Life after Brexit

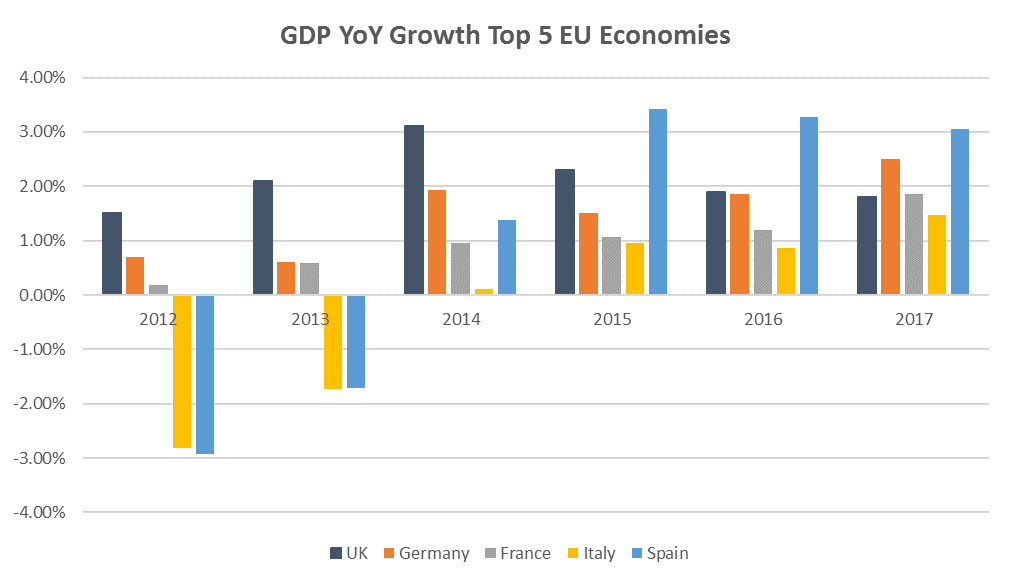

In the first three months of 2018 the British economy grew at its slowest pace in more than five years, making it the worst performer among the European Union’s (EU) largest economies. .

Those figures should come as no surprise since after all, the country has done nothing but shoot itself in the foot (twice) over the past two years. Starting in June 2016, when David Cameron’s Brexit referendum backfired and a year later when his successor Theresa May lost her majority in parliament after a snap election. A stagnant economy sounds about right….right?

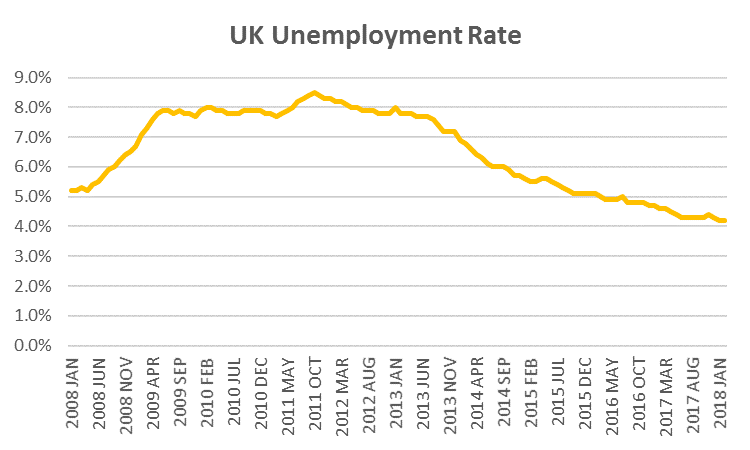

From June 2016 to December 2017, the United Kingdom (UK) economy performed fairly well,keeping up with most of its EU peers despite being at a more mature economic cycle. In terms of employment, the country not only maintained its ultra-low unemployment rate (4.2%) but alsoadded 560,000 jobs, bringing income inequality to a 30-year low. How many countries in Europe and around the world wouldn’t want these numbers?

Source: Office for National Statistics

Source: Office for National Statistics

Almost two years after the vote, Brexit-fueled fears about the UK collapsing economically, politically and monetarily have remained just that—fears and theories. In reality international companies have not fled the country and foreign investment has not disappeared. While banks may have threatened to relocate to cities like Frankfurt and Paris, the actual impact of job losses in the City moved from an expected 100,000 to an almost insignificant 3,000.

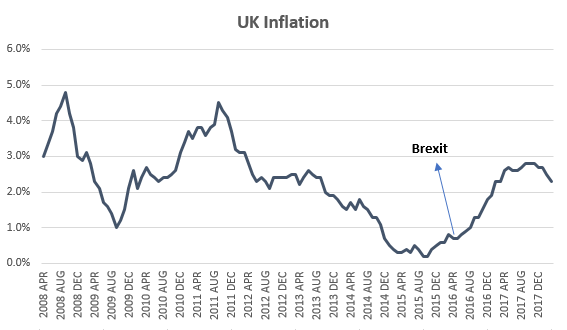

One prediction that did come true was the devaluation of the British pound, but the effect on the economy was mixed. On the one hand, a weaker Sterling made British goods less expensive to outsiders and exports more competitive, thus, reducing the trade deficit. Retail sales alsobenefited from thousands of tourists flocking to the UK to take advantage of the favorable exchange rate. On the other hand, the higher cost of imports resulted in pricing inflation for British consumers, hurting domestic consumer spending.

Source: Office for National Statistics

What has changed in 2018?

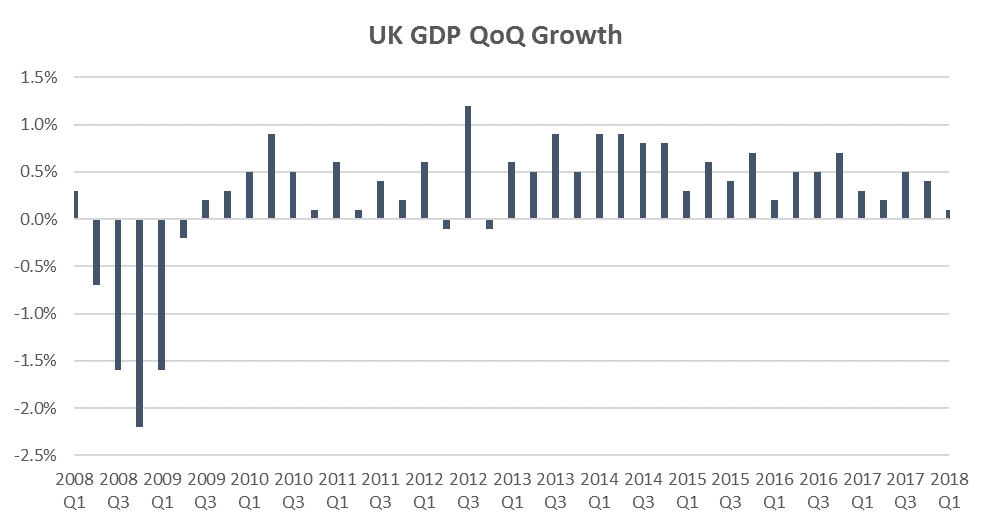

The first quarter of 2018 tell a completely different story. GDP growth was barely positive +0.1%, the slowest pace since the fourth quarter of 2012, and below consensus forecast of +0.3%. A -3.3% decline in construction activity, a weak manufacturing sector and weak consumer spending were some of the drivers of the sharp deceleration.

And so the question becomes, was Q1 a “one-off” or is this environment here to stay? Chancellor of the Exchequer Phillip Hammond, the UK’s equivalent of the Secretary of the Treasury, believes in the former. He attributed the poor results to freezing weather in February and March. Is he right? Is Mother Nature the one to blame?

On paper, he appears to be correct. After many years of subdued wage growth, a tight labor market is finally pushing income growth above inflation, while price inflation is also starting to show signs of stabilization. These should be the right ingredients to boost consumer spending....right?

Source: Office for National Statistics

Wrong again. April data (and Spring weather) did not live up to expectations. Consumers appeared to sharply cut back on borrowing, possibly driven by the Bank of England’s monetary tightening and the low savings levels seen in 2017. As a result, household expenditure contractedtwo percentage points from a year earlier (the eleventh month of decline of the past 12 months) while retail sales saw the largest fall since 2005 with a 4.2% decline.

Structural shifts in the retail industry are certainly not helping. Brick and mortar spending declined 5.5% YoY while online spending continues to grow at high double-digit levels, to the detriment of traditional retailers.

Worryingly, if household spending levels continue at this pace, 2018 could mark the worst annual performance since 2012.

On the industrial side, things did not improve either. Activity in UK factories grew at the slowest rate in 17 years and the UK’s manufacturing Purchasing Managers Index came in below the March number.

Productivity concern

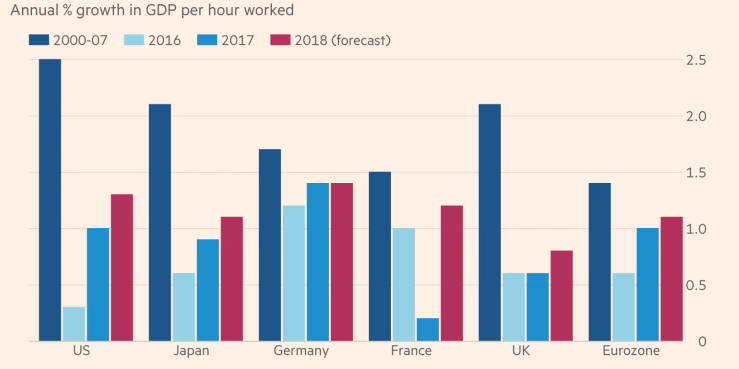

Could it be that Britain’s lack of productivity is finally taking its toll on the economy? During the 10-year period before the financial crisis of 2008, productivity growth averaged a best in class 2%, but fast forward 10 years and productivity has fallen behind leading economies such as the US, Japan and France. To put this in context, output per hour worked in Germany is more than a quarter higher than in the UK.

No one knows exactly why this is happening but some argue that the causes might be connected to the country’s dependence on financial services, an ultra-loose monetary policy, and low capital investment.

Source: Financial Times, The Conference Board Total Economy Base

The good news

Auto sales—a good proxy for the state of an economy—are starting to turn the corner. In April,passenger vehicles sales increased +10.4%, a significant improvement versus the 12% decline of posted in Q1.

Over the past month, the FTSE 100 (a leading economic indicator) outperformed the DAX, CAC, FTSE MIB, IBEX, and the S&P 500, signaling investors’ confidence on the UK’s outlook, despite Brexit uncertainty.

More questions

Is Britain starting to feel the impact of its decision to leave the European Union? Is the economic slowdown the result of normal economic cycles (or just bad weather)? Are there some hidden secular trends that are driving the country’s underperformance? These are some of the questions economists will be asking themselves in the coming months. Will they get it right this time? Only time will tell.

© Morse, Towey & White Group at HighTower

Read more commentaries by Morse, Towey & White Group at HighTower