Weekly Market Summary

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSummary: US equities are up two months in a row and positive for the year. They are outperforming the rest of the world, despite ongoing Quantitative Tightening here and QE abroad. In the past few days, the Nasdaq has joined the small cap indices at new all-time highs. With expanding breadth momentum and a solid macro backdrop, the outlook for (still rangebound) large caps is positive.

The upcoming weeks could test investors' resolve. Options expiration, an FOMC rate decision, the DPRK Summit and weak mid-June seasonality are all on deck for next week. The early June gap ups in SPX are very likely to fill.

US equities rose for a second month in a row in May. SPX gained 2.5%, NDX gained 5.7% and small caps gained 6.1%.

Increased volatility has given 2018 has the feel of disappointment, but YTD, SPX is up 2.5% and NDX is up over 11%. Enlarge any chart by clicking on it.

US equities are handily beating foreign equities so far this year. This is despite the fact that the US Fed has been engaged in Quantitive Tightening (QT) since late last year while the central banks in Europe and Japan are still easing. This is not a surprising outcome (a post on this is here; chart below from Bespoke, here).

Our longer term view remains that US equities are in a bull market and that new highs lie ahead in 2018.

Small cap stocks made new highs in May. Yesterday, both the Nasdaq Composite (COMPQ) and Nasdaq 100 (NDX) made new highs. The Nasdaq usually leads the broader large cap indices, meaning SPX is likely to follow to new highs as well.

NDX is currently trading outside its upper Bollinger Band (bottom panel) and momentum is "overbought" (top panel). That makes this a key test: if the uptrend is now reasserting itself, NDX will grind higher, as it did several times in 2017. Uptrends remain overbought. On any weakness the rising 13-ema (green line) should be support. Holding the 7000 area is the main watch out.

The odds favor the breakout holding. When COMPQ makes a new high this time of year for the first time in more than 2 months, the index has a strong propensity to continue higher, gaining a median of nearly 3% and 5% in the next 1 and 2 months, respectively. Risk/reward is heavily skewed long (from Sentiment Trader; to become a subscriber (and support the Fat Pitch), click here).

That, again, is favorable for large caps. The SPX outperforms (blue line vs pink line) whenever NDX is pushing higher ahead of SPX (from Quantifiable Edges, here).

For its part, SPX is still, objectively, in a consolidation/trading range. The next big battle to the upside is at 2780-2800, a level it has tried to breach just once since plunging through it February 1st. This week's R2 is at 2780. Holding support in the 2680-2700 area is key short term.

The 2700 area is an important marker longer term as well. For the third week in a row, SPX has defended its rising 20-weekly MA (blue line). SPX has a strong tendency to trend higher above this moving average (and to be choppy and corrective below it). The weekly MACD is close to a positive cross, another sign the uptrend is reasserting itself (lower panel).

Breadth is confirming the move higher in price. The Summation Index crossed above 500 last week after having been negative earlier this year (lower panel). During the past 20 years, when this has occurred while SPX was above its 200-dma, the index has subsequently made a new expansion high. This does not preclude near term weakness (see 2010 and 2011), but it does corroborate the longer term trend.

Longer term sentiment indicators favor upside as well. Retail accounts at TD Ameritrade added to their equity holdings by just a small amount in May. This was the first uptick in 2018 (after heavily selling in the prior 4 months), and suggests that investors have been slow to embrace the recovery in equities since their lows in February and March.

A final point: positive technicals are supported by solid macro economic data. Unemployment claims are at a 49 year low; home sales are growing at a 12% annual pace; even durable goods orders are up 9% in the past year. High yield spreads are falling and default rates are well below average (from JP Morgan).

It's true that equity prices typically fall ahead of the next recession, but several macro indictors weaken even earlier and help distinguish a 10% correction (like we have already seen in 2018) from an oncoming bear market. Right now, none of these indicators is hinting at an imminent recession (two recent posts on this are here and here).

Keeping a focus on the longer term is important. The best way to trade the market in the short run is to have a good idea where it's most likely to go in the long run.

But the upcoming weeks could test investors' resolve.

Next week, the FOMC will meet and likely decide to raise the federal funds rate for a 7th time since 2015. Now, the most important fact to remember is that since 1981, the NYSE has peaked after the last rate hike of the cycle. Rates are relatively low and the Fed sees growth ahead (so does the bond market). This a good combination for equities.

But the post-hike reaction hasn't been immediately bullish after 5 of the last 6 hikes. Disentangling the rate decision from concurrent events is hard, but a rally into next week could be a 'sell the news' event.

That might be especially the case this time as the North Korean summit is also next week. An anticipated good result from the meeting could be sold. A bad result would be worse.

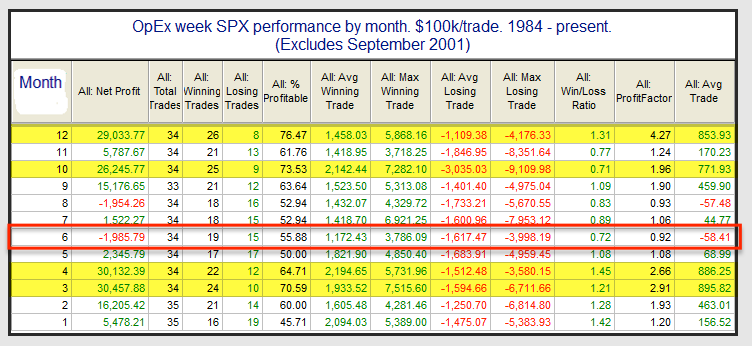

Options expiration week is also next week. June OpX has poor risk/reward, one of the worst of the year (from Quantifiable Edges, here).

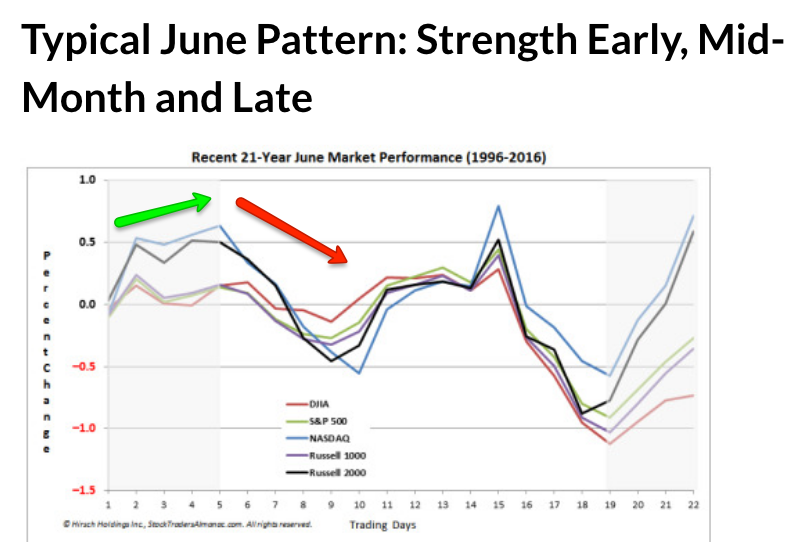

On top of all this, after a strong start, seasonality in mid-June is typically weak. The gains tend to occur in the first and last weeks, with a swoon in the middle (from the Stock Almanac).

Then, there is this remarkable statistic: since 1970, the low in June has always been below (or equal to) the close in May. June started with two unfilled gap ups, on Friday and Monday. This implies that SPX is likely to fill those gaps during the next few weeks and trade down to at least 2705 (equal to 270.9 in SPY; from Steve Deppe, here).

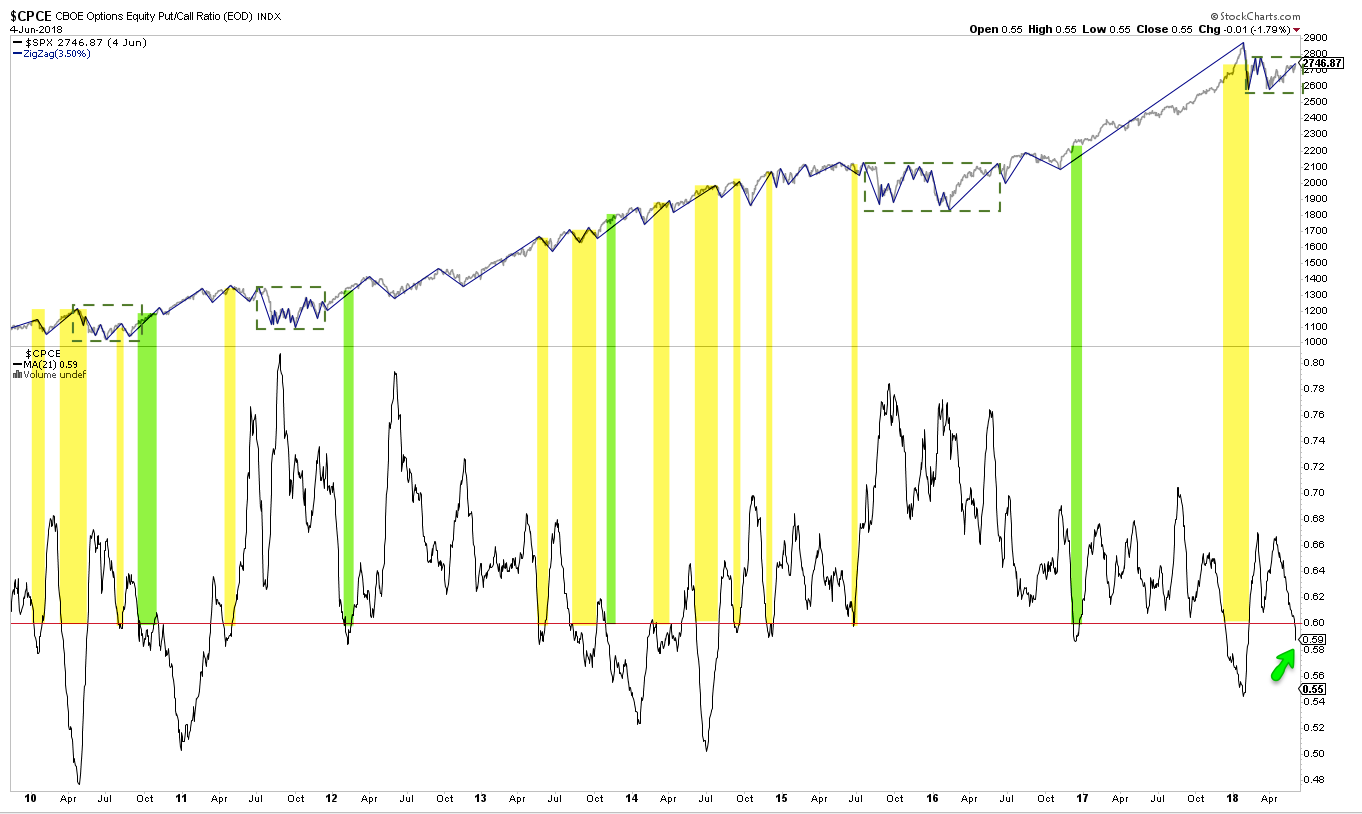

Lastly, investors have been heavy equity call buyers (relative to puts) over the past one month. The ratio is now extended (lower panel). In general, this has led either to lower equity prices or, if prices move higher, to those gains being given back in the weeks ahead (yellow shading). This is not a very precise timing tool. One important caveat is that when equities are emerging out of a notable low (like in 2010, 2011 and 2016; dashed boxes), SPX has continued higher unabated (green shading). That latter circumstance would appear to apply to now.

Backtesting this ratio over the 5 years (n=10), the win-rate for SPX over the next week has been poor (only 36% were higher). That would correspond to all of the other factors potentially impacting equities in the next week. Importantly, win-rates 2 and 4 weeks later are fine (70%; backtest engine from Sentimentrader).

In summary, US equities are up two months in a row and positive for the year. They are outperforming the rest of the world, despite ongoing Quantitative Tightening here and QE abroad. In the past few days, the Nasdaq has joined the small cap indices at new all-time highs. With expanding breadth momentum and a solid macro backdrop, the outlook for (still rangebound) large caps is positive.

The upcoming weeks could test investors' resolve. On the upcoming calendar: CPI and the DPRK Summit on June 12; the FOMC meeting concludes on June 13; retail sales on June 14; industrial production and June OpX on June 15.

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All