Near the beginning of the year, Goldman Sachs analyst Jeffrey Currie made the case that the macro backdrop right now favored commodities in 2018. With inflation pushing prices up and world economies borrowing record amounts of capital, it was the best time “in decades,” he said, for investors to have exposure to base metals, energy and other materials.

“Commodities had a miserable year” in 2017, Currie told CNBC. “History says commodities will outperform equities this year.”

Currie’s forecast has been mostly accurate so far. Except for a rocky June, commodities have been one of the best performing asset classes in the first half of the year. From January to the end of May, the group, as measured by the Bloomberg Commodities Index, rallied close to 3 percent—170 basis points ahead of the S&P 500 Index. Advances were largely driven by crude oil, which currently seeks to close above $80 a barrel for the first time since November 2014.

Of the 14 major commodities we track at U.S. Global Investors, oil was the standout performer, gaining roughly 23 percent, followed by nickel (up 16.76 percent) and wheat (16.51 percent). You can view our always-popular, interactive Periodic Table of Commodity Returns by clicking here.

click to enlarge

There are a number of factors supporting oil right now, not least of which is President Donald Trump’s decision to withdraw the U.S. from the Iran nuclear deal. The move has the potential to significantly curb exports out of the Middle Eastern country, responsible for about 4 percent of the world’s supply. Markets were further disrupted two weeks ago when the U.S. government warned importers to stop buying Iranian oil or face sanctions.

In addition, supply is being squeezed by worsening economic conditions in Venezuela, which sits atop the world’s largest known oilfield, and conflict in Libya, home to Africa’s largest oil reserves. On Wednesday of this week, though, Libya indicated it would resume exports from its eastern ports, which sent Brent crude down more than 2 percent.

Global Oil Consumption Blasted to New Heights

Many investors might be inclined to believe the oil rally is over, but I think we could continue to see movement to the upside on further supply restrictions and rising demand. In its June Statistical Review of World Energy, British oil and gas giant BP reports that consumption grew for the eighth straight year in 2017, climbing to 98.2 million barrels per day (bpd) for the first time ever. We would need to see growth of only 2 percent by the end of this year for demand to reach and surpass 100 million bpd—a phenomenally large sum.

This could be achieved if Chinese demand growth remains as robust as it’s been for the past decade. Consumption stood at 12.8 million bpd in 2017, a new record for the country. This figure is up 64 percent from only 7.8 million bpd in 2007.

Although China is now the world’s number one auto market in terms of sheer size, vehicle and vehicle finance penetration are still relatively low compared to the U.S., Japan, Germany and other major economies. There were about 115 vehicles per 1,000 people in 2015, according to J.D. Power, compared to the U.S. with 800 vehicles per 1,000 people. That means there’s plenty of upside potential for energy as more Chinese households are able to afford automobiles.

Speaking of autos, the excitement over electric vehicles (EVs) is helping to drive up the cost of nickel, vital in the production of lithium-ion batteries. In the first six months of the year, the price of nickel rose close to 17 percent, to $14,823 per metric ton. As impressive as that is, it’s still three and a half times below its all-time high of $54,050, set in May 2007.

Commodities Now a Buy: Goldman Sachs

As I said earlier, commodities had a rough June, falling some 3.64 percent as trade tensions between the U.S. and China escalated. This was the group’s biggest monthly slump in nearly two years, led by copper and soybeans.

click to enlarge

Goldman analysts say this has created a well-timed buying opportunity, as the selloff was overdone. According to the bank, the U.S.-China trade war impact on commodities “will be very small, with the exception of soybeans where complete rerouting of supplies is not possible.”

Goldman now forecasts a 10 percent return on commodities over the next 12 months as the U.S. dollar corrects and trade fears subside.

If you recall, I made a similar bullish call on commodities back in April after showing that, relative to equities, commodities are as cheap now as they’ve possibly ever been. They’re even cheaper than they were in 2000, before the start of the last commodities super cycle. Had you invested in a fund tracking a commodities index in 2000, you would have seen your money grow at a compound annual growth rate (CAGR) of around 10 percent for the next 10 years, according to Bloomberg data.

click to enlarge

Copper Demand Should Accelerate With Electric Vehicle Sales

Among the most attractive opportunities I see is copper, which rose to an 11-month high of $3.29 per pound in early June before sinking 15 percent. Like nickel, copper has benefited from the forecast that EV adoption will accelerate. According to Bloomberg New Energy Finance, EV sales are expected to grow from a record 1.1 million units worldwide in 2017, to 11 million in 2025, then to 30 million in 2030.

This is good news for copper. As I’ve pointed out before, EVs require three to four times as much copper as traditional gas-powered vehicles.

click to enlarge

“You’re going to need a telescope to see copper prices in 2021,” Robert Friedland, billionaire founder and executive chairman of Ivanhoe Mines, told us back in January when he visited our office.

Robert’s comment might be hyperbolic, but the thing to keep in mind is that demand for the red metal is about to turn red hot.

Explore investment opportunities in commodities!

Index Summary

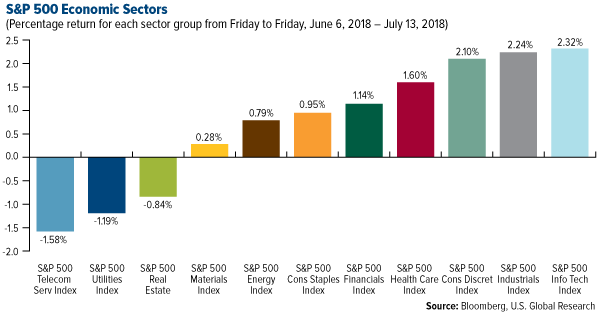

- The major market indices finished mixed this week. The Dow Jones Industrial Average gained 2.30 percent. The S&P 500 Stock Index rose 1.50 percent, while the Nasdaq Composite climbed 1.79 percent. The Russell 2000 small capitalization index lost 0.41 percent this week.

- The Hang Seng Composite gained 1.56 percent this week; while Taiwan was up 2.41 percent and the KOSPI rose 1.67 percent.

- The 10-year Treasury bond yield remained flat at 2.82 percent.

The Economy and Bond Market

Strengths

- The Labor Department said on Thursday its consumer price index (CPI) edged up 0.1 percent as gasoline price increases moderated and apparel prices fell. In the 12 months through June, the CPI increased 2.9 percent, the biggest gain since February 2012. The underlying trend continues to point to a steady buildup of inflation pressures that could keep the Federal Reserve on a path of gradual interest rate increases.

- U.S. producer prices increased slightly more than expected in June amid gains in the cost of services and motor vehicles, leading to the biggest annual increase in six-and-a-half years. The Labor Department said on Wednesday its producer price index (PPI) for final demand climbed 0.3 percent last month, also lifted by increases in gasoline prices. The PPI rose 0.5 percent in May. In the 12 months through June, the PPI advanced 3.4 percent, the largest gain since November 2011. Producer price gains echo the stronger economic environment.

- The number of U.S. workers filing for unemployment benefits fell more than expected last week, hitting a two-month low, in a sign that labor market conditions remained robust in early July. Initial claims for unemployment benefits dropped 18,000 to a seasonally-adjusted 214,000 for the week ended July 7, the lowest level since early May, the Labor Department said on Thursday.

Weaknesses

- Consumer sentiment dropped below expectations at the beginning of July to a six-month low on rising fears regarding the Trump administration's trade tariffs. Consumer sentiment fell to 97.1, according to the University of Michigan's monthly survey of consumers. Economists expected a reading of 98.2, according to Reuters.

- While business optimism remains near record highs, the latest NFIB Small Business Optimism Survey showed that 55 percent reported few or no qualified applicants for the positions they were trying to fill. Twenty-one percent of employers surveyed cited the difficulty of finding qualified workers as their top business problem.

- If the end of easy monetary policy, a trade war and myriad geopolitical dangers weren’t enough, a U.S. yield curve poised to invert is adding to the risks for investors.

Opportunities

- Aside from a dip in April, retail sales have remained robust during the first five months of 2018. Next week’s retail sales advance is likely to uphold the growth trend.

- New housing starts have trended upward in the last two months. A strong report next week could cement the momentum.

- After a choppy first quarter, U.S. manufacturing has picked up pace since April. Next week’s U.S. Empire Manufacturing Survey will be scrutinized for gauging activity for the second quarter.

Threats

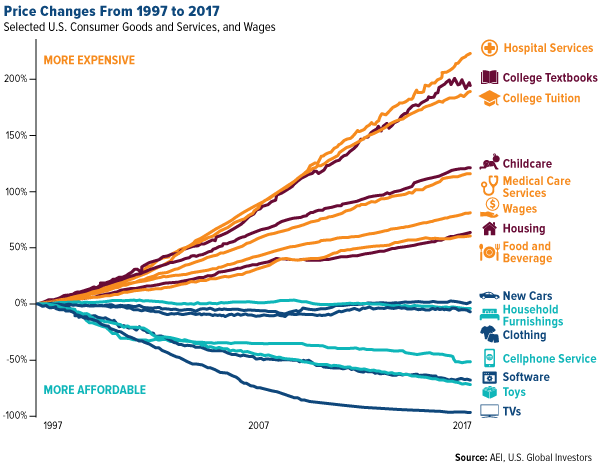

- The prices of goods subject to foreign competition, such as toys and television sets, have tumbled over the past two decades as trade barriers have come down around the world. Prices of so-called non-tradeables, such as hospital stays and college tuition, have surged. Just as globalization has been a headwind holding back inflation, its unraveling could end up being a tailwind in the years ahead, pushing costs higher as countries and companies retreat from the international marketplace. That would be on top of the one-time effect that Trump’s tariffs will have on prices of selected imports, putting pressure on the Fed to raise interest rates at a faster pace than the gradual path it has currently mapped out.

click to enlarge

- The Leading Index has been decelerating since the start of the year. Unless we see a reversal in next week’s release, we could soon fall into negative growth. As a precursor to future economic growth, this would flash a warning sign about future prospects.

- Industrial production has been falling since April. With escalating tariff tensions, next week’s release is likely to continue the soft patch in production.

Gold Market

This week spot gold closed at $1,241.45 down $13.75 per ounce, or 1.10 percent. Gold stocks, as measured by the NYSE Arca Gold Miners Index, ended the week lower by 3.18 percent. Junior-tiered stocks outperformed seniors for the week, as the S&P/TSX Venture Index came in off just 2.01 percent. The U.S. Trade-Weighted Dollar reversed course this week with additional tariff treats and rose 0.79 percent.

| Date |

Event |

Survey |

Actual |

Prior |

| Jul-10 |

Germany ZEW Survey Current Situation |

78.1 |

72.4 |

80.6 |

| Jul-10 |

Germany ZEW Survey Expectations |

-18.9 |

-24.7 |

-16.1 |

| Jul-11 |

PPI Final Demand YoY |

3.1% |

3.4% |

3.1% |

| Jul-12 |

Germany CPI YoY |

2.1% |

2.1% |

2.1% |

| Jul-12 |

Initial Jobless Claims |

226k |

214k |

232k |

| Jul-12 |

CPI YoY |

2.9% |

2.9% |

2.8% |

| Jul-15 |

China Retail Sales YoY |

8.8% |

-- |

8.5% |

| Jul-18 |

Eurozone CPI Core YoY |

1.0% |

-- |

1.0% |

| Jul-18 |

Housing Starts |

1322k |

-- |

1350k |

| Jul-19 |

Initial Jobless Claims |

220k |

-- |

214k |

Strengths

- The best performing metal this week was gold, down 1.10 percent. Holdings in the SPDR Gold Shares ETF, which accounts for more than one-third of total bullion-backed ETFs, have fallen to the smallest since August. However, gold assets in the London-listed iShares Physical Gold ETC are at a new record. Investors in the U.K. are seeking a haven for their investments as Prime Minister Theresa May struggles to keep the government together, writes Bloomberg. Investors added $17.5 million in assets to the State Street SPDR Gold MiniShares ETF, an increase of 33 percent, for the fourth straight day of inflows. This is a new ETF with lower fees than the SPDR Gold Shares ETF mentioned earlier.

- U.S. wholesale prices rose by the most since November 2011 in the 12 months ended in June, as the costs of services accelerated, as shown in a Labor Department report this week. Bloomberg’s Shobhana Chandra writes that this is an indicator that inflation pressures in the production pipeline are firming due to increased demand and tariffs on steel and other goods. Inflation has historically been positive for the price of gold.

- Japan’s largest gold retailer said that gold bar sales in the first half of this year climbed 32 percent compared to the prior year due to falling prices, yen appreciation and growing demand from local investors. Oil saw its biggest weekly loss in more than five months due to escalating trade tensions, which is positive for precious metal miners in easing energy costs at mines.

Weaknesses

- The worst performing metal this week was platinum, down 1.80 percent as hedge funds boosted their bearish platinum outlook. Investors withdrew money for the ninth straight week from commodity-focused ETFs, reports Bloomberg. Outflows from ETFs that invest in precious metals narrowed while funds that can buy all types of commodities had losses, the article continues.

- Sentiment for gold remained bearish this week, with traders saying this comes on the back of a subdued global trend, reports Bloomberg. The dollar extended gains from the previous session with U.S. inflation data along with trade war concerns boosting demand for the greenback. Other U.S. data came out this week, showing that some 3.56 million workers left positions in the month of May. According to Labor Department data, that is the most Americans quitting since 2000 and up from the prior month’s 3.35 million workers.

- Greg Barnes, an analyst with TD Securities, downgraded the recommendation on Kinross Gold Corp. to buy from action list buy, reports Bloomberg. Kinross recently had analyst tour their Fort Knox operations in Alaska where the mine’s life could be extended another nine years with the addition of the Gilmore property.

Opportunities

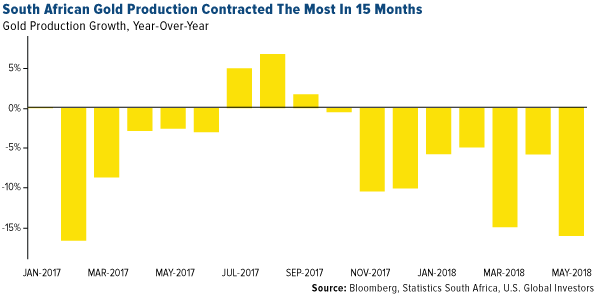

- According to Bloomberg Intelligence Commodity Strategist Mike McGlone, the history of compressed gold prices could be a guide to show that the dollar should be peaking, with a potential for higher gold prices. McGlone writes that it has been almost two decades since gold sustained a narrower 24-month range and that the most recent similarly compressed period in 2001 and 2002 coincided with a peak in the trade-weighted broad dollar index and a bottom in gold. The yellow metal could also rise due to slumps in production. South Africa was once the world’s biggest producer of gold; however, production has been in a steady decline the last few years and fell 16.2 percent from a year earlier in May, for eight straight months of decreases. Another headwind for gold production in South Africa is that mining unions began wage talks this week where laborers have demanded a 37 percent increase in pay, as producers are constantly struggling to reduce costs in the world’s deepest mines.

click to enlarge

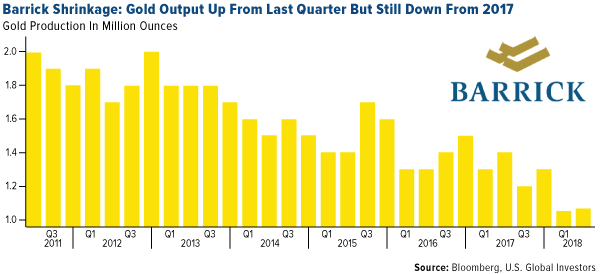

- Barrick Gold Corp., the world’s largest producer of gold, reported a decline in second-quarter production as planned maintenance weighed on output, as expected. The gold miner produced only 1.05 million ounces in the first quarter of this year, which is the lowest amount for Barrick in 16 years. This emphasizes the notion that the world has hit “peak gold” supply where most of gold has already been discovered and it’s become much more difficult to find new deposits. Tighter gold supply can lead to higher prices.

click to enlarge

- The Federal Reserve began shrinking its balance sheet in October of last year and has already shrunk it by about $179 billion, with an expectation of eventually shrinking by $1.9 trillion. However, as Cornerstone Macro writes, the balance sheet shrinking is contributing to push the effective federal funds rate closer to the top of the range the Fed specifies, which was not supposed to happen so early. This could lead to rates not being increased by as much or as fast as previously expected with the Fed maintaining $800 billion to $1 trillion than expected on its balance sheet.

Threats

- JPMorgan writes that if a global recession is looming, it might be time to own the Swiss franc, Singapore dollar, the U.S. dollar and the Japanese yen and to let go of emerging market currencies. Recessions are when creditors start to ask for their money back and the U.S. dollar would benefit since it is the world’s default funding currency. JPMorgan says that talk of a recession is “premature” and drew its research of currency performance over the last five recessions.

- A Bloomberg opinion piece from Noah Smith shows that tightened immigration policies might have been a contributing factor to the stock market crash of 1929. In 1924 immigration was severely curtailed and the result of this dramatic drop in population influx was that it reduced long-term economic growth. Reducing the flow of people also limited the economy. The housing crash in the mid-1920’s might have been a direct result of the tightening of immigration, which then exacerbated the stock market crash in 1929. History can repeat itself if the lessons are forgotten.

- The U.S. released a list of an additional $200 billion in tariffs on Chinese products this week. There have been growing signs of frustration among GOP lawmakers as House Speaker Paul Ryan has said that tariffs “are not the solution.” Bloomberg writes that many Republicans have said they want to give President Trump a chance to see if his tariff approach works or persuade him to back down, rather than restricting his power to impose such tariffs. The tariffs might not have taken much of a toll on the economy yet as a lull in U.S. consumer inflation in June could prove temporary as the tariffs take effect. Oddly on the new tariff list are rare earth elements that are used in everything from phones to wind turbines, but the U.S. has no domestic production and China accounts for 85 percent of the world’s production and 78 percent of our imports.

Emerging Europe

Strengths

- The Czech Republic was the best performing country this week, gaining 67 basis points. The Czech inflation rate rose in June to a seven-month high, boosting the case for more interest rate increases. The Consumer Price Index (CPI) is at 2.6 percent, above the central bank’s target of 2 percent. Andrej Babis won parliamentary approval for a minority government, ending more than eight month of political uncertainty.

- The Russian ruble was the best performing currency this week, gaining 73 basis points against the dollar. Despite Brent crude declining more than 6 percent this week, the Russian ruble, which usually is highly correlated with the price of oil, appreciated. International inflows in government bonds probably supported the ruble, according to an analyst at VTB Capital.

- The utilities sector was the best performing sector among eastern European markets this week.

Weaknesses

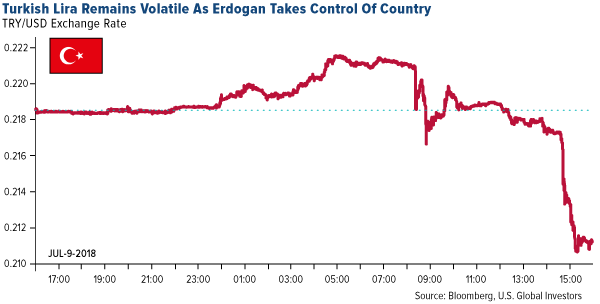

- Turkey was the worst performing country this week, losing 8.95 percent. Equites trading on the Istanbul exchange sold off sharply after President Erdogan was sworn into office on Monday, eliminating the prime minister position and ruling with executive powers. Banks declined the most, with Turkiye Garanti Bankasi losing 18.8 percent.

- The Turkish lira was the worst performing currency this week, losing 5.85 percent against the dollar. On Monday, the lira gained more than 1 percent against the dollar in the morning session of trading. However, the lira then sold off sharply, weakening by more than 3 percent in a single day. President Erdogan, under his new executive powers, announced that he would be appointing central bank members going forward, not the Cabinet. Moreover, he removed Mehmet Simsek, an investor-friendly Treasury and Finance Minister, from his Cabinet and names his son-in-law, Mr. Berat Albayrak, the former Energy Minister, to oversee economic policy.

click to enlarge

- The real estate sector was the worst performing sector among eastern European markets this week.

Opportunities

- China signed more than 20 agreements with Central and Eastern European (CEE) countries last Saturday to boost cooperation under the Belt and Road Initiative. These agreements involved in fields such as transport, infrastructure, industrial parks, finance, healthcare, education and agriculture. China-CEE cooperation, also known as the "16+1" mechanism, promotes the development of China and the sixteen CEE nations by shrinking the disparity inside members of the European Union (EU) for more balanced development. This will push forward European integration, said Premier Li Keqiang during his visit to Bulgaria.

- Turkey could end a state of emergency rule that was imposed after the failed July 2016 coup attempt. Most likely, it will not be extended after July 18, which could create some positive sentiment.

- Next week, the final June inflation data for the Eurozone will be released. Most Bloomberg Economists predict upward revision from 1.9 percent to 2 percent. Core inflation most likely will stay unchanged at 1 percent.

Threats

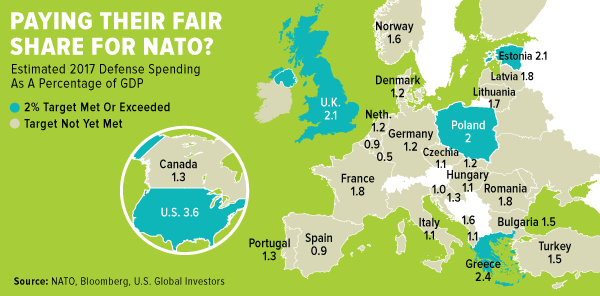

- NATO summits usually demonstrate unity among its members, but not this time. During this week’s meeting, Trump once again has criticized NATO members for not paying enough. Only five countries – US, UK, Greece, Poland and Estonia – meet their NATO obligation and pay at least 2 percent of their gross domestic product (GDP). He also criticized Germany for being too dependent on Russian gas, saying, “it certainly doesn’t seem to make sense that [Germany] paid billions of dollars to Russia and we have to defend them against Russia.” Germany aims to spend 1.5 percent of its GDP on defense by 2025.

click to enlarge

- In Germany, the far-right Alternative for Germany (AfD) party overtook the Social Democrats for the first time in polls. INSA poll, which was published by the Bild daily, gave the centre-left Social Democratic party 17 percent of the vote, with the AfD taking 17.5 percent. AfD is an anti-immigration, far-right party that is benefiting from the recent turbulence inside Chancellor Merkel’s coalition government over migration policies.

- German investor confidence declined to its lowest level since 2012, as trade war picks up between major economies. The ZEW Center for European Economic Research said on Tuesday that its Index of Investor Expectations fell to minus 24.7 in July from minus 16.1 in June. The negative reading means that more investors saw a worsening of the outlook than forecast an improvement.

© US Global Advisors

www.usfunds.com

© U.S. Global Investors

Read more commentaries by U.S. Global Investors