Boston - Recent posts from the diversified fixed income team have discussed how bond investors should be prepared to navigate a market that may look very different from what they've grown used to. In other words, it might be time to reassess the old bond-investing playbook.

The markets are in the throes of transition -- in fact, several transitions. These shifts will occur over various periods of time: short term, medium to long term, and long term.

Here, we'll introduce some of these important shifts. Future posts will delve deeper into specific themes that point to a new regime in the bond market, and why investors may not have to view a secular rise in interest rates as the ultimate headwind for fixed income.

Indeed, there are many challenges facing fixed-income investors now. But two of the most important include how to plot a course through rising interest rates, and how shifting correlations may change the role of bonds in an overall portfolio allocation. I believe it's safe to say that many portfolio managers haven't faced the type of environment we may be moving into.

Handoff from monetary to fiscal policy

The transition from monetary policy to fiscal policy falls in our "short-term" bucket of important bond market transitions.

The immediate challenge for investors is to understand that global central banks are now ending the period of monetary stimulus. The Federal Reserve and other central banks want to get back to normal after a decade of supporting markets and economies with quantitative easing (QE).

This means rate hikes and shrinking central bank balance sheets. In this complacent landscape, it is difficult to imagine why rate moves higher would be anything other than gradual. Except that valuations in the bond markets are stretched. Therefore, the old playbook of reaching for yield by lengthening duration and going down in credit quality may not work as well as in the past.

Now, governments are trying to pick up the slack with fiscal stimulus such as lower taxes and infrastructure spending. We believe this will add to volatility and uncertainty because politicians are much less predictable than central banks clearly telegraphing their moves to markets. Also, there really isn't a playbook for fiscal stimulus this late in the economic cycle.

It's unprecedented to see fiscal stimulus this late in the cycle when the economy is relatively healthy. However, it is needed to drive growth and help close the inequality gap. But what will be the unintended consequences? It's not clear if politicians will be able to implement fiscal stimulus. But it is clear that politicians generally have less fear of inflation than central bankers.

Return killer: Inflation is percolating

With so little inflation in the economy, many investors seem to think the battle against inflation has already been won. We think that inflation is percolating and is a significant headwind against return for bond investors, particularly in developed markets.

In the U.S., investor expectations of inflation over the next five years have been moving higher since the beginning of 2016. The five-year break-even inflation rate, measured by the yield difference between nominal and inflation-linked Treasurys, has climbed above 2%, which is the Fed's target. Can it rise more from here? I think it can.

The labor markets in the U.S. are the tightest they've been in nearly 20 years. The unemployment rate is now 3.8% and there are now more job openings than people looking for work. We are seeing shortages for low-skilled and highly skilled workers. Companies have essentially two choices. They can accept lower profits to pay workers more, or raise prices to offset rising wages. Companies can typically raise prices in a healthy economy because the feedback loop with higher incomes generates more demand, which allows companies -- but not all -- to raise prices. The result is inflation.

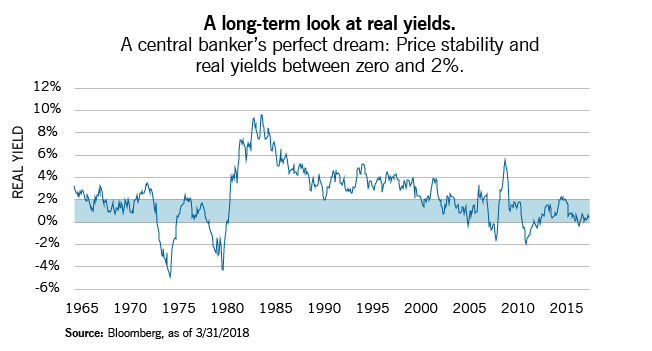

Inflation is a bond killer because it can push real yields into negative territory, as happened during the 1970s and shown in the figure below. The absolute level of rates is now so low that a pick-up in inflation will eat away at real returns, and they are already too low to meet many investors' long-term objectives.

Safe havens?

I believe rising inflation, rate normalization and extreme valuations will open the door for new strategies to protect against challenging returns. The "safe havens" where global investors tend to flock during volatility are the U.S. dollar and U.S. Treasurys. The dollar benefits from its status as the world's reserve currency, but King Dollar's reign looks more uncertain than ever.

The U.S. seems to be looking inward, and fiscal looseness, political uncertainty and rising inflation could weigh on the dollar. At the same time, more economies around the globe are strengthening and competing for investor assets (one reason why we are upbeat on emerging markets). We see opportunities in bonds denominated in currencies other than the U.S. dollar. Growing emerging nations will be issuing more sovereign and corporate debt to build out their capital markets and enlarging the global universe of bonds.

The expected long-term return for U.S. Treasurys is around 2%. Regarding Treasurys, the risk is fairly clear cut -- rising interest rates. In particular, Treasury bonds may not provide stability when risker assets such as stocks hit some turbulence. The first quarter of 2018 is a case in point, when Treasurys and U.S. equities both experienced negative performance.

Bottom line: If we are in a big regime change, then investors may need to adapt their approach and consider how bonds complement the rest of their portfolio. For example, bonds may not provide the diversification to equities that they have in the past. Also, investors may need to consider additional sources of return in order to beat the impact of rising inflation. I believe flexibility and experience will be important for fixed-income managers to navigate conditions that we haven't seen in a long time.

© Eaton Vance Management. All rights reserved.

© Eaton Vance

Read more commentaries by Eaton Vance