Weighing the Week Ahead: What is Working, and Will It Persist?

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsThe economic calendar is modest. Volatility is lower even with plenty of news. The summer doldrums have arrived!

It provides time for introspection to fill those empty timeslots and pages. Pundits might be (and should be) asking:

What is working? Will it keep working?

Last Week Recap

In my last edition of WTWA speculated that the first part of the week would be all about international issues and the Fed, but the summer doldrums might hit by week’s end. That was more accurate than I expected. Who would have expected so little volatility from a week loaded with potentially market-moving events? I suggested a pivot to more talk about identifying important continuing issues. We did see some of that, and I expect there will be much more.

The Story in One Chart

I always start my personal review of the week by looking at a great chart. I especially like the version updated each week by Jill Mislinski. She includes a lot of valuable information in a single visual. The full post has even more charts and analysis, including commentary on volume. Check it out.

The market was unchanged with the smallest trading range in months — about 1%. I summarize actual and implied volatility each week in our Indicator Snapshot section below. Volatility is back into the long-term range.

Noteworthy – Analysis of Debt

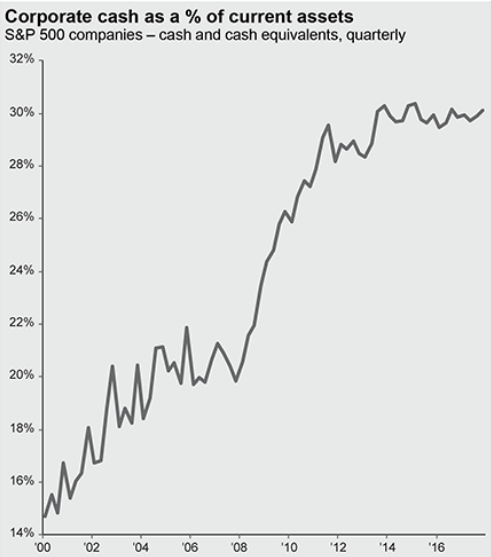

Readers have frequently commented or inquired about debt. My response has been that it is not a concern at the household and corporate levels, and not an immediate investment concern for government. The stories about debt have great popular appeal, especially when they do not include any comparisons. I have been including this “Noteworthy” section to permit analysis of important topics that do not necessarily relate to “the week ahead.”

Urban Carmel has an excellent, comprehensive analysis. It takes note of decades of similar arguments. You can also consider evidence about comparisons to past debt levels and ability to pay. Those interested in this topic will appreciate the analysis and charts. There are so many good ones that it is difficult to choose. Just as an example, “Debt should be looked at on a net cash basis; this is material as cash levels have risen dramatically. Debt to GDP ratios [Jeff – a popular chart comparison] ignore cash (chart from JPM)”.

The News

Each week I break down events into good and bad. For our purposes, “good” has two components. The news must be market friendly and better than expectations. I avoid using my personal preferences in evaluating news – and you should, too!

The positive economic trends continue. New Deal Democrat’s useful update of high-frequency indicators shows continuing strength in the current and short-term leading indicators, and improvement in the long-term group.

The Good

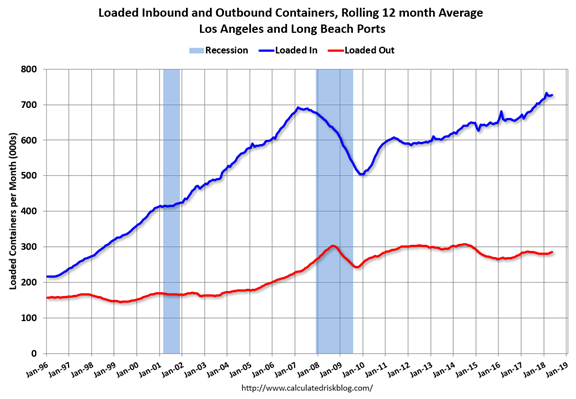

- Port traffic increased again in May on a year-over-year basis. Calculated Risk uses a rolling twelve-month analysis because of the strong seasonal component in the data.

- The FOMC rate decision was well-received. The rate hike was expected, and the accompanying press conference raised no fresh worries. Fed expert Tim Duy has a complete account and analysis of what is to come. Scott Grannis, with his usual chart pack, explains the market expectation: The pace of increases has been necessary just for monetary policy to stay “neutral.”

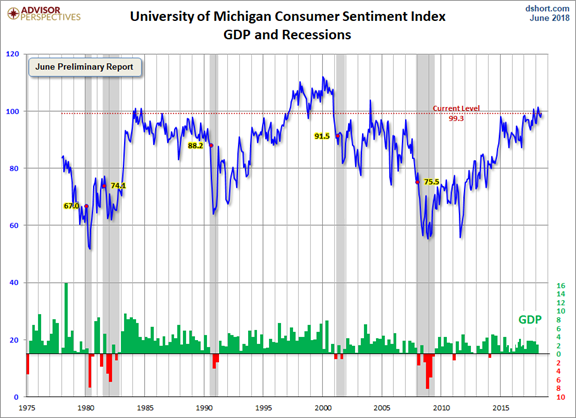

- Michigan sentiment rose slightly and remained at recent high levels. Jill Mislinksi has the story and a chart that pulls it all together.

- Consumer inflation remains tame. The core and headline CPI both increased the expected 0.2%.

- Initial jobless claims were only 218K, beating expectations (223K) and the prior week (222K).

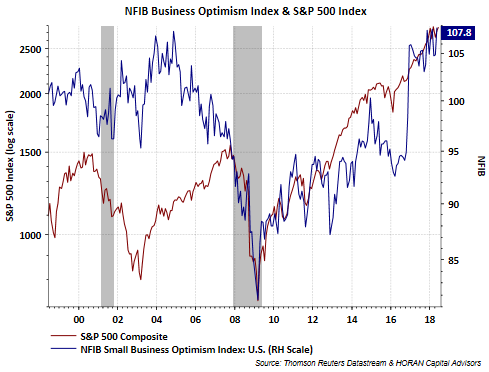

- The NFIB business optimism index posted the second-highest level in history. David Templeton (HORAN) has good coverage, and an interesting chart comparison with the S&P 500.

- Retail sales showed a 0.8% increase, much better than the expected (and prior month) gain of 0.4%. Please check the effect and a link for more detail in the Big Four update in the quant section.

The Bad

- Producer prices increased 0.5% compared to expectations of 0.3% and last month’s 0.1%.

- Industrial production declined 0.1% versus an expected gain of about 0.1%. Steven Hansen (GEI) has a detailed analysis, including explanation of the indicator and year-over-year comparisons.

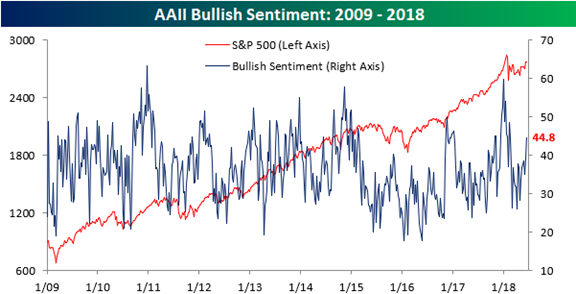

- Bullish sentiment (a contrary indicator) is at a four-month high. (Bespoke).

The Ugly

Fake news. Very fake news. Satire. When people pick up satire – in this case about a breakdown in Merkel’s coalition – the speed of social media leaves no time for analysis. Bloomberg shows the impact on the Euro. Many traded based on the false information or the “signals” from the information.

The Week Ahead

We would all like to know the direction of the market in advance. Good luck with that! Second best is planning what to look for and how to react.

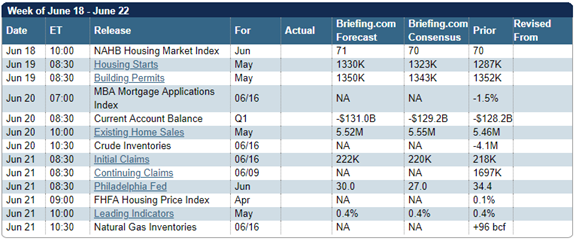

The Calendar

We have a modest economic calendar featuring several different housing reports. Fans of the Leading Indicators series will see that at week’s end.

If the FOMC meeting didn’t provide enough Fed news for you, look forward to a significant uptick in FedSpeak.

Briefing.com has a good U.S. economic calendar for the week (and many other good features which I monitor each day). Here are the main U.S. releases.

Next Week’s Theme

There is little news on the calendar, providing a vacuum. As in the famous quote: The punditry abhors a vacuum! (Mrs. OldProf says I got this wrong, but she is too focused on her HS science classes). In Chicago, the news is filled with the deal with Elon Musk to build a rapid transit tunnel and the suburban Stormy Daniels performances. After some controversy, the schedule has been confirmed. It is attracting many first-time visitors to such an establishment, all willing to pay $30-50 for a brief show. As you can see, there is a vacuum.

Any news event might pop up and command attention, but I can’t even guess about that. It is a good time for an assessment of current trends and whether than will continue. I expect pundits to be asking:

What is working, and will this trend persist?

Here are some current popular themes. Please feel free to suggest more in the comments.

- Small cap stocks. “Red hot” says Ed Yardeni.

- Economic growth and health – both the US and global.

- Demographic trends

- Millennials – consumption, housing, employment

- Baby boomers – retirement, health care, housing shifts

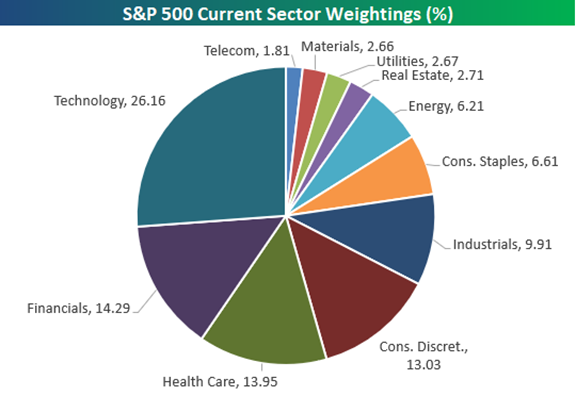

- Leadership in cap-weighted ETFs. Brian Gilmartin shows the current list and then a striking contrast — the top ten by earnings weight. You can guess one of the two big missing names from the second list, but perhaps not both. Bespoke’s typically fine chart shows the current sector weightings, emphasizing the increase in cyclical stocks.

- Yield plays. Interest rate increases are hitting real estate and utility stocks. (WSJ)

- Trade issues. Will the actions escalate and what stocks are affected? (Barron’s)

- Worldwide hot spots. South Korea? (Rob Marstrand). Russia?

- Emerging market ETFs. Hot and then not. What will dollar strength do?

- Energy. Are oil prices capped by production increases? (WSJ).

- Factor investing trends and traps. Greenline’s CIO warns about data mining effects, even in the most popular factors.

- Autonomous vehicles. Prof. Timothy Taylor looks far into the future and checks what may happen along the way. You will appreciate the nice examples as well as the analysis.

- Mid-term elections. Probably important, but tricky to play effectively.

These are all important, with significant potential impacts. As usual, I’ll offer my own conclusions in today’s Final Thought.

Quant Corner

We follow some regular featured sources and the best other quant news from the week.

Risk Analysis

I have a rule for my investment clients. Think first about your risk. Only then should you consider possible rewards. I monitor many quantitative reports and highlight the best methods in this weekly update.

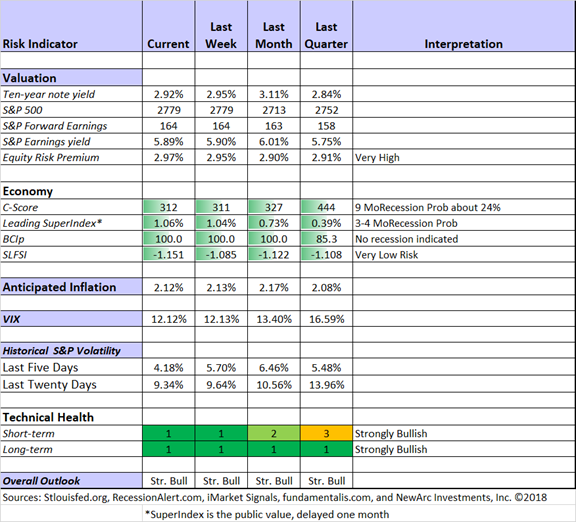

The Indicator Snapshot

Short-term trading conditions continue at favorable levels, much improved from a quarter ago. Also noteworthy is the reduced volatility. Some investors were spooked out of their holdings by volatility earlier in the year. Even though levels were in line with historic norms, and even though volatility is not a leading indicator of declines, it was too much for some.

The Featured Sources:

Bob Dieli: Business cycle analysis via the “C Score.

Georg Vrba: Business cycle indicator and market timing tools. None of Georg’s indicators signal recession.

Brian Gilmartin: All things earnings, for the overall market as well as many individual companies.

RecessionAlert: Strong quantitative indicators for both economic and market analysis.

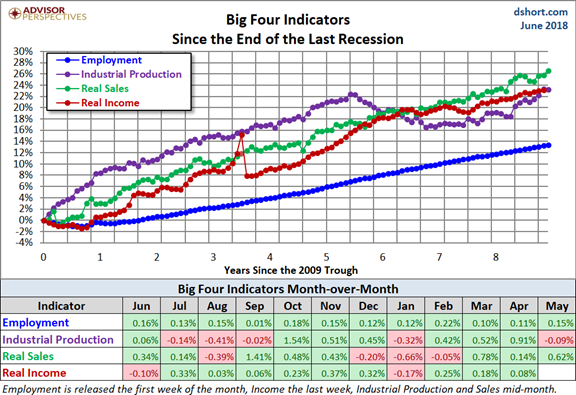

Doug Short and Jill Mislinski: Regular updating of an array of indicators. Great charts and analysis. With two important updates this week, it is time to take a look at the latest chart of the Big Four economic indicators used by the NBER in recession determination.

The continuing strength in the important indicators is apparent.

Insight for Traders

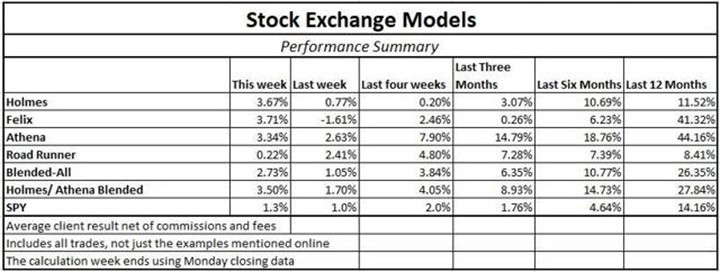

Check out our weekly Stock Exchange post. We combine links to important posts about trading, themes of current interest, and ideas from our trading models. This week we asked fellow traders about their experiences in designing a trading system. Our analysis included a list of lessons from my own work as well as ideas from a range of great sources. All the lessons are grounded in experience, including the brutal (but typical) blowout story of a rookie trader.

We also discussed some stock ideas and updated the ratings lists for Felix and Oscar, this week featuring the Nasdaq 100. Blue Harbinger is our editor for this information and ringleader for the group discussion. We also have weekly performance updates. Even those who are not interested in trading with a one to six-month time frame may be interested in what style is working. One of the models aims for, and usually achieves, a long term holding period.

Insight for Investors

Investors should have a long-term horizon. They can often exploit trading volatility.

Best of the Week

If I had to pick a single most important source for investors to read this week it would be Charlie Bilello’s work – two articles! In one he takes on a famous piece of Buffett advice – Rule #1: Never lose money. After demonstrating that Mr. B (like everyone else) had some losses, including major portfolio drawdowns, he changes focus to portfolio construction. He explains the role of both stocks and bonds in a portfolio.

In the second, he explains the difference between investing and speculating. Most importantly (and like Mr. B) he notes that for investors, lower stock prices are a good thing. You are not planning to sell right away.

Because it is giving them the opportunity to reinvest interest/dividends and add new capital at discounted prices. If you have a long enough time horizon and a diversified portfolio, buying at lower prices will increase your long-term returns. Which is why a stock market crash is the best thing that could happen to young investors.

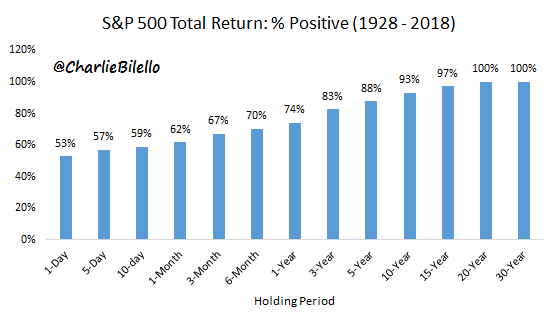

He then includes a series of charts looking at the median market return for different holding periods. It is quite clear that investors are characterized by expected holding period.

Holding stocks for a day or a week is not much better than a coin flip. In that time frame, you don’t have the luxury of waiting for stocks to come back and any decline should make you nervous. In contrast, holding stocks for 20-30 years has never yielded a negative return, even for investors who bought at the peak in 1929 and held throughout the Great Depression. If that is your time frame you want stocks to go on sale – the earlier, the better.

Stock Ideas

Chuck Carnevale does his typical tour de force. He analyzes Proctor & Gamble (PG) helping us to find the best valuation metric.

Brian Gilmartin does his expected comprehensive work on Apple (AAPL). His balanced analysis helps investors to see exactly what they should be watching.

Marc Gerstein uses his stock screening approach to unearth an idea: Zagg.

RoseNose provides a portfolio update. Check out the changes implied by the solid choice of criteria.

Stone Fox Capital looks at the DOJ Time Warner decision and sees value in AT&T (T).

Barron’s features American Axle (AXL), a cheap auto stock which caters to the growing market segments.

When to sell?

D.M. Martins Research asks whether the time has come for Target (TGT).

I raise a broader question about taking profits and pay taxes? While there is no easy and universal answer, I shared a method that I find useful – what I am calling our Tax Tool. It helps to clarify what is at stake.

Portfolio Construction

Kirk Spano takes on the question of how to start a portfolio – right now. You might view this as an alternative take on this week’s theme. He has his own list of the big secular trends.

Personal Finance

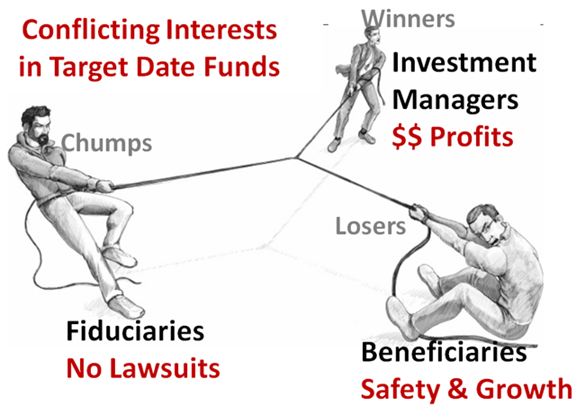

Seeking Alpha Senior Editor Gil Weinreich has expanded his excellent series for financial advisors (and serious individual investors) to include some podcasts. This week I especially enjoyed his post on the fleeting fame of some investments. A favorite link was the analysis of target date funds by Ronald Surz. Do these really match your personal needs?

Abnormal Returns always has helpful links and now some longform posts as well. I am a subscriber, and I read every post. It is a helpful source for many ideas I feature on WTWA. On Wednesday he has a special group of links for those interested in personal finance. This week included many good ideas, but my favorite was Richard Quinn’s discussion of how investors should evaluate health benefits as part of retirement planning. Most workers undervalue these benefits, throwing off their overall plan.

Watch out for…

Harley Davidson? Valentum suggests that the Glory days may be behind the company.

Dave and Buster’s? (PLAY) Stone Fox Capital analyzes the apparent earnings beat.

MLPs. Dividend Sensei analyzes the Kinder Morgan (KMG) news and highlights five things you need to know. There is a lesson here for those attempting this approach to income investing.

Target Date Fund conflicts of issues. Ronald Surz extends his analysis to look at the fund advice, sales, marketing and purchase from different perspectives. This is important reading.

Final Thoughts

I raised many questions this week. The Final Thought section allows me to keep my own conclusions separate. While I give a hint of the reasoning and my methods, I cannot give a full analysis of each point. Feel free to disagree! If there is interest in a topic, I’ll try to take it up in greater depth.

Diversity

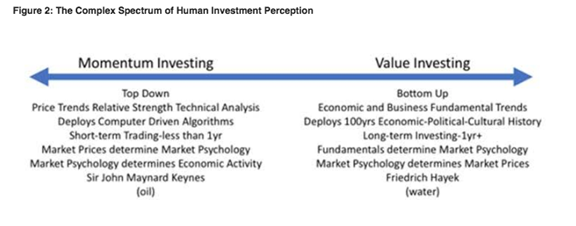

Most of my colleagues seek diversity in allocation by type of assets. I like to find diversity in methods. Davidson (via Todd Sullivan) explains that there is no “math solution” to the market. He has a nice contrast between momentum and value strategies. As a value investor, he has developed some respect for momentum. Here is his conceptual scheme, but you need to read the entire post to appreciate it. In most week’s this would be the BOTW.

Personally, I seek value stocks as well as growth at a reasonable price (GARP). My own portfolio, and that of clients who can handle short-term gains, includes momentum-driven strategies as well. This is diversity of method – an important concept.

Being Contrarian

This certainly does not mean being foolish, but it includes a willingness to embrace the unloved stocks and sectors. A particularly fertile source is analyzing the economy. So many market participants take pride in a lack of economic education. They love to write about mistakes of economists. John Rekenthaler (Morningstar) writes that “everybody” missed the market rally. He recounts some old fears and summarizes the many errors. I should not be surprised that I read Mr. Rekenthaler more than he reads me! What he summarizes in this article you can go back and read on WTWA in real time. Or check out the CNBC interview. It is a good thing that fame is not my goal. I would have to do a lot more schmoozing!

My fundamental triad: Growth in expected earnings, low recession risk, and comparison of stocks with other easily purchased assets. I provide the ingredients every week. You need not read my entire post, although I appreciate those who do. You can just check out the indicator snapshot. And my secret sauce? I know enough to find real experts and then follow their lead.

Major Social Trends

Another angle is a focus on demographic trends and needs. It is obvious that people are getting older and will need more health care. Drug development and medical facilities will be increasingly important. You may play this angle in many ways, but the current market is over-emphasizing the control of drug prices. People will demand new solutions. Those who succeed in development must (somehow) get a reward for their efforts.

Ignoring Simplistic “Headline” Takes

Avoiding overly-simplistic two-variable comparisons is also a great source of ideas. Market participants, guided by algorithms that derive correlations from past relationships, place excessive emphasis on minor data points. Home ownership and construction is a good example. Purchase costs have increased, but the demographic forces are powerful. The best analysts emphasize scarcity of inventory, not cost, as a limiting factor in home sales. You cannot solve this problem with two variables.

Energy is a similar problem. Instead of considering an interplay between supply and demand, most sources look at each independently. The biggest mistake is viewing oil prices as an economic indicator. I do see price increases as limited due to supply and potential supply increases.

Even if you do not agree with my suggestions, I hope they are stimulating and helpful!

If you are distracted by noise from so many financial sources, feel free to request more information or a no-obligation consultation. Just send an email to main at newarc dot com. (Like you, we hate spam and do not share addresses). We have several free resources that might be helpful in avoiding pitfalls and focusing on the best methods.

I’m more worried about:

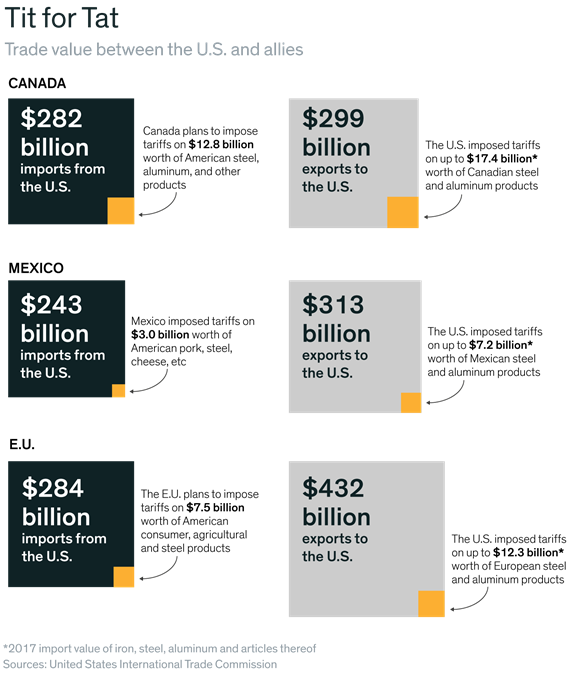

- Trade policy. The reciprocal retaliations have begun.

- Iran negotiations. There are many ways this can go wrong.

I’m less worried about:

- The overall economy. The general pattern of economic data, more useful than reaction to individual reports, is positive and improving.

- Inversion of the yield curve. The long end of the curve, not controlled by the Fed, may eventually reflect higher inflation expectations. Meanwhile, the arbitrage with European debt has a ceiling on US rates.

Membership required

Membership is now required to use this feature. To learn more:

View Membership Benefits