NewsLetter - June 2018

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsDEPRESSING IF TRUE

“Medicare to go broke three years earlier than expected, trustees say.

“Medicare’s hospital trust fund is expected to run out of money in 2026, three years earlier than previously projected, the program’s trustees said in a new report published this afternoon.

“The more pessimistic outlook is largely due to reduce revenues from payroll and Social Security taxes, and higher payments than expected to hospitals and private Medicare plans last year.

“The solvency report is the first since the repeal of Obamacare’s Independent Payment Advisory Board earlier this year as part of a massive spending agreement in Congress. The panel outside experts was designed to tame excessive Medicare spending growth, but costs never grew fast enough to trigger the controversial board, and no members were ever appointed. Social Security faces depletion in 2034, the program’s trustees also said today. That’s identical to last year’s projection.”

https://www.politico.com/story/2018/06/05/medicare-outlook-2026-625908

GOOD NEWS? BAD NEWS?

From my friend and long-term care guru, Bill Dyess.

I don’t know if it’s good news that someone needed LTC this long, but it was certainly good news that their insurance covered them. Here are the largest claims as of 12/31/2017 (and they’re still being paid!)

PITHY THOUGHT

For market timers….

Think about the few times when there was lots of certainty—2000 or 2009. How did that work out?

TEST RESULTS

From my last NewsLetter …

A TEST

John Durand wrote Timing: When to Buy and Sell in Today’s Markets, a classic in active investment management. He also wrote How to Secure Continuous Security Profits in Modern Markets, in which he opined: “As this is written, one of the greatest bull markets in history is in progress. People have been saying for several years that prices and brokers’ loans are too high; yet they go on increasing.… People who deplore the high at which gilt-edged common stocks are now selling apparently fail to grasp the fundamental distinction between investments yielding a fixed income and investments in the equities of growing companies. Nothing short of an industrial depression … can prevent common stock equities in well-managed and favorable circumstanced companies from increasing in value, and hence in market price.” When was his book published?

No winners, but here are ones that came mighty close:

Alan Rosoff ……………… 1928

Richard Lorenz…………. 1930

Jewell Davis ………….… 1925

The publication date was September 1929.

The Great Depression started October 29,1929.

TIDBITS FROM AARP

- Only about 37% of couples share financial decision-making equality. For shame!

- The average parent thinks allowances should begin at age 10.

- Approximately 29% of women in dual-income marriages make more money than their spouses; that’s up from 16% in 1981.

- The “average” family in the top 10% of wealth in the United States receives an inheritance of about $367,000, while families at the median level of wealth report an average of about $16,000.

- The average payout from the tooth fairy in 2017 was $4.13; in the West, it was $6.

- About 53% of grandparents contribute to their grandkids’ education, and 23% contribute to health and dental bills.

FOREWARNED IS FOREARMED

When markets take a dip, it’s not the end of the world (and if it is, who cares about markets?).

Even better, from our perspective, is that corrections are great buying opportunities.

GOOD NEWS, BAD NEWS

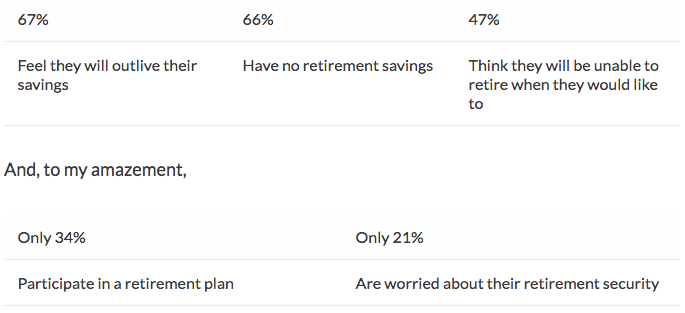

While the Federal Reserve’s “Report on the Economic Well-Being of U.S. Households in 2017” stated that “overall economic well-being has improved over the past five years,” that optimistic headline masks a lot of sad news.

“Economic Well-Being. A large majority of individuals report that financially they are doing okay or living comfortably, and overall economic well-being has improved over the past five years.

“Even so, notable differences remain across various subpopulations, including those of race, ethnicity, and educational attainment.”

Furthermore:

“Dealing with Unexpected Expenses. While self-reported financial preparedness has improved substantially over the past five years, a sizeable share of adults nonetheless say that they would struggle with a modest unexpected expense.

“• Four in 10 adults, if faced with an unexpected expense of $400, would either not be able to cover it or would cover it by selling something or borrowing money. This is an improvement from half of adults in 2013 being ill-prepared for such an expense.

“• Over one-fifth of adults are not able to pay all of their current month’s bills in full.

“• Over one-fourth of adults skipped necessary medical care in 2017 due to being unable to afford the cost.”

PHEW!

Good thing I went to college a zillion years ago. Here are the statistics for Cornell’s Class of 2022:

Applicants – 51,000+ (a record high)

Admit rate – 10.3% (an all-time low)

Admitted – 5,288

SAD BUT TRUE

Cyberattacks are a reality of life today, and we take the risk very seriously.

2.9% of advisors have faced successful attacks on their firm (not us).

44% of firms with more than one employee require mandatory cybersecurity training (we do).

81% of advisors believe addressing cybersecurity is high or very high on their priority list (we believe it’s very high).

IF YOU HAVEN’T SEEN THIS

New York Times

“Hoping to thwart a sophisticated malware system linked to Russia that has infected hundreds of thousands of internet routers, the F.B.I. has made an urgent request to anybody with one of the devices: Turn it off, and then turn it back on.

“The malware is capable of blocking web traffic, collecting information that passes through home and office routers, and disabling the devices entirely, the bureau announced on Friday.”

https://www.ic3.gov/media/2018/180525.aspx

TULIPS

As I wrote in my last NewsLetter:

Here’s what Crypto pioneer Mike Novogratz said on Monday on CNBC’s “Fast Money” (12/11/17).

“This is going to be the biggest bubble of our lifetimes.” Which, of course, does not stop him from investing hundreds of millions in the space. While conceding that cryptos are the biggest bubble ever … “Bitcoin could be at $40,000 at the end of 2018. It easily could.” Then, of course, it may not.

Turns out, so far, it’s “not.”

GOOD ADVICE

Also from AARP, an excellent article (as always) by Jean Chatzky: “Planning for the Worst.” Why disability insurance may be a must-have for you and this article is must-have reading for my younger readers.

https://www.aarp.org/work/working-at-50-plus/info-2018/disability-insurance-chatzky.html

DISMAL

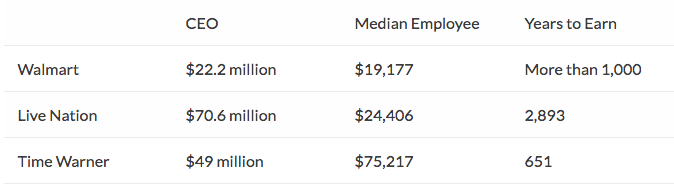

THE ANSWER IS “BECOME A CEO”

“Income inequality in the United States has increased significantly since the 1970s, after several decades of stability….”

Wikipedia

The New York Times ran an interesting, albeit depressing, story highlighting this issue:

“Want to Make Money Like a CEO? Work 275 years.

“This year, publicly traded corporations in the United States had to begin revealing their pay ratios—comparisons between the pay of their chief executive and the median compensation of other employees at the company. The results were predictably striking.”

Examples included:

WHY WE NEED A FIDUCIARY STANDARD

From the Wall Street Journal:

https://www.wsj.com/articles/wells-fargos-401-k-practices-probed-by-labor-department-1524757138

“Wells Fargo’s 401(k) Practices Probed by Labor Department

“Department is examining if bank pushed participants in low-cost 401(k) plans into more expensive IRAs

“The Labor Department is examining whether Wells Fargo & Co. has been pushing participants in low-cost corporate 401(k) plans to roll their holdings into more expensive individual retirement accounts at the bank, according to a person familiar with the inquiry.

“Labor Department investigators also are interested in whether Wells Fargo’s retirement-plan services unit pressed account holders to buy in-house funds, generating more revenue to the bank, the person said.”

It’s important to note that at this stage, it’s just a “probe,” but it’s no secret that these actions are common throughout the financial services world. If you’re responsible for a 401(k) plan, be sure your advisor is a 3(38), not a 3(21), fiduciary.

From the National Institute of Pension Administrators: “A 3(21) investment fiduciary is a paid professional who provides investment recommendations to the plan sponsor/trustee. The plan sponsor/trustee retains ultimate decision-making authority for the investments and may accept or reject the recommendations. Both share the fiduciary responsibility. By properly appointing a monitoring an authorized 3(38) investment manager, a plan sponsor/trustee is relieved of all fiduciary responsibility for the investment decisions made by the investment professional.”

WE HAVE A LONG WAY TO GO

“The Securities and Exchange Commission’s enforcement strategy to protect retail investors resulted in the return of a record $1.07 billion to harmed investors in 2017, SEC officials said Tuesday.”

Financial Advisor.

“JPMORGAN TO REMOVE SOME FIDUCIARY RULE HANDCUFFS, OTHERS MAY FOLLOW”

“JPMorgan Chase & Co. is telling its brokers and private bankers to prepare for changes to its retirement account policies and products in preparation for the likely repeal of the Department of Labor’s fiduciary rule next week.

“The message, sent in emails from bank executives to advisors at J.P. Morgan Securities, Chase Wealth Management and Chase Private Bank on Wednesday, signals that Wall Street firms are poised to move quickly to reverse restrictions that they imposed to comply with the conflict-of-interest rule that took partial effect last June.”

ONE MORE TIME

As I continue to beat the fiduciary drum continually, what can I say? It’s REALLY important. So, below is an excerpt from an interview with Phyllis Borzi in my friend Christopher Carosa’s FiduciaryNews.

FN: Now to the present. It looks like the Conflict-of-Interest Rule has not survived its court challenge and that the current administration seeks to, in essence, rewrite it. Still, the impact of the Rule remains. The term “fiduciary” – in part thanks to your efforts, in part thanks to John Oliver – has been elevated in the minds of the investing public. What aspects of the Conflict-of-Interest Rule are now “baked into the cake” of the retirement industry and would be hard to reverse, formal regulation or not?

Borzi: It’s probably too early to tell. But one of the lasting legacies of the DOL conflict-of-interest rules is in the greater public understanding of the need to seek an advisor who is willing to agree in writing to be a fiduciary. Unfortunately, most consumers are not yet at the point where they can tell for sure whether someone who assures them they are acting in their best interest (and thus using that term as a marketing slogan) is genuinely accepting legal liability as a fiduciary. That’s why consumers must get that acknowledgement of fiduciary status in writing and not simply accept the representations of individuals purporting to be acting in their interest.”

That’s why getting the Committee for the Fiduciary Standard’s oath (http://www.thefiduciarystandard.org/wp-content/uploads/2015/02/fiduciaryoath_individual.pdf) signed by your advisor is so important.

You can read the full transcript of the FiduciaryNews interview here:

ROBO PLANNING

The hot story in the planning world is Robo-Advisors: i.e., planning based on computer algorithms. I just heard a quote from an MIT AgeLab presentation that captures my thoughts:

“My life is not an algorithm; my life is a story.”

PRINCIPLES

Of course, when discussing fiduciary concepts, it’s important to consider principles, so I thought I’d share the story of “A Man of Principles” from my friend Phil.

“In 1952, Armon M. Sweat, Jr., a member of the Texas House of

Representatives, was asked about his position on whiskey. What follows

is his exact answer (taken from the Political Archives of Texas):

“‘If you mean whiskey, the devil’s brew, the poison scourge, the bloody

monster that defiles innocence, dethrones reason, destroys the home,

creates misery and poverty, yea, literally takes the bread from the

mouths of little children; if you mean that evil drink that topples

Christian men and women from the pinnacles of righteous and gracious

living into the bottomless pit of degradation, shame, despair,

helplessness, and hopelessness, then, my friend, I am opposed to it

with every fiber of my being.’

“‘However, if by whiskey you mean the lubricant of conversation, the

philosophic juice, the elixir of life, the liquid that is consumed

when good fellows get together, that puts a song in their hearts and

the warm glow of contentment in their eyes; if you mean Christmas

cheer, the stimulating sip that puts a little spring in the step of an

elderly gentleman on a frosty morning; if you mean that drink that

enables man to magnify his joy, and to forget life’s great tragedies

and heartbreaks and sorrow; if you mean that drink the sale of which

pours into Texas treasuries untold millions of dollars each year, that

provides tender care for our little crippled children, our blind, our

deaf, our dumb, our pitifully aged and infirm, to build the finest

highways, hospitals, universities, and community colleges in this

nation, then my friend, I am absolutely, unequivocally in favor of it.’

“‘This is my position, and as always, I refuse to compromise on matters

of principle.’”

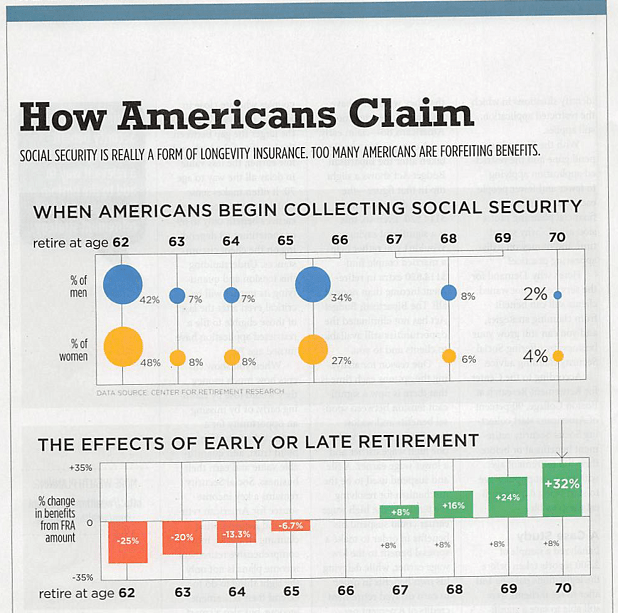

DELAY MAY BE GOOD

If you’ve not yet planned your retirement, the two major contributors to increasing the probability of financial success are delaying retirement and social security. If you have questions, check with us. That’s our forte.

Source: Wealthmanagement.com

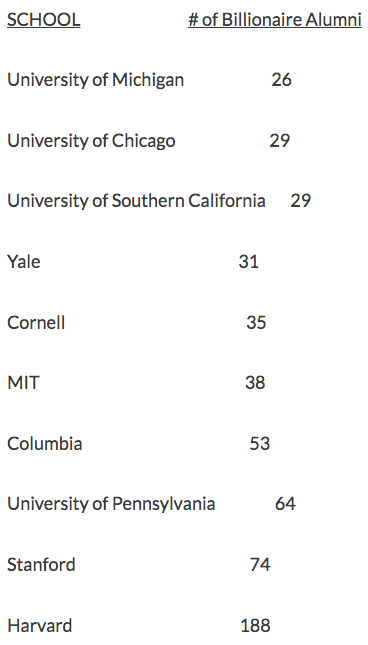

A GOOD START

“10 Universities with the most billionaire alumni”—a useless but interesting tidbit. Here’s the list:

OVERCONFIDENCE

“The overconfidence effect is a well-established biased in which a person’s subjective confidence in his or her judgments is reliably greater than the objective accuracy of those judgments, especially when confidence is relatively high.” ~Wikipedia

Overconfidence (e.g., Lake Woebegone, where all the children are above average) is a classic behavioral heuristic and one that often leads to poor investment decisions.

“There’s a Big U.S. Gender Gap in Retirement Investing Confidence Wealth Management

“Sixty percent of college-educated, not-yet-retired men say they’re comfortable managing their investments, compared to 35 percent of women.”

It’s that recognition of reality that makes women generally better investors then men.

OLD MEN

Given my current age, I kind of liked this:

One evening the old farmer decided to go down to the pond, as he hadn’t been there for a while.

He grabbed a twenty-liter bucket to bring back some fruit while he was there.

As he neared the pond, he heard voices shouting and laughing with glee. As he came closer, he saw it was a bunch of young women skinny-dipping in his pond. He made the women aware of his presence and they all went to the deep end. One of the women shouted to him, ‘We’re not coming out until you leave!’

The old man frowned, ‘I didn’t come down here to watch you ladies swim naked or make you get out of the pond naked.’

Holding the bucket up he said, ‘I’m here to feed the crocodile….’

Some old men can still think fast.

Hope you enjoyed this issue, and I look forward to “seeing you” again in a few months.

Harold Evensky

Chairman

Evensky & Katz / Foldes Financial Wealth Management

© Evensky & Katz / Foldes Financial Wealth Management

© Evensky & Katz / Foldes Financial Wealth Management

Read more commentaries by Evensky & Katz / Foldes Financial Wealth Management

Membership required

Membership is now required to use this feature. To learn more:

View Membership Benefits