- Roman Roulette

- New Businesses Needed

Governmental instability is not a new experience for Italy; the country has had 64 governments since the end of World War II. In the 1970s, Italians were terrorized by the Brigate Rosse, a leftist group that killed a former prime minister and sought to remove Italy from the North Atlantic Treaty Organization. More recently, former prime minister Silvio Berlusconi (whose appetite for vice was exceeded only by his appetite for power) was convicted of tax fraud and banned from holding office.

In light of that history, the drama that unfolded earlier this week should not be viewed as altogether unusual. On Monday, Italian President Sergio Mattarella prevented a prospective coalition from forming a government, as is his right under the constitution. But the reason for the denial—the potential that Italy would drop the euro—raised an uncomfortable issue that many thought had been closed.

The conditions that led to Monday’s imbroglio are not unique to Italy. The government of Spain is under renewed stress as its economy struggles to sustain momentum. The underlying issues in Europe’s periphery require a broad remedy. But the dissolution of the euro is a very remote possibility.

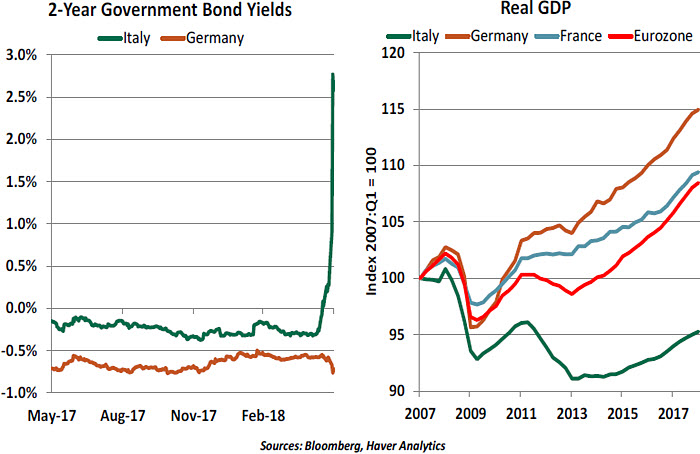

To be sure, the governance crisis in Italy came at an unfortunate time. The eurozone has been riding a nice wave of economic growth and market outperformance. Unemployment has been falling, and reform efforts were back on the table. But first-quarter results were soft, and recent headlines put a dent in investor confidence. Markets reacted angrily to Italy’s impasse, punishing Italian bonds and the euro.

While headline outcomes for the eurozone have been encouraging, conditions beneath the surface are far from perfect. Performance among member nations has been uneven; Germany has prospered, while Italy has foundered. Italy’s real gross domestic product (GDP) has yet to surpass its pre-crisis high, and its unemployment rate of 11% is one of the highest in the euro area.  Italy’s banks remain troubled, almost a decade after the onset of the financial crisis. The failure to resolve bad debts created by the recession (authorities preferred a strategy referred to as “delay and pray”) has left the country’s financial institutions poorly positioned to support economic activity. The close relationship between some Italian

Italy’s banks remain troubled, almost a decade after the onset of the financial crisis. The failure to resolve bad debts created by the recession (authorities preferred a strategy referred to as “delay and pray”) has left the country’s financial institutions poorly positioned to support economic activity. The close relationship between some Italian

lenders and their government has delayed the kind of financial rehabilitation that provided a foundation for recovery in other countries.

The lingering malaise in Italy and other Mediterranean countries provides fertile ground for populism. The movement has different forms in different places, but its supporters are united by their antipathy toward trade, immigration and multinational organizations like the European Union. Elections last year threatened to create a populist wave, but outcomes in the Netherlands, France and Germany produced conventional leaders. Markets breathed a sigh of relief.

But anti-establishment parties garnered substantial support and have a growing voice in European affairs. Until and unless the root causes of discontent are addressed, populism will remain a significant force in regional and global politics.

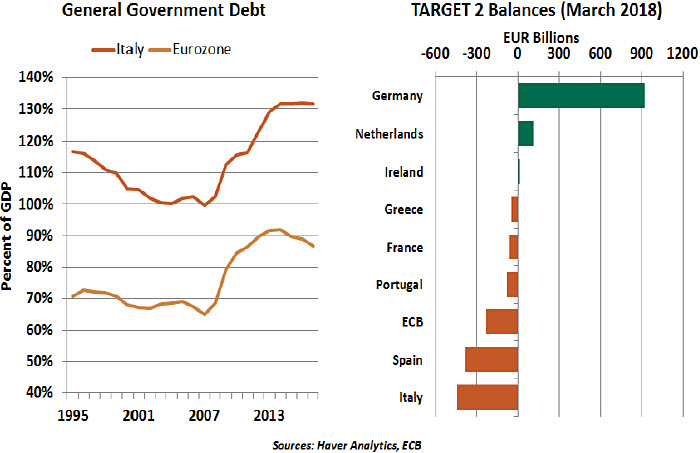

Italy is especially vulnerable, given its political history and the crushing weight of the national debt. Government borrowing totals more than 130% of GDP, and Italy’s central bank has a substantial deficit to its eurozone counterparts through the eurozone’s payment system (known as “TARGET2”). There is no clear path to bringing either situation under control.

The euro has been described as a marriage with no potential for divorce. Procedural steps for a departure do not exist. But Paolo Savona, the gentleman who was originally designated to become Italy’s next finance minister, had apparently developed a playbook to achieve separation.

One wonders if that playbook includes the wide range of adverse consequences that would ensue from such a step. There would almost certainly be a default on Italian debt and stress on the eurozone payment system. Italian banks would be cut off from international funding and capital markets, leading to widespread failures. The new lira would be a weak currency; while that would promote Italian exports, most economists anticipate that negative effects would dwarf this benefit. The Italian economy could be in ruins for quite some time.

Syriza, the Greek populist party, was elected in 2015 on a platform of economic confrontation with Germany and the eurozone more generally. But its leaders were forced to capitulate after the realities of international finance became painfully apparent. Italy is not Greece, for a number of reasons. But the lesson is instructive nonetheless. Once you peer over the cliff, you may decide not to jump.  And that may be what motivated a settlement in Italy at the end of the week. The populist coalition agreed to appoint a more conventional finance minister, who is (at least outwardly) more supportive of remaining in the eurozone. The new government was approved on Thursday. Markets calmed, but will have to await the direction that Italy’s new

And that may be what motivated a settlement in Italy at the end of the week. The populist coalition agreed to appoint a more conventional finance minister, who is (at least outwardly) more supportive of remaining in the eurozone. The new government was approved on Thursday. Markets calmed, but will have to await the direction that Italy’s new

leadership chooses.

It will be very interesting to see what comments Mario Draghi, president of the European Central Bank (ECB), offers on this subject after the next ECB meeting on June 14. The ECB had dropped a reference to downside risks in its official statement and seemed on track to end its asset purchase program before the end of the year. But renewed uncertainty in Italy may extend the effort by some months. And Draghi must avoid appearing to be overly partisan.

It has been a volatile few days, and more may follow. The Italian flair for the dramatic could keep the situation in the headlines for some time. But eurozone leaders have shown the will and the capacity to defend their common currency. And if an existential threat arises, we believe that it will be dealt with effectively.

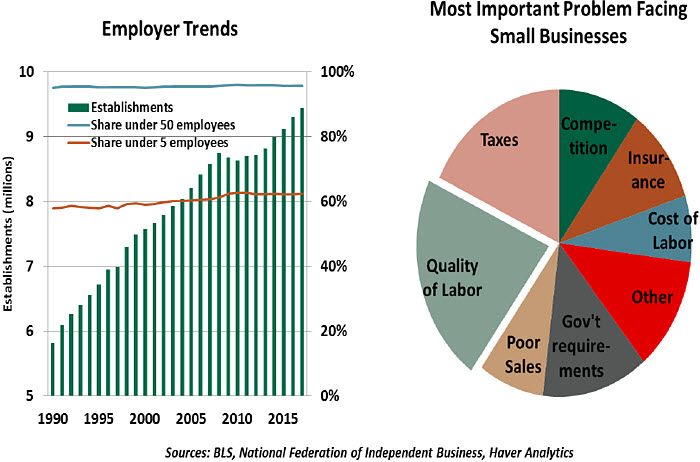

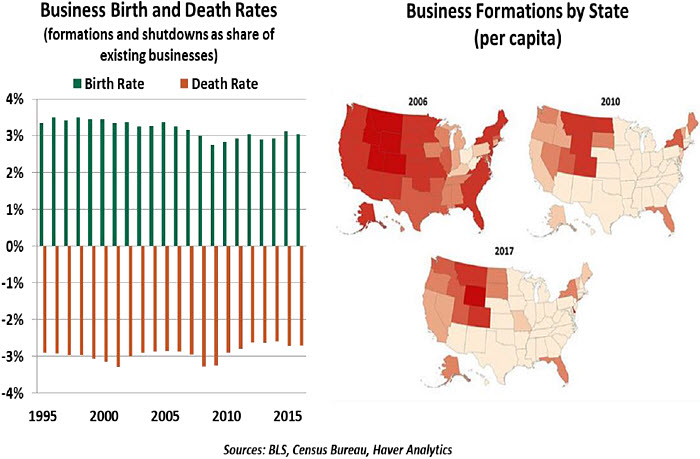

Once new ideas have demonstrated their potential to become viable businesses, they launch and grow. This is the economically crucial moment at which they may take on employees. New firms that hire people create jobs and broaden the tax base. New businesses serve as a fountain of youth for an economy, creating continued employment

Once new ideas have demonstrated their potential to become viable businesses, they launch and grow. This is the economically crucial moment at which they may take on employees. New firms that hire people create jobs and broaden the tax base. New businesses serve as a fountain of youth for an economy, creating continued employment

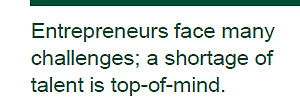

Despite the competitive forces, today’s small business owners are optimistic. The National Federation of Independent Business (NFIB) monthly survey of economic trends has, for the past year, shown greater optimism and less uncertainty. When small business owners were asked in the most recent survey to select the greatest challenge they face, the

Despite the competitive forces, today’s small business owners are optimistic. The National Federation of Independent Business (NFIB) monthly survey of economic trends has, for the past year, shown greater optimism and less uncertainty. When small business owners were asked in the most recent survey to select the greatest challenge they face, the