Index provider MSCI’s decision to include Saudi Arabia in its emerging-markets index will likely transform the Kingdom’s equity market, and potentially those across the Middle East and North Africa (MENA) region, according to Bassel Khatoun and Salah Shamma, Franklin Templeton Emerging Markets Equity. They weigh in on the implications they see for Saudi Arabia and the wider region of the MSCI announcement, which follows index provider FTSE’s reclassification in March.

MSCI’s decision to include Saudi Arabia in its emerging-market index recognizes the positive changes the country’s capital market has undergone over the last few years.

We think Saudi Arabia has an exciting growth story to tell, and we see a seat at the MSCI Emerging Market (EM) Index1 table as just reward for the improvements made to its equity market infrastructure, bringing it more in line with international standards.

Saudi Arabia’s emerging-market inclusion, which will take effect over two phases in May and August 2019, will likely transform the Kingdom’s capital market, and should have a positive impact on the wider Middle East and North Africa (MENA) region. We think it is the most significant reform story for emerging-market economies since China.

The speed of capital market reform in Saudi Arabia is impressive. The country’s Capital Markets Authority (CMA) and stock exchange (the Tadawul) have spearheaded the drive to modernize the Kingdom’s equity market infrastructure and accessibility for investors, by providing flexible ownership limits and introducing a two-day settlement cycle for trades.

The MSCI move follows FTSE Russell’s decision earlier this year to change Saudi Arabia’s stock-market classification to Secondary Emerging-Market status within the FTSE Russell Global Equity Index Series, effective March 2019.

Saudi Arabia’s Reform Story

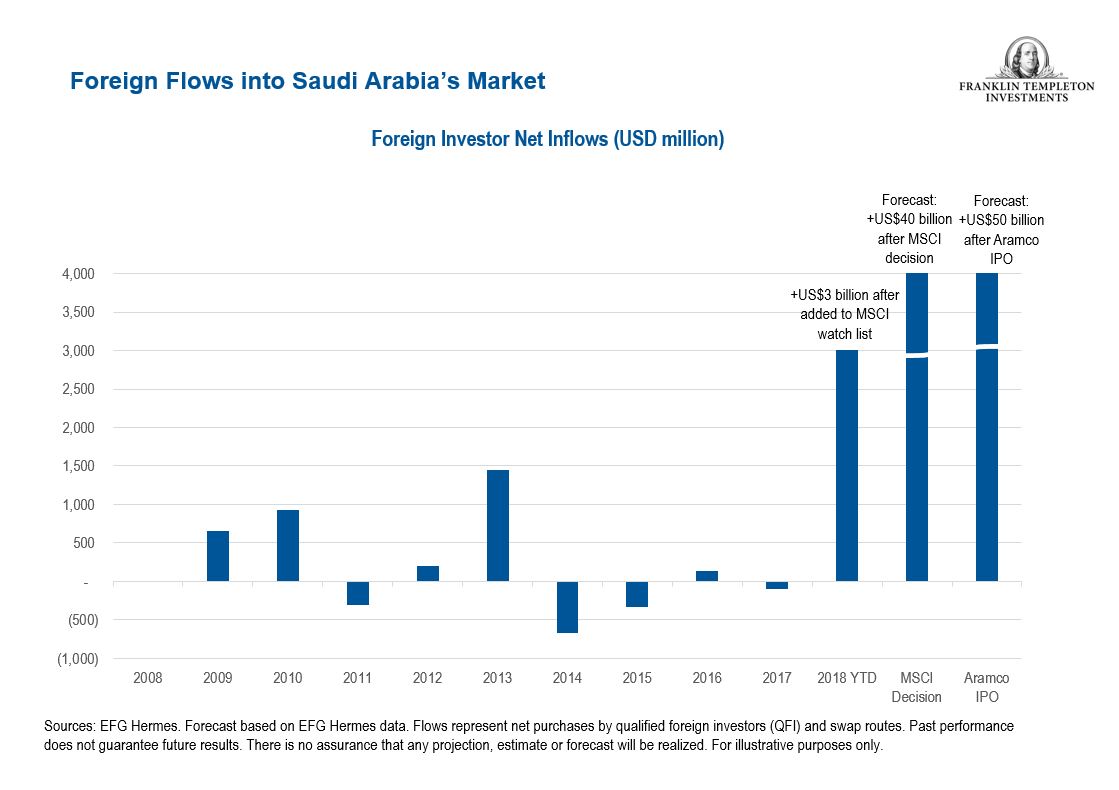

With approximately US$9 billion in foreign investment already in the Kingdom’s stock exchange2, we think Saudi Arabia’s new emerging-market status is likely to bring significant foreign investment, which could, in the long term, trickle through to surrounding economies.

Improving economic fundamentals are also likely to lure investors. A mix of higher oil prices and lower deficits have resulted in more government spending, which in turn has increased non-oil gross domestic product (GDP)3 accelerated corporate earnings growth.

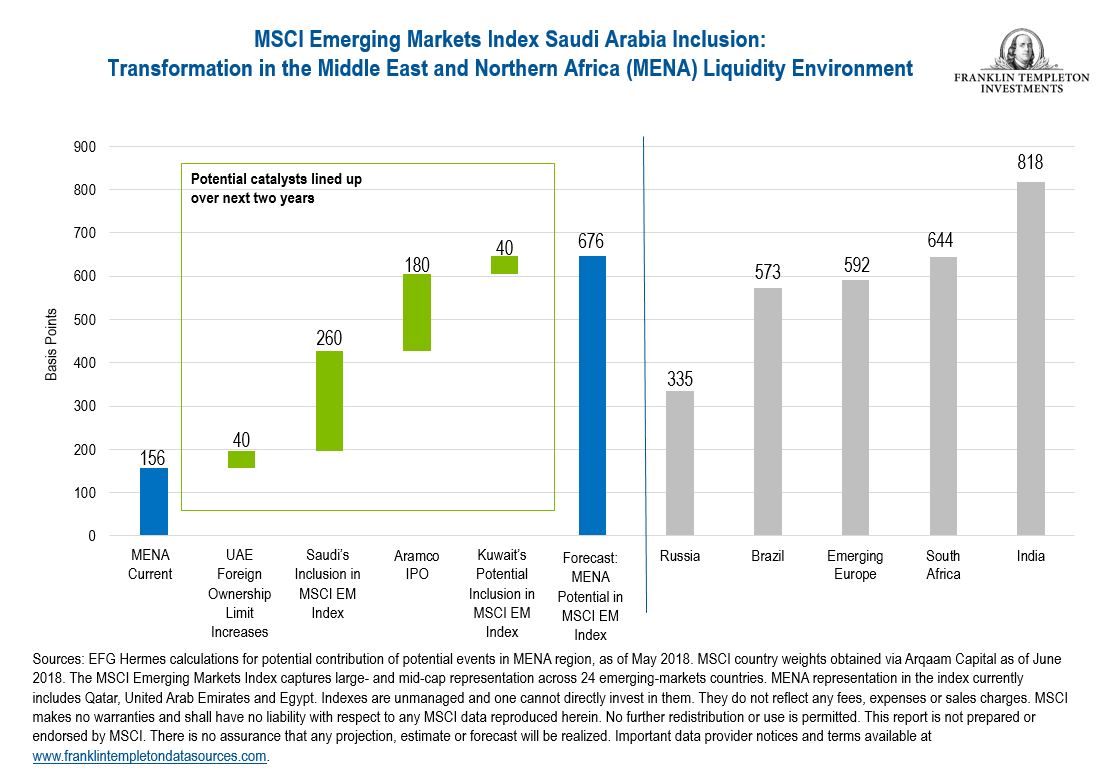

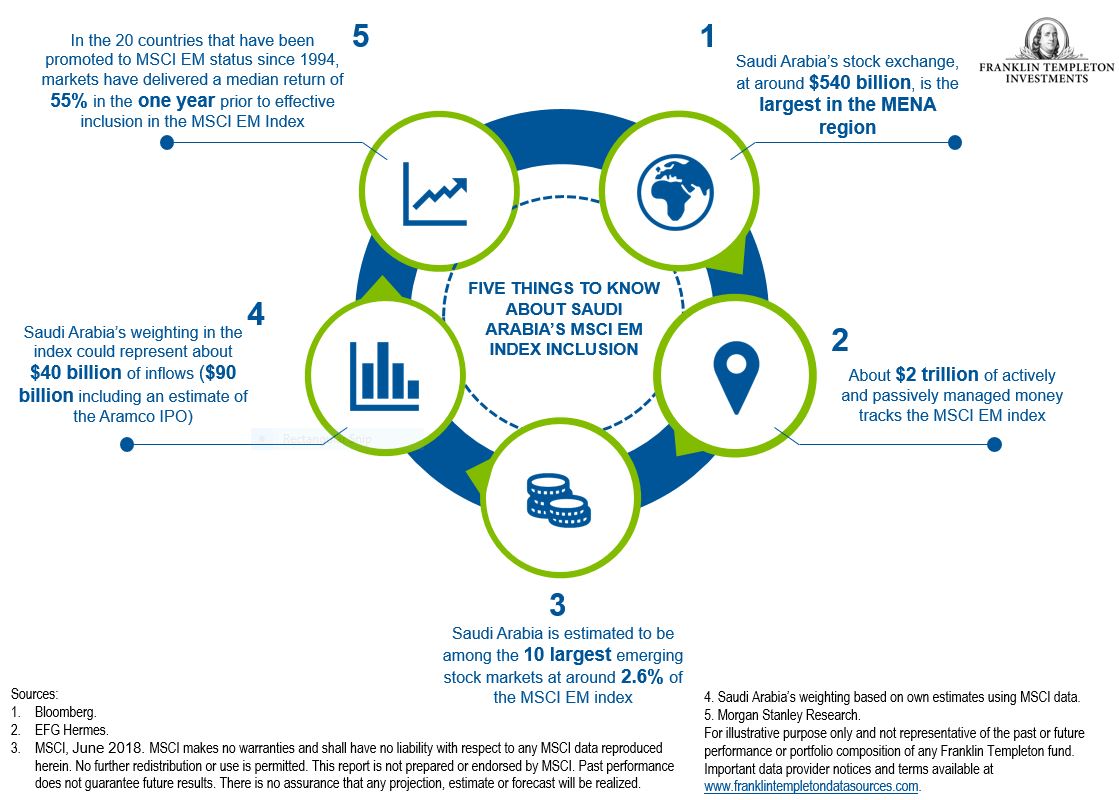

Saudi Arabia’s inclusion in the MSCI EM Index should help eradicate what we have always viewed as a material disconnect between the GDP contribution of the region and its representation in international equity indexes. To date, our analysis shows the MENA region accounts for a paltry 1.56% of the MSCI EM Index, through the United Arab Emirates (UAE), Qatar and Egypt.4 With Saudi Arabia’s inclusion, that share of the index could increase significantly. Initially, Saudi Arabia will command 2.6% of the index alone. However, with the upcoming initial public offering (IPO) of state-owned oil company, Saudi Aramco, Saudi Arabia’s weight in the index could increase substantially to over 4% in our estimation. Additionally, as part of this market classification review, MSCI has also decided to include Kuwait on its watch list. We think it’s likely Kuwait will soon follow Saudi Arabia’s footsteps in the near future, and also be upgraded to MSCI EM status.

What we are beginning to witness is the transition of this region from the peripheries into the mainstream of emerging-market investment. We think it provides suitable investors with an additional incentive to be invested in the wider MENA region.

Deepening Foreign Investment and Liquidity

Even after the recent inflows, foreigners still own only 1.8% of the Tadawul.5 By comparison, foreigners own 14.0% of the UAE (13.8% Abu Dhabi and 14.3% Dubai) and by our calculations 9.2% of Qatar, so Saudi Arabia still lags in this respect. We expect foreign ownership levels to substantially increase in the run-up to Saudi Arabia’s official MSCI EM inclusion.

Indexes have become a significant dictator of equity flows. With a massive US $1.9 trillion6tracking the MSCI EM Index7, 80% of which is active and 20% of which is passive, Saudi Arabia’s 2.6% country weighting,8 could represent an additional US$40 billion in foreign flows assuming that benchmark weight.9 This is unprecedented in the context of historical inflows into the Tadawul. According to our research, the IPO of Saudi Aramco could also potentially add another US$50 billion of assets into the market, which is approximately about US$536 billion in size.10 This is substantial, considering that over the past 10 years11, only a fraction of these net flows have come into the Saudi market, at approximately $1.9 billion12 in total.

Historical Precedents from Upgraded Equity Markets

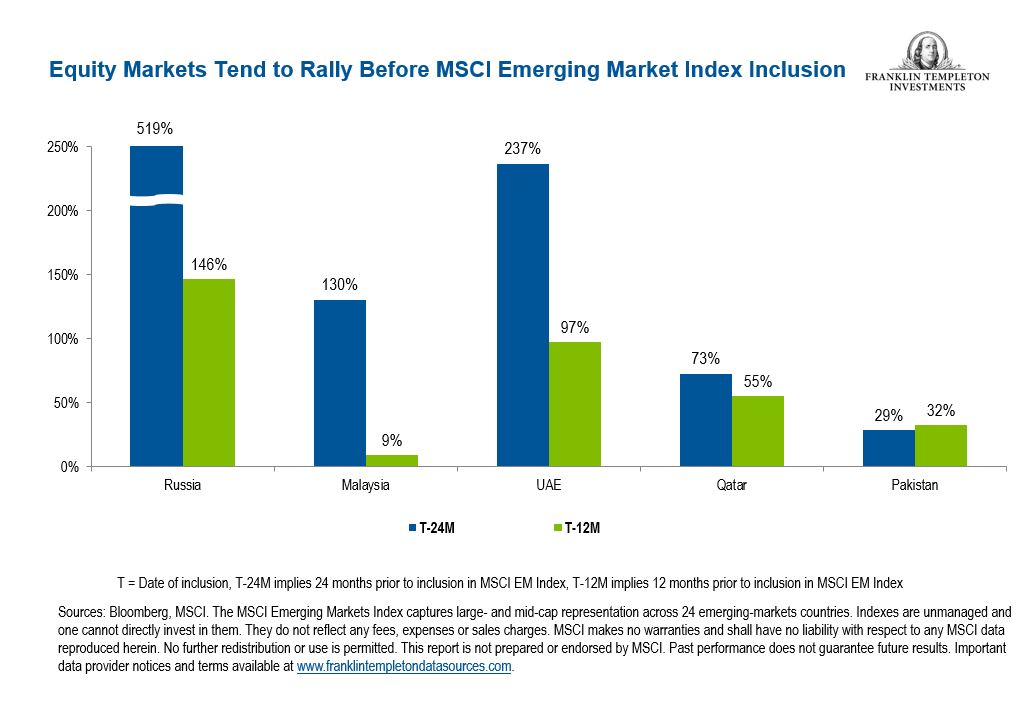

Historical precedents of MSCI EM inclusion also paint an encouraging picture. Research indicates increased investor interest in the equity market, in the one-to-two years prior to promotion. Russia, Malaysia, Qatar, the UAE and Pakistan all notably rallied in the period prior to achieving emerging-market status, as seen in the chart below. In the 20 countries that have been promoted to MSCI EM status since 1994, markets have delivered a median return of 55% in the one year prior to effective inclusion13 in the MSCI EM Index.14

We anticipate that the bulk of new investment entering Saudi Arabia will likely come from other emerging-market constituents, the largest of which are China, Korea and Taiwan. Other MENA countries’ representation in the MSCI EM Index is still low, so its surrounding neighbors will unlikely be a major source of funding for Saudi Arabia, at least in the immediate future.

That said, we think that this addition to MSCI EM could indeed trigger a re-rating of MENA markets as investors look to regional opportunities beyond Saudi Arabia. We believe the knock-on effect for the Kingdom’s neighbors could be substantial over the longer term.

THE IMPORTANCE OF ECONOMIC AND SOCIAL CHANGE

Saudi Arabia is taking extensive steps to reform its economy—and we think its new MSCI EM status coincides with the numerous fiscal reforms the Kingdom has undertaken to diversify its economy and reduce its budget deficit.

This year’s Saudi budget, for example, marks a record. We expect public spending to reach an all-time high as the Kingdom seeks to diversify its economy away from oil.

Social reform has also played an important part in the region’s development, particularly in Saudi Arabia. Riyadh is a markedly different place than it was just 12 months ago, with a slew of decisions made related to social activities and building up this part of its economy.

The Kingdom for example recently lifted a ban that prohibited women from driving, bringing additional freedom for them to potentially pursue new activities within the country. Saudi Arabia is also relaxing laws related to sports events, while cinemas and concerts are finally being reintroduced to Saudi Arabia as well, another sign of the social changes underway in the country.

From a wider environmental, social and governance (ESG) perspective, we see signs of progress inside Saudi Arabia, albeit from a relatively low base. Governance standards, in particular, have seen a broad-based improvement as a result of recent capital markets legislation. And while more can be done, we think that as the number of foreign investors in the Kingdom increases, they will in turn help support our efforts for progress through shareholder engagement.

Some Uncertainty Still Persists

Despite the exciting transformation, there are still areas of uncertainty. Lower crude oil prices, for example, could still hamper the Kingdom’s short-term growth prospects. Economic reform will need to continue if the nation is to succeed in bringing down its budget breakeven price of oil. Another factor to consider is the impact of last year’s anti-corruption purge. We have seen a number of steps taken to reassure investors, but it will be important that the Kingdom continues on this trajectory. Lastly, any increase in geopolitical tensions will also need to be monitored closely for its impact on investor confidence.

What’s Next for Saudi Arabia

2018 is a historic year for Saudi Arabia, and its MSCI EM inclusion appears to be the most significant milestone for its equity market to date. The increase in foreign flows we expect to see come into the Kingdom should be extremely supportive of the investment environment in the run-up to Saudi Aramco’s IPO. And with plans from the Saudi government to increase the number of listed companies in the Tadawul from 180 to 250 by 2022, we think this is just the start of a journey to broadening and deepening the equity market.

The results of the Kingdom’s wider economic and social reform agenda are also starting to show. With its budget deficit significantly reduced, despite a record budget expenditure being announced, we are of the view that the overall economic fundamentals are continuing to improve, and that this is being reflected in corporate earnings.

Saudi Arabia’s new MSCI EM status is undoubtedly a huge win for its capital market. The Kingdom is continuing to visibly transform, and we look forward to what it unveils to the world next.

The comments, opinions and analyses presented herein are for informational purposes only and should not be considered individual investment advice or recommendations to invest in any security or to adopt any investment strategy. Because market and economic conditions are subject to rapid change, comments, opinions and analyses are rendered as of the date of the posting and may change without notice. The material is not intended as a complete analysis of every material fact regarding any country, region, market, industry, investment or strategy.

What Are the Risks?

All investments involve risks, including the possible loss of principal. Investments in foreign securities involve special risks including currency fluctuations, economic instability and political developments. Investments in emerging markets, of which frontier markets are a subset, involve heightened risks related to the same factors, in addition to those associated with these markets’ smaller size, lesser liquidity and lack of established legal, political, business and social frameworks to support securities markets. Because these frameworks are typically even less developed in frontier markets, as well as various factors including the increased potential for extreme price volatility, illiquidity, trade barriers and exchange controls, the risks associated with emerging markets are magnified in frontier markets. Stock prices fluctuate, sometimes rapidly and dramatically, due to factors affecting individual companies, particular industries or sectors, or general market conditions.

1. The MSCI Emerging Markets Index captures large- and mid-cap representation across 24 emerging-markets countries. MENA representation in the index currently includes Qatar, United Arab Emirates and Egypt. Indexes are unmanaged and one cannot directly invest in them. They do not reflect any fees, expenses or sales charges. MSCI makes no warranties and shall have no liability with respect to any MSCI data reproduced herein. No further redistribution or use is permitted. This report is not prepared or endorsed by MSCI. Important data provider notices and terms available at www.franklintempletondatasources.com.

2. Source: Tadawul Market Report, May 31, 2018. This figure excludes joint ventures and strategic stakes.

3. The Ministry of Finance of Saudi Arabia, Budget Performance Report, 2018.

4. Source: EFG Hermes.

5. Source: Tadawul Market Report, May 31, 2018. This figure excludes joint ventures and strategic stakes.

6. Source: MSCI.

7. The MSCI Emerging Markets Index captures large- and mid-cap representation across 24 emerging-markets countries. MENA representation in the index currently includes Qatar, United Arab Emirates and Egypt. Indexes are unmanaged and one cannot directly invest in them. They do not reflect any fees, expenses or sales charges. MSCI makes no warranties and shall have no liability with respect to any MSCI data reproduced herein. No further redistribution or use is permitted. This report is not prepared or endorsed by MSCI. Important data provider notices and terms available at www.franklintempletondatasources.com.

8. Source: MSCI, June 2018.

9. EFG Hermes. Estimate based on EFG Hermes data.

10. Source: Bloomberg.

11. Time period of December 2008 – December 2017.

12. Source: EFG Hermes.

13 Source: Morgan Stanley Research, August 2014. Countries include the 20 market promotions to MSCI EM status since 1994, including: Colombia, India, Pakistan, Peru, Sri Lanka, Venezuela, Israel, Poland, South Africa, China, Czech, Hungary, Taiwan, Russia, Malaysia, Egypt, Morocco, Greece, UAE and Qatar.

14. Past performance does not guarantee future results.The MSCI Emerging Markets Index captures large- and mid-cap representation across 24 emerging-markets countries. MENA representation in the index currently includes Qatar, United Arab Emirates and Egypt. Indexes are unmanaged and one cannot directly invest in them. They do not reflect any fees, expenses or sales charges. MSCI makes no warranties and shall have no liability with respect to any MSCI data reproduced herein. No further redistribution or use is permitted. This report is not prepared or endorsed by MSCI. Important data provider notices and terms available at www.franklintempletondatasources.com.

© Franklin Templeton Investments

© Franklin Templeton Investments

Read more commentaries by Franklin Templeton Investments