Three reasons why high yield has performed well in past rising rate environments

US interest rates have defied market expectations in recent years, staying historically low despite solid economic growth. But in the last year, and especially the last few months, rates have started to climb. The 2-year Treasury currently yields 2.58% compared to 1.92% at the start of the year and 1.31% a year ago.1 The 10-year Treasury yield has breached 3.0% in recent days, compared to 2.46% at the start of the year and 2.34% a year ago.1 What do these rate moves mean for high yield investors?

High yield has done well during periods of rising rates

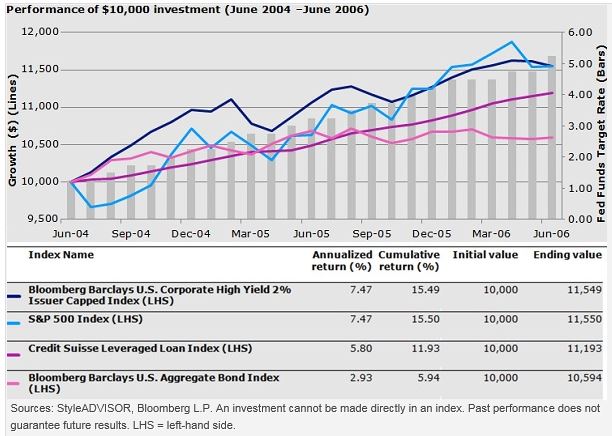

High yield bonds performed well in the last rate-hiking cycle in the mid-2000s, and we at Invesco Fixed Income expect similar performance in the current cycle (Figure 1).

Figure 1: High yield vs. equities, leveraged loans, and investment grade bonds

High yield performed well during the rate hikes of the mid-2000s

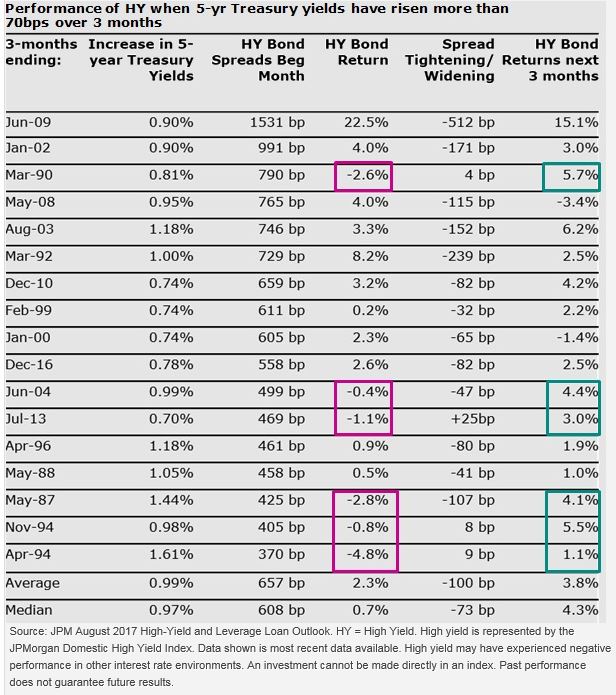

Looking further back, there have been 17 quarters since 1987 when yields on the 5-year Treasury note rose by 70 basis points or more (Figure 2). In 11 of those quarters, high yield bonds demonstrated positive returns. In the six quarters when high yield bond returns were negative (highlighted in pink), the asset class rebounded the following quarter (highlighted in green). In our view, it is reassuring that high yield bonds have performed positively in past periods of rising rates and in the months afterward.

Figure 2: High yield performance in periods of rising rates

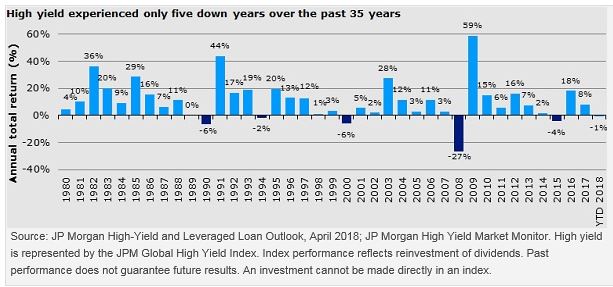

In fact, in the past 35 years, the high yield bond asset class has only experienced negative annual returns in five calendar years (Figure 3).

Figure 3: High yield market historical returns

Why has high yield done well in rising rate environments?

There are three reasons why rising rates by themselves may not be bad for most high yield bonds:

- Normally, rates rise as the economy is expanding. The expanding economy typically generates more profits for most companies and, with increased profits, companies may better service their debt. In this type of environment, we typically see lower or declining default rates and potentially tightening credit spreads.

- High yield bonds may offer call protection. When rates rise, issuers often refinance their debt before rates go higher. If an issuer refinances its debt before maturity, it normally pays a penalty (call price) that varies between 102 and 105. This pre-payment penalty is added to the returns of the high yield bond.

- The duration of high yield bonds is typically lower compared to investment grade bonds due to the comparatively short maturities and high coupons of high yield issues. For example, the Bloomberg Barclays U.S. Corporate High Yield Index has a modified average duration of 3.99 years, compared to 7.24 years for the Bloomberg Barclays U.S. Corporate Investment Grade Index.2

Key takeaway

As high yield investors, we are aware of duration risk and the volatility associated with interest rate movements. We believe that rising rates are not only associated with potentially improving fundamentals among high yield issuers, but also create opportunities for experienced active managers with an understanding of multi-cycle investing and a well-defined credit analysis process.

Investors interested in funds that invest in high yield bonds may want to consider Invesco High Yield Fund.

1 Source: US Department of the Treasury, data as of May 15, 2018, Jan. 2, 2018, and May 15, 2017.

2 Source: Barclays, as of May 21, 2018

Scott Roberts, CFA®

Head of High Yield Investments

Scott Roberts is Head of the High Yield team for Invesco Fixed Income.

Mr. Roberts joined Invesco in 2000 as a high yield analyst and was named portfolio manager in 2009. Previously, he was a high yield analyst and trader with Van Kampen Investment Advisory Corp. He entered the industry in 1995.

Mr. Roberts earned a BBA degree in finance from the University of Houston. He is a CFA charterholder.

Shawn Pope

Quantitative Analyst

Shawn Pope is a Quantitative Analyst with the Multi-Sector Macro team within Invesco Fixed Income. In this role, he focuses on building various quantitative macro models predicting inflation, gross domestic product growth and other economic indicators; researching riskpremia factors in credit; and creating systematic strategies research infrastructure.

Mr. Pope joined Invesco in 2013 as a fixed income risk analyst. He previously served as an analyst at Cambridge Systematics.

Mr. Pope earned BS and MS degrees in civil engineering from the Georgia Institute of Technology. In addition, he earned an MS degree in quantitative and computational finance from the Georgia Institute of Technology.

Important information

Blog header image: Sergey Molchenko/Shutterstock.com

The Bloomberg Barclays U.S. Corporate High Yield 2% Issuer Capped Index is an unmanaged index that covers US corporate, fixed-rate, noninvestment-grade debt with at least one year to maturity and $150 million in par outstanding.

The Bloomberg Barclays U.S. Corporate High Yield Index is an unmanaged index considered representative of fixed-rate, noninvestment-grade debt.

The Bloomberg Barclays U.S. Corporate Investment Grade Index is an unmanaged index considered representative of publicly issued, fixed-rate, nonconvertible, investment-grade debt securities.

The Bloomberg Barclays U.S. Aggregate Bond Index is an unmanaged index considered representative of the US investment-grade, fixed-rate bond market.

The Credit Suisse Leveraged Loan Index represents tradable, senior-secured, US-dollar-denominated, noninvestment-grade loans.

The S&P 500® Index is an unmanaged index considered representative of the US stock market.

The JPMorgan Domestic High Yield Index is an unmanaged index of high yield fixed income securities issued by developed countries.

The JP Morgan Global High Yield Index is designed to mirror the investable universe of the US dollar global high yield corporate debt market, including domestic and international issues.

A basis point is one hundredth of a percentage point.

Modified duration measures the rate of change of price with respect to yield.

Fixed income investments are subject to credit risk of the issuer and the effects of changing interest rates. Interest rate risk refers to the risk that bond prices generally fall as interest rates rise and vice versa. An issuer may be unable to meet interest and/or principal payments, thereby causing its instruments to decrease in value and lowering the issuer’s credit rating.

Junk bonds involve a greater risk of default or price changes due to changes in the issuer’s credit quality. The values of junk bonds fluctuate more than those of high quality bonds and can decline significantly over short time periods.

The risks of investing in securities of foreign issuers can include fluctuations in foreign currencies, political and economic instability, and foreign taxation issues.

This does not constitute a recommendation of any investment strategy or product for a particular investor. Investors should consult a financial advisor/financial consultant before making any investment decisions. Invesco does not provide tax advice. The tax information contained herein is general and is not exhaustive by nature. Federal and state tax laws are complex and constantly changing. Investors should always consult their own legal or tax professional for information concerning their individual situation. The opinions expressed are those of the authors, are based on current market conditions and are subject to change without notice. These opinions may differ from those of other Invesco investment professionals.

All data provided by Invesco unless otherwise noted.

Invesco Distributors, Inc. is the US distributor for Invesco Ltd.’s retail products and collective trust funds. Invesco Advisers, Inc. and other affiliated investment advisers mentioned provide investment advisory services and do not sell securities. Invesco Unit Investment Trusts are distributed by the sponsor, Invesco Capital Markets, Inc., and broker-dealers including Invesco Distributors, Inc. Each entity is an indirect, wholly owned subsidiary of Invesco Ltd. PowerShares® is a registered trademark of Invesco PowerShares Capital Management LLC, investment adviser. Invesco PowerShares Capital Management LLC (PowerShares) and Invesco Distributors, Inc., ETF distributor, are indirect, wholly owned subsidiaries of Invesco Ltd.

©2017 Invesco Ltd. All rights reserved.

What might rising rates mean for high yield bonds? by Invesco