Trade actions are capturing a great deal of media attention, and justifiably so. However, the actual tariffs are still relatively new. The Section 232 tariffs on steel and aluminum are only a month old, and the first round of Section 301 tariffs targeting China have only just gone into force. The economic effects of those actions (and resulting retaliations against them) are not yet manifest in economic data.

The challenge of forecasting the shock of tariffs is the lack of a counterfactual case. We expect the U.S. economy to continue growing, but not quite at the rate it could achieve without these impairments to free trade. Our outlook for 2018 is positive, with 3% real growth expected this year. We expect a reduction in growth to follow in 2019 as the costs of trade actions become clearer, and as short-term incentives from the Tax Cuts and Jobs Act expire.

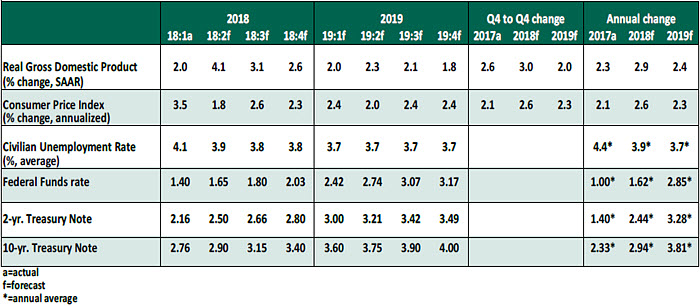

Key Economic Indicators

Influences on the Forecast

- The unemployment rate increased slightly to 4.0% in June from 3.8% in May.While rising unemployment is often seen as a warning sign, it appears this increase was driven by factors that reflect well on the economy.

- The pace of job creation remains strong, with 213,000 jobs created in June and upward revisions to estimates for April and May.However, more than 600,000 people were estimated to have re-entered the workforce, which drove up the unemployment rate.

- The labor force participation rate accordingly increased slightly to 62.9%, reflecting the additional job seekers.The participation rate is now above its age-adjusted norm (its natural course is a shrinkage over time because of retirements).

- First quarter real gross domestic product (GDP) was revised downward to a 2.0% annual pace, an insignificant change from initial estimates. We expect this to be the slowest quarter of 2018, with better growth to follow. Early indications suggest the second quarter’s GDP will be strong.

- Inflation continues to show signs of moderate growth. The Consumer Price Index grew 2.8% year-over-year in May, the highest level seen thus far in this economic cycle. The deflator on core personal consumption expenditures, the Fed’s preferred measure of inflation, has increased 1.96% over the past year, just shy of the Fed’s target of 2%. As trade actions are poised to increase costs, we anticipate inflation to continue to rise.

- Wage growth is keeping pace with inflation but has yet to take off in the manner we would expect during an interval of low unemployment. Average hourly earnings grew by 2.7% year-over-year in June, continuing a trend of steady growth. Despite moderate income growth, real personal spending in May was flat.

- The practical outcomes of trade actions are starting to show anecdotally, as exemplified by Harley-Davidson’s decision to expand its manufacturing capacity outside the U.S.Such actions are being taken in expectation of higher costs for raw materials. Reflecting this, the prices paid component of the Purchasing Managers’ Index (PMI) stood at 76.8 (where a reading over 50 indicates growth), down slightly from its May reading but remaining elevated.

- As widely anticipated, the Federal Open Market Committee raised the overnight federal funds rate to a range of 1.75%-2.0% at its June meeting. Minutes of the session indicated committee members are paying attention to risks surrounding trade and a flatter yield curve. Absent a shock that would change the Fed’s well-signaled intentions, we expect two more rate increases to follow in 2018 and three more hikes to approach the terminal rate in 2019.

- Long-term interest rates have remained low. This is due to high foreign investor demand for long-dated U.S. bonds, increasing their prices and driving down yields. We expect long-term yields to gradually increase along with short-term rates.

Information is not intended to be and should not be construed as an offer, solicitation or recommendation with respect to any transaction and should not be treated as legal advice, investment advice or tax advice. Under no circumstances should you rely upon this information as a substitute for obtaining specific legal or tax advice from your own professional legal or tax advisors. Information is subject to change based on market or other conditions and is not intended to influence your investment decisions.

© 2018 Northern Trust Corporation. Head Office: 50 South La Salle Street, Chicago, Illinois 60603 U.S.A. Incorporated with limited liability in the U.S. Products and services provided by subsidiaries of Northern Trust Corporation may vary in different markets and are offered in accordance with local regulation. For legal and regulatory information about individual market offices, visit northerntrust.com/disclosures.

© Northern Trust

Read more commentaries by Northern Trust