The conventional wisdom is that risk-adjusted, overall portfolio returns are enhanced by combining exposure to a U.S. small-cap equity benchmark, like the Russell 2000 Index, with large-cap stocks. However, we find this belief is simply not supported by the data.

Based on our analysis, the small-cap "risk premium" first identified in the early 1980s still holds -- but only for "quality" small caps.

So, when considering small caps, we believe investors should focus on quality if they want to get the most from this distinctive asset class.

What premium?

Let's start with a look at the past decade and the 1-, 3-, 5- and 10-year annualized returns for the small-cap Russell 2000 vs. the large-cap Russell 1000. Only for the 10-year period have small caps outperformed large caps. Yet, even for this 10-year period of outperformance, the return was insufficient to account for higher risk -- small caps had a higher standard deviation (25.45% vs. 20.26%) and a lower Sharpe ratio (0.37 vs. 0.45).

So, over the past decade, risk-adjusted performance suggests that small-cap stocks haven't delivered vs. large caps. We believe this can be explained by the declining quality of stocks in the Russell 2000, which is why we also believe active management and a focus on quality are critical when investing in U.S. small caps.

Benchmark blues

Intuitively, the small-cap universe should offer the potential for higher returns, along with opportunities to capitalize on inefficiencies. Smaller companies often have higher growth rates, insider ownership, and can be acquisition targets.

Historically, simply tracking an index of small-caps stocks has tended to deliver the small-cap premium. But that may be changing. It may not be enough to simply buy the next-largest 2,000 publicly traded companies after the Russell 1000, which is how the Russell 2000 is constructed.

Why? First, the number of stocks in the U.S. market has declined significantly. The number of public companies has declined by over 50% from a peak of 6,364 in December of 1997, to only 3,114 today, according to Jefferies. The pond is getting smaller and is biased to lower quality companies. In fact, the smallest company in the benchmark today (at the annual Russell reconstitution in June) is only 16% larger than it was in 1997 vs. a 160% increase in the average cap and a more than 400% total return for the benchmark, according to Bloomberg data. There haven't been enough IPOs to backfill the natural process of mergers, acquisitions and bankruptcies. IPOs totaled only 196 in 2017 vs. 880 in 1996, according to Jefferies.

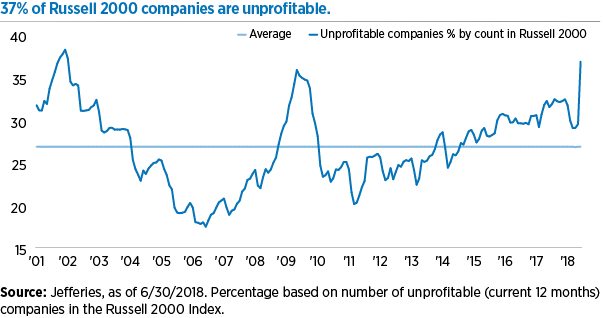

As we discussed in a previous blog post, fewer stocks in the market means that the average company size in the Russell 2000 has gotten smaller (as measured by market cap), particularly in the bottom half of the index. This has resulted in the index holding more unprofitable companies.

In other words, the quality of the companies in the Russell 2000 has declined. In fact, 37% of companies in the Russell 2000 are unprofitable, more than at the trough of the 2008/2009 recession.

Furthermore, since 2000, in only four months has the small-cap benchmark held a greater number of unprofitable companies, according to Jefferies. The return on assets (ROA) of the Russell 2000 has declined by 38%, while leverage has increased by 21%. This compares with a 2% increase in ROA for the large-cap Russell 1000, and a less concerning 10% increase in leverage, according to FactSet data.

Quality control

We believe the declining quality of companies in the Russell 2000 creates opportunity for active strategies in small caps. It seems reasonable to assume a significantly larger percentage of the benchmark will be unprofitable if the economic cycle were to turn negative. Typically, higher leverage and a lack of earnings have been a recipe for underperformance and one that a quality-focused active manager seeks to avoid.

Also, there is less Wall Street analyst coverage of small caps vs. large caps as well as a wider dispersion of outcomes vs. expectations. For example, the difference in actual earnings per share in a given year for the average small-cap company vs. what the consensus estimate was at the beginning of that year is in excess of 40%! We think this is fertile ground for active management and bottom-up research.

Bottom line: Blindly buying small caps without regard to company profitability and quality could be a recipe for disappointment. With so many unprofitable companies included in the Russell 2000, investors need to sort through the massive universe and actively invest in the quality companies that can one day grow and achieve large-cap status.

The Russell 2000 Index is an unmanaged index of 2,000 U.S. small-cap stocks.

The Russell 1000 Index is an unmanaged index of 1,000 U.S. large-cap stocks.

The S&P 500 Index is an unmanaged index of large-cap stocks commonly used as a measure of U.S. stock market performance

Sharpe ratio: Return above the risk-free rate, per unit of volatility/risk.

The value of equity securities is sensitive to stock market volatility. Smaller companies are generally subject to greater price fluctuations, limited liquidity, higher transaction costs and higher investment risk than larger, more established companies.

© Eaton Vance

© Eaton Vance

Read more commentaries by Eaton Vance