Russia Is Defying Expectations

Membership required

Membership is now required to use this feature. To learn more:

View Membership Benefits

We’re a little more than a week into the 2018 FIFA World Cup, and so far Russia has surprised experts and fans alike. Expectations were low at best. Because of recent setbacks, including a disastrous performance at the 2016 UEFA European Championship and injuries sustained by key players, the federation ranked a dismal 66th place among Fédération Internationale de Football Association teams—its lowest position ever. The only reason it didn’t have to qualify to compete was because Russia is the host nation. (This is the first time in its 88-year history, by the way, that the World Cup has been held in Eastern Europe.)

And yet Russia currently ranks first in its group after defeating Saudi Arabia (5-0) and Egypt (3-1), defying predictions that the federation would be eliminated right out of the gate. Left winger Denis Cheryshev has so far scored three goals, more than any other player in the 32-team tournament except Portugal’s Cristiano Ronaldo.

It’s still early, and the team has an uphill battle ahead of it. We’ll see how Russia fares when it goes up against group favorite Uruguay on Monday. As for which team might win the Cup, sophisticated predictive models using portfolio theory and the historical performance of players are pointing to France beating Spain in the final.

Russian Airports Could Be Biggest Beneficiaries of Hosting World Cup

This is the second time in the past five years that Russia has hosted a major international sports tournament, and questions have surfaced about what economic benefits, if any, doing so affords.

As I shared with you back in February, the Eastern European country spent as much as $50 billion, a record-breaking sum, to host the 2014 Winter Olympics in Sochi. It seems insurmountable, but Fitch Ratings concluded that the debt was “manageable,” citing the reduction of interest rates to 0.5 percent and noting that the cost is less than 2.5 percent of Russia’s gross domestic product (GDP).

Hosting the World Cup has set Russia back an estimated $14 billion—again, a record amount for the competition. But unlike the Olympics, the Cup could produce some modest net economic benefits—in the short-term, at least—according to experts.

Back in April, tournament organizers predicted that, as a result of increased tourism and large-scale spending on infrastructure, the competition would add nearly $31 billion to Russia’s economy in the 10 years between 2013 and 2023. (FIFA selected Russia as the host nation in 2010.)

"Moscou" by OliBac Licensed under a Creative Commons Attribution 2.0 Generic (CC-BY2.0). https://flic.kr/p/ovkQad

Analysts with Moody’s Investors Service were slightly less upbeat, writing that they see “very limited economic impact at the national level.” Among the beneficiaries are food retailers, hotels, telecommunications firms and transportation, as “better public infrastructure will likely generate additional tax revenue and reduce capital spending needs for the hosting regions in the coming years.” But the greatest long-term beneficiary, Moody’s says, are Moscow-based international airports, since “upgraded facilities will support higher passenger flow, even after the event.”

Watch this brief video on opportunities in the global airline and airport industries by clicking here!

Russia’s Recovery Gathering Pace

Besides its soccer prowess, Russia is defying expectations in other ways—and equity investors should be taking notice.

Having emerged last year from a two-year recession that was triggered by the collapse in oil prices and imposition of sanctions following its annexation of Crimea, the country is now in full-on recovery mode. In a note to investors this week, Capital Economics senior emerging markets economist William Jackson says that GDP growth in May picked up to more than 2 percent year-over-year, up from 1.3 percent in the first quarter. Most of the changes, according to Jackson, came in manufacturing, which he estimates to be growing by more than 5 percent year-over-year, compared with only 1 percent previously.

“This all supports the point we’ve been making for some time,” he writes, “that Russia’s recovery was likely to resume and gather pace this year.”

Once almost entirely reliant on oil exports, the government of the world’s leading oil producer has lowered the structure of exports from 70 percent energy in 2013 to 59 percent last year, according to the World Bank. Today, the budget is back in surplus, and government debt stands at a remarkable 33 percent of GDP, the lowest among G20 nations.

Key inflation is currently running at a record low of 2.4 percent year-over-year, well below the Central Bank of Russia’s (CBR) target of 4 percent. Food inflation, in particular, is near zero percent.

Unemployment continues to decline. In May it fell to 4.7 percent, a record low since the collapse of the Soviet Union in 1991.

Because of low inflation and a near-full employment jobs market, real wages are expanding healthily across all sectors. This is helping to drive stronger private consumption and investment. In May, retail sales grew 2.4 percent compared to the same month last year.

Government Policy Supportive of Future Growth

The Russian government is currently enacting or considering policy that should help sustain the economy’s recovery. For one, it recently moved to raise the retirement age to reduce the cost to the state budget on an aging population, the Financial Times reports. (The median age in Russia is nearly 40, compared to around 30 for the entire world.) The pension age for men will increase from 60 years to 65 years in 2028, while for women it will increase from 55 years to 63 years in 2034.

The reform could help the government save an estimated $27.3 billion a year, according to a Russian think tank.

The government is also reportedly working on a plan to invest more in infrastructure and reduce “unnecessary regulation that is holding back private investment.” That’s according to Morgan Stanley’s Clemens Grafe, who adds that plans for “national projects” will be drawn up by October “that should help Russia to become one of the five largest economies in the world.”

Time to Consider Investing in Moscow?

Some might consider that fanciful thinking, but it doesn’t take away from the fact that Russia is an attractive place to invest right now, especially compared to the U.S. market.

Besides an economy in recovery, consider the following: Whereas the S&P 500 Index is up a little more than 13 percent for the 12-month period, the MOEX Russia Index has seen gains closer to 22 percent. That comes with an appealing 6.46 percent dividend yield, compared to 1.94 percent for U.S. stocks.

The price is right too. Russia trades at an inexpensive 6.39 times earnings, the U.S. at 21.08 times earnings, according to Bloomberg data.

Interested in learning more about emerging Europe? Watch this brief video featuring U.S. Global research analyst Joanna Sawicka as she describes her favorite three countries in this fast-growing region.

Index Summary

- The major market indices finished mixed this week. The Dow Jones Industrial Average lost 2.03 percent. The S&P 500 Stock Index fell 0.89 percent, while the Nasdaq Composite fell 0.69 percent. The Russell 2000 small capitalization index gained 0.10 percent this week.

- The Hang Seng Composite lost 3.34 percent this week; while Taiwan was down 1.07 percent and the KOSPI fell 1.95 percent.

- The 10-year Treasury bond yield fell two basis points to 2.90 percent.

Domestic Equity Market

Strengths

- Utilities was the best performing sector of the week, increasing by 2.5 percent versus an overall decrease of 0.70 percent for the S&P 500.

- Darden Restaurant was the best performing stock for the week, increasing 15.7 percent.

- Harsher Fed stress tests this year are not preventing U.S. banks from increasing their payouts to shareholders. As the annual review gets under way this week, the 25 largest lenders are gearing up to announce dividends and buybacks totaling roughly $30 billion more than last year, representing a 25 percent increase, according to analysts’ estimates compiled by Bloomberg.

Weaknesses

- Industrials was the worst performing sector for the week, decreasing by 3.39 percent versus an overall decrease of 0.70 percent for the S&P 500.

- Red Hat was the worst performing stock for the week, falling 18.63 percent.

- General Electric, an original member of the Dow Jones industrial average, has lost its spot after 111 consecutive years. It will be replaced by Walgreens as of next Tuesday, reports Reuters.

Opportunities

- After the release of a trio of bullish notes from Wall Street analysts, shares of Netflix jumped above the $400 plateau for the first time on Tuesday.

- The National Association of Manufacturers quarterly outlook published Tuesday showed 95.1 percent of manufacturers surveyed said they had a positive outlook for their companies, the highest in 20 years.

- Security software company Symantec revealed Tuesday that a hacking campaign based in China had burrowed into satellite operators, defense contractors and telecom companies in the US and southeast Asia. The company said the hackers were driven by national espionage goals, which include intercepting military and civilian communications. While very concerning, increased fears about hacking are driving demand for cybersecurity companies.

Threats

- The Dow Jones industrial average fell 1.15 percent on Tuesday, dropping into negative territory for the year.

- Starbucks forecasts weaker sales and says it's closing 150 US stores. Shares slumped as much as 5 percent in after-hours trading Tuesday after the coffee chain said same-store sales for the third quarter would rise 1 percent, missing the 2.9 percent growth that analysts were expecting.

- Oracle beat on both the top and bottom lines, but shares fell more than 3 percent in after-hours trading Tuesday after its first quarter earnings forecast of $0.67 to $0.69 a share missed Wall Street estimates of $0.72.

The Economy and Bond Market

Strengths

- U.S. housing starts rebounded last month to the highest level since 2007, driven by a construction bounce in parts of the country that have lagged for much of the economic recovery as well as a lasting apartment boom. Housing starts rose 5 percent in May from the prior month to a seasonally adjusted annual rate of 1.35 million, the Commerce Department said Tuesday. Compared with a year earlier, starts were up 20.3 percent.

- Steady growth in Japanese exports for a second-straight month offers more reassurance that Japan’s economy is rebounding in the current quarter, despite rising trade tensions. The value of exports rose 8.1 percent year-over-year in May, above the 7.5 percent consensus forecast, according to data from the finance ministry.

- All banks passed Fed’s stress test, which showed the firms’ aggregate common equity tier 1 capital ratio would fall from 12.3 percent in the fourth quarter of 2017 to 7.9 percent in the hypothetical stress scenario. This was an improvement compared to the 4.5 percent requirement, but lagged the 9.2 percent ratio from last year given the harsher scenarios modeled.

Weaknesses

- The National Association of Realtors said on Wednesday that existing home sales slipped 0.4 percent to a seasonally adjusted annual rate of 5.43 million units last month. It was the second straight monthly decline in sales. Economists polled by Reuters had forecast existing home sales rising 1.5 percent to a rate of 5.52 million units in May. Existing home sales, which make up about 90 percent of U.S. home sales, dropped 3.0 percent year-over-year in May. They have declined on a year-over-year basis for three straight months.

- The Philadelphia Fed Manufacturing Index dropped sharply to 19.9 in June, down from 34.4 and missed expectation of 29. Six-month expectation dropped to 34.8, down from 38.7. The Federal Reserve Bank of Philadelphia stated that “responses to the June Manufacturing Business Outlook Survey indicate continued expansion for the region’s manufacturing sector, although indicators for general activity and new orders fell notably from last month.”

- The Conference Board released a report on Thursday showing a smaller than expected increase by its index of leading U.S. economic indicators in the month of May. The Conference Board said its leading economic index inched up by 0.2 percent in May after climbing by 0.4 percent in April. Economists had expected the index to rise by 0.4 percent. "The U.S. [Learning Economic Index] still points to solid growth but the current trend, which is moderating, indicates that economic activity is not likely to accelerate," said Ataman Ozyildirim, Director of Business Cycles and Growth Research at the Conference Board.

Opportunities

- Personal consumption has been improving since February. A continuation in next week’s release would cement confidence in this trend.

- Consumer sentiment has held up pretty well this year despite geopolitical tensions between the U.S. and China, Italy’s political crisis and overall higher volatility in markets. As such, next week’s Conference Board Consumer Confidence Index is likely to match forecasts.

- The Chicago Purchasing Manager Index saw a bottoming from its December highs in March and has swiftly picked up momentum since. That momentum is likely to continue in next week’s report.

Threats

- Longer-term Treasuries look good to investors shaken by the prospect of a nasty trade dispute between the world’s two biggest economies. They’re shunning shorter term debt, already undercut by the Federal Reserve’s resolve to raise interest rates a total of four times this year. The yield premium for buying 10-year notes over two-year has fallen to its lowest since before the financial crisis and sparked speculation the curve may invert soon.

- Given weak consumer spending in the first quarter, the odds for next week’s first quarter release of the gross domestic product (GDP) annualized quarter-on-quarter favor missing the forecast for growth of 2.2 percent.

- Monthly durable goods orders have been on the decline since February, posing a threat to next week’s release.

Gold Market

This week spot gold closed at $1,269.42 down $10.13 per ounce, or 0.79 percent. Gold stocks, as measured by the NYSE Arca Gold Miners Index, ended the week lower by 0.27 percent. Junior-tiered stocks outperformed seniors for the week, as the S&P/TSX Venture Index gained 0.24 percent. The U.S. Trade-Weighted Dollar reversed course this week and slipped back 0.28 percent.

| Date | Event | Survey | Actual | Prior |

|---|---|---|---|---|

| Jun-19 | Housing Starts | 1311k | 1350k | 1286k |

| Jun-21 | Initial Jobless Claims | 220k | 218k | 221k |

| Jun-25 | New Home Sales | 669k | -- | 662k |

| Jun-26 | Hong Kong Exports YoY | 9.5% | -- | 8.1% |

| Jun-26 | Conf. Board Consumer Confidence | 128.0 | -- | 128.0 |

| Jun-27 | Durable Goods Orders | -0.8% | -- | -1.6% |

| Jun-28 | Germany CPI YoY | 2.1% | -- | 2.2% |

| Jun-28 | GDP Annualized QoQ | 2.2% | -- | 2.2% |

| Jun-28 | Initial Jobless Claims | 220k | --- | 218k |

| Jun-29 | Eurozone CPI Core YoY | 1.0% | -- | 1.1% |

Strengths

- The best performing metal this week was silver, down 0.68 percent. According to the National Association of Realtors, sales of previously owned U.S. homes fell in May for a second month due to a lack of inventory and higher asking prices. Data shows that the median sale price increase 4.9 percent year-over-year to a record of $264,800.

- Russia sold $47.4 billion of U.S. Treasuries in April, which is more than any other major foreign holder. Bloomberg reports that the country’s gold reserves are now at the highest of President Vladimir Putin’s 18 years in power. Russia’s central bank holdings increased by 1 percent in May and now stand at 62 million troy ounces valued at $80.5 billion. Why might Russia be increasing its gold holdings? U.S. Treasuries are typically viewed as a safe haven asset, however, since Russia is feuding with the U.S. due to sanctions, the nation is moving toward gold – another perceived safe haven asset. Another nation flocking toward gold is Kyrgyzstan. In an effort to protect itself from currency volatility in China and Russia due to economic standoffs with the U.S., the central Asian nation is working to grow its share of gold in its $2 billion international reserves from 16 percent all the way to 50 percent, writes Bloomberg.

- The VanEck Vectors Gold Miners ETF saw its biggest weekly inflow in more than four months this week of over $200 million. Wednesday, June 20, was the biggest one-day increase since March 26 and the fourth straight day of inflows for the ETF. However, gold bullion-based ETFs cut 180,578 troy ounces of gold from their holdings to mark the fifth straight day of declines on Friday. Bloomberg writes that precious metals funds had $119 million of losses this week, compared with $408 million of outflows from the previous week. This shows that money is rotating into gold stock ETFs since they are outperforming bullion itself.

Weaknesses

- The worst performing metal this week was palladium, down 3.30 percent. Gold futures fell to an almost six-month low as the growing trade spat between the U.S. and China pushed the dollar up to an 11-month high. Hedge fund managers betting on gold this week after last Friday’s sell off were again unrewarded as bullion gave up almost $10 this past week.

- The new steel and aluminum tariffs are bringing in big bucks to the U.S. So far the Trump administration has collected $775 million from the metal import tariffs and the Commerce Department expects to reach $1 billion in six weeks. President Trump said on Wednesday that “one thing no one talks about is the money pouring into the Treasury. These tariffs are billions and billions of dollars.” Tariffs are taxes that ultimately raise the price of goods to the consumers bearing the inflation hit.

- Evy Hambro, manager of Blackrock Inc.’s World Mining Fund, said this week that investors “have lost a bit of patience with regard to their exposure to gold because they’ve been frustrated that it hasn’t been delivering returns. Although gold is historically seen as a safe haven asset during times of geopolitical turbulence, it has not been performing that role recently. Darwei Kung, portfolio manager of the Deutsche Enhanced Commodity Strategy Fund, says that gold’s appeal is dulled due to President Trump’s fickleness and that investors are flocking toward the dollar and U.S. Treasuries rather than gold due to high transaction costs for bullion.

Opportunities

- Nearly a dozen of the major banks have been named in lawsuits alleging manipulation in the metals markets with three class action suits on gold, silver and platinum and palladium. HSBC and UBS are named in all three lawsuits plus Barclays and Scotiabank are involved in both the silver and gold suits. This is positive in the sense that the manipulation is being recognized finally instead of saying that it doesn’t exist by the regulators. Bloomberg writes that plaintiffs are seeking tripled damages for artificial pricing on trillions of dollars in trades.

- Orion Resource Partners formed a deal to increase its holding to 80 percent in Dalradian Resources Inc., which is developing a gold mine in Northern Ireland. Orion is offering $1.10 per share, a 62 percent premium, valuing Dalradian at around $400 million. The Dalradian deal is actually more of a take-under transaction in that only about of the 1/3 to just 1/2 of its value would be realized if shareholders vote to approve the transaction. The reason this lowball bid might succeed is that the fast money that is active in the gold mining space is just trading the gold stock ETFs for their beta to gold, while alpha trades on specific companies are being ignored. Billionaire hedge fund manager John Paulson believes that Detour Gold Corp. should put itself up for sale due to stock losses and managerial missteps. Detour still needs to release its new mining plan in a couple of weeks before any bidding emerges in what could be the next take-under. Arizona Mining received an all cash bid totaling $1.3 billion for its Taylor lead-zinc-silver carbonate replacement deposit. This was very positive for Barksdale Capital which was up 46 percent for the week on the Arizona Mining news as Barksdale controls the adjacent land position where the Taylor deposit runs onto their ground. The valuation gap between the two companies is $20 million market cap for Barksdale’s Sunnyside deposit versus $1.449 billion for Arizona Mining. Asarco drilled the Sunnyside in 1980 and hit the same ore beds as Arizona Mining has its property. In addition, Asarco did intercept the porphyry copper deposit at depth, the source for the mineralizing fluids, but the copper grade of 0.44 percent was not economic in the 1980s, although deposits of that grade are being mined today.

- Jim Rickards says that now is the perfect environment for gold since the Fed is tightening into weakness and will eventually over-tighten and cause a recession. In a recession the Fed typically cuts interest rates 300 basis points to lift the economy, however if a recession arrives in the near future, the Fed won’t be able to cut rates 3 percent if they’re only between 1.75 and 2 percent now. David Rosenberg, chief economist and strategist at Gluskin Sheff & Associated, told conference attendees this week that “Cycles die, and you know how they die? Because the Fed puts a bullet in its forehead.” No surprise Rosenberg thinks the S&P 500 has peaked and sees a recession in 12 months. Jefferies is bullish on mining and commodities, citing in a new report that it’s due to a lack of supply growth. Below we updated the trailing 5-year measure of inflation using the two New York Fed’s Underlying Inflation Gauges. One is only price data and it is compounding at 1.56 per over the measurement period while the full data set measure, which contains non-price data like inventory changes for example, had been compounding at 12.75 percent over the same period with much of the rise occurring in the last couple of years. The NY Fed noted in its seminal research paper printed in 2017 that the full data set may be a better predictor of future inflation.

Threats

- Bloomberg writes that the first step in the inversion of the U.S. Treasury curve may occur as soon as next week as the spread between seven- and 10-year yields held below 4 basis points on Tuesday. A negative slope of the yield curve has historically been a precursor of recessions. Former U.S. Treasury Secretary Lawrence Summers warned this week that developed countries are poorly prepared for another recessions and that central banks should be wary of rising interest rates to stop inflation from running too high.

- Housing affordability has dropped to the lowest since 2008 this quarter, according to data from the National Association of Realtors. Average wage earners would need to spend 31.2 percent of income to buy a median-priced home this quarter, which is above the historic average of 29.6 percent of income. Ben Steverman of Bloomberg writes that millennials are far behind the savings levels of the previous generation when at the same age due to student debt and stagnant wages. Steverman says that millennials can only contribute the bare minimum to retirement plans and struggle to find affordable homes within commuting distance of their jobs.

- According to head of global exchange-traded funds at Franklin Templeton, Patrick O’Connor, fixed income indexes are broken. He says they are broken due to weighting of individual securities based on debt issued so that companies that issue more debt will have a higher weight in an index-based ETF. These same arguments apply to the gold stock ETFs that only base their index inclusion criteria on market capitalization and liquidity, with no view toward the financial quality of the companies or management’s skill that are being bought for the funds.

Blockchain and Digital Currencies

Strengths

- Of the cryptocurrencies tracked by CoinMarketCap, the best performing for the week ended June 22 was Dascoin, which gained 112.19 percent.

- Shares of Square Inc. were up on Monday and on track to close at a new high after the company said it received the proper license to allow bitcoin trading on its Cash app in New York, reports MarketWatch. Previously, app users in NY couldn’t buy and sell bitcoin, but the company was granted a virtual currency license by New York State on Monday.

- So far in 2018, no fewer than seven ETFs related to blockchain technology have debuted, reports MarketWatch. Blockchain ETFs are considered “thematic funds,” the article continues, meaning they are dedicated to a niche sub-sector of the equity market. “For smaller sponsors, a thematic fund is something that can be easily explained to people, whether you agree with the investment thesis or not, and it provides an entry point into a segment of the market where the larger players don’t have a commanding hold,” said Noel Archard, global head of SPDR product at State Street Global Advisors.

Weaknesses

- Of the cryptocurrencies tracked by CoinMarketCap, the worst performing for the week ended June 22 was Hexx, which lost 51.92 percent.

- According to a report published by the Bank for International Settlements (BIS) this week, cryptocurrencies have a range of shortcomings including instability, large electricity consumption, and are subject to too much manipulation and fraud, reports Bloomberg. The report also analyzed what it would take for the blockchain software underpinning bitcoin to process the digital retail transactions currently handled by national payment systems. “As the size of the ledgers swell, the researchers found, it would eventually overwhelm everything from individual smartphones to servers,” the article continues.

- Cryptocurrencies fell overnight Tuesday after another South Korean exchange, called Bithumb, was hacked, following last week’s heist at Coinrail, reports Seeking Alpha. Popular coins such as Ripple were stolen, with hackers looting around 35B won, or $32 million. “While the stolen coins will be covered by Bithumb’s reserves, the announcement renews concerns about the safety of crypto trading venues,” the article continues.

Opportunities

- On Tuesday, the cryptocurrency market added $12 billion, reports CCN, as major currencies such as bitcoin, Ethereum, Ripple and Bitcoin Cash experienced a short-term corrective rally. “While it is too early to conclude that BTC has entered into a mid-term rally give that it is still likely for BTC to fall below the $6,000 mark in the short-term, the cryptocurrency market has gained a breathing room from the recent major correction that began in early May,” the article continues.

- Brazil’s central bank announced on Tuesday that it has built a platform that will allow secure data sharing between itself and other domestic financial regulators, reports Coindesk. The bank, in its release, credits blockchain technology for its ability to provide a horizontal network of information, as well as immutable data storage, the article continues.

- U.S. House members were advised this week that they must publicly reveal any digital token holdings worth more than $1,000, as stated in a memo issued June 18 by the House Ethics Committee. “The ethics guidance means the public will soon learn whether members of Congress are among those who’ve been drawn to what’s become a global investment craze,” Bloomberg reports. “Bitcoin, the most valuable cryptocurrency, was initially embraced by those who were distrustful of banks and government control over monetary policy.”

Threats

- From late 2017 to early 2018, many small- and mid-cap companies tried to use the hype surrounding cryptocurrencies to boost their stock value – either by adding “bitcoin” to their name or associating themselves to the space somehow, reports Bloomberg. However, as a study of 45 companies who did just that shows, the stock pop from such a rebrand doesn’t last. “The market is going to figure out whether or not it has the appropriate growth profile,” says Steven DeSanctis, a strategist at Jefferies LLC.

- Until it figures out how to deal with a surge in demand from the energy-hungry cryptocurrency mining industry, Quebec will make electricity prohibitively expensive for crypto miners, reports Bloomberg. “Provincial regulator Regie de l’energie authorized utility Hydro-Quebec to charge 15 cents per kilowatt hour to blockchain companies, about three times the price they have enjoyed up to now,” the article continues.

- With cryptocurrencies having a volatile year, hedge funds investing in this asset class are also feeling some of the pain, reports Bloomberg. One example is Pantera Capital’s Digital Asset Fund, which includes a number of virtual currencies. The fund dropped 26 percent in May, according to CEO Dan Morehead. That compares with Bitcoin’s fall of around 15 percent.

Energy and Natural Resources Market

Strengths

- Crude oil was the best performing major commodity this week rising 6.38 percent. The commodity rallied after the Organization of the Petroleum Exporting Countries (OPEC) and its allies reached an unlikely agreement to keep the crude oil output curbs in place with the addition of a much lesser than expected increase of around 700,000 barrel per day.

- The best performing sector this week was the S&P 1500 Oil & Gas Producers and Explorers Index. The index rose 4.98 percent after energy investors felt vindicated with OPEC’s decision, calling it a “best case” outcome.

- The best performing stock for the week was TPI Composites Inc. The Arizona-based manufacturer of wind energy equipment rose 10.89 percent after market analysts upgraded their views on the stock after new contracts give greater visibility for the company to achieve its revenue guidance.

Weaknesses

- Coal was the worst performing commodity this week. The commodity dropped 4.65 percent after Bloomberg New Energy Finance's research team published a report arguing coal consumption will fall more than forecast, giving way to cheaper wind and solar generation.

- The worst performing sector this week was the Bloomberg Americas Auto Parts & Equipment Index. The index dropped 3.36 percent after President Donald Trump’s latest tweet threatening a 20 percent tariff on European cars coming into the U.S. intensified fears of a trade war.

- The worst performing stock for the week was OJI Holdings Corp. The Japanese producer of paper and packaging goods dropped 8.7 percent after local media reported on rumors that four major Japanese packaging companies are looking to cooperate or combine parts of their businesses. All equities in the sector fell on this news.

Opportunities

- Investors are piling into gold ETFs. More than $200 million has come into VanEck Vectors Gold Miners ETF so far this week, which would be the biggest weekly inflow in more than four months. Cash margins of large producers are expected to remain positive next year, said analyst Eily Ong in a note last month. The aggregate free cash flow of producers tracked by Bloomberg Intelligence is forecast to reach a record $8.6 billion next year, Ong said.

- Crude prices reacted positively to the announcement that OPEC and allies including Russia will boost oil production starting next month. OPEC agreed on a “nominal” production increase of 1 million barrels a day. In reality, several ministers said the accord will add a smaller amount of oil to the market - about 700,000 barrels a day - because a number of countries are unable to raise their output. The output increase is smaller than initially expected, resulting in positive momentum moves for oil and energy markets.

- It may be a busy summer with mining mergers and acquisitions action back in the cards. Three mining deals were consummated this week, led by South32 Ltd.’s cash offer for Canada’s Arizona Mining Inc. for approximately $1.4 billion. Another two fairly well known junior miners in Canada received a take out offer and a sizeable silver streaming agreement.

Threats

- The Chinese yuan extended its losses for a seventh straight session on Friday after the People’s Bank of China (PBOC) failed to stabilize the currency hit by the simmering US-China trade dispute. A fraction of China market commentators suggested the PBOC would like to let the yuan weaken further to boost exports amid the trade war. The weakness in the yuan has negative implications for commodity demand imports to China.

- Investors pull a record amount of money from emerging market funds according to the Financial Times. According to the publication, rising trade tensions and a strengthening dollar sent a shockwave through Asian markets, leading to a weekly record $8.1 billion outflow. Money flows leaving emerging markets have negative implications for emerging market currencies, making commodity imports more expensive.

- The biggest U.S. shale region will have to shut wells within four months because there aren’t enough pipelines to get oil to customers, according to Pioneer Natural Resources Co. The worsening bottleneck in the Permian region offers an unexpected reprieve to OPEC members, who have seen rampant production from America’s shale producers grab market share.

China Region

Strengths

- India’s Nifty and Sensex indices eked out a slightly positive week, closing up 6 basis points and 21 basis points, respectively. The rest of the region got more or less pummeled.

- Non-oil exports in Singapore solidly beat expectations this week, clocking in at a 15.5 percent year-over-year pace for the month of May, well ahead of analysts’ anticipated 3.0 percent print and also higher than April’s 11.8 percent number.

- Philippines overseas remittances were up for the latest (April) measurement period, coming in up 12.7 percent year over year, better than analysts’ anticipated 10.6 percent rate and back to growth versus March’s decline by 9.8 percent.

Weaknesses

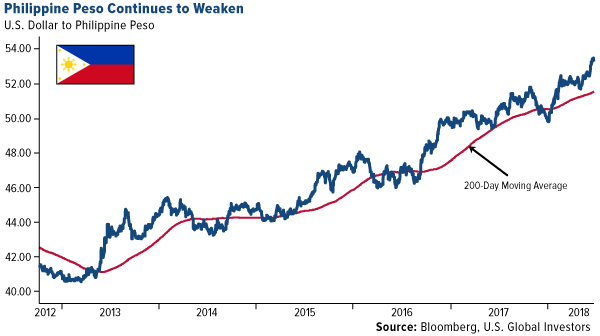

- In a red week across the region, the Philippines’ stock index (PCOMP) dropped the most, falling some 6.17 percent since last Thursday (the market was closed—like several others across the region—for holiday last Friday). Inflation pressures continue in the island nation.

- Materials constitute the worst-performing sector for the Hang Seng Composite Index (HSCI) for this week on trading. Materials dropped some 6.32 percent, followed lower by Industrials (-4.41 percent) and Financials (-3.80 percent).

- Daimler came out this week and lowered its earnings outlook due to trade concerns, demonstrating the reality of possible fallout from (a) trade war(/s).

Opportunities

- Chinese phone maker Xiaomi opted to delay a mainland listing in favor of a Hong Kong listing for its IPO, marking a win for Hong Kong in netting a large technology IPO. Later in the week, Chinese internet company Meituan Dianping announced an intention to file for an IPO in Hong Kong as well. Meituan was most recently valued near $30 billion, according to Bloomberg News.

- Talks are reportedly in the works between Chinese officials and their U.S. counterparts to revive negotiations and attempt to avert a trade war, even as U.S. President Donald Trump threatened not just $200 billion in escalation if China retaliates, but an additional $200 billion if China retaliates for the U.S. retaliation to Chinese retaliation on initial U.S. tariffs. (Are you with me?) It remains possible that such talks may lead to a breakthrough of some sort.

- Any easing of trade tensions may lead to a bounce in market sentiment.

Threats

- China, trade talks and tariffs remain and will continue to remain front and center with respect to threats as well.

- The inflation scenario in the Philippines continues to weigh on markets there, in addition to concerns about the central bank response and the peso.

- Global markets continue to monitor central banking policies for missteps and policy errors, even as the U.S. Federal Reserve continues its normalization process.

Emerging Europe

Strengths

- Turkey was the best performing country this week, gaining 1.4 percent. Elections in Turkey will take place this Sunday. Most polls are showing a close range, making it hard to predict the outcome of the elections. Capital Economics believes the vote is unlikely to have much of an impact on the near-term outlook, stating that growth will slow down sharply in the coming months regardless of the outcome. However, a victory for President Erdogan and the AKP party would add to the thinking that the longer-term outlook would be marked by slower growth, higher inflation and a weaker lira.

- The Turkish lira was the best performing currency this week, gaining 1.1 percent against the U.S. dollar. It is likely that the currency rebounded this week before the elections on Sunday due to traders trimming underweight positions.

- Real estate was the best performing sector among eastern European markets this week.

Weaknesses

- Poland was the worst performing country this week, losing 1.9 percent. Jastrzebska Spolka Weglowa declined the most among companies trading on the Warsaw stock exchange. Equity declined more than 7 percent after the company announced wage hikes and the pay out of bonuses for the prior year.

- The Polish zloty was the worst performing currency this week, losing 50 basis points against the U.S. dollar. The zloty is selling off due to Poland’s tension with the European Union over the nation’s overhaul of its Supreme Court. Two-fifths of justices will be forced to retire after July 3, when the new court rule takes effect.

- Health care was the worst performing sector among eastern European markets this week.

Opportunities

- Eurozone countries have agreed on a debt relief deal for Greece. The deal gives Athens more time to repay its loans worth 96.9 billion euros and extends the period in which Greece will pay little or no interest. Moreover, under this deal Greece will receive another 15 billion that will help to pay the country’s bills. After eight years of three bailouts, Greece may become a best performer in Europe.

- Russia’s RDIF sovereign wealth fund aims to attract over 7 billion rubles ($110 billion) from its global partners into infrastructure and technology projects. This fund would come on top of the 3 trillion rubles already pledged by Russia’s Finance Minister, Anton Siluanov. Asia and the Middle East are planning to take part in the projects via co-investment and potentially buy the ruble government bonds. Saudi Arabia has agreed to invest a total of $10 billion.

- Australia will begin negotiations with the European Union on a free-trade agreement to secure better access for Australian agricultural products, including beef, sheep meat, sugar, cheese and rice. The EU market is worth $17.3 trillion, covering 500 million people. As trade war tensions build up between the U.S., China and the eurozone, other trade opportunities emerge.

Threats

- The European Central Bank (ECB) is becoming increasingly concerned that a looming trade war could derail the eurozone’s recovery and complicates its exit from its monetary easing program. Reuters cited sources highlight that the ECB’s new economic forecasts, unveiled just a few weeks ago, may prove to be too optimistic. Protectionism could have a bigger impact on the economy than it was previously estimated.

- As EU leaders are preparing to hold a summit on the immigration crisis, Hungary just passed a law called Stop Soros that will allow it to criminalize organizations that help illegal immigrants. According to Bloomberg, it is now a crime to provide legal assistance to asylum claimants, or even to provide information about how to seek asylum. Central emerging Europe countries like Hungary, Poland and the Czech Republic do not agree with the EU’s policy on migration.

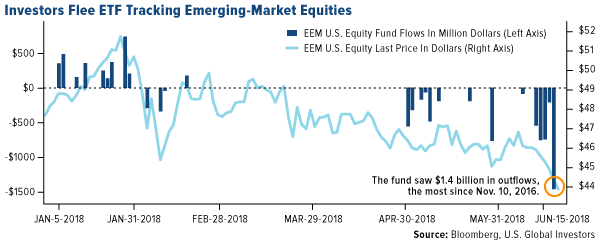

- Investors are selling the second largest exchange-traded fund tracking emerging market equites, as higher interest rates in the U.S. and intensifying trade tensions make investors bearish on emerging-market stocks. The iShares MSCI Emerging Markets ETF, or EEM, saw over $1.4 billion worth of outflows on Monday, the most since the two days following President Donald Trump’s election in November 2016.

© US Global Investors

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All