted as, recommendations.

Calamos Investments LLC 2020 Calamos Court | Naperville, IL 60563-2787 800.582.6959 | www.calamos.com | [email protected]

Calamos Investments LLP 62 Threadneedle Street | London EC2R 8HP Tel: +44 (0)20 3744 7010 | www.calamos.com/global

©2018 Calamos Investments LLC. All Rights Reserved. Calamos® and Calamos Investments® are registered trademarks of Calamos Investments LLC. OUTLKCOM 18651 0618O C

This material is distributed for informational purposes only. The information contained herein is based on internal research derived from various sources and does not purport to be statements of all material facts relating to the information mentioned and, while not guaranteed as to the accuracy or completeness, has been obtained from sources we believe to be reliable.

NOT FDIC INSURED | MAY LOSE VALUE | NO BANK GUARANTEE

© Calamos Investments

Read more commentaries by Calamos Investments