The Dynasty Economic & Market Outlook: Volatility is the New Black

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsTopics for discussion

- Economic Outlook – “It’s a Mad Mad Mad Mad World”

- Market Outlook – “Volatility is the New Black”

- Building “All Weather” Portfolios

Economic Outlook: “It’s a Mad Mad Mad Mad World”

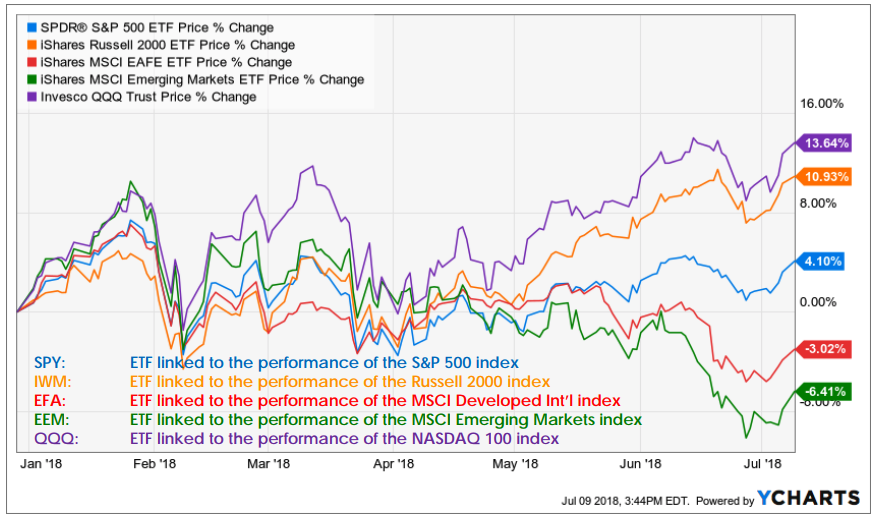

Divergence is the new kid in town

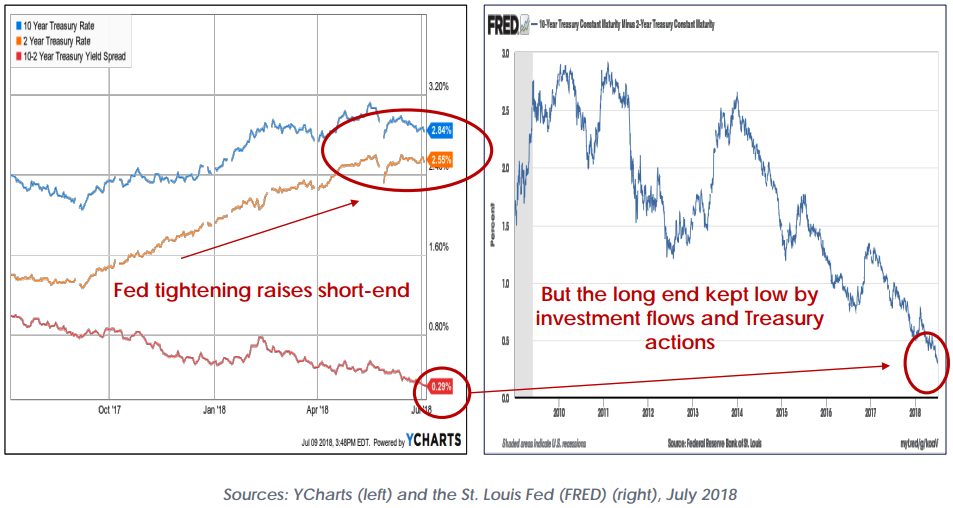

Yield curve getting flatter…

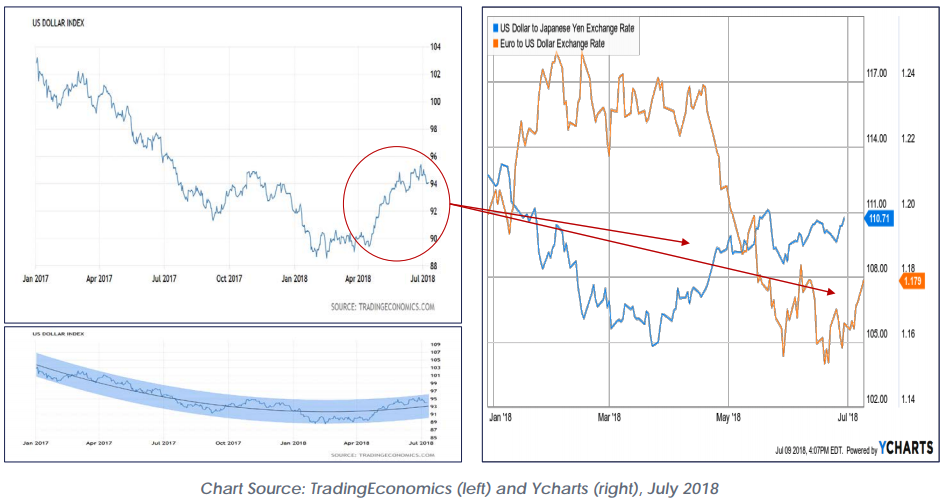

USD finally behaving as we expected

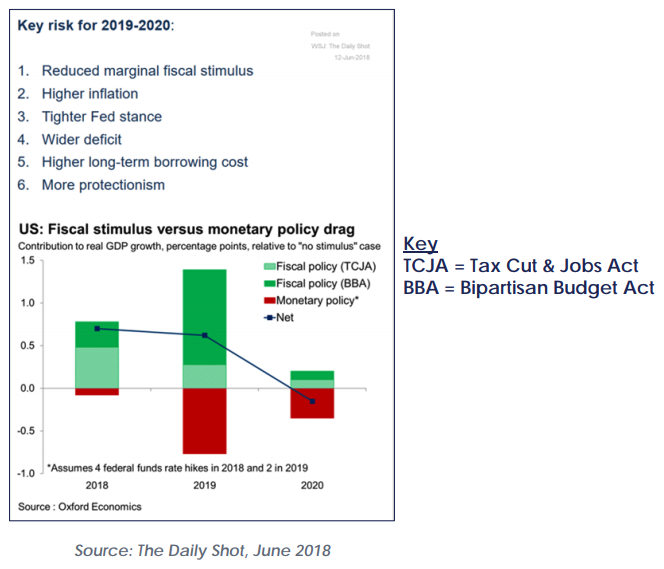

The fiscal vs. monetary tug-of -war

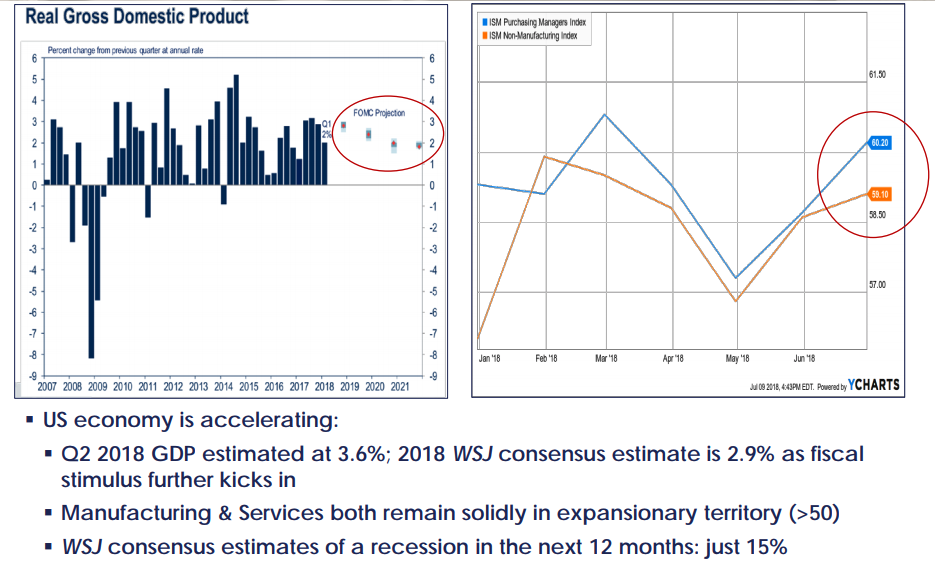

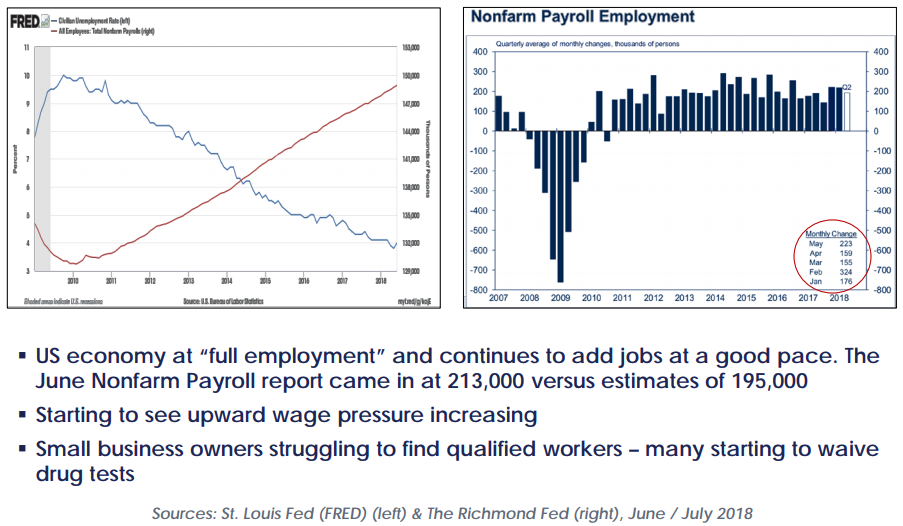

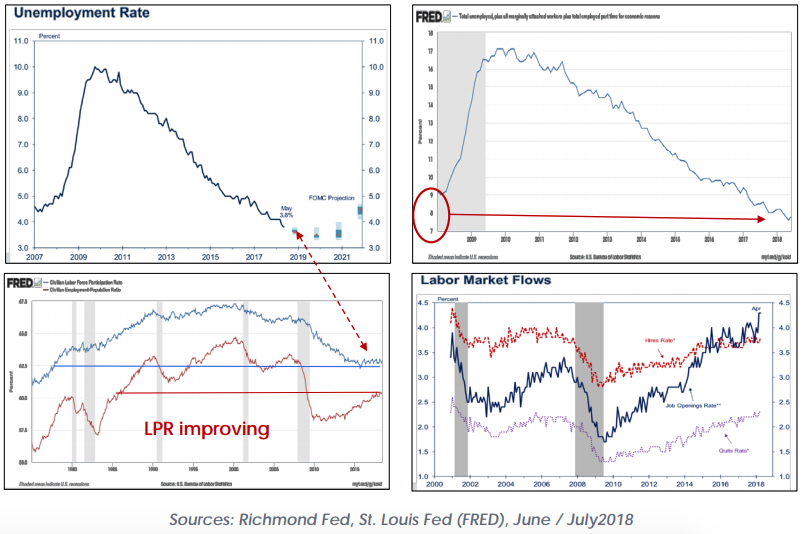

US economy gaining speed

![]()

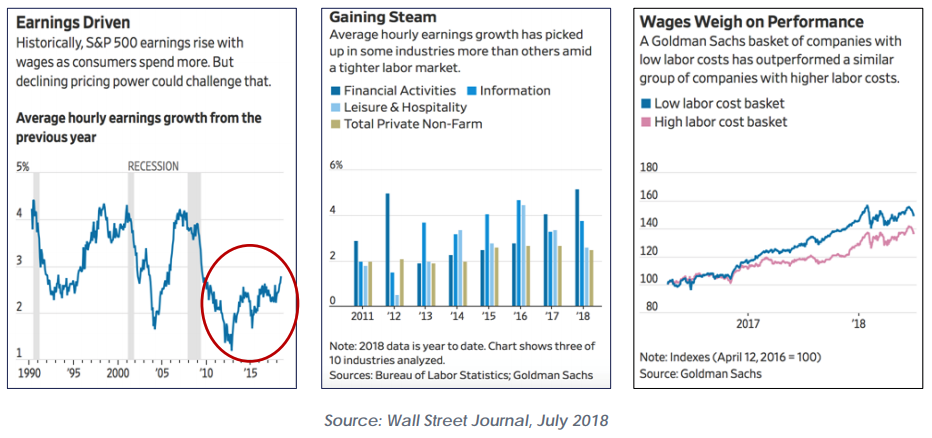

Wage inflation starting to kick in

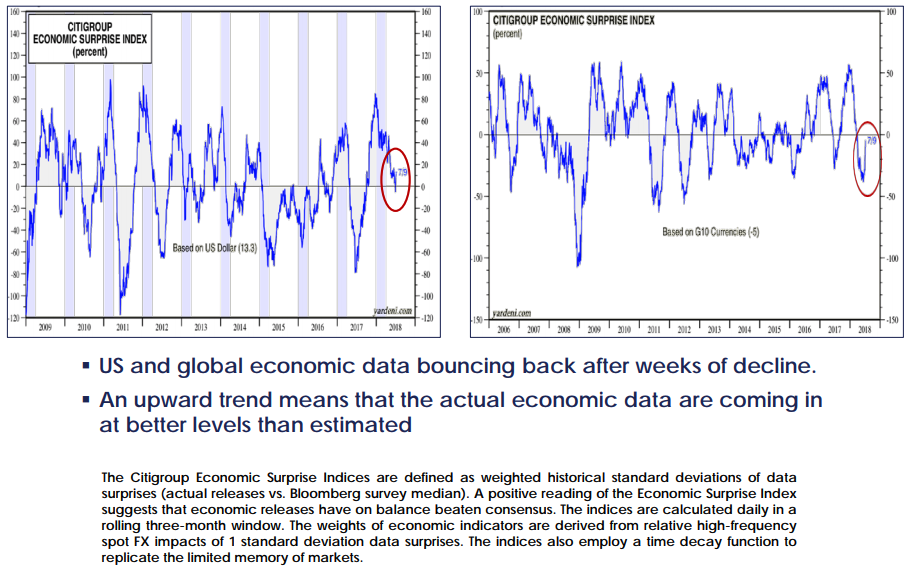

Some signs of economic “decoupling”

![]()

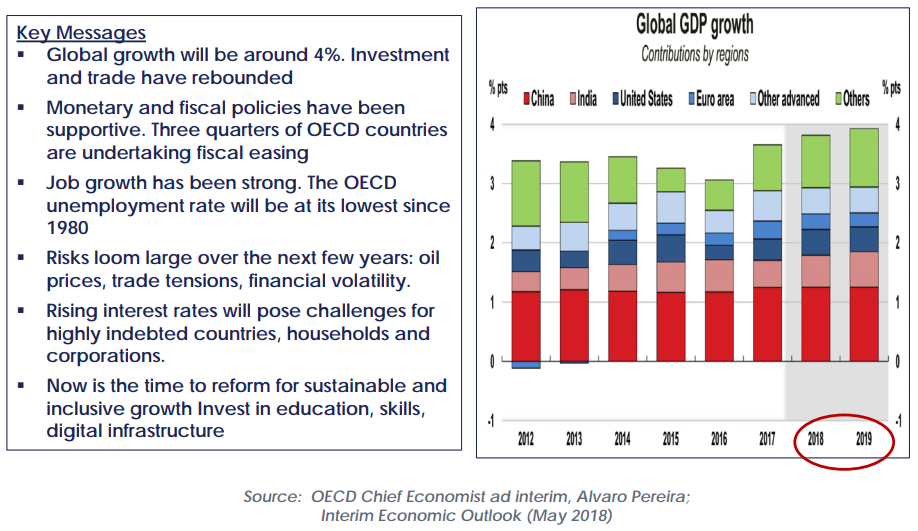

Global economy remains positive

Labor squeeze = wage inflation

The numbers behind the number

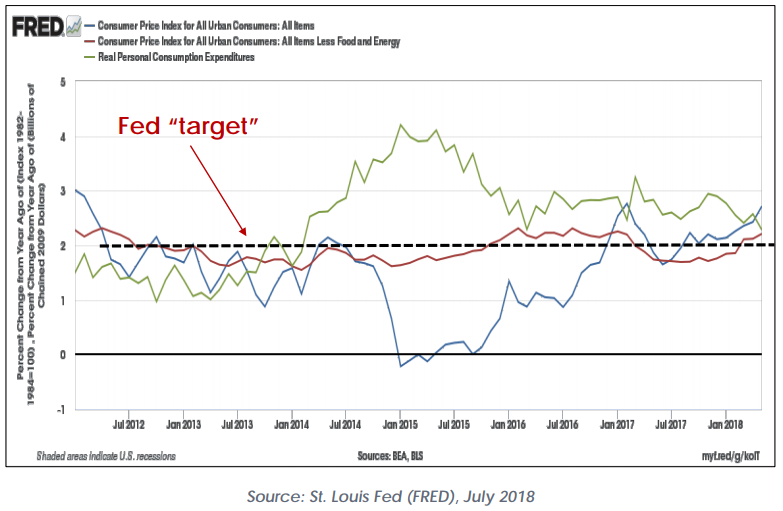

Inflation rising slowly but surely

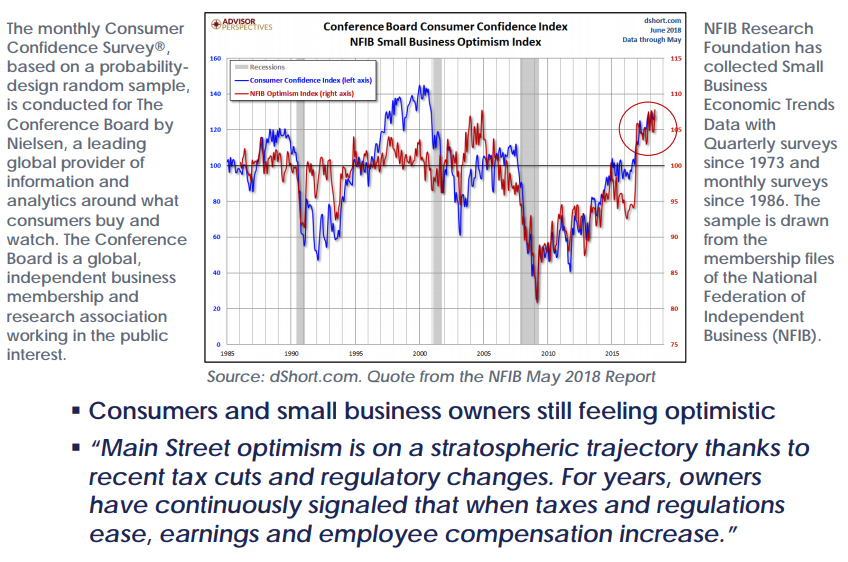

Sentiment high and improving

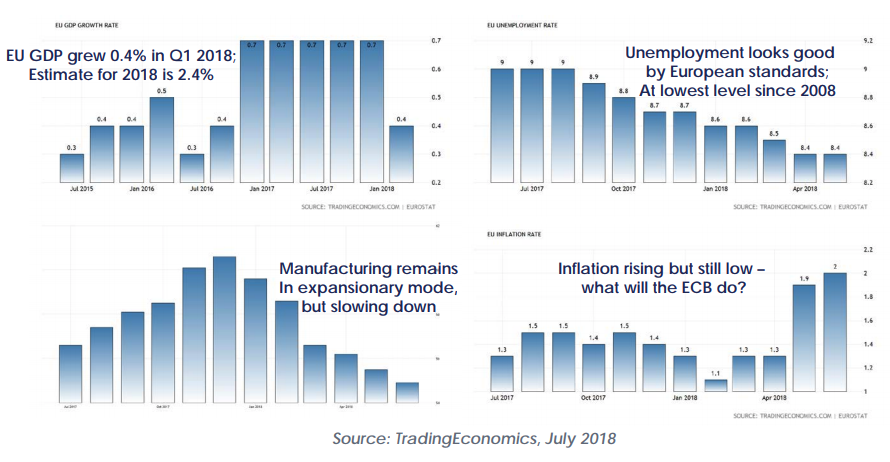

Euro area starting to decelerate

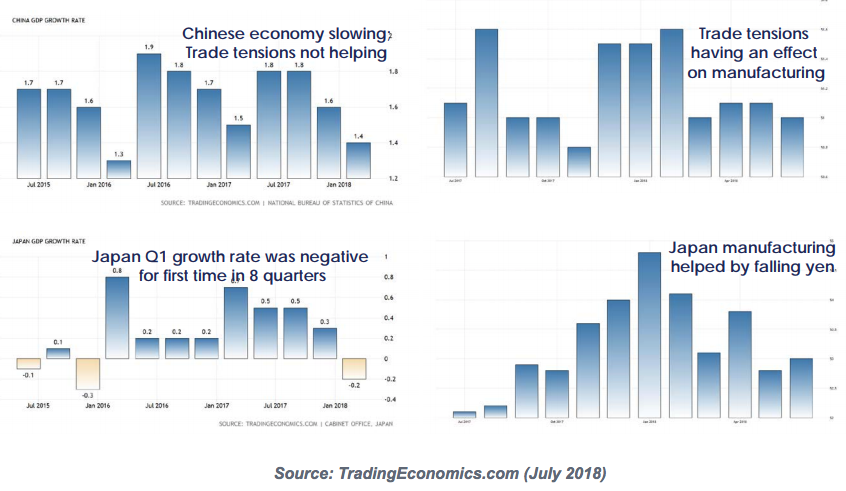

Japan and China ok, but slowing

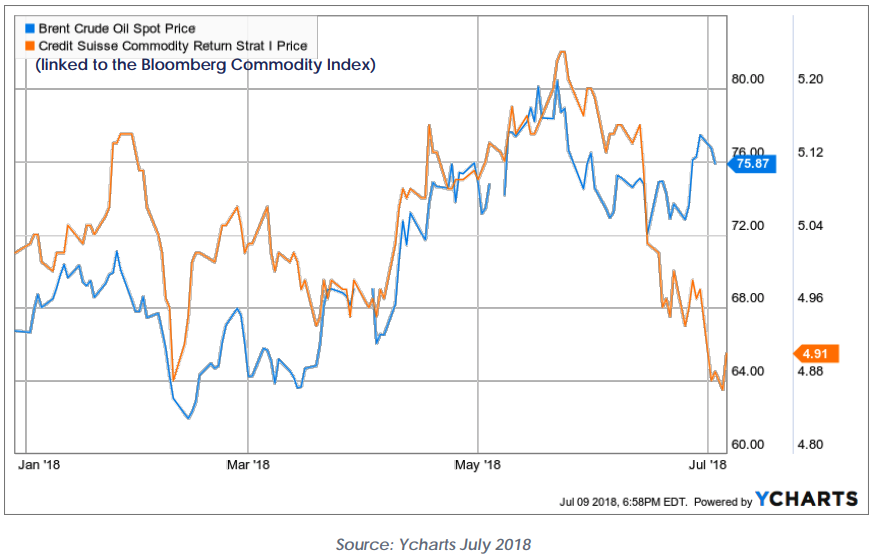

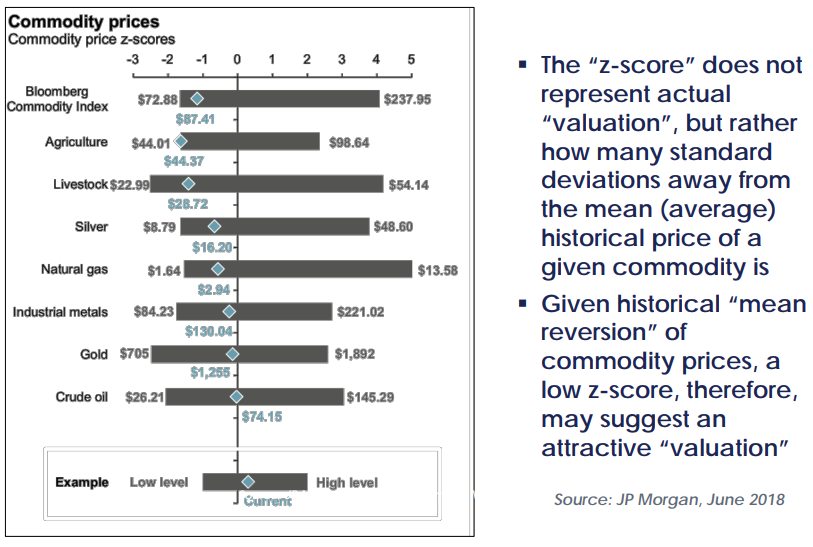

Divergence between oil and other commodities

How we see the world…

The word for the current state of affairs is desynchronization:

- The consensus estimate for Q2 GDP growth in the US is a sizzling 3.6%. GDP growth is expected to remain strong but decelerate through Q3 (3.0%) and Q4 (2.9%); (source: The Wall Street Journal);

- There remains some uncertainty regarding this forecast, however, as the outcome of ongoing trade negotiations could change the economic outlook for the US over the remainder of the year;

- Specifically, current trade negotiations seem to be taking a protectionist-leaning turn for the worst, which has already resulted in retaliation policies that will affect both inflation and global growth. Of specific concern are agricultural products, including soy beans, which are a major source of exports to China;

- Politically, these policies affect many of the voters who helped propel Donald Trump into office. We can expect that Congress people and Senators from states most affected by increased tariffs will increasingly speak out against current policy;

- Both the US manufacturing and services sectors remain well in expansionary mode (58.7 and 58.6 in May, respectively; any reading above 50 is considered expansionary), and after several month-overmonth declines seem to be accelerating again;

- The manufacturing index has been in expansionary territory for 109 consecutive months, while the non-manufacturing index notched its 100th consecutive expansionary month (source: Institute for Supply Management);

- Inflation (as measured by CPI) rose 2.8% year-over-year in May, slightly above market expectations, driven largely by increases in gasoline and housing costs;

- The Personal Consumption Expenditure (PCE) index – which is the Fed’s preferred measure of overall inflation, increased 2% year-overyear in May, in line with the Fed target rate (source: TradingEconomics);

- We continue to believe that inflation will tick up over the rest of this year, but that it does not yet constitute a primary risk to economic growth. Further, we continue to believe the Fed will allow inflation to run slightly “hot” before stepping in more aggressively;

- After raising rates (as expected) in mid-June, the consensus estimates are that the Fed will raise rates at least two more times in 2018. This may change depending on what unfolds with the outcome of current trade negotiations – a negative turn of events may slow down the planned steady tightening initiatives;

- After a sharp decline in yields in late May due to the Italian political crisis, interest rates continued their “grind higher” path through most of June, before dropping yet again toward month-end as trade war fears swept the market. The 10-year Treasury yield is once again below the mental barrier level of 3%, currently trading at approximately 2.9%;

- We maintain our outlook that rates in the US generally will inch steadily higher, with periodic reversals during market disruptions;

Market Outlook: “Volatility is the New Black”

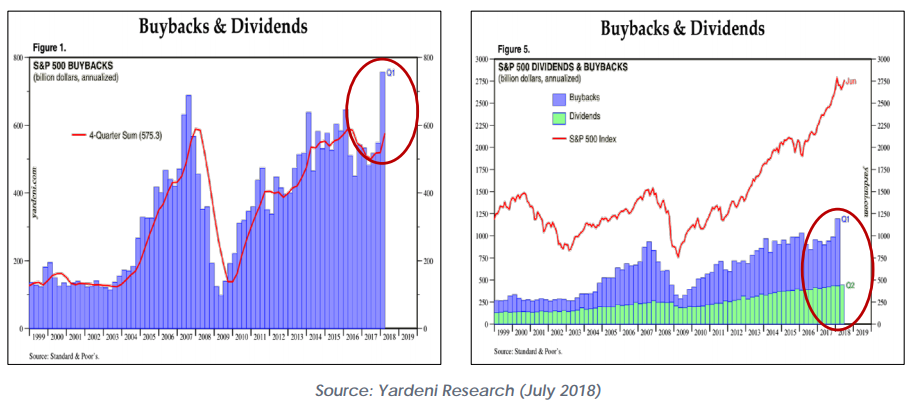

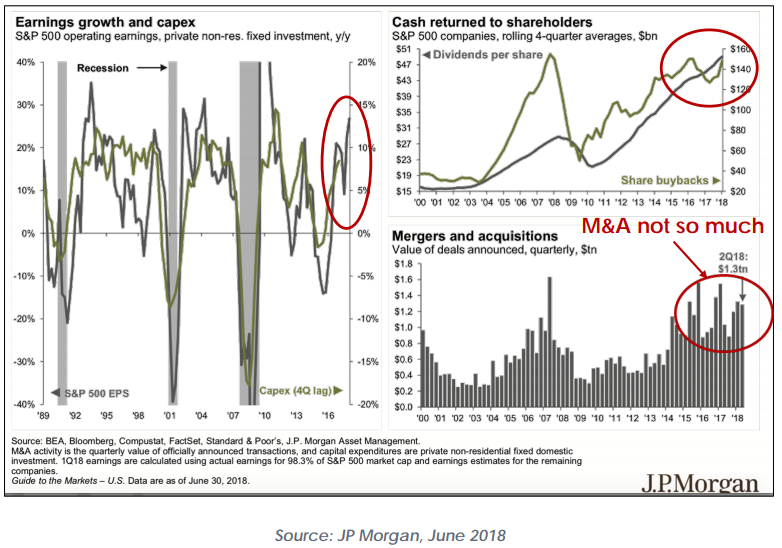

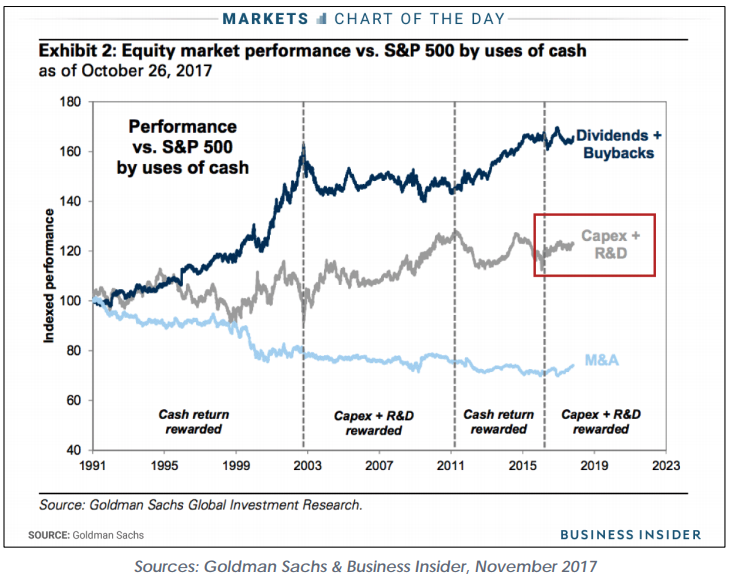

Tax reform driving share buybacks

But CAPEX and dividends also improving

But companies just doing what shareholders prefer

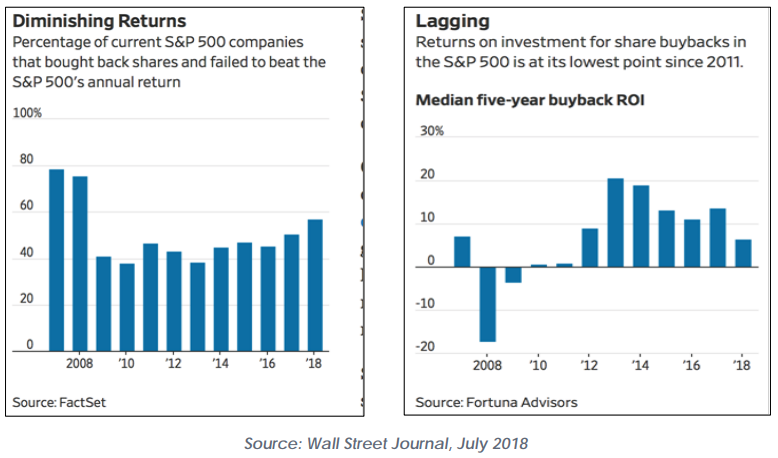

But is the bloom coming off the rose for financial engineering?

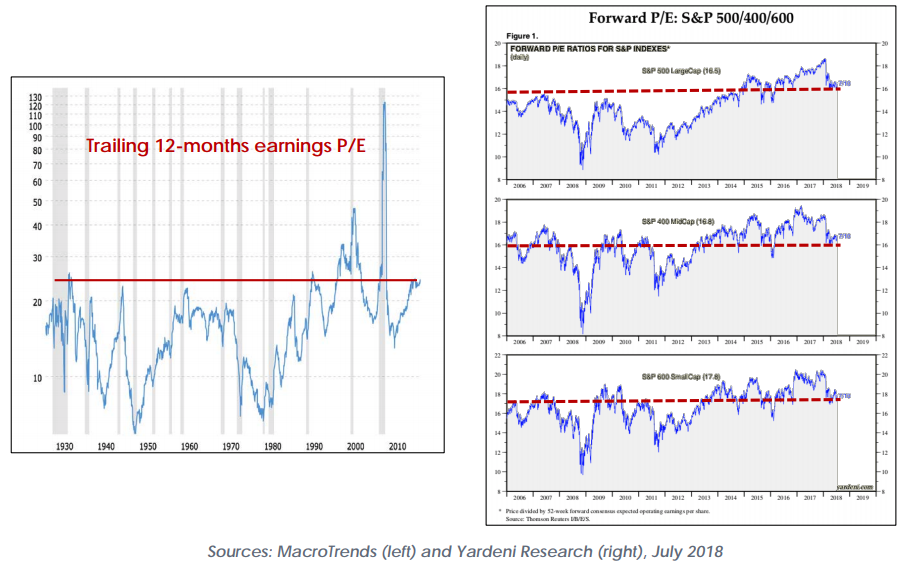

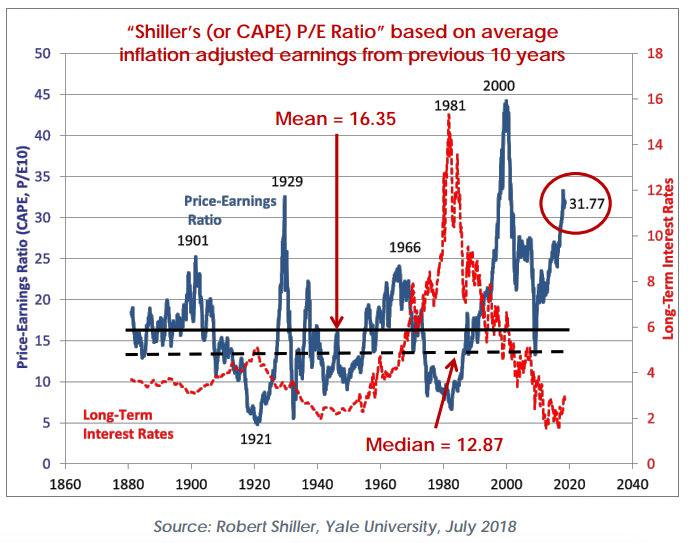

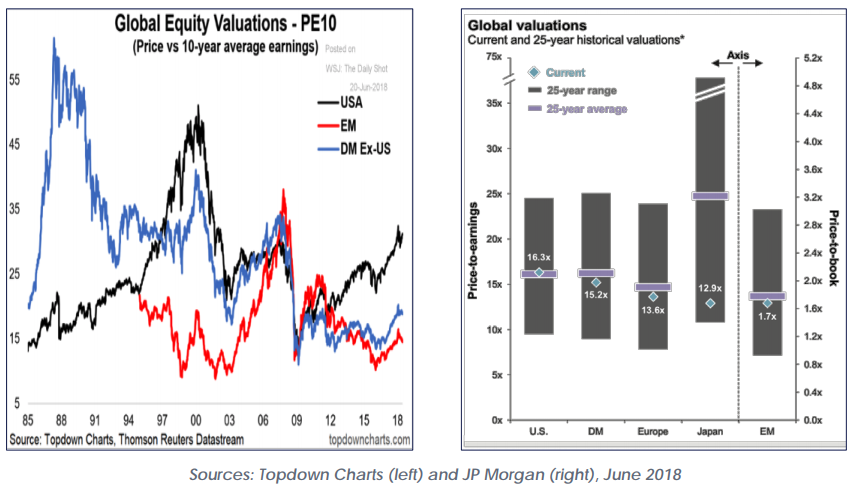

Mixed signals on valuations

Cape fear?

Non-US valuations look more attractive, but risks are higher

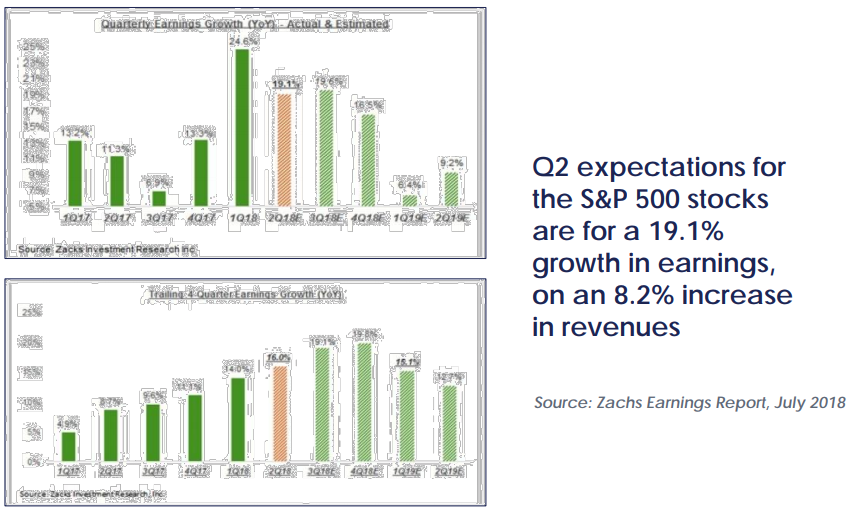

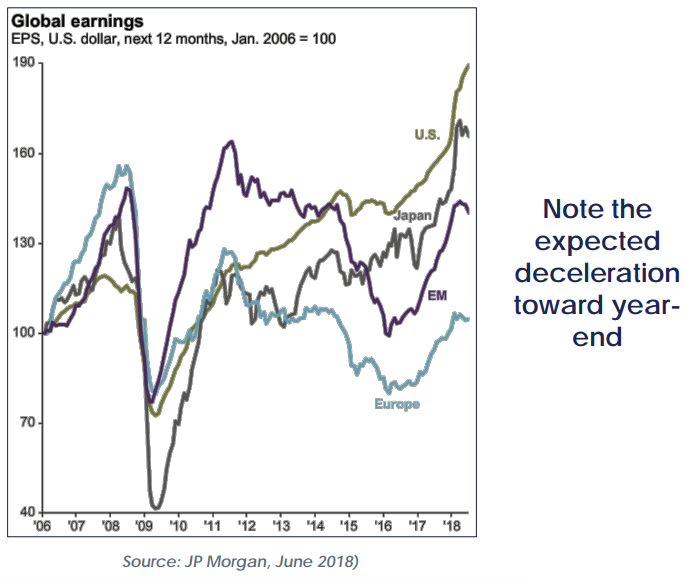

Earnings are solid, but expected to decelerate in Q3 or Q4

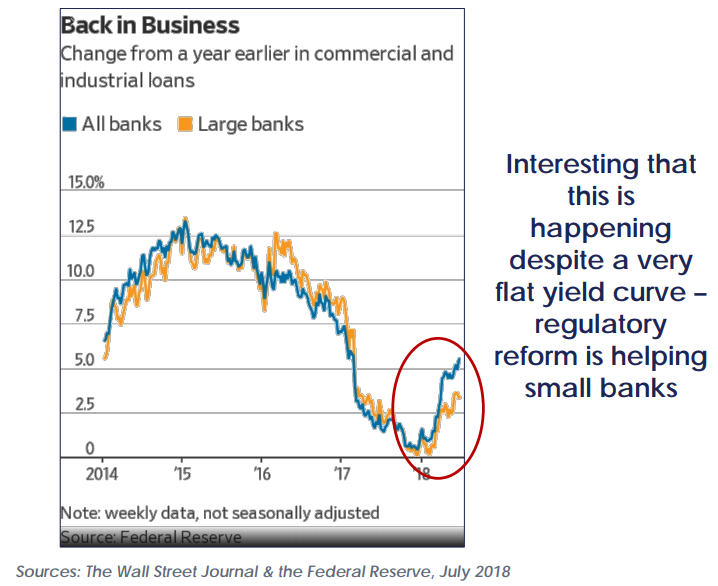

And banks are lending again

Non-US earnings positive, but below US

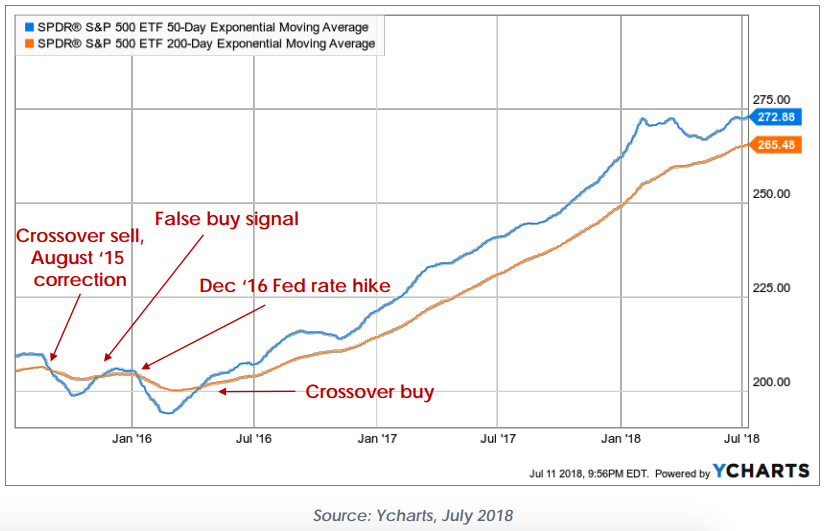

Momentum still in your favor

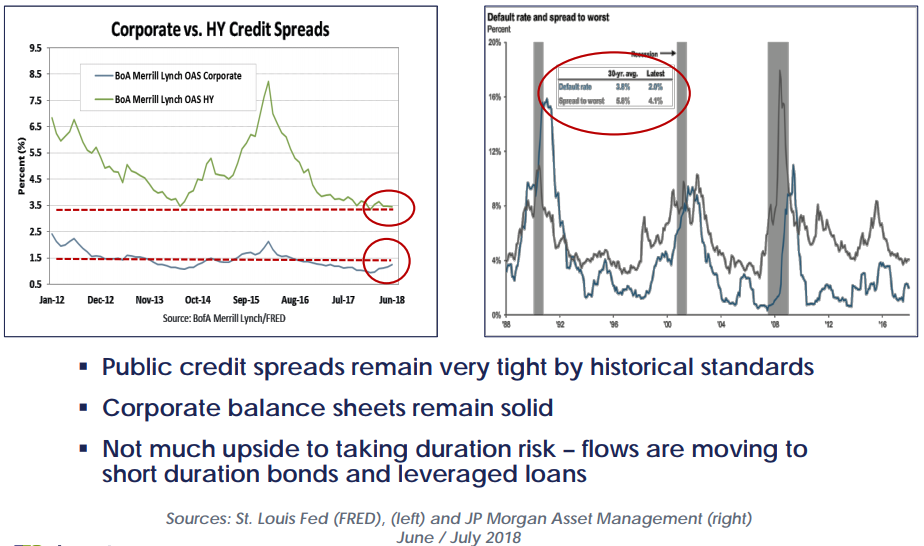

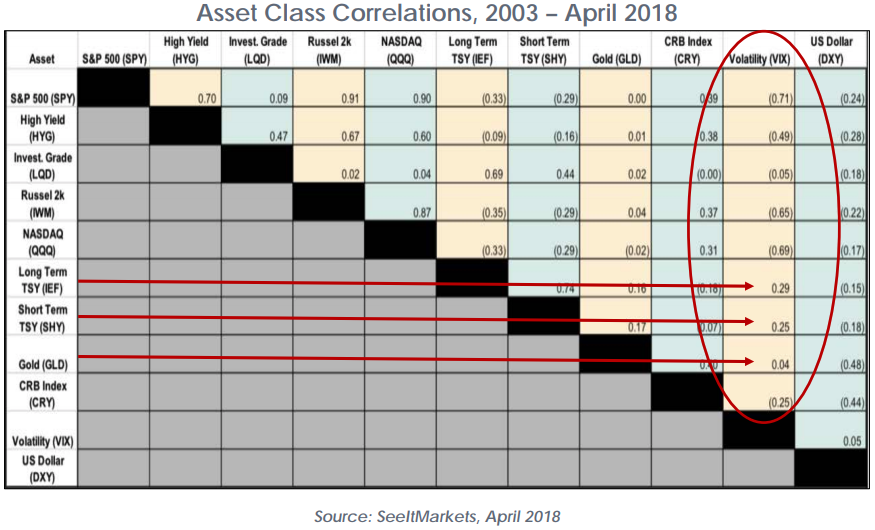

Spreads are tight, but so are defaults

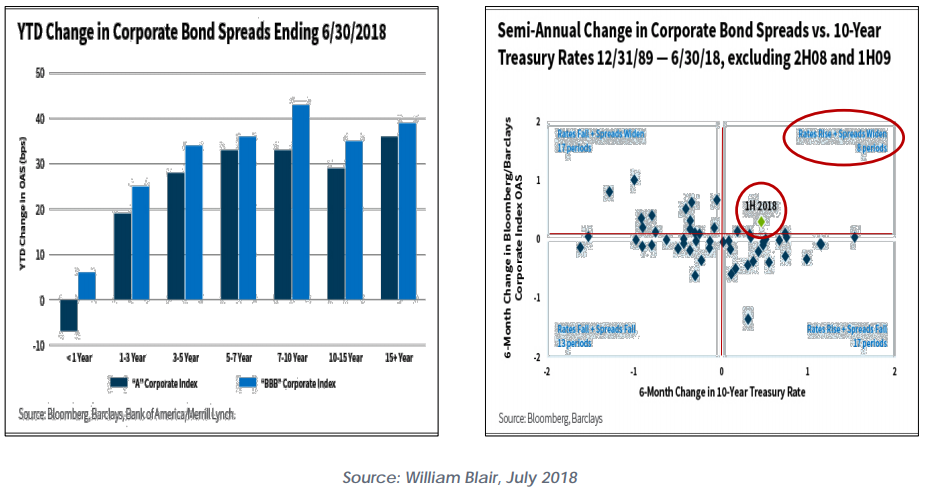

Spreads widening, rare risk regime

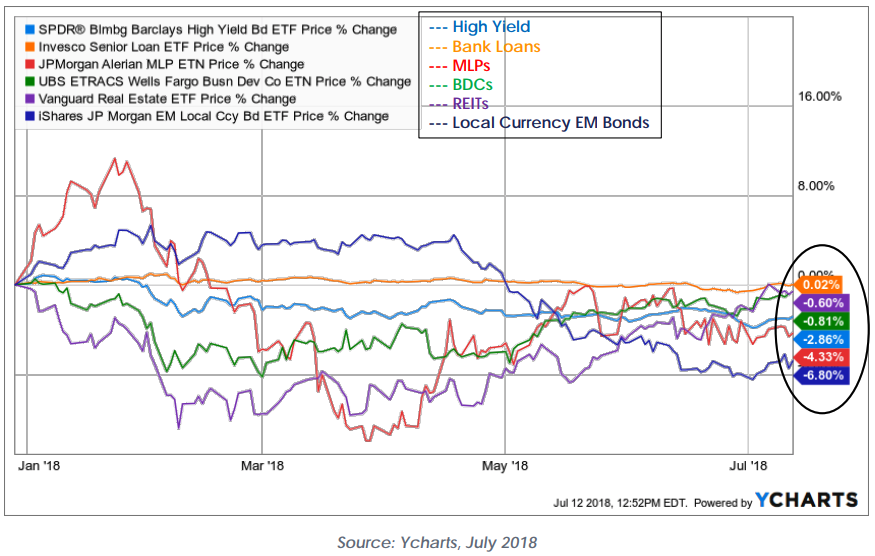

Remains a rough year for yield hunters

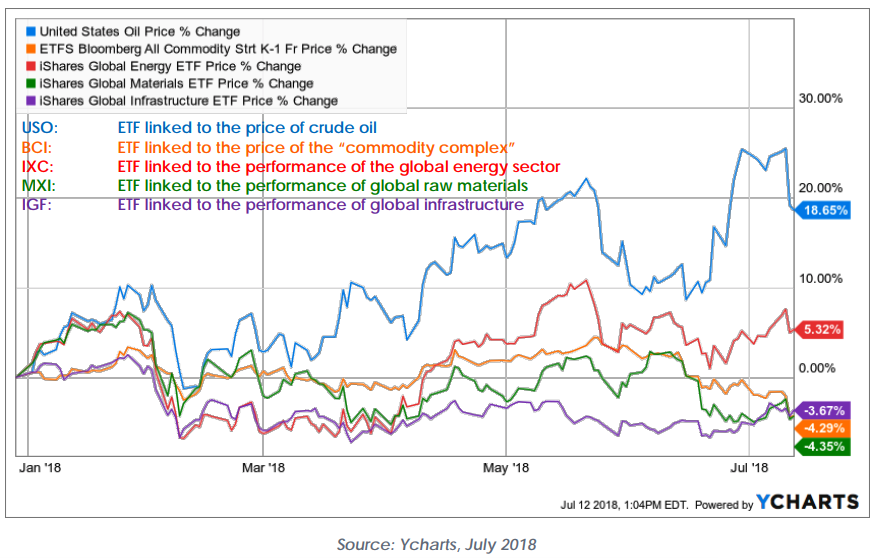

Ex-oil, mixed bag for “real assets”

But “valuations” look ok

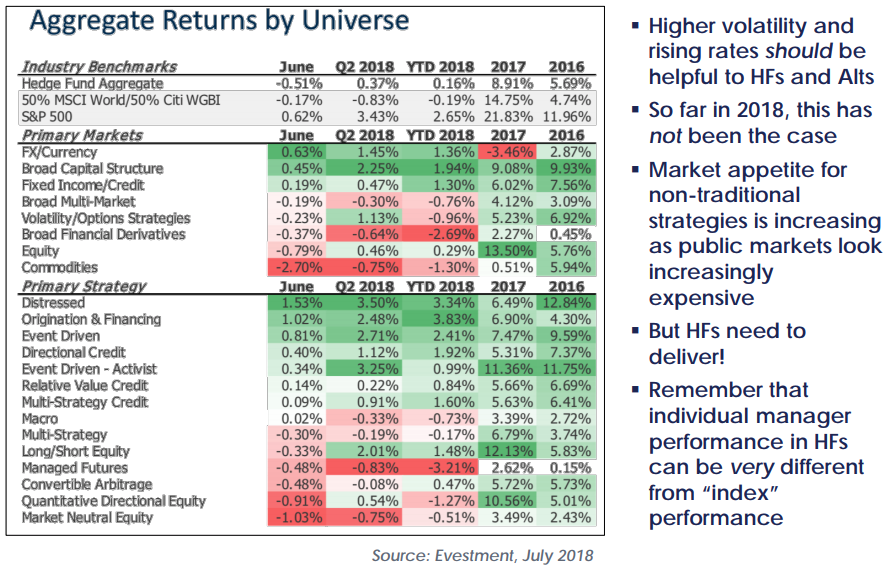

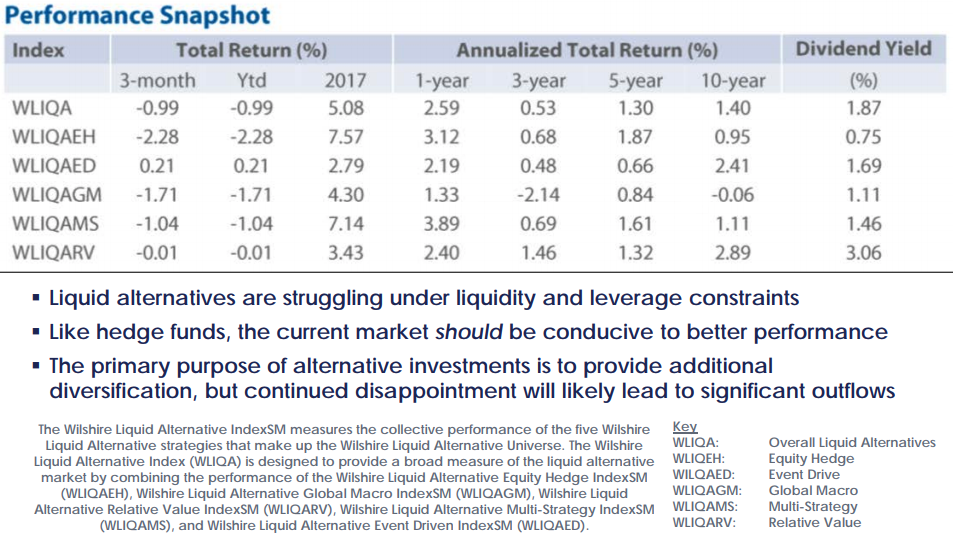

Modest year for most HF strategies

Liquids alts not delivering, so far

![]()

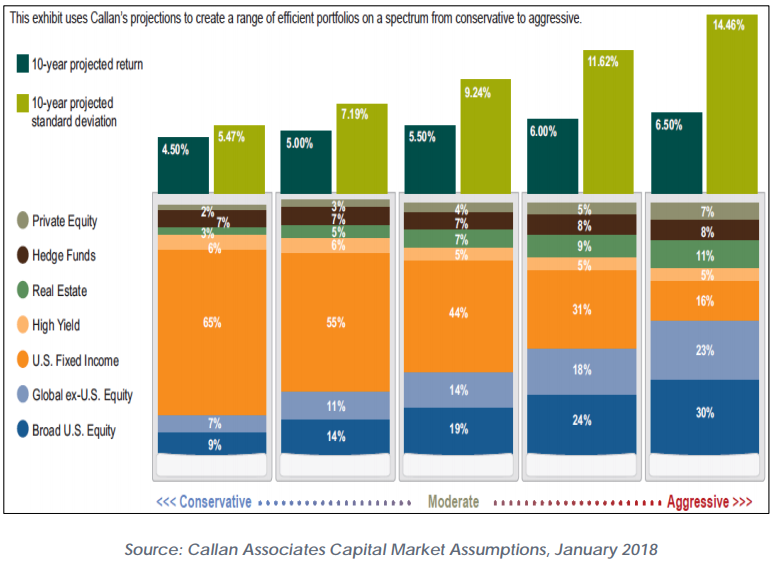

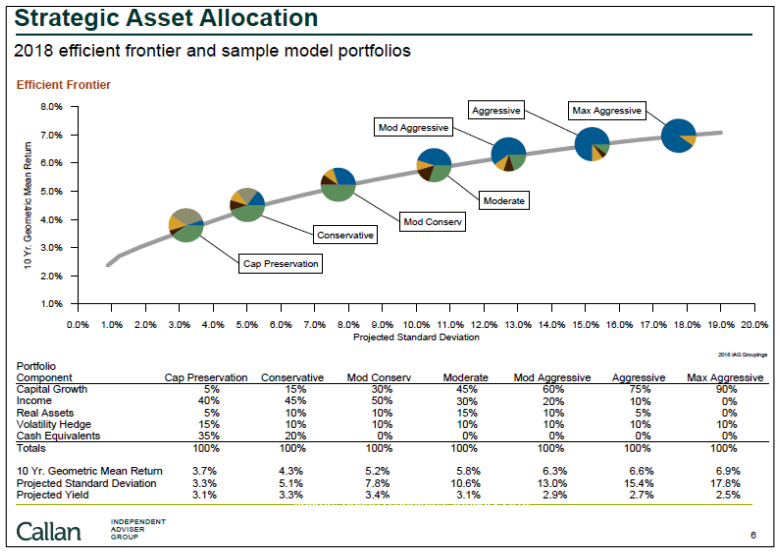

Building “All Weather” Portfolios

Reminder: no free lunch anymore

Are you being adequately rewarded?

![]()

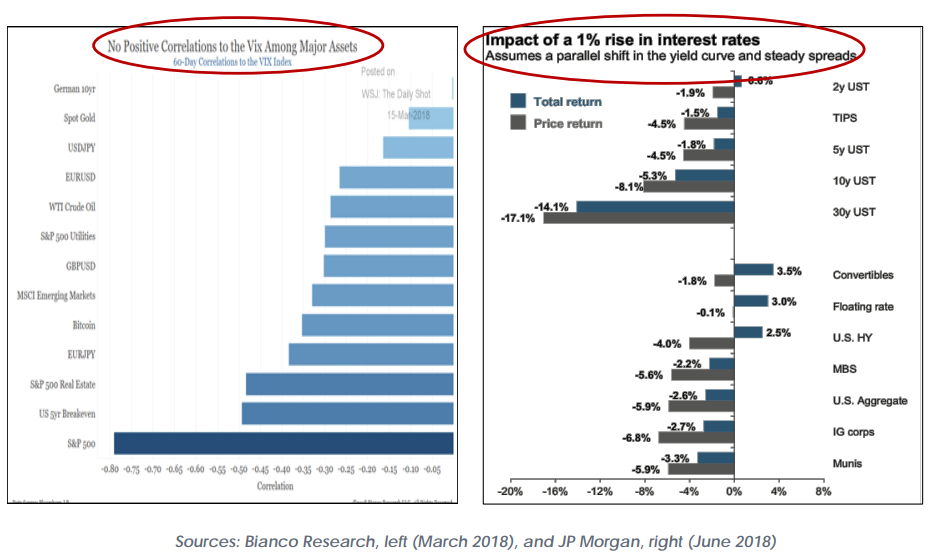

Who you gonna call?

Not very many anti -volatility tools

How we see things…

- The global economy continues to expand, though there is a “desynchronization” of growth. The US economy appears to be accelerating as the full effects of regulatory and tax reform work their way through the system. At the same time, the rest of the world appears to be decelerating – still expansionary, but slowing down;

- We believe going forward that an expanding US economy, rising inflation rates, continued tightening of Fed policy, and strong investment flows will further strengthen the dollar;

- Inflation is trending higher, but we maintain our belief that it (as of yet) does not represent a problem for continued economic expansion. Wages finally are starting to increase, though slowly, as there currently are more job openings in the US than qualified workers to fill them;

- Outside the US, inflation simply is not a problem, despite rising oil prices. We also maintain our belief that the Fed is inclined to let inflation “run hot” before stepping in;

- In the US, tax and regulatory reform currently are trumping (pun fully intended) monetary tightening. Adding stimulatory fat to an already raging economic fire remains an unknown with respect to the longer term impact on deficits and inflation.

- We continue to believe this is at least a contributing factor to ongoing market uncertainty and volatility;

- Solid US GDP growth, and solid earnings and revenue growth, make for a generally positive market environment, and we still think stocks will end the year higher than where they began. However, decelerating earnings growth and rising interest rates will most likely combine to push valuations down and volatility up;

- Market volatility will also be affected by what seems to be a continuing series of geopolitical events. The most current (and probably the most feared) is the ongoing trade tensions.

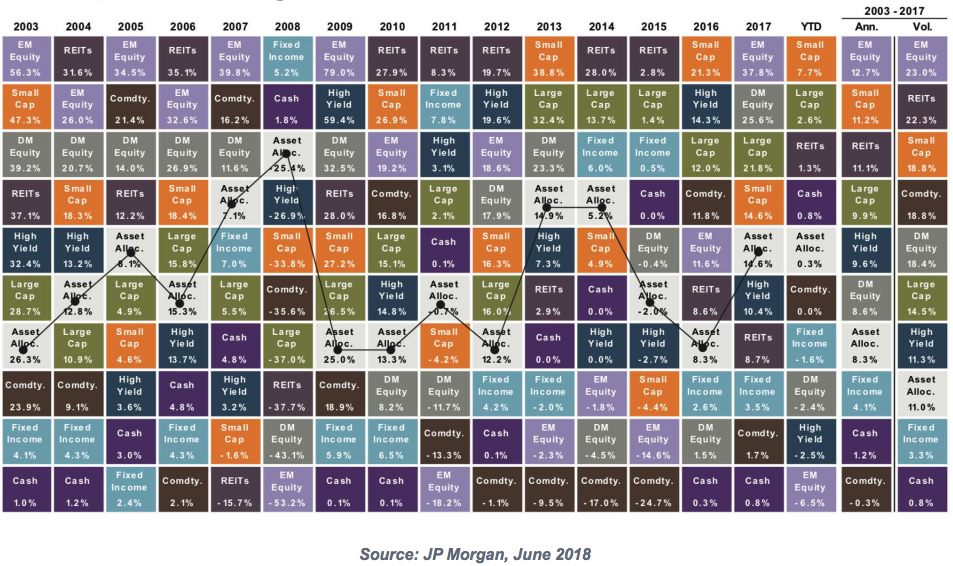

Boring but true: diversification and compounding work

Important disclaimers & disclosures

Dynasty Financial Partners is a U.S. registered trademark of Dynasty Financial Partners, LLC (“Dynasty”). Dynasty is a brand name and functions through Dynasty’s wholly owned subsidiary Dynasty Wealth Management, LLC, (“DWM”) a registered investment advisor with the Securities and Exchange Commission when providing investment services. A copy of DWM’s current written disclosure statement discussing our advisor services and fees is available for your review upon request. This message is intended for the exclusive use of members or prospective members considering joining the Dynasty Network of registered investment advisors for educational purposes. It is not intended for any other persons, clients or other entities. It should not be construed as an attempt to sell or solicit any products or services of Dynasty, Dynasty Wealth or any investment strategy, nor should it be construed as legal, accounting, tax or other professional advice. Information contained herein is based on sources believed to be reliable, but there are no representations or warranties as to the accuracy of such information.

DWM serves as a sub-advisor to Dynasty Strategist Portfolios (“the Portfolios”), however DWM does not directly manage client assets within the Portfolios. Any reference to the term “registered investment adviser” or “registered” does not imply that Dynasty or any person associated with Dynasty has achieved a certain level of skill or training.

Past Performance of model performance shown is no guarantee of future results. The model portfolio performance does not reflect actual trading or any advisory, management, or transaction fees, all of which could result in substantially lower results. This does not reflect the impact that material economic and market factors may have had on decision making. You cannot invest directly in an index. Please contact Dynasty for lifetime performance reporting of each Dynasty Strategist Portfolios.

Historical performance results for investment indices and/or product benchmarks have been provided for general comparison purposes only, and do not include the charges that might be incurred in an actual portfolio, such as transaction and/or custodial charges, investment management fees, or the impact of taxes, the incurrence of which would have the effect of decreasing historical performance results. It should not be assumed that your account holdings correspond directly to any comparative indices.

The views expressed in the referenced materials are subject to change based on market and other conditions. This document may contain certain statements that may be deemed forward‐looking statements. Please note that any such statements are not guarantees of any future performance and actual results or developments may differ materially from those projected. Any projections, market outlooks, or estimates are based upon certain assumptions and should not be construed as indicative of actual events that will occur. The information provided herein does not constitute investment advice and is not a solicitation to buy or sell securities.

Performance information provided by Dynasty or any third parties does not reflect the impact of taxes on non-qualified accounts. In providing this information Dynasty believes the information to be reliable, but has not in all cases independently verified such information. Strategy performance information is obtained through the use of Zephyr and Bloomberg data sources. Callan Associates is an independent company and unaffiliated with Dynasty. There is no form of legal partnership, agency, affiliated or similar relationship between Callan and Dynasty. The information contained herein is general in nature, is provided for informational purposes only and is not legal advice.

Different types of investments involve varying degrees of risk, and there can be no assurance that the future performance of any specific investment, investment strategy, investment model, or products, including the investments, investment strategies or investment themes referenced herein, will be profitable, equal any corresponding indicated historical performance level(s), be suitable for a particular portfolio or individual situation, or prove successful. Due to various factors, including changing market conditions and/or applicable laws, the content may no longer be reflective of current opinions or positions

This content may not be modified, distributed or otherwise provided in whole or in part to a prospective investor or someone considering investing in the portfolio models without the express authorization of the party delivering the presentation. Please note that nothing in this content should be construed as an offer to sell or the solicitation of an offer to purchase an interest in any security or separate account. Nothing is intended to be, and you should not consider anything to be direct investment, accounting, tax or legal advice to any one investor. Consult with an accountant or attorney regarding individual accounting, tax or legal advice. No advice may be rendered, unless a client service agreement is in place.

This material is proprietary and may not be reproduced, transferred, or distributed in any form without prior written permission from Dynasty Financial Partners, who reserve the right at any time and without notice to change, amend, or cease publication of the information contained herein. This material has been prepared solely for informative purposes. The information contained herein includes information that has been obtained from third-party sources and has not been independently verified. It is made available on an "as is" basis without warranty. Strategies and investment programs described in this presentation are provided for educational purposes only and are not necessarily indicative of securities offered for sale or private placement offerings available to any investor.

Asset allocation and diversification do not ensure or guarantee better performance and cannot eliminate the risk of investment losses. Target asset allocations may differ from illustrations due to market conditions and investment decisions. There can be no guarantee that target allocations will be achieved or maintained. No projection or representation can be made regarding future performance results. There is no guarantee that such performance could be achieved or that similar results could be attained in the future. All investments carry risk of loss.

iCapital Securities, LLC, acts as the placement agent for alternative investments offered through the Dynasty Select platform. iCapital Securities, a subsidiary of Institutional Capital Network, Inc., is registered as a broker-dealer with the U.S. Securities and Exchange Commission (“SEC”) and is a member of the Financial Industry Regulatory Authority (“FINRA”) and the Securities Investor Protection Corporation (“SIPC”). The registrations and memberships above in no way imply that the SEC, FINRA or SIPC have endorsed the entities, products or services discussed herein.

This message is intended for the exclusive use the Dynasty Network of registered investment advisors for educational purposes. It is not intended for any other persons, clients or other entities. It should not be construed as an attempt to sell or solicit any products or services of Dynasty, Dynasty Wealth or any investment strategy, nor should it be construed as investment, legal, or tax advice.

Dynasty Financial Partner is a U.S. registered trademark of Dynasty Financial Partners LLC (“Dynasty”). Dynasty is an integrated services provider to the independent channel of registered investment advisers. Dynasty is a brand name and functions through Dynasty's wholly owned subsidiary, Dynasty Wealth Management, LLC (“DWM”) a registered investment advisor with the Securities and Exchange Commission. References herein to DWM as a “registered investment adviser” or any reference to being “registered” does not imply a certain level of expertise. Dynasty conducts business through DWM when providing investment advisory services. A copy of Dynasty Wealth's current written disclosure statement discussing our advisory services and fees is available for your review upon request. Dynasty's wholly owned subsidiary Dynasty Securities LLC is a U.S. registered broker-dealer, member of FINRA and SIPC and may receive referral fees on brokerage transactions.

Past performance is not a guarantee or indicator of future performance.

Dynasty Financial Partners makes no warranties with regard to the information or results obtained by its use and disclaims any liability arising out of your use of, or reliance on, the information.

The information is subject to change and, although based upon information that is considered reliable, is not guaranteed as to accuracy or completeness. Please see the important disclosures at the end of this presentation.

Membership required

Membership is now required to use this feature. To learn more:

View Membership Benefits