Today’s popular stocks have literally overwhelmed the stock market in the last four years and six months. To understand today’s financial euphoria, we will analyze three terrific movies made by the actor, Jim Carrey. In Liar Liar, The Truman Show and in Bruce Almighty, we learn morals which we believe should guide us in the long-duration investment process.

Liar Liar is the story of a fast-track lawyer who was fast and loose with the truth. His son makes a wish, while blowing out his birthday candles, that his dad can't lie for 24 hours and his wish comes true. The humor comes from the pain that Carrey’s character, attorney Fletcher Reede, feels as he goes through the day. He had to tell the truth to virtually everyone he encountered, including his female boss, his ex-wife, and his executive assistant. The moral of the story is it is always ultimately better to tell the truth.

Why is this important? It seems today’s popular stocks are led by people who have a hard time telling the truth or have an easy time being deceptive. Here is how investor, Jim Chanos, recently explained how the truth is being stretched in the US stock market:

Chanos: well, i mean, one of the things we talked about today at the conference is the culture in Silicon Valley. And this ties a little bit in with tesla. And why some of these things appear to be growing out in Silicon Valley, the willingness to sort of say anything by ceos. There was - there was an expose on vice media talking a little about the same thing. And the lack of due diligence on behalf of both the boards and the investors in believing a lot of these things. And is it increasing as the market goes on?

One of the central tenets of the course is that the fraud cycle follows the financial and business cycle with a lag. And that is as bull markets go on, people's sense of disbelief is reduced and they begin to believe things that are too good to be true. It's human nature. And bad people take advantage of that. And i think we're going to see an increase in these kinds of revelations as time goes on. Particularly out in Silicon Valley. You can't lie to investors. And this is the problem.1

A few examples would be helpful. We recently went with a group of analysts to an investor day at Amazon just eight blocks from our office. About 30 questions were asked and the answer to half of them was “we don’t disclose that.” The reason a public company is called a public company is because they are required to share their financial information with public shareholders.

The following is a small list of questions regarding financial information which Amazon would not disclose:

- What are your margins on selling books?

- What are your margins in grocery?

- What is Amazon’s e-commerce paying Amazon Web Services (AWS)?

- Who are all Amazon’s web-hosting clients?

- What part of AWS profits comes from the porn industry?

- What was the outcome of the Amazon Fresh and Amazon Go beta tests?2

Here is a list for Facebook:

- Are you a monopoly?

- Did you know that political entities were paying you a great deal of money to deceive people?

- Are you manipulating your un-paid customers/actors?

Below is the Google list:

- Do you use your algorithms to benefit your own marketplace activities in front of your best customers?

- Is the US government going to be willing to let a for-profit entity know more about US citizens than they do?

In The Truman Show, Carrey’s character is unknowingly being followed in a made-for-TV world. It effectively introduced the idea of unscripted TV, which our own holding, Discovery Inc. (DISCA), has dominated. Truman didn’t know that his life was a massive profit center for the broadcasting company which was manipulating him and his life.

Facebook (FB) is effectively a ‘Truman Show’ for its huge volunteer army of participants. They are unpaid actors and actresses, who are selling a massive amount of advertising for Facebook. They have been willing to trade their privacy to gain the social networking connections they enjoy. When Truman found out that his life was one big manipulation, he rejected it and rejected being taken advantage of.

We believe that Facebook and Alphabet (GOOG, GOOGL) will become regulated businesses like AT&T, the broadcast networks and the railroads. Our assumption is that a Teddy Roosevelt like character will emerge politically out of one of the two major parties. This explains why they haven’t received the nosebleed price-to-earnings ratios of the Amazon’s and Netflix’s of the world.

Bruce Almighty is the story of a guy who complains about God too often and is given almighty powers to teach him how difficult it is to run the world. Bruce was put into positions only God should be put in, and in the process, Bruce humbled himself and gladly gave up on complaining and criticizing God.

These tech companies have amassed power like we haven’t seen since the Gilded Age of the late 1890’s. The idolatry associated with their success, and the small g god status of their CEOs, should send chills down the spine of investors. Bruce didn’t get his humility until he had lost his job, his girlfriend and his hometown of Buffalo.

Standard Oil was the only major producer of oil and refiner of gasoline in the year 1900. There were 4,000 cars sold in the US in 1900, and by 1925 we sold 3.5 million cars. What would have happened if Standard Oil hadn’t been broken up by the trust-busting President, Teddy Roosevelt? Standard Oil became nine major oil companies and the competition created by busting it up kept oil and gas prices affordable for what became the most powerful economy in the world.

Stock market bulls believe they are correct in their argument that technology is the most important driver of the economy going forward. Therefore, these major tech companies which are monopolizing social networking, search engines, e-commerce and cloud services — and are violating the privacy of 330 million Americans — are easily as important to the democratic capitalist system today as Standard Oil was in 1900!

At some point, US investors will have to deal with the fact that the S&P 500 Index, the Exchange-Traded-Fund (ETF) complex, growth stock mutual funds and many individual investors are all twisted up in the sins described by Jim Carrey’s series of movies. Here is a reminder of the common denominators of financial euphoria episodes from John Kenneth Galbraith’s, A Short History of Financial Euphoria:

- Extreme brevity of financial memory.

- The specious association of money and intelligence.

- Something new in the world-an element of pride in discovering what is seemingly new and greatly rewarding.

- What happens after the inevitable crash. This, invariably, will be a time of anger and recrimination and also profound unsubtle introspection. The anger will fix upon the individuals who were previously most admired for their financial imagination and acuity.

Galbraith argues that these financial euphoria episodes themselves never get the blame for the misery, because there is a classical belief in the inherent virtue in the invisible hand of market pricing. Hence, the emergence of efficient market theories which have helped popularize passive index investing. How incredibly painful it very well could be when this euphoria episode gets connected with the virtuous cost and theory behind the explosion in indexing and ETFs.

The investor, Howard Marks, has recently warned investors in a very subtle way that the playpen which has been created for tech stock ownership is at the center of the mania. In a world where the owners neither know nor care which companies are owned or the position sizes, Galbraith’s theory behind the inevitable crash is laid. Under Galbraith’s theory, when the most popular stocks crash and burn, Jack Bogle (Vanguard) and Larry Fink (Blackrock), will be glad that Jeff Bezos, Reid Hastings and Mark Zuckerberg will be vilified. Bogle and Fink will get a pass, even though they have allowed the capital to get trapped much more than it would have in prior eras.

Where does this take us? First, we are going to stick with the companies which meet our eight criteria for common stock selection and are available at prices which we’d be proud to own in any era. This has led us to healthcare, media, retail, homebuilding and financial services. Second, we will avoid participation in high-risk and high-reward situations tied to the euphoria.

Third, we remain diligent in analyzing buying opportunities created by excessive enthusiasm for tech darlings. Amazon told everyone one year ago that they bought Whole Foods for positive reasons, while we firmly believe that it was failed Seattle-area beta tests on Amazon Fresh and Amazon Go which forced their hand. We like Target (TGT) and Kroger (KR). In our opinion, spooking the pharmacy stocks was Amazon’s latest prank and we added to Walgreens (WBA) on the steep short-term decline.

We ended the quarter with our largest position in Discovery, Inc. John Malone bought over $32 million of the shares in his own account in June and we know from his public interviews how undervalued he believes the company to be. It is our view that the highly profitable, unscripted TV produced by Discovery, Inc. is not threatened by new distribution methods.

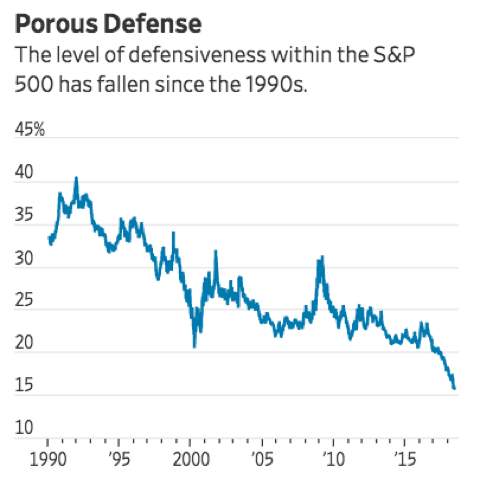

Lastly, we believe today’s healthcare introductions should be the thing that investors are the most excited about. Amgen (AMGN), Merck (MRK), Pfizer (PFE) and Johnson & Johnson (JNJ) are on the cutting edge of many thrilling new drug introductions and their copious dividends help us wait for attention to turn that direction. The stocks of healthcare, staples and utilities are the least represented in the S&P 500 Index they have been since 1990 as the chart below shows:3

In review, Jim Carrey’s movies taught us a great deal about truth, deception and idolatry. As long duration investors, we must avoid getting caught in the regular bouts of financial euphoria to which the US stock market is susceptible. Despite this, many meritorious companies are available at very reasonable prices because of the attention being drawn by today’s tech darlings. Thank you, as always, for your confidence and patience.

1https://www.broadwayworld.com/bwwtv/article/CNBC-Transcript-Kynikos-Associates-Founder-and-President-Jim-Chanos-on-CNBCs-CLOSING-BELL-Today-20180613

2https://investorplace.com/2018/06/amazon-stock-amazon-fresh/

3https://www.wsj.com/articles/investors-double-down-on-faang-in-rocky-quarter-for-stocks-1530264600?mod=searchresults&page=1&pos=2

The price-earnings ratio (P/E Ratio) measures a company's current share price relative to its per-share earnings. Margin refers to sales minus cost of goods sold. Beta tests are a trial of machinery, software, or other products, in the final stages of its development, carried out by a party unconnected with its development.

The information contained herein represents the opinion of Smead Capital Management and is not intended to be a forecast of future events, a guarantee of future results, nor investment advice.

Smead Capital Management, Inc.(“SCM”) is an SEC registered investment adviser with its principal place of business in the State of Washington. SCM and its representatives are in compliance with the current registration and notice filing requirements imposed upon registered investment advisers by those states in which SCM maintains clients. SCM may only transact business in those states in which it is notice filed or qualifies for an exemption or exclusion from notice filing requirements. Registered investment adviser does not imply a certain level of skill or training.

This newsletter contains general information that is not suitable for everyone. Any information contained in this newsletter represents SCM’s opinions, and should not be construed as personalized or individualized investment advice. Past performance is no guarantee of future results. There is no guarantee that the views and opinions expressed in this newsletter will come to pass. Investing in the stock market involves gains and losses and may not be suitable for all investors. Information presented herein is subject to change without notice and should not be considered as a solicitation to buy or sell any security. SCM cannot assess, verify or guarantee the suitability of any particular investment to any particular situation and the reader of this newsletter bears complete responsibility for its own investment research and should seek the advice of a qualified investment professional that provides individualized advice prior to making any investment decisions. All opinions expressed and information and data provided therein are subject to change without notice. SCM, its officers, directors, employees and/or affiliates, may have positions in, and may, from time-to-time make purchases or sales of the securities discussed or mentioned in the publications.

© 2018 Smead Capital Management, Inc. All rights reserved.

This Missive and others are available at www.smeadcap.com

Follow us on Twitter @SmeadCap