Meal delivery services have been around for a long time. Most consumers have ordered pizza or Chinese food and had that food delivered. What appears to be new in recent months is that consumers are beginning to show a preference for having all types of restaurant food delivered as opposed to either picking it up or consuming it at a restaurant location. Delivery charges as high as ten dollars do not appear to be dissuading consumers from their preference for delivered meals.

For the restaurant industry, non-pizza delivery increased 20% last year to over 3% of total sales. Starting from a low percentage of overall sales, delivery is potentially incremental to the restaurants, and restaurants appear to be willing to give those economics to the emerging delivery services. Uber Eats, Grubhub, DoorDash, and Postmates appear to absorb over 20% of the total check, a figure equal to the margins of many restaurant chains. “We are losing money on delivery orders, or, best case scenario, breaking even,” said a New York restaurateur.

As for the delivery services themselves, a business model remains elusive. The industry is not profitable today, and experiments are ongoing on whether the restaurant or the consumer is the more important relationship, where to deliver, how fast to deliver, how far to deliver, and whether consumers prefer a transaction or a subscription model. Historically, last mile businesses of all sorts hinge on route density. In that vein, existing delivery systems may have the right stuff to address the growing consumer demand for delivered meals.

- Demand for restaurant meal delivery is growing fast.

- The early leaders in the market have contrastive strategies.

- Digital interfaces and route densities offer the clearest path to profits.

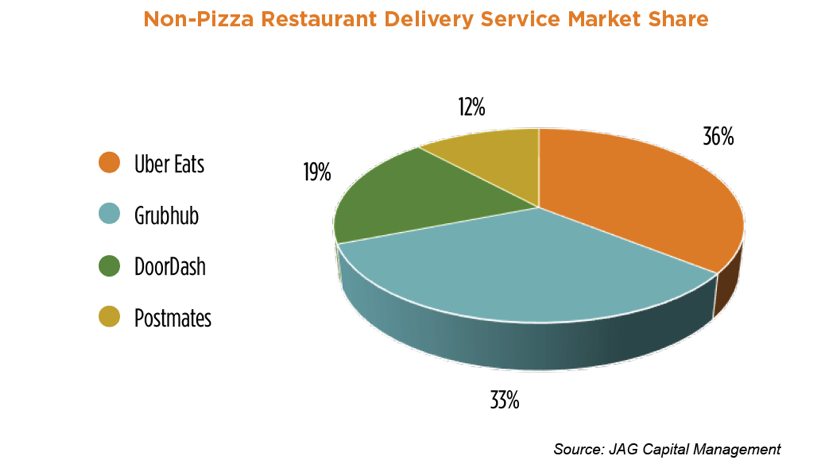

Uber Eats is a subsidiary of the Uber ridesharing business. They are currently expanding from about 110 markets to nearly 200, and the firm claims to be gross margin positive in 27 markets at present. Uber Eats uses regular Uber drivers for delivery, but they also have dedicated Uber Eats drivers. Recent management comments suggest they have found food delivery to be different from people delivery. Uber Eats is also unique in the industry in that they require customers to meet their delivery drivers outside.

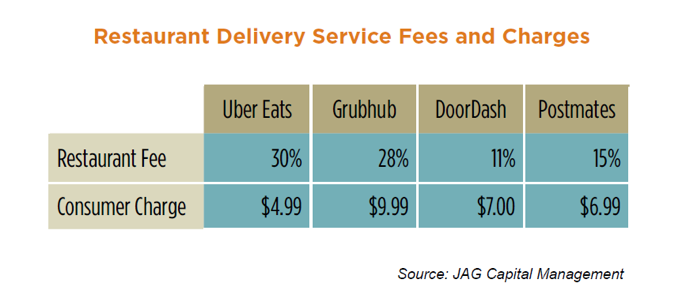

That’s probably not an issue for single family homes, but it may be a competitive issue for apartments and office complexes. That said, Uber Eats should be more cost efficient than door-to-door competitors. The business model for Uber Eats is to take 30% of the bill from the restaurant partner, and it charges a $4.99 booking fee to the customer. Uber Eats is believed to have about $750 million in revenues, but disclosures are scant.

Grubhub is often considered the leader in the restaurant delivery market, and they do have the highest gross revenue in the market. Gross revenue differs from net revenues in that gross revenue includes the cost of the delivered food, while net records include only the fees and charges earned. Net sales are near $700 million, putting Grubhub second in net market share. Grubhub has designed its system so that drivers are independent contractors, working for themselves and not for Grubhub. Lawsuits have already been filed contesting this arrangement, and we’ll see how that goes. As for financials, Grubhub’s asset light approach makes it the only profitable restaurant delivery service at present. Grubhub assesses an average 17.5% listing fee to its restaurant partners to access its digital platform. In addition, the firm charges a 10% delivery fee for a total assessment to the restaurant of 27.5%. Grubhub charges customers $9.99 per delivery with a $50 minimum. Grubhub is the only restaurant delivery service with a minimum. This minimum may prove interesting given Grubhub’s newly announced relationship with Yum Brands whose restaurants have an average check in the $6 range.

DoorDash’s approach to the home delivery market is to maximize restaurant partners. For example, a recent article in Indystar reported that DoorDash had 122 restaurant partners, double competitor restaurant listings. DoorDash may have been too aggressive in recruiting restaurant partners. In-&-Out Burger expressed disappointment with the partnership, and Taco Bell quit DoorDash to go to Grubhub. DoorDash recently upped the ante by offering shared space to restaurant partners. DoorDash charges restaurants about 11% for listing on the service, and they have a variable delivery and service charge which averages $7.00 per delivery (ranges from $0 to $9.99 depending on demand volume). DoorDash has $400 million in net revenues, and they burned through $140M in cash last year. DoorDash attracted a well-heeled partner earlier this year, convincing Softbank to inject $540 million in new capital into the business.

Postmates is the subscription model in restaurant delivery. Postmates assesses customers $9.99 per month for a month-to-month subscription or $6.99 per month for an annual subscription. There are additional delivery fees for orders under $20, but otherwise, Postmates will deliver anything, meals, groceries, cold remedies, whatever. The average fee to restaurant partners is 15%. Postmates is the most widely distributed restaurant delivery service with service in 385 markets, and Postmates is the only restaurant delivery service that promises delivery in 35 minutes or less. It also seems more technology connected than competitors, recently experimenting with robots, and separate interfaces like Snapchat. Despite the broad availability, Postmates is believed to generate only $250 million in net revenue, making them the smallest of the bigger companies in the market. Postmates lost $75 million last year, and they have confirmed previous merger discussions with DoorDash. A new relationship with Chipotle may give Postmates a needed boost.

Time and Distance

Consumers want meal delivery service, and they appear to be willing to pay for it. However, neither the restaurants nor the delivery services have found a route to profits. Delivery services have several exogenous factors with which to contend: dwell time, parking, re-deliveries, and route density.

Restaurants require time to prep and package food, and often those time requirements expand during busy periods. Reports suggest that 10 minute wait times for delivery drivers to acquire the ordered meals are not infrequent. Parking is another issue for delivery services in that drivers have to park twice, once at the restaurant and once at the customer location. Parking twice can add time and, in some cities, incur additional fees. Along with dwell time and parking, re-delivery adds complexity to the restaurant meal delivery model. If a mistake is made in the order, like the wrong item is delivered or the on-the-side salad dressing was not packed, the food needs to be re-delivered, potentially doubling the time spent on an order. Finally, significant efficiencies can be gained if more than one delivery can be made each time the driver leaves a restaurant or group of restaurants. Given that food is perishable and must be delivered appropriately hot or cold, synchronizing orders can prove difficult.

Blog sites indicate that Postmates has sent drivers as far as 11 miles one-way from a restaurant on a delivery run. We think that may be the extreme; whereas, the norm is closer to 9 miles round-trip for a restaurant meal delivery. To travel 9 miles at 35 miles per hour, the trip would take about 15 minutes. Adding on 5 minutes for dwell time, parking, customer interaction, and potential mistakes, it would take 20 minutes to make the average delivery. As a figure representative of the industry, Glassdoor reports that Grubhub drivers make $12 per hour on average and that data would point towards a driver cost of $4 per order. Adding to that, the delivery services tend to pay mileage one-way on each order at about $0.60 per mile, which we will round up to $2.75 per order. In sum, average delivery cost nears $6.75 per order. At that expense, most of the industry breaks even or loses money comparing delivery cost to delivery and booking fees charged.

Digital or Density

With delivery operating at or below breakeven and the restaurants themselves operating at or below breakeven on delivery orders, what is the profit model to satisfy consumer demand for delivered meals?

Uber Eats, Grubhub, DoorDash, Postmates, and the like, would make the case that the listing fee is their profit opportunity. Each of these firms earns a fee for providing a digital, mobile customer interface. Like ad-driven websites, such as Google and Facebook, these firms charge increased fees for more prominent listings, better graphics, improved targeting, and couponing. These capabilities do appear to add value, but it’s fair to doubt that value given that the restaurant partners often fail to profit from delivery service.

While customer interface platforms may or may not ultimately produce a return on investment, earning a profit on delivery may be possible with increased route density. Route density can be achieved with shorter length of haul, a regular route (if demand supports it), or an optimized path to multiple stops.

Several technology businesses offer route optimization software and those are likely to be utilized by restaurant meal delivery services going forward. That will help some. However, there is precedent in the industry for shorter delivery routes.

Domino’s (Pizza) has over 5,000 domestic locations. That degree of physical store presence gives Domino’s the ability to have short delivery routes, believed to be near five miles roundtrip. At such a length, the average delivery takes 12 minutes. Domino’s employs its drivers directly, and they pay the Federal hourly minimum for employees with tip income. That cost is just over $7 per hour. Domino’s compensates for mileage at a flat rate of $1.10 per delivery, so the average cost of delivery for Domino’s is $2.50 per order. Except during promotional periods, they charge $3 per delivery, so Domino’s is making a 20% profit on its delivery service. Low employment costs are possible due to the driver’s ability to earn tip income on 4-5 deliveries per hour. Low mileage compensation is possible due to shorter routes.

Domino’s continues to shorten delivery routes by splitting franchise territories to locate stores closer to customers. Should Domino’s get into the business of distributing meals from other restaurants, it would likely overwhelm the upstart delivery vendors. Domino’s is estimated to be more than ten times the size of the entire non-pizza restaurant delivery industry.

Conclusion

In looking for a success path for the restaurant meal delivery service industry, JAG would favor companies providing delivery service to proximate restaurants rather than those focused on assembling a larger suite of restaurants, and we would favor short delivery routes as opposed to longer ones. High delivery charges, like $9.99, make more sense short-term to account for rising demand and high costs. Looking longer term, delivery services taking a lower percentage of the restaurant check is probably necessary over time in order for the food providers themselves to maintain viability. Finally, big pizza could disrupt this market quickly. JAG investments will continue to position for the evolving trend of restaurant meal delivery.

These comments were prepared by Joseph Kinnison, CFA, an analyst, of JAG Capital Management, LLC, an SEC registered investment advisor. The information herein was obtained from various sources believed to be reliable; however, we do not guarantee its accuracy or completeness. The information in this report is given as of the date indicated. We assume no obligation to update this information, or advise on further developments relating to securities discussed in this report. Opinions expressed are those of the advisor listed as of 7/18/18 and are subject to change without notice. Opinions of individual representatives may not be those of the Firm. Additional information is available upon request.

The information contained in this document is prepared for general circulation and is circulated for general information only. It does not address specific investment objectives, or the financial situation and the particular needs of any recipient. Investors should not attempt to make investment decisions solely based on the information contained in this communication as it does not offer enough information to make such decisions and may not be suitable for your personal financial circumstances. You should consult with your financial professional prior to making such decisions. For institutional investors: J.A. Glynn Investments, LLC, and JAG Capital Management, LLC, both have reasonable basis to believe that you are capable of evaluating investment risks independently, both in general and with regard to particular transactions or strategies. For institutions who disagree with this statement, please contact us immediately.

Market Index performance statistics are provided by Advent Axys via benchmark data from FT Interactive Data and are presented for the time frame noted. Individuals cannot invest directly in an index. PAST PERFORMANCE SHOULD NOT BE CONSIDERED INDICATIVE OF FUTURE PERFORMANCE. ANY INVESTMENT CONTAINS RISK INCLUDING THE RISK OF TOTAL LOSS.This document does not constitute an offer, or an invitation to make an offer, to buy or sell any securities discussed herein. J.A. Glynn & Co., JAG Capital Management, LLC, and its affiliates, directors, officers, employees, employee benefit programs and discretionary client accounts may have a position in any securities listed herein.

Nothing in this document is intended as an offer or a recommendation to purchase or sell securities.

© JAG Capital Management, LLC

Read more commentaries by JAG Capital Management