Key Points

-

Total credit market debt is down from its pre-financial crisis high, but still stratospheric.

-

Although household and financial sector leverage has come down significantly post-financial crisis, government and nonfinancial corporate leverage has been skyrocketing.

-

Expected stronger economic growth is a good thing, but it’s also bringing tighter monetary policy, which has implications for servicing the rising burden of debt.

I spend a lot of time on the road speaking to our investors and advisors and one of the common questions I get during the Q&A sessions is, “What keeps you up at night?” Aside from having an 18-year old daughter—and being a chronic insomniac anyway—my reply usually centers around debt and the burden it has and will continue to place on our economy. The broadest measure of debt is “total credit market debt,” which includes every measurable form of debt across the government and private sectors. (What it decidedly does not include is the future debt associated with this country’s unfunded entitlements…but that’s a story for another day.)

Some of the best data gathering on debt is done quarterly by my friends at Ned Davis Research (NDR). By the way, I’ve been an insatiable consumer of NDR’s research since the mid-1980s, when Ned and my first boss, Marty Zweig, often put their considerable talents together with research projects. In addition, I am always grateful to my friends at NDR who often work with us on custom research projects and data gathering.

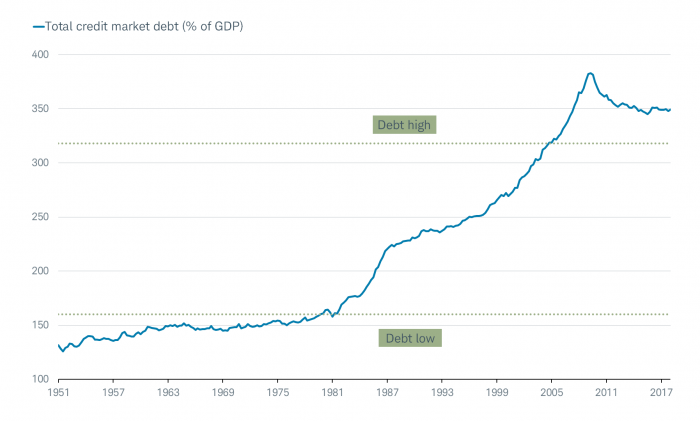

This report will be chart-heavy (many from NDR) but less wordy; as in many cases, the charts practically speak for themselves. First up, is the aforementioned total credit market debt, which as you can see below, is at a whopping 350% of U.S. gross domestic product (GDP). That’s down from nearly 380% of GDP before the global financial crisis (GFC), but still “comfortably” in the high debt zone. The implications of such a high debt load are notable across the spectrum of economic statistics, as seen in the accompanying table.

Debt Down, But Still in Stratosphere

Source: Charles Schwab, FactSet, Ned Davis Research (NDR), Inc. (Further distribution prohibited without prior permission. Copyright 2018© Ned Davis Research, Inc. All rights reserved.), as of March 31, 2018.

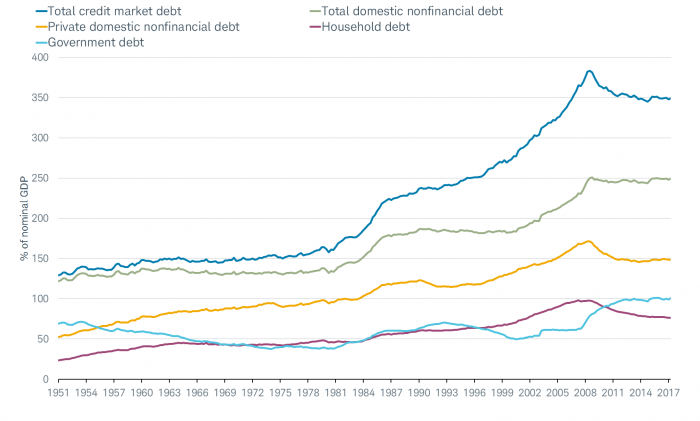

Total credit market debt has several key components, including government debt, domestic nonfinancial debt and household debt. As you can see in the chart below, it was largely the deleveraging by the private sector—specifically households—in the aftermath of the GFC which accounted for the overall decline.

Total Credit Market Debt Components

Source: Charles Schwab, Federal Reserve, Ned Davis Research (NDR), Inc. (Further distribution prohibited without prior permission. Copyright 2018© Ned Davis Research, Inc. All rights reserved.), as of March 31, 2018. Government debt=federal, state and local.

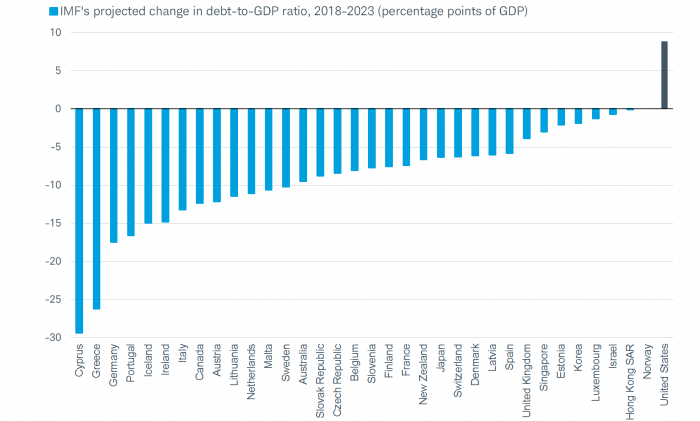

Looking ahead, the picture doesn’t get much brighter. The latest projections from the International Monetary Fund (IMF) of government debt as a share of GDP across 35 major global economies has only the United States moving higher over the next five years.

IMF Singles Out United States for Rising Debt Burden

Source: Charles Schwab, IMF (International Monetary Fund) April 2018 Fiscal Monitor. GDP weights are based on 2023 current US$ GDP.

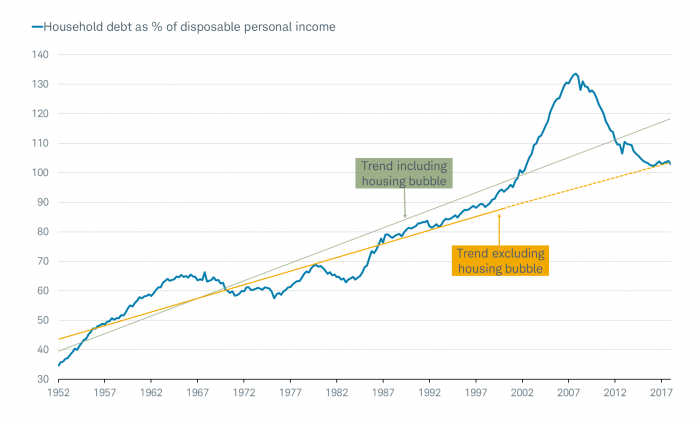

As mentioned, the GFC ushered in a record-breaking era of deleveraging on the part of the household sector. Of course, it was forced upon households when the housing market crashed, took down the economy and markets with it, and led to a drying up of both the supply of new loans, but the demand for borrowing as well. As you can see in the chart below, household debt as a percentage of disposable personal income has not only broken through the long-term trendline; it’s done so relative to the pre-debt bubble trendline as well.

Household Debt Back to Reasonable Levels

Source: Charles Schwab, FactSet, Federal Reserve, as of March 31, 2018.

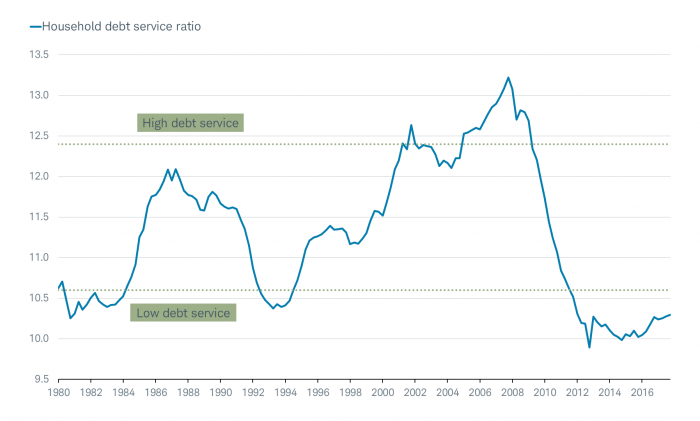

For now, the cost to households of servicing that debt remains exceptionally low; but of course, that will rise alongside a rise in longer-term interest rates. (There is a lot more that can be written on household debt, including its components and trouble spots, like student loans; but let’s leave that for another day.)

Households’ Debt Service Costs Low But Rising

Source: Charles Schwab, FactSet, Federal Reserve, as of December 31, 2017.

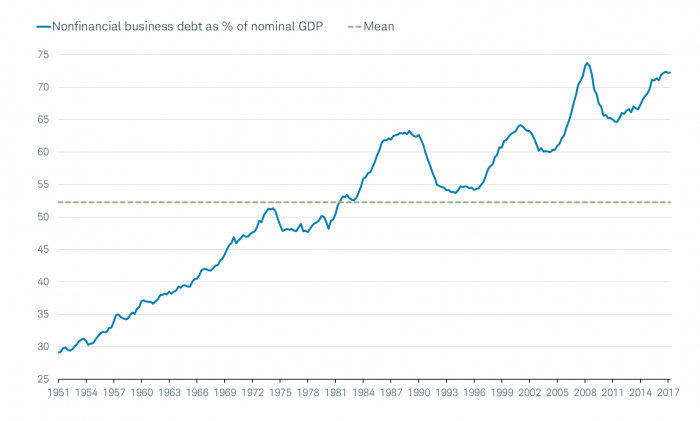

A subject lately about which I’ve received numerous questions is corporate debt; and as you can see below, nonfinancial business debt as a share of GDP has been rising and is nearly as high as GFC-era levels.

Corporate Debt Near Prior Peak

Source: Charles Schwab, Department of Commerce, Federal Reserve, Ned Davis Research (NDR), Inc. (Further distribution prohibited without prior permission. Copyright 2018© Ned Davis Research, Inc. All rights reserved.), as of March 31, 2018.

I had an exchange with my colleague Collin Martin (Director, Fixed Income Strategy) last week and here is a summary of his thoughts:

Rising corporate debt levels are definitely a risk in the long-term. Many companies took advantage of the low interest rate environment which has persisted since the GFC by issuing more and more debt with low coupon rates, while extending the average maturity of their debt. According to SIFMA, corporate bond issuance has increased every year since 2011, and the amount of investment grade corporate bonds outstanding has more than doubled over the past decade.

It’s the case that many of the proceeds from issuing debt have been used for share repurchases, dividend payouts and merger and acquisition (M&A) activity. As such, debt/net worth of nonfinancial corporates has actually been declining since the end of the GFC. Companies are often criticized for share repurchases as it’s seen as “financial engineering,” which is in contrast to putting that cash to work toward more productive long-term capital investments. There is validity to that; but for what it’s worth, NDR’s data shows that companies which have spent more on buybacks as a percent of their market cap have generally been outperforming. But that of course means that stock investors have been rewarded, at the expense of the economy.

That being said, much of the repurchase resurgence this year has come from companies which are repatriating overseas cash because interest rates were lower than tax rates. If companies spend repatriated money on buybacks, then refinancing debt in a few years could become increasingly difficult; especially if the Fed continues to raise rates, as is expected. It may not be a 2018 issue, but it will increasingly be a risk in the next year or two.

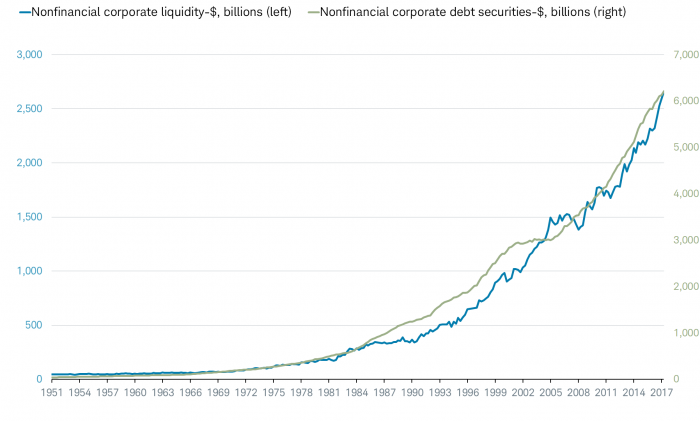

In sum, we don’t think the credit markets will necessarily “break” in the near-term. While corporate debt continues to rise, aggregate cash balances and liquid assets remain relatively high as well, as you can see in the chart below.

Debt High, But So’s Liquidity

Source: Charles Schwab, Federal Reserve, Ned Davis Research (NDR), Inc. (Further distribution prohibited without prior permission. Copyright 2018© Ned Davis Research, Inc. All rights reserved.), as of March 31, 2018.

In the meantime, corporate profits continue to rise and financial conditions remain relatively easy despite rate hikes. Although short-term interest rates are up sharply over the past few years, it will take some time for higher financing costs to make their way through the corporate market since average corporate bond maturities have been extended.

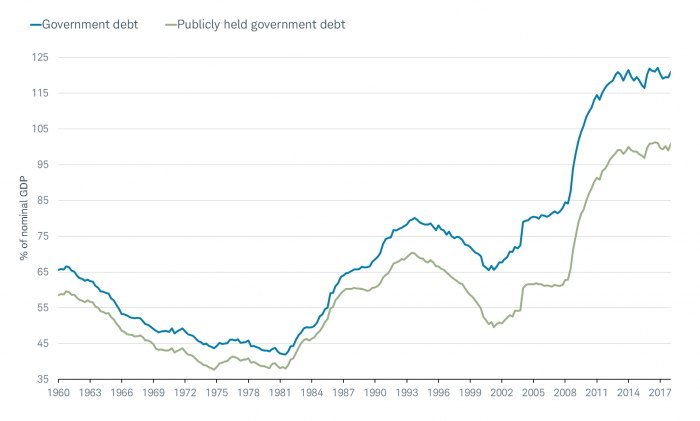

Finally, there is government debt; and the chart below shows overall debt, but also just debt which is held by the public. Clearly, there has been no deleveraging on the part of the public sector.

Government Debt Remains Near All-Time High

Source: Charles Schwab, Department of Commerce, Department of Treasury, Federal Reserve, Ned Davis Research (NDR), Inc. (Further distribution prohibited without prior permission. Copyright 2018© Ned Davis Research, Inc. All rights reserved.), as of March 31, 2018. Government debt=federal, state and local.

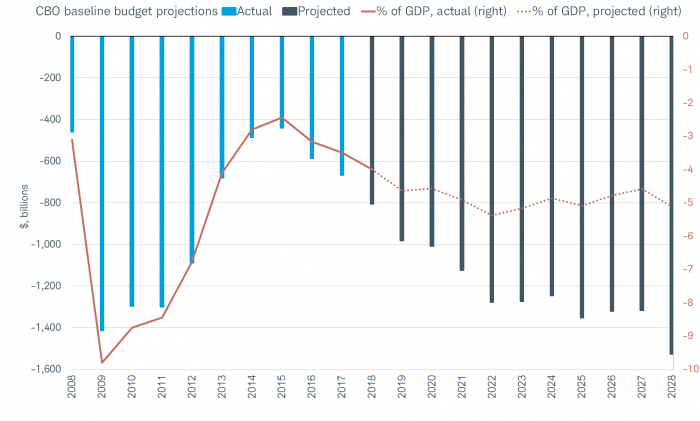

To the extent you look at the chart above and hope the flattening-out is a sign that debt is rolling over; think again. Remember, government debt is the cumulative effect of running budget deficits. The deficit had actually been improving between 2009 and 2015; but has recently deteriorated. Then of course, we got the new budget earlier this year, which incorporated a significant boost to government spending. And that was separate from the tax reform bill passed last year. As such, Congressional Budget Office (CBO) projections for the next decade show a massive deterioration. And most of this represents mandatory entitlement spending if no reform is seen.

Budget Deficits Blowing Out

Source: Charles Schwab, CBO’s (Congressional Budget Office) April 9, 2018 Report: The Budget and Economic Outlook: 2018 to 2028, FactSet.

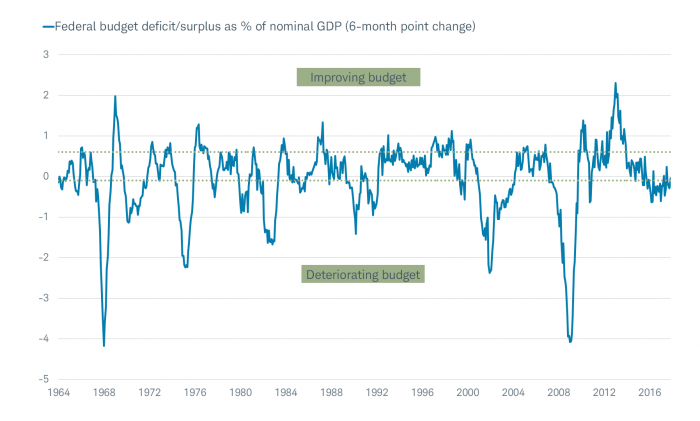

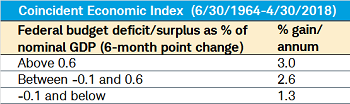

If you look historically at rolling six-month trends in the budget deficit/surplus (seen in the chart below), you will see that a deteriorating budget deficit has been historically met with weak economic growth (see the accompany table, which shows the “coincident index,” a monthly proxy for quarterly GDP).

Deteriorating Budget

Source: Charles Schwab, Ned Davis Research (NDR), Inc. (Further distribution prohibited without prior permission. Copyright 2018© Ned Davis Research, Inc. All rights reserved.), as of April 30, 2018.

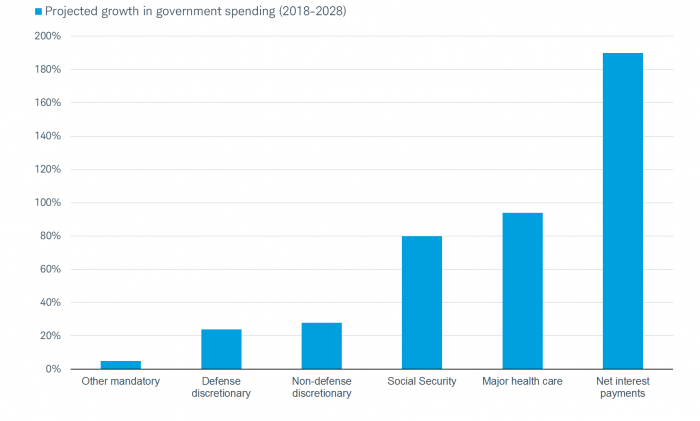

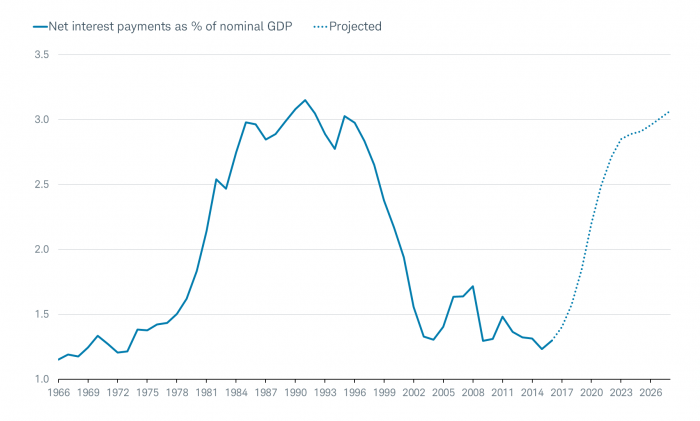

The saddest of projections can be seen in the two charts below. All else equal, by the end of the next 10 years, net interest payments will swamp the government’s spending on everything else.

Net Interest Payments’ Growth to Swamp Other Spending

Source: Charles Schwab, CBO’s (Congressional Budget Office) April 9, 2018 Report: The Budget and Economic Outlook: 2018 to 2028, FactSet.

Net Interest Payments to Surge as % of GDP

Source: Charles Schwab, CBO’s (Congressional Budget Office) April 9, 2018 Report: The Budget and Economic Outlook: 2018 to 2028, FactSet.

In a “be careful what you wish for” mode, economic growth has recently picked up alongside inflation. The former is great for Main Street, which may feel better than Wall Street this year. But it also means the Fed will continue to normalize interest rates; and could do so at a stepped-up pace this year and next. This would cause debt service to increase sharply, which in turn would likely cause growth to ease and the window to narrow between now and the next recession. Total domestic nonfinancial debt is nearly $50 trillion, meaning a one percentage point increase in interest rates equates to nearly $500 billion in additional debt service costs. Perhaps this will be accompanied by higher savings and less debt, which would improve the country’s balance sheet, but that may be a tall order

Important Disclosures:

The information provided here is for general informational purposes only and should not be considered an individualized recommendation or personalized investment advice. The investment strategies mentioned here may not be suitable for everyone. Each investor needs to review an investment strategy for his or her own particular situation before making any investment decision.

All expressions of opinion are subject to change without notice in reaction to shifting market conditions. Data contained herein from third-party providers is obtained from what are considered reliable sources. However, its accuracy, completeness or reliability cannot be guaranteed.

Examples provided are for illustrative purposes only and not intended to be reflective of results you can expect to achieve.

SIFMA is a member-driven trade association that represents a broad spectrum of the capital and financial markets.

©2018 Charles Schwab & Co., Inc. All rights reserved. Member SIPC.

© Charles Schwab

Read more commentaries by Charles Schwab