Infrastructure, data centers and timber REITs are growing in importance

When most investors think about traditional real estate investment trust (REIT) investment opportunities, they often think about the “four major food groups” of real estate — the retail, office, residential and industrial sectors. While these sectors continue to be a major component of REIT investing, they are increasingly being joined by nontraditional REIT sectors. Our growing reliance on technology and changing demographics are leading to new opportunities in three nontraditional REIT sectors: infrastructure, data centers and timber.

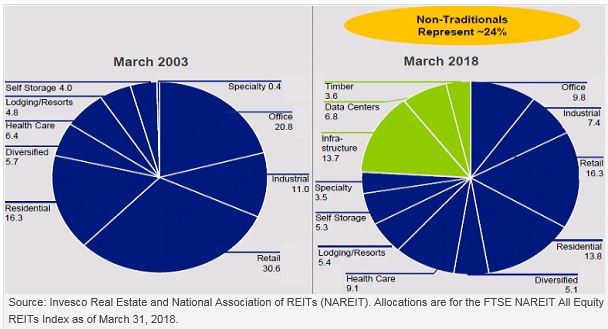

A changing picture of the REIT landscape

The retail, office, residential and industrial sectors have seen their cumulative weight in the FTSE NAREIT All Equity REIT Index fall from 79% in 2003 to 47% in 2018, as shown in the chart below. Over the same time period, timber, data centers and infrastructure grew from a 0% weight to 24%, as illustrated below. Concurrently, the remainder of REIT sectors that have seen their business models evolve — health care, lodging/resorts, specialty, diversified and self storage — have seen their cumulative index weight grow from 21% to 28%.

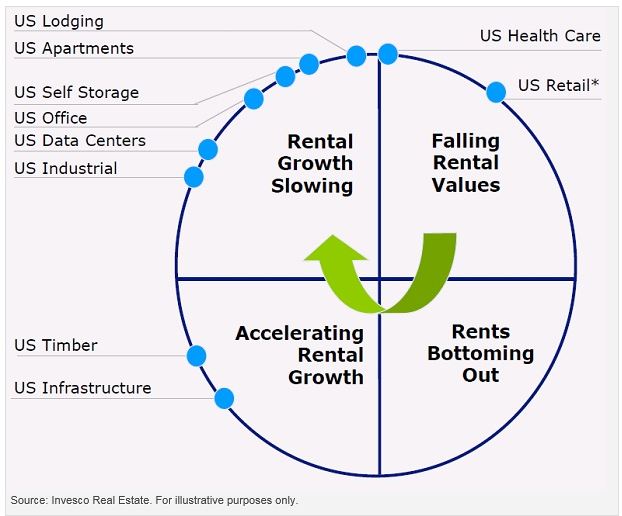

Finding growth amidst a moderating rental cycle

According to analysis by Invesco Real Estate, rental growth for most US REIT sectors has been positive but moderating to various degrees among many traditional constituents of the REIT universe as we move into the latter stages of the macroeconomic cycle. In certain sectors such as health care and retail, rental values have been falling in absolute terms.

- In the health care sector, too much supply is coming online in the near term, which has caused pressure on rents for senior housing and skilled nursing facilities. We believe that health care represents a very strong long-term opportunity given changes in US demographics. And we have conviction that market demand will eventually rebalance with a larger pool of supply.

- Concurrently, the traditional retail space is facing headwinds from the rise of online shopping. We believe that high-quality, class “A” malls and shopping centers that adopt a shop/work/live/play structure will be sustainable in the long-run, but that the lower-productivity “B” and “C” malls and shopping facilities will continue to come under stress.

The growing influence of nontraditional REITs

While the traditional retail space has been hampered by the rise in e-commerce, infrastructure and data centers have been strong beneficiaries of the shift to online retail and smartphone penetration, and they currently offer the highest rates of rental growth in the REIT space. In the timber sector, we have been seeing rental and cash flow acceleration thanks to a strong economy and an improvement in housing starts.

Infrastructure REIT sector: Receiving tailwinds from increased data usage, smartphone penetration and rising e-commerce

The infrastructure REIT sector is dominated by three large cell tower players – American Tower, Crown Castle and SBA Communications

This oligopoly of US cell towers has one of the most attractive business models in the REIT space, in our view. Each of these companies owns portfolios of between 50,000 and 150,000 cell tower sites worldwide,1 and the growing wave of data usage from smartphones and tablets has created an increased need for these towers and the networking equipment they carry.

Furthermore, we believe that the cell tower business structure is becoming increasingly attractive thanks to colocation opportunities where more than one wireless carrier pays rent on a single tower. This provides the scope for higher tenant revenue and improved gross margins.

The contractual structure between the cell tower operators and wireless carriers is also highly attractive in our opinion — leases are typically five to 10 years in length with renewal options, are generally non-cancellable, and have inflation-linked rent increases or fixed price bumps that boost rental growth each year.

Bottom line: Cell tower companies have produced stable and predictable cash flows along with accelerating rental growth rates well above other traditional REIT sectors.2

Data center REIT sector: Providing vital services to the world’s largest technology companies

The US data center REIT sector is dominated by five main players — Equinix, Digital Realty Trust, CyrusOne, CoreSite Realty and QTS Realty Trust

Data centers provide critical support for e-commerce and the online economy by warehousing networking equipment, communications hardware and data storage. Companies that use these highly sophisticated facilities include technology giants such as Google, Facebook and Amazon as well as more traditional companies in the communications and financial services industries.

Data centers have a unique leasing structure unlike any other in the REIT space. Given the huge amount of power required by data centers, rents are based on the electricity demands of tenants as opposed to traditional square footage charges. The data center leasing structure is typically five to 10 years in length with renewal options, and contracts also contain annual rent increases tied to inflation or fixed price bumps.

Bottom line: Like cell towers, the leasing model of data centers has historically provided stable and predictable cash flows along with higher rates of rental growth than traditional REIT sectors.3

Timber sector: Building new homes for millennials

The US REIT timber sector also has a high concentration among three key competitors — Weyerhaeuser, Rayonier and PotlatchDeltic

Timber REITs are currently experiencing strong rates of cash flow acceleration thanks to a strong US economy, improving housing starts and the surging price for timber. Each of the above companies has between 2 million and 12 million acres of working forests across many states, and they can provide wood for use in a variety of markets including lumber, pulp, paper and other wood-based products.4

Bottom line: On the lumber and panel front, we expect housing starts to continue to rise in the next several years as more millennials form new households. This should continue to be supportive of timber REITs.

1 Sources: American Tower, Crown Castle and SBA Communications

2 Sources: Bloomberg, L.P.; S&P Global; Invesco Real Estate. The earnings growth rate for cell towers was 10.40% in 2016 and 11.21% in 2017. That compares to the earnings growth rate for apartments (2.27% and 5.58%), industrial (9.65% and 6.21%), lodging (11.11% and -1.81%), office (12.22% and 1.30%), regional malls (12.16% and 6.40%) and shopping centers (5.24% and 2.72%).

3 Sources: Bloomberg, L.P.; S&P Global; Invesco Real Estate. The earnings growth rate for data centers was 12.45% in 2016 and 14.50% in 2017. That was higher than the earnings growth rate for apartments (2.27% and 5.58%), industrial (9.65% and 6.21%), lodging (11.11% and -1.81%), office (12.22% and 1.30%), regional malls (12.16% and 6.40%) and shopping centers (5.24% and 2.72%).

4 Sources: Weyerhaeuser, Rayonier and PotlatchDeltic

David Wertheim

Senior Client Portfolio Manager

David Wertheim is a Senior Client Portfolio Manager focused on real asset securities. In this capacity, he works with Invesco’s real assets investment management team, serving as its representative to clients and prospects.

Mr. Wertheim began his career in 2000 and joined Invesco in 2018. Prior to joining Invesco, he was a senior client portfolio manager for real assets, commodities and equities with Deutsche Asset Management.

Mr. Wertheim earned a BBA from George Washington University with a dual concentration in international business and marketing.

Important information

Blog header image: SERHAT AKAVCI/Shutterstock.com

The FTSE NAREIT All Equity REIT Index is an unmanaged index considered representative of US REITs.

Investment in infrastructure-related companies may be subject to high interest costs in connection with capital construction programs, costs associated with environmental and other regulations, the effects of economic slowdown and surplus capacity, the effects of energy conservation policies, governmental regulation and other factors.

Investments in real estate related instruments may be affected by economic, legal, or environmental factors that affect property values, rents or occupancies of real estate. Real estate companies, including REITs or similar structures, tend to be small and mid-cap companies and their shares may be more volatile and less liquid.

This does not constitute a recommendation of any investment strategy or product for a particular investor. Investors should consult a financial advisor/financial consultant before making any investment decisions. Invesco does not provide tax advice. The tax information contained herein is general and is not exhaustive by nature. Federal and state tax laws are complex and constantly changing. Investors should always consult their own legal or tax professional for information concerning their individual situation. The opinions expressed are those of the authors, are based on current market conditions and are subject to change without notice. These opinions may differ from those of other Invesco investment professionals.

All data provided by Invesco unless otherwise noted.

Invesco Distributors, Inc. is the US distributor for Invesco Ltd.’s retail products and collective trust funds. Invesco Advisers, Inc. and other affiliated investment advisers mentioned provide investment advisory services and do not sell securities. Invesco Unit Investment Trusts are distributed by the sponsor, Invesco Capital Markets, Inc., and broker-dealers including Invesco Distributors, Inc. Each entity is an indirect, wholly owned subsidiary of Invesco Ltd. PowerShares® is a registered trademark of Invesco PowerShares Capital Management LLC, investment adviser. Invesco PowerShares Capital Management LLC (PowerShares) and Invesco Distributors, Inc., ETF distributor, are indirect, wholly owned subsidiaries of Invesco Ltd.

©2017 Invesco Ltd. All rights reserved.

A new generation of nontraditional REIT opportunities by Invesco