Massive investor popularity can produce some pretty strange circumstances in the U.S. stock market. Mark Twain said, “History doesn’t repeat itself, but it rhymes!” Today’s strange occurrence has been called a “zero cost of capital” and it rhymes with what happened in 1999-2000. This is a phrase coined by NYU Business Professor, Scott Galloway, in his effort to explain the moat surrounding today’s tech darlings. What is a “zero cost of capital” and why does it exist today? How long might it last and does it guide us as long-duration investors on where to place our capital?

What is a zero cost of capital?

Normally, publicly traded businesses are subject to a significant price to raise capital to fund their growth. If you borrow money, the interest rate is the cost of capital, combined with being obliged to pay it back at maturity. If you sell common stock, you dilute the share of future profits for existing shareholders. A simplistic way to think about the cost is the inversion of the company price-to-earnings ratio (P/E). As a back of the envelope exercise, a company trading at a P/E of 10 would spend 10% to issue new shares.

All of this has been brought to light by a terrific piece on The Wall Street Journal website called, “Bull Market in Tech-Company Convertible Debt Rages On.” Writer Maureen Farrell tell us that today we have the most publicly-traded convertible bonds in existence paying little or zero interest since the year 2000. Here is how she explains this rhyme:

Publicly traded technology companies have been issuing bonds that convert into equity at a pace unseen since the height of the dot-com bubble as demand for tech stocks surges.

So far this year, 24 U.S. technology companies have issued $11 billion of convertible bonds, the highest volume in a comparable period since 2000 and 29% above the already-elevated level of 2017, according to Dealogic.

For those of you who need refamiliarization with the instrument, companies raise capital either via issuing common/preferred stock, selling bonds, or by selling hybrid bonds called converts. Investors collect interest on these bonds and at some point in the future they have the right to convert the bonds into common shares. Her article goes on to say:

Three— Nutanix Inc., RingCentral Inc. and Etsy Inc. —have issued convertible bonds this year that pay no interest. Since the dot-com crash, such deals have been relatively rare. Only 13 other companies had issued convertible bonds without coupons since then.

When you borrow money by selling bonds which are paying no interest and are only convertible into equity at much higher prices, you effectively provide those companies capital which costs nothing! Galloway argues that extremely high P/E ratios on stocks like Amazon (AMZN), Tesla (TSLA) and Netflix (NFLX) implies a nearly zero rate for them. A 200 P/E multiple inverts to an interest rate of 0.5%.

Why does zero cost of capital exist today?

The most obvious reason for the low cost of capital is the historically low interest rates of the last ten years. Bonds and stocks both took their cues from the alternative U.S. treasury interest rates. Even with the low interest rates established by the government, up and coming companies pay junk bond interest rates to borrow in the public market. Using Tesla as a recent example, their common stock trades at an infinite P/E ratio because they are losing money. Their junk bonds are rated CCC+, were issued to yield 5.3%, and trade underwater at 87 cents on the dollar.

Smead Capital Management believes the next reason is that we are in a classic financial euphoria episode as described in John Kenneth Galbraith’s, A Short History of Financial Euphoria. As described in his book, investors are suffering from what is called “recency bias.” Once a trend lasts long enough, investors extrapolate the trend way out into the future based on momentum. Here is how Galbraith explains it:

Let the following be one of the unfailing rules by which the individual investor and, needless to say, the pension and other institutional-fund manager are guided; there is the possibility, even the likelihood, of self-approving and extravagantly error-prone behavior on the part of those closely associated with money.

Galbraith explains that those who pursue the trend are grouped as two kinds of participants. One group is made up of supposedly smart people who buy in and are ready to leave with one foot out the door. The second group are less experienced investors who feel pioneering and empowered by being alive when common men and women anticipate getting rich.

Remember that Warren Buffett says, “What the wise man does at the beginning, the fool does at the end.” Galbraith says it this way:

A further rule is that when a mood of excitement pervades a market or surrounds an investment prospect, when there is a claim of unique opportunity based on special foresight, all sensible people should circle the wagons; it is time for caution.

How long might a zero cost of capital exist?

Judging by Maureen’s article, not much longer:

The surge in convertible debt worries some investors who see a bubble developing at a time when there are signs the multiyear bull market in stocks has run its course. But that has yet to damp demand.

And tech companies are even more bullish on their own stocks.

They’re betting they will eclipse the level at which the companies have agreed to convert shares during the bonds’ life, which is usually five years. Most of the tech companies that have issued convertible debt this year have paid for a “call-spread overlay,” a derivative that typically increases the price at which shares convert to double the starting price. The cost of these derivatives is steep—between 5% and 10% of proceeds, bankers and issuers estimate—but they reduce the risk of dilution that conversion triggers.

What should long-duration investors do with this information?

First, we have a saying in our company which goes back to 1999 when the last big episode of “zero cost of capital” happened: “When there is going to be a hurricane in Miami, you don’t want to be in Palm Beach.” We believe investors should avoid high P/E and popular tech-related companies which are tied in some way to the current episode.

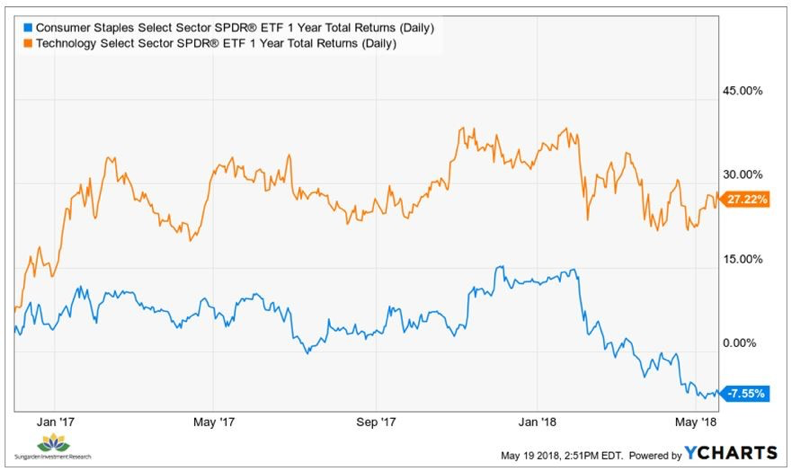

Second, look at history. In the chart below, you can see the last time that “zero cost of capital” companies sucked in most of the capital, while the most reliable staple companies saw their capital get sucked out. Our look at history comes to us thanks to a recent article by Rob Isbitts from Sungarden Investment Research. This shows how much tech dominated staples in 2000:1

Here is what is going on today:1

Third, do what the Mafia does when it makes an investment. The Mob demands very attractive terms, because nobody else wants to invest in the project (usually because it is an illegal activity). The wise long-duration investor looks to buy into sectors, industries and companies which most investors are afraid to buy. Investors are afraid to provide capital to companies which compete with the “zero cost of capital” companies.

In today’s market this means buying into retailers when commentators on CNBC call them “un-investable.” We like Target (TGT) and Nordstrom (JWN), which sell at attractive P/E multiples, gush free cash flow and pay over 3% in dividends. It means buying Walgreens (WBA) at 10.5 P/E, while staples are getting slugged by the tech mania. Lastly, nothing seems more hated than the television and cable industries. The cost of capital for Discovery Communications (DISCA) is 10% at a 10 P/E and we believe the company’s earnings and free cash flow should grow immensely in a world of “zero cost of capital” companies.

In conclusion, strange things do happen in the stock market and occasional “zero cost of capital” manias seem to rhyme. We like to say that the stock market will do whatever it needs to do to frustrate the most people. We believe many unsuspecting common stock investors are caught in this mania via passive indexes and sector exchange-traded funds. Caveat emptor (Buyer Beware)!

Warm regards,

William Smead

1Source: "These 2 S&P Sectors Tell a Very Dot-Com-Like Story" Published on May 24, 2018 by Rob Isbitts, Co-Founder and Chief Investment Officer at Sungarden Fund Management.

The information contained in this missive represents Smead Capital Management's opinions, and should not be construed as personalized or individualized investment advice and are subject to change. Past performance is no guarantee of future results. Bill Smead, CIO wrote this article. It should not be assumed that investing in any securities mentioned above will or will not be profitable. Portfolio composition is subject to change at any time and references to specific securities, industries and sectors in this letter are not recommendations to purchase or sell any particular security. Current and future portfolio holdings are subject to risk. In preparing this document, SCM has relied upon and assumed, without independent verification, the accuracy and completeness of all information available from public sources. A list of all recommendations made by Smead Capital Management within the past twelve-month period is available upon request.

© 2018 Smead Capital Management, Inc. All rights reserved.

This Missive and others are available at www.smeadcap.com

Follow us on Twitter @SmeadCap