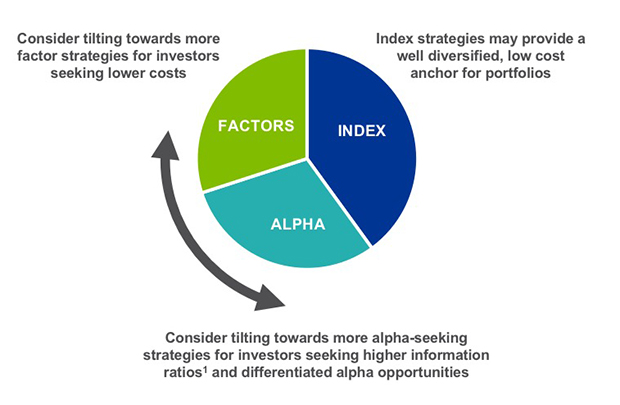

Yesterday’s alpha has been unbundled into market capitalization index, factors and alpha-seeking investments. What does this mean for investors?

The first album I bought was Thriller by Michael Jackson. I loved hearing and seeing this phenomenal artist. But even on this blockbuster album, I tended to listen to my favorite tracks: Billie Jean, Beat It, and Thriller itself.

Released in 1982, Thriller sold 66 million copies, and album sales have been shrinking since. Music streaming services like Spotify or SoundCloud mean we no longer need to buy the whole album. We listen to the tracks we want, at the time we want—and our playlists are better for it.

Just like the music industry, asset management is undergoing a transformation of its own.

Separating the Tracks

For illustrative purposes only.

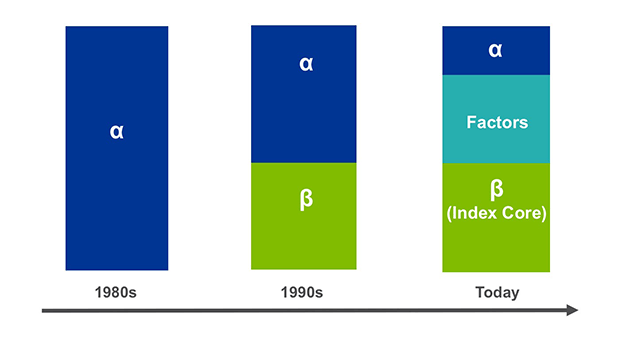

In the 1980s, when I was buying Thriller, investors used to go to one fund manager and buy all the tracks. The fund manager would bundle market-capitalization weighted index (or beta), factors, and alpha together. Beginning in the 1990s, we started to measure the returns generated by active managers in excess of market cap benchmarks. Today, we recognize that some of those excess returns are now attributable to factors—broad and persistent sources of return that are well understood but have continued to endure. True alpha today involves specialized skills, or being able to react tactically to non-repeatable market conditions beyond factors.

Just as you no longer have to buy the whole album, investors can now take the components that are right for them and pay the appropriate price.

Amplifying the Sound

Just as three chords (I-IV-V) underpin much of Western music, here are three principles to ensure the different portfolio components—index, factors, and alpha— play in sync:

- Understand what’s driving your returns. There are plenty of active managers out there who are delivering true alpha. But there are some who ARE just loading up on factor exposures. With tools like BlackRock’s Factor Box, it’s possible to evaluate the factor exposures in actively managed equity mutual funds and to see if those same exposures can be replicated with lower-cost, fully transparent, smart beta ETFs. Using Factor Box is like turning off Auto-Tune on a song: you get to see (or hear) how good your favorite active managers (or singers) really are.

- Select appropriate managers. Once you understand what’s really driving the returns of different funds, manager selection can get a whole lot easier. If you want one simple rule, try this: don’t pay active fees for factor-based returns.

- Revamp your portfolio. Chances are, you may want to make some changes to your existing portfolio. In addition to replacing active managers that aren’t delivering true alpha, you may want to add certain style factors to obtain more balance in your portfolio. Some investors may consider tilting toward certain factors, depending on where we are in the business cycle.