Midyear Outlook 2018: The Plot Thickens

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsIn a World of Rising Volatility, Will Opportunities Emerge?

When we as investors began 2018, we were tuned in to the recent fiscal policy changes that were expected to propel economic activity and the financial markets higher in the coming year. The handoff in leadership from monetary policy to fiscal policy was well underway as a driver of consumer spending, business investment, and corporate profits. Instead of depending on the Federal Reserve (Fed) to move this expansion forward, fiscal incentives are now critical for continued growth, with the new tax law taking the lead.

We often don’t see massive change without a little drama, however, and thus we expected this shift to come with a rise in stock market volatility after a very quiet 2017. Volatility would be normal, even healthy, as a sign that market forces were playing a larger role in directing the economy and stock prices and the accustomed support from the Fed was slowly fading into the backdrop.

The first half of 2018 broadly played out in line with our view, although with its own twists and turns. The shift to fiscal policy leadership, through changes in the tax code, deregulation, and increased government spending, were initially well received by markets. Then, as is often the case, investors grew concerned about the costs of these benefits, namely, Fed tightening, higher deficit spending, and the potential impact on inflation. As a result, early in the year we saw the S&P 500 Index’s first decline of over 10% since the Brexit vote in June 2016.

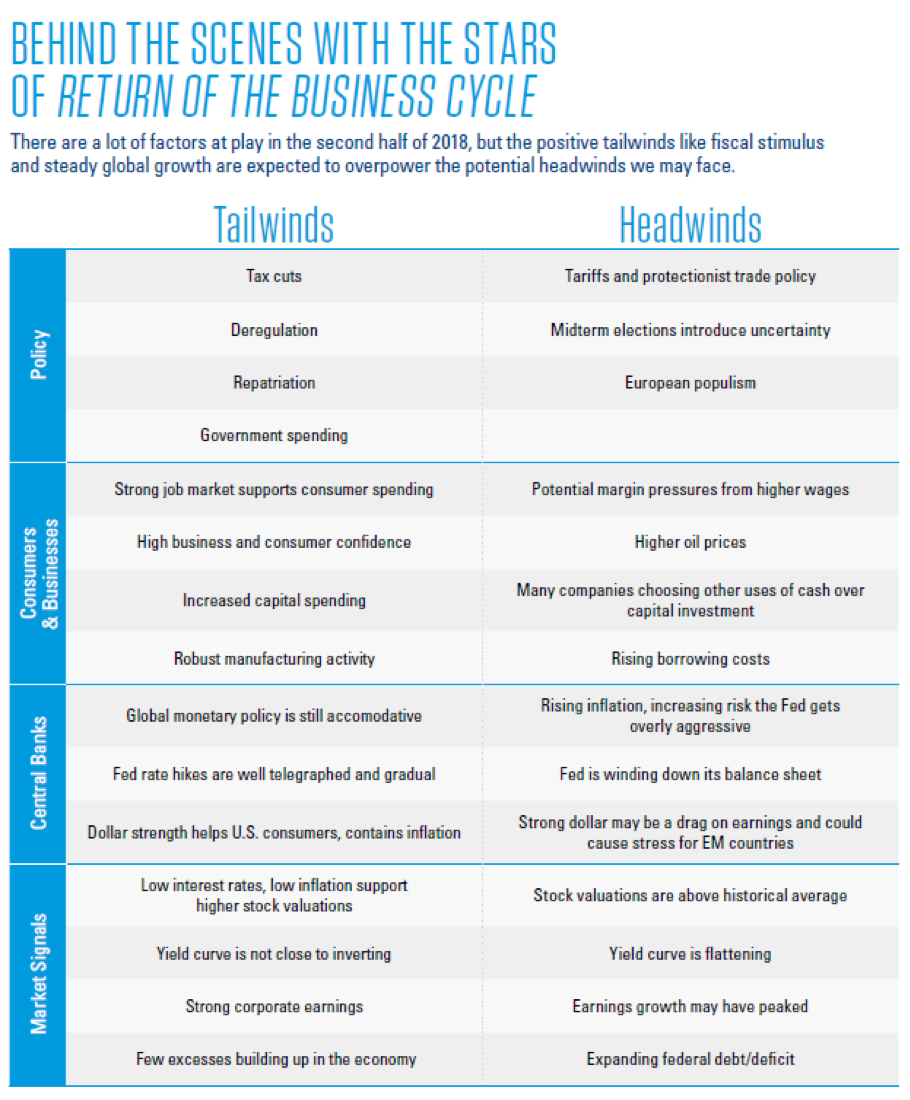

The stock market has been recovering since then. Although we believe the benefits of a return to the business cycle may further support markets and reward patient investors, navigating the volatility of a normal business cycle environment is something we haven’t seen in some time. This adds a layer of complexity to our current late cycle environment and the challenges we’re facing, such as trade tensions and upcoming midterm elections.

There’s also the potential for greater market sensitivity due to the late cycle concerns that can emerge when the economy is doing well. Peaks in manufacturing and earnings, along with higher short-term interest rates, all reflect a healthy economy, but they can also lead investors to wonder if that means this is as good as it gets.

So indeed, the plot has thickened. But that doesn’t mean we’ve taken a turn for the worse. The underlying forces are still forging ahead and this expansion and bull market have not been defeated. And, when we think about these potential obstacles, we should try to remember that challenges can be overcome and they may not signal the end of the story. Volatility means ups and downs. So it doesn’t need to be the villain we fear; instead, we should embrace it and strategize accordingly.

It’s also important to think of the big picture. Right now, there are many positive fundamentals, like business investment and corporate profits, supporting economic growth and potential market gains. With that backdrop, periods of weakness can be used as opportunities. Employing more active portfolio strategies, focusing on the beneficiaries of the shift from monetary to fiscal leadership, and positioning well-balanced portfolios for the long term are several potential ways to do this.

The LPL Research Midyear Outlook 2018: The Plot Thickens presents guidance on how the return of the business cycle may unfold during the remainder of 2018 and beyond, along with the investment insights to help investors navigate the twists and turns.

AT A GLANCE

KEY THEMES

Fiscal Policy

The handoff in leadership from monetary policy to fiscal policy in the U.S. is in motion, and we expect these fiscal measures may continue to drive the economy and stock market forward. Tax cuts, a more business-friendly regulatory environment, and increased government spending should support consumer spending, business investment, and corporate profits. We also expect these measures to outweigh the potential costs of higher tariffs. While the Fed is expected to continue raising interest rates, as long as a gradual approach continues, we believe it’s unlikely to result in a policy mistake.

Market Signals

We are starting to see peaks in several market indicators, but that doesn’t mean a recession is necessarily around the corner. Specifically, we may have seen peaks in manufacturing growth and earnings, while short-term interest rates are rising faster than long-term rates. However, growth can still be steady after a peak. The context is also critically important here—reaching these points in a positive growth environment is expected and not necessarily a warning sign. So although we are in the later stages of the economic cycle, we don’t see a recession in the near term.

Rising Volatility

Given that we are in the later stages of this economic cycle, with factors such as increased trade tensions and geopolitical uncertainty at play, we do expect greater volatility in 2018. But it’s important to remember that volatility isn’t defined simply as market declines, and experiencing these ups and downs is a normal aspect of our market environment. If we try to embrace it, instead of fearing it, we have the potential to create opportunities.

FORECASTS

Economy: Up to 3% Early this year we slightly upgraded our gross domestic product (GDP) forecast, as tax cuts should improve personal and business spending. We expect the combination of tax cuts, a new government spending package, and financial deregulation to support continued growth.

Stocks: 10%+ We expect strong earnings to remain the key driver of stock gains, thanks to the benefits of the new tax law. Although we do expect volatility to increase, in the context of steady economic growth and strong corporate profits, we see the potential for further stock gains in the second half of 2018.

Bonds: Flat to Low-Single-Digits As expected, accelerating global growth and rising interest rates continue to pressure bonds. We maintain our forecast of flat to low-single-digit returns for the Bloomberg Barclays U.S. Aggregate Bond Index, but believe high-quality bonds may provide diversification benefits for investors’ portfolios.

RECOMMENDATIONS

Top of the List

Investment ideas we can’t stop watching or talking about

- Small Caps: Beneficiaries of lower corporate tax rate, and their U.S. emphasis.

- Value: Relatively attractive valuations, and rate environment should help financials.

- Cyclical Stocks: Accelerating growth may support economically sensitive sectors.

- Emerging Markets: Strong growth and attractive valuations offset tighter monetary policy.

- Bank Loans: Floating rates may benefit holders if short-term rates rise further.

- Investment-Grade Corporates: Added yield versus Treasuries is attractive; we favor intermediate maturities.

Recommended for You

They may not be grabbing all the buzz, but these ideas could be a solid addition to your queue

- U.S. Stocks: Accelerating growth and fiscal stimulus provide an edge.

- Mortgage-Backed Securities: Yield relative to rate sensitivity is attractive, but slowing Fed purchases limit upside.

- High-Yield Corporates: Yields are attractive despite full valuations.

Save for Later

These investments may not be at the top of your list this year, but don’t count them out

- Developed International Bonds: Accelerating growth and very low yields create little margin of error.

- Developed International Stocks: European growth may have peaked, while structural concerns remain.

- Long-Term High-Quality Bonds: Offer inadequate compensation for added rate sensitivity.

- U.S. Defensive Stocks: Economic growth and rising rates decrease attractiveness.

LAUNCHING POLICY ACTION

The positive impact of tax cuts is up against increased deficit spending and ongoing trade tensions. In the end, we expect the benefits to heavily outweigh the costs.

Our view on the return of the business cycle was premised on policy delivering incentives for businesses to hire and invest, and consumers to have the choice over how to use a greater proportion of their income. The $1.5 trillion tax cut passed at the end of 2017 has already started to have a big impact on major corporations, small businesses, and individual taxpayers—and we think there’s a lot more to come. Lower corporate tax rates initially grabbed the most attention, but the legislation delivered a larger than expected boost to individuals, which should provide support for future consumer spending.

Along with lower tax rates, the new law includes other provisions for businesses that could further stimulate economic growth. These tax advantages encourage companies to invest in capital projects (thanks to immediate expensing) and bring their overseas profits back to the U.S. (known as repatriation). Both of these elements have the potential to benefit the economy in the long term.

A Friendlier Setting

The tax law may be the new star, but that’s not the only policy action in town. Other measures that may be supportive of economic and profit growth include an ongoing reduction in regulatory hurdles for energy infrastructure and financial institutions, as well as a new federal budget. Passed in March 2018, the new budget includes a total of $300 billion in additional government spending over the next two years.

Both Congress and the Fed have also taken action to create a more business-friendly regulatory environment. Congress recently passed a law reducing the number of banks deemed systemically important financial institutions (SIFI), while the Fed has announced plans to ease up on the severity of bank stress testing. As a result of these measures, banks have more lending capacity, which is a positive for the economy.

Under the leadership of new Chair Jerome Powell, the Fed has also remained consistent in its intentions to both gradually raise interest rates and reduce the size of its balance sheet. At its most recent meeting in June, the Fed raised its target for the federal funds rate by 0.25% (or 25 basis points), to a range of 1.75–2.0%. Though we expect the Fed to raise rates a total of three times in 2018 (so one more additional hike), the possibility exists for a fourth; we maintain our confidence that this gradual approach is unlikely to result in a policy mistake.

Could There Be a Twist?

Yet, as is often the case, policy tailwinds confront headwinds, and the costs are weighed against the benefits. Of course, this usually occurs after decisions are made and laws are signed. To be sure, the costs of the tax cuts and additional government spending plans have resulted in increased deficit spending and Treasury issuance at a time when the Fed is no longer supporting the market for government debt by purchasing bonds. This has contributed to bond investors demanding higher yields to offset these risks. And, fortunately, market interest rates have been heading higher, with improved growth expectations and an accompanying manageable pickup in inflation serving as the main drivers.

The biggest risk to investor confidence has been around trade, including new tariffs and trade negotiations. President Trump’s call to increase tariffs has weighed on sentiment, with the tax-related market gains tempered by the potential for higher trade costs. Some of what’s occurring is likely part of a negotiating tactic; nonetheless, the threat of a trade war is real and disturbing to investors and businesses.

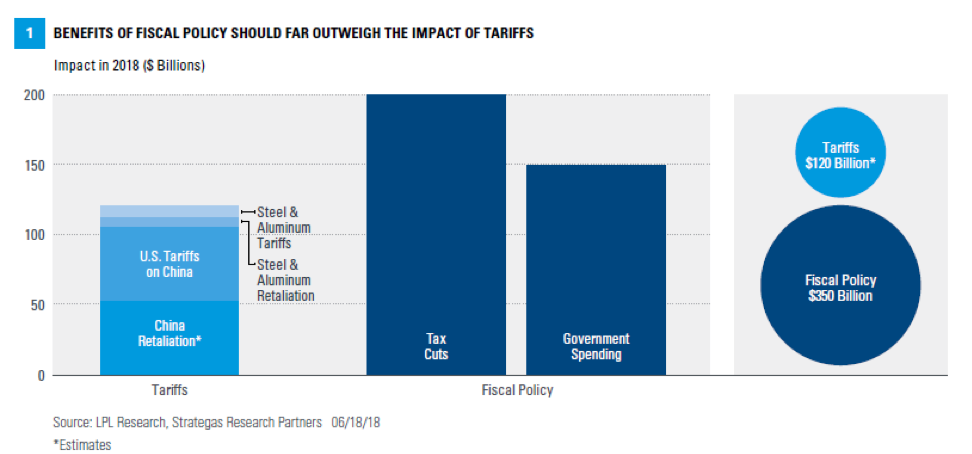

We do believe that some perspective is in order when considering trade risks. The size of the fiscal stimulus from tax cuts and increased government spending should far outweigh the threatened import duties. Between the U.S. tariffs and China’s projected retaliation, in particular, those costs are estimated at approximately $105 billion over the next year (on top of the $15 billion in steel and aluminum tariffs already announced), yet the U.S. fiscal policy tailwinds amount to $350 billion [Figure 1]. There is also the potential added impact of businesses bringing home foreign profits. The tariffs are also still subject to revisions as negotiations evolve, whereas the tax law is permanent and we believe may have a growing impact on individuals and businesses.

So we think the good should outweigh the bad, thanks to the benefits of fiscal policy, with a potentially greater impact on growth than is currently anticipated.

WORLDWIDE ECONOMY MAY SOAR

Domestically, now that fiscal measures are in place, we expect the U.S. economy to reap those benefits and start seeing better growth. Globally, the economic growth outlook for emerging markets may outshine developed international markets.

We believe that the global growth story will continue, with an expectation of 3.8% GDP growth for the world economy, thanks to new fiscal policies and improved business vitality [Figure 2]. We continue to expect the U.S. economy to remain a primary driver, aided by the anticipated higher growth trajectory of emerging markets, while Europe and Japan may lag. Primary risks include an unexpected rise in inflation, a substantial increase in trade friction, or a policy mistake.

Last Time, on the U.S. Economy

The U.S. economy grew at a rate of 2.2% in the first quarter, which was better than the consensus estimate of 2.0% but a slowdown from the near 3% growth of the prior three quarters. First quarter averages are historically lower, so this type of seasonal dip is not unusual. In addition, although the supportive fiscal measures had been enacted, it was a little early for them to affect growth in the first quarter.

Fiscal Stimulus Drives the Story

While the threat of tariffs and increased oil prices may weigh on consumption and investment decisions, we believe the positive impacts of fiscal stimulus will prevail for the remainder of the year. The individual tax cuts should improve consumer spending, an important driver of economic growth, while the influence on business spending may be even more impactful. As companies experience higher profitability, this should trickle down to other elements of the economy, with profits helping to drive growth in employment, wages, consumption, and investment. Add the government spending package signed earlier this year and the benefits of increased lending capacity (from recent financial deregulation), and we’re looking at significant fiscal tailwinds. We continue to believe that the combination of these forces will result in GDP growth of up to 3% for the U.S. in 2018.

Are Signs Pointing to a Climactic Moment?

We’re continuing to see a healthy labor market, with unemployment at its lowest level in 18 years (at 3.8% as of May). Underemployment (includes those who are employed part time but would like to work full time), at 7.6%, is also near previous cycle lows. A tighter labor market is often viewed as a precursor to higher wage growth and ultimately higher inflation, but sustaining inflation above the Fed’s comfort range has been elusive so far. Wages and prices, as well as market interest rates, have climbed recently, though wage growth at current levels of about 2.8% on a year-over-year basis is still well below the 4.0% pace that has typically concerned central bankers. As a result, we continue to look for inflation to climb gradually, with the Consumer Price Index finishing the year in the 2.25–2.5% range.

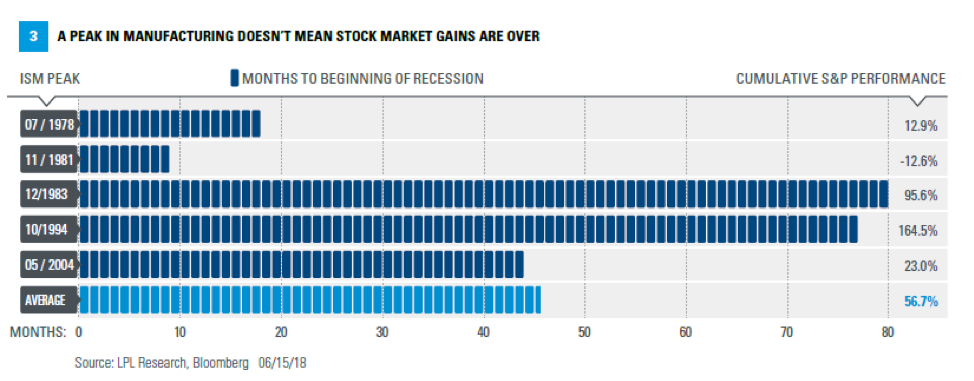

Manufacturing doesn’t have the clout it once did in the economy as a whole, but the financial performance of manufacturing firms still has a major impact on S&P 500 Index earnings. In addition, the Institute for Supply Management (ISM) manufacturing index, which measures whether manufacturing as a whole is expanding or contracting in the U.S., hit its strongest level in over a dozen years in February 2018.

It would be easy to perceive the recent peak in manufacturing growth to be a negative for the economy, but even when you’re past the peak, growth can still be steady. History has also shown that a peak in ISM manufacturing does not typically mean the end of stock gains or that a recession is around the corner. As shown in Figure 3, on average over the last five economic cycles, expansions have continued for nearly four years following an ISM manufacturing peak, during which the S&P 500 has cumulatively gained an average of nearly 57%.

Emerging Markets’ Key Supporting Role

Looking at developed international, consensus expectations1 for European growth have increased, though we suspect forecasters may have gotten ahead of themselves as European and Japanese data have been coming in below heightened expectations in recent months. We still believe both Europe and Japan will see growth in 2018, but our expectation of 2.1% growth for developed international remains below consensus expectations.

From our perspective, the emerging economies still appear to have a more sustainable growth trajectory. Though tariffs and the potential for a trade war with China have weighed on investor sentiment and could take a toll on emerging markets, we don’t expect these factors to derail their growth trajectory. We continue to expect the U.S. and China will successfully navigate trade issues and ultimately reach an agreement, particularly once the crucial intellectual property policy issues are addressed.

Despite these challenges, we expect that the powerful demand trajectory driven by 6 billion emerging market consumers, along with innovative businesses embracing dynamic global output changes, should result in emerging market economic growth approaching 5.0% in 2018.

SWITCHING LANES WITH BONDS

When considering the overall bond market, investors face several challenges, the combination of which may pressure bond prices over the next few years.

As expected, the return of the business cycle and the accelerating economic growth that has accompanied it have combined to push market interest rates higher in the first half of the year. Periods of stock market volatility have resulted in temporary “flights to quality” where investors seek safe-haven assets like U.S. Treasury bonds,2 pushing their yields lower and highlighting the diversification benefits of high-quality fixed income within portfolios. However, we continue to believe the long-term fundamental drivers, including economic growth, deficit spending, rising inflationary pressures, and expectations of future Fed rate hikes, may push bond yields marginally higher as the year progresses. Given this back and forth volatility in market interest rates, we encourage suitable investors to employ more active strategies within their fixed income portfolios going forward.

Deciphering the Yield Curve Signal

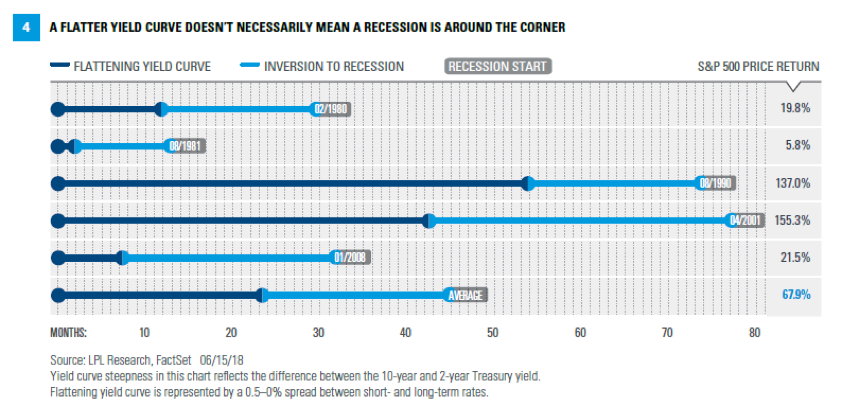

This volatility in market interest rates has been accompanied by a flattening of the U.S. Treasury yield curve, where short-term rates have risen faster than long-term rates. This may eventually lead to an inverted yield curve where short-term rates are above long-term rates. Historically, this has been a negative signal for the U.S. economy, often providing an early warning of an eventual recession. Yet in this circumstance, we believe that the curve flattening with interest rates rising (rather than falling) is a market signal pointing toward future growth.

Moreover, a look at the last five cycles shows that the average time it takes from a flattening yield curve (represented by a 0.50% spread between short- and long-term rates) to a recession has been almost four years, with stock prices climbing by an average of 67.0% during that time frame [Figure 4]. Outliers have skewed the average, but a median return of 21.0% is a helpful reminder of the need for investors to maintain a long-term outlook.

Maneuvering Around Those Rising Rates

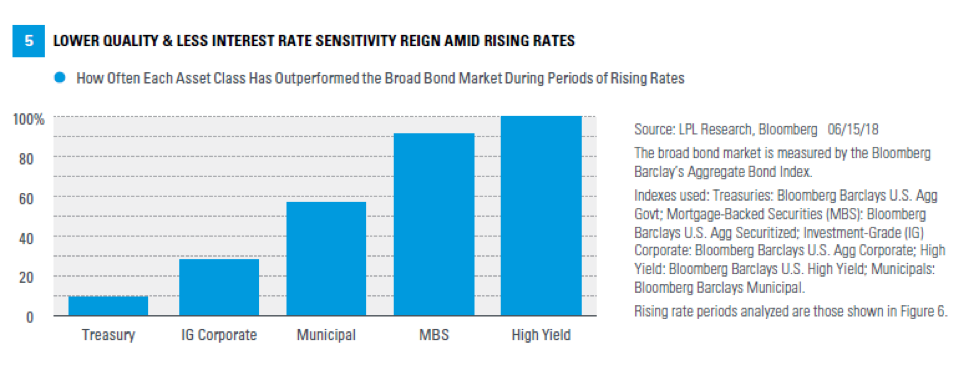

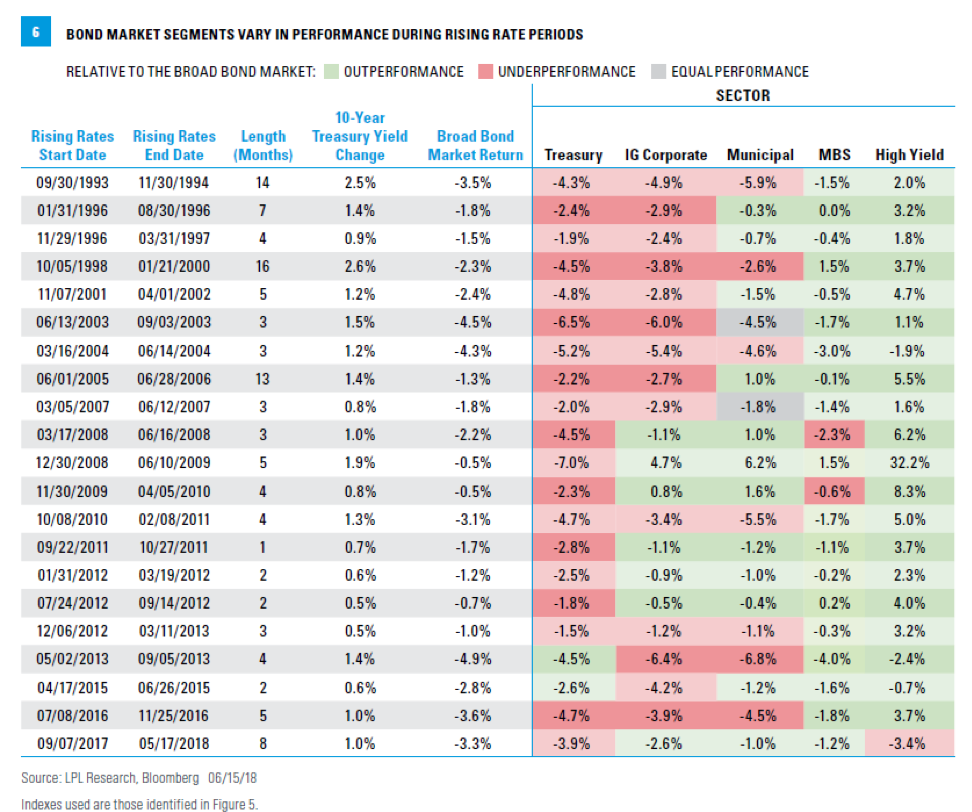

Considering our recommendation for a more active approach to bonds, it is important to identify how different types of fixed income securities have performed in rising interest rate environments [Figures 5, 6]. As a reminder, we expect yields to grind gradually higher with periodic bouts of volatility, and we maintain our year-end forecast of 2.75–3.25% for the 10-year Treasury. Risks to our forecast include a meaningful upside surprise in inflation or growth, which could pressure rates higher.

U.S. Treasuries: Within the sub-asset classes for bonds, U.S. Treasuries tend to have the most interest rate sensitivity, and historically have performed poorly during Fed tightening cycles. Though increased Treasury issuance to fund federal deficit spending will accentuate this trend, an attractive valuation compared to other sovereign debt may support buying, which should help contain yields.

Investment-grade (IG) corporates: Though investment-grade corporate bonds are also sensitive to a more aggressive Fed, better economic growth is helping to contain the interest rate differentials (spreads) to Treasuries, suggesting investor confidence in their ability to service their debt. Also, to boost this confidence, corporations have gone to great lengths to maintain healthy balance sheets and tighten their income statements during these past several years, evidenced by still low debt-to-earnings ratios. Perhaps more important, the contained spreads collectively indicate a lack of stress in credit markets.

Munis: Higher-quality municipal securities tend to hold up better than Treasuries in rising rate periods, as their tax-exempt status historically attracts investor assets.

MBS: While higher-quality mortgage-backed securities (MBS) have performed well in previous rising rate environments, they are not without their own risks. If rates move significantly higher, fewer homeowners refinance their mortgages at those higher rates, leaving MBS investors with longer maturities than expected, essentially locking in lower interest rates.

High-yield: For suitable investors, other areas of fixed income may enhance yield within diversified portfolios, including bank loans and high yield. With less sensitivity to rising rates, we believe high-yield corporate bonds remain attractive given the combination of income potential and reduced default risk, given solid economic growth prospects. Nonetheless, we encourage investors not to get too enticed by the higher yields, which can often mask other fundamental deficiencies for companies in this space.

Don’t Speed Toward International Bonds

Global bonds present a mixed bag of opportunities and risks. As mentioned earlier, U.S. Treasuries remain relatively attractive when compared with other sovereign debt. Global investors may be attracted to the 10-year Treasury yielding near 3.0%, for example, in comparison to the German bund, hovering around 0.50%, or the Japanese government bond, which yields less than 0.05%. Currency translation matters, though, and we continue to favor hedging that risk in developed markets. Emerging market debt yields appear attractive, yet investors should be mindful of escalating trade conflicts.

Finally, we want to emphasize that fixed income continues to play an important role in a diversified portfolio. Bonds can provide income and liquidity, and may serve to help manage portfolio volatility during periods of stock market turbulence. We continue to position portfolios with below-benchmark (Bloomberg Barclays Aggregate) interest rate risk, preferring to take credit risk in the current environment.

OVERCOMING OBSTACLES WITH STOCK GAINS

The current environment looks favorable for strong earnings and stock gains. We do expect volatility, but steady economic growth provides a strong backdrop and the potential for opportunity.

The first half of 2018 saw the return of equity volatility after the docile trading patterns of 2017. The surge in bond yields after the January jobs report, along with the initial trade concerns in late March, resulted in the first market corrections (a pullback of at least 10.0%) since the Brexit vote in June 2016. Though higher bond yields caused market disruptions, rising market interest rates (especially from relatively low levels) have typically been associated with an improving economy and higher stock prices. As a result, when viewing market volatility in the context of steady economic growth, it is not something to fear, in our opinion, but to embrace, as temporary market sell-offs may provide suitable investors with opportunities to rebalance portfolios toward long-term targets.

Given that the Fed is well on its way to unwinding accommodative measures, we encourage investors to focus on the fiscal tailwinds of favorable taxes, regulation, and government spending, while identifying companies that are willing and able to take advantage of these developments.

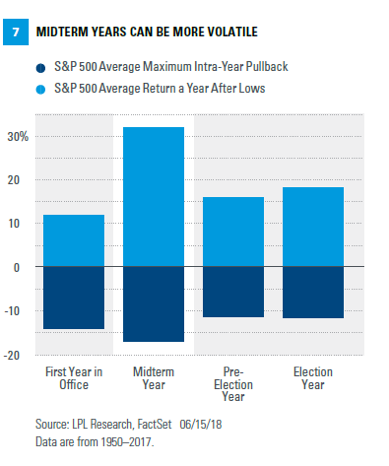

Midterm Elections: The Next Market Challenge?

Throughout the increased volatility in the first half of the year, we’ve emphasized to investors that “bottoming is a process.” In other words, when the market does experience a correction, even as the catalysts for that decline dissipate, the recoveries can still take several months. We saw this in 2011 and 2015, and this year has been no exception. The second half of the year will also likely see the added potential headwind of midterm elections, which have historically provided the most volatility within the four-year presidential election cycle.

Because the president’s party typically loses approximately 25 House seats, investors have historically struggled with the policy uncertainty leading up to midterm elections. The good news is that stocks tend to bounce back strongly after midterm election year corrections, as the average decline (-16.0%) is followed by a solid recovery from the trough (+32.0%) over the ensuing 12 months [Figure 7].

The Strength to Persevere

We also believe that during volatile periods, investors should focus on positive fundamentals like the strength in corporate profits. In the first quarter of 2018, S&P 500 Index companies’ earnings per share (EPS) came in well ahead of expectations. Given this development, we have decided to slightly upgrade our operating earnings forecast from $152.50 to $155.00 per share for the S&P 500, which would represent approximately 17.0% year-over-year growth.

Our forecast is still below consensus expectations and may prove conservative given the substantial impact of the transition to fiscal leadership. However, we remain cautious due to several ongoing factors that could affect earnings:

- A stronger U.S. dollar would affect the EPS currency translation for multinational companies

- Geopolitical risks and trade tensions may hinder capital spending

- Wage increases could negatively impact companies’ profit margins

Based on our earnings forecast (of $155 EPS), our fair value projection is for the S&P 500 to trade within the range of 2900–3000 by year-end, which at the midpoint represents an annual increase in excess of 10.0% for the index and a target price-to-earnings (PE) ratio of 19. A PE of 19 is slightly above its historical average; however, when put in the context of still relatively low interest rates and low inflation, we believe a PE at this level is justified.

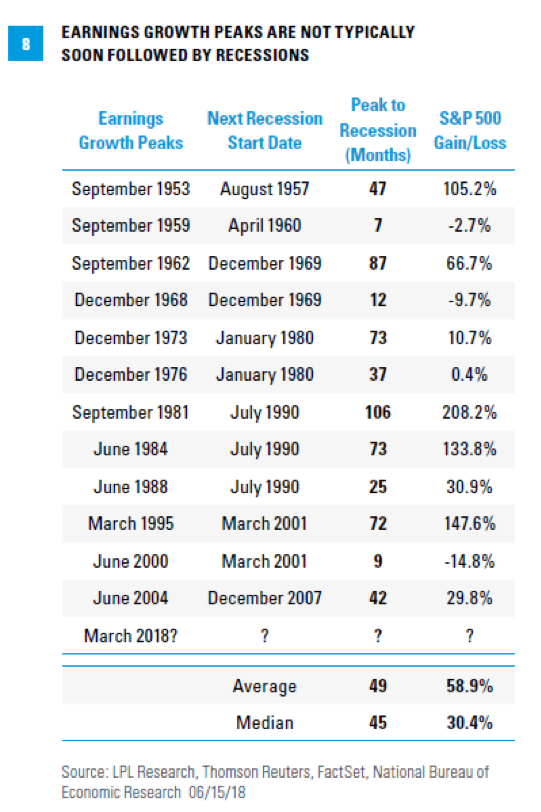

Earnings Have Climbed to the Top

Another concern for investors that has recently surfaced is whether the recent first quarter earnings season would prove to be “as good as it gets.” Despite widespread discussion of “peak profits,” the first quarter EPS growth of more than 25% year over year does not necessarily mean trouble is imminent—even if it were to be the percentage EPS growth peak in this cycle. In fact, a look back at six decades of earnings growth peaks suggests that it typically takes about four years from a profit growth peak before the economy slips into recession [Figure 8]. It is noteworthy that the S&P 500 gained an average of 59% during these periods between earnings growth peaks and the start of the next recession.

Developed International May Be the Weak Link

The profit story remains a global one, although earnings growth expectations are not as strong in developed international markets. A combination of slower economic activity (Japan) and political disruptions (Europe) have weighed on investor sentiment. We also remain concerned about government debt levels, and the potential for continued political uncertainty has led us to prefer U.S. and emerging markets.

Though emerging markets have been pressured by a combination of rising interest rates, U.S. dollar strength, and fears of a trade war, we continue to believe that advantageous demographics, early cycle acceleration, and commodities gains will ultimately benefit the group. This positive economic outlook is translating to a strong earnings growth outlook, with consensus estimates showing an expectation of approximately 14.0% EPS growth, while valuations remain attractive. Trade remains a key risk for emerging market nations, especially China and Mexico, which could continue to pressure their stocks in the near term.

Can Stocks Prevail in the End?

In the spirit of embracing volatility, we recommend that investors take advantage of periodic weakness to invest excess cash or rebalance portfolios back toward targeted long-term allocations. The fundamentals supporting economic growth and corporate profits remain solid from our perspective, and we’ll continue to position portfolios toward beneficiaries of the transition from monetary to fiscal leadership.

As a result, we continue to favor small caps over their large cap counterparts, primarily because of the new tax law, trade policy, and a potentially stronger U.S. dollar. Small cap companies generally had higher taxes, so they benefit more from the reduction in corporate rates. With less overseas revenue, small cap companies are not impacted as much by tariffs and the stronger dollar is less of a drag, compared with large caps.

Though the growth style of investing has maintained momentum, we continue to see attractive valuations on the value side and a fair amount of cyclical value stocks that we think will benefit from the return of the business cycle. Value stocks have historically performed better when economic growth accelerates, a condition that is in place today. We believe the financials sector is well positioned given lower taxes, deregulation, higher interest rates, and attractive valuations. Industrials should prosper given capital investment growth, immediate expensing opportunities, and solid global growth. Technology should also maintain momentum, which can be justified by lower taxes and higher business investment.

Finally, we continue to favor emerging market stocks over developed international for the reasons we described earlier. While we expect volatility to persist, we also believe that it represents an opportunity for investors as the economic and profit cycle persists.

Overall, earnings growth may have peaked and volatility may stay with us. But we see enough growth in the economy and corporate profits to potentially carry stocks to further gains in the second half of 2018.

Up Next

New market-driving forces have arrived. With fiscal incentives in place, and monetary policy support fading into the background, we expect steady economic growth and stock market gains may continue throughout 2018 and beyond. However, we would be remiss not to acknowledge the potential for increased volatility along the way, as we are in the later stages of the economic cycle and factors such as trade tensions and geopolitical uncertainty can raise investors’ concerns. We’ve suggested that investors embrace this volatility, instead of fearing it. So what does that mean exactly?

For one, by expecting volatility, we may be better equipped to manage it. Experiencing market declines, or ups and downs, can be unnerving for any investor; but when we’re prepared, it can be easier to stay calm and avoid emotional reactions. In addition, we need to remember that volatility does not necessarily mean that the bull market is over or that a recession is looming. In fact, volatility is a normal part of investing, and a sign that traditional market forces are guiding the economy and stock market, just as we expected with the return of the business cycle.

Keeping all of that in mind, as we prepare for the rest of 2018—and even further to 2019—we will be looking for opportunities to make the most out of any ups and downs in the markets. For suitable investors, market weakness can mean a chance to take advantage of lower stock prices, or to reallocate a portfolio so that it’s more in line with long-term targets. Remembering those long-term goals during these periods is often helpful, particularly when trying to avoid reacting in the short term.

Another key theme that may gain attention this year is that certain economic and market indicators have peaked, and that we may have seen the best out of this expansion. Although we may not top first half results from manufacturing and earnings reports, and short-term interest rates continue to rise, context is critical here. Reaching these milestones with a strong economic backdrop indicates the potential for continued, steady growth; while historically speaking, we’ve seen an average of four more years of stock gains after triggering these market signals.

With the shift in market leadership and continued uncertainty regarding trade and the upcoming midterm elections, as well as the heightened sensitivity of a late cycle market, there are many factors at play. So the plot has thickened, but that doesn’t mean the story of this bull market is over. We continue to see the potential for economic and market growth in 2018 and beyond, and will strategize accordingly should volatility ramp up as we expect.

Armed with the investment insights of LPL Research’s Midyear Outlook 2018, and supported by the guidance of a trusted financial advisor, we expect investors can remain optimistic that what’s “up next” may be positive for their investment portfolios.

IMPORTANT DISCLOSURES

The opinions voiced in this material are for general information only and are not intended to provide or be construed as providing specific investment advice or recommendations for any individual security. To determine which investments may be appropriate for you, consult your financial advisor prior to investing.

All indexes are unmanaged and cannot be invested into directly. Unmanaged index returns do not reflect fees, expenses, or sales charges. Index performance is not indicative of the performance of any investment. All performance referenced is historical and is no guarantee of future results.

Economic forecasts set forth may not develop as predicted, and there can be no guarantee that strategies promoted will be successful.

Investing involves risks including possible loss of principal. No investment strategy or risk management technique can guarantee return or eliminate risk in all market environments.

Investing in stock includes numerous specific risks including: the fluctuation of dividend, loss of principal, and potential illiquidity of the investment in a falling market.

Investing in foreign and emerging market securities involves special additional risks. These risks include, but are not limited to, currency risk, geopolitical risk, and risk associated with varying accounting standards. Investing in emerging markets may accentuate these risks.

The prices of small cap stocks are generally more volatile than large cap stocks.

Value investments can perform differently from the market as a whole. They can remain undervalued by the market for long periods of time.

Because of their narrow focus, sector investing will be subject to greater volatility than investing more broadly across many sectors and companies.

Bonds are subject to market and interest rate risk if sold prior to maturity. Bond and bond mutual fund values and yields will decline as interest rates rise and bonds are subject to availability and change in price.

Government bonds and Treasury bills are guaranteed by the U.S. government as to the timely payment of principal and interest and, if held to maturity, offer a fixed rate of return and fixed principal value. However, the value of fund shares is not guaranteed and will fluctuate.

International debt securities involve special additional risks. These risks include, but are not limited to, currency risk, geopolitical and regulatory risk, and risk associated with varying settlement standards. These risks are often heightened for investments in emerging markets.

High-yield/junk bonds (grade BB or below) are not investment-grade securities, and are subject to higher interest rate, credit, and liquidity risks than those graded BBB and above. They generally should be part of a diversified portfolio for sophisticated investors.

Municipal bonds are subject to availability and change in price. They are subject to market and interest rate risk if sold prior to maturity. Bond values will decline as interest rates rise. Interest income may be subject to the alternative minimum tax. Municipal bonds are federally tax-free, but other state and local taxes may apply. If sold prior to maturity, capital gains tax could apply.

Mortgage-backed securities are subject to credit, default, prepayment, extension, market, and interest rate risk.

There is no guarantee that a diversified portfolio will enhance overall returns or outperform a nondiversified portfolio. Diversification does not ensure against market risk.

Rebalancing a portfolio may cause investors to incur tax liabilities and/or transaction costs and does not assure a profit or protect against a loss.

All information is believed to be from reliable sources; however, we make no representation as to its completeness or accuracy.

DEFINITIONS

Credit risk is the risk of loss of principal or loss of a financial reward stemming from a borrower’s failure to repay a loan or otherwise meet a contractual obligation. Credit risk arises whenever a borrower is expecting to use future cash flows to pay a current debt. Investors are compensated for assuming credit risk by way of interest payments from the borrower or issuer of a debt obligation. Credit risk is closely tied to the potential return of an investment, the most notable being that the yields on bonds correlate strongly to their perceived credit risk.

Interest rate risk is the risk that an investment’s value will change due to a change in the absolute level of interest rates, in the spread between two rates, in the shape of the yield curve or in any other interest rate relationship. Such changes usually affect securities inversely and can be reduced by diversifying (investing in fixed-income securities with different durations) or hedging (e.g. through an interest rate swap).

The modern design of the S&P 500 stock index was first launched in 1957. All performance back to 1928 incorporates the performance of predecessor index, the S&P 90. Yield curve is a line that plots the interest rates, at a set point in time, of bonds having equal credit quality, but differing maturity dates. The most frequently reported yield curve compares the 3-month, 2-year, 5-year, and 30-year U.S. Treasury debt. This yield curve is used as a benchmark for other debt in the market, such as mortgage rates or bank lending rates. The curve is also used to predict changes in economic output and growth. The Consumer Price Index (CPI) is a measure of the average change over time in the prices paid by urban consumers for a market basket of consumer goods and services.

Gross domestic product (GDP) is the monetary value of all the finished goods and services produced within a country’s borders in a specific time period, though GDP is usually calculated on an annual basis. It includes all of private and public consumption, government outlays, investments, and exports less imports that occur within a defined territory.

INDEX DEFINITIONS

The S&P 500 Index is a capitalization-weighted index of 500 stocks designed to measure performance of the broad domestic economy through changes in the aggregate market value of 500 stocks representing all major industries.

The Bloomberg Barclays U.S. Aggregate Bond Index is a broad-based flagship benchmark that measures the investment-grade, U.S. dollar-denominated, fixed-rate taxable bond market. The index includes Treasuries, government-related and corporate securities, MBS (agency fixed-rate and hybrid ARM pass-throughs), ABS, and CMBS (agency and non-agency).

The Bloomberg Barclays U.S. Corporate Bond Index measures the investment grade, fixed-rate, taxable corporate bond market. It includes U.S. dollar-denominated securities publicly issued by U.S. and non-U.S. industrial, utility and financial issuers.

The Bloomberg Barclays U.S. Corporate High Yield Bond Index measures the U.S. dollar-denominated, high yield, fixed-rate corporate bond market. Securities are classified as high yield if the middle rating of Moody’s, Fitch and S&P is Ba1/BB+/BB+ or below. Bonds from issuers with an emerging markets country of risk, based on Barclays EM country definition, are excluded.

1 LPL Research refers to Bloomberg for its source for consensus expectations.

2 U.S. Treasuries may be considered “safe haven” investments but do carry some degree of risk including interest rate, credit, and market risk. They are guaranteed by the U.S. government as to the timely payment of principal and interest and, if held to maturity, offer a fixed rate of return and fixed principal value.

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All