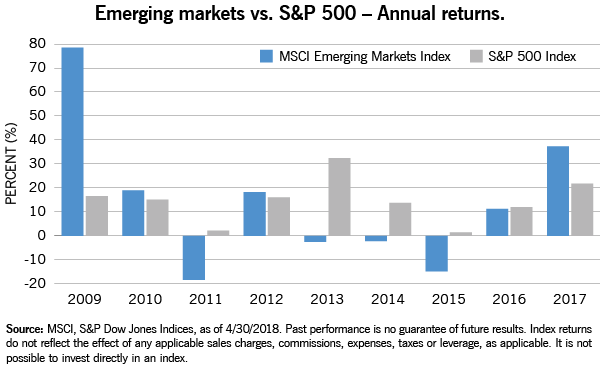

London - Emerging market (EM) stock indices have generally trailed the S&P 500 Index in the years after the financial crisis, although developing markets handily outpaced the U.S. in 2017.

The performance shift last year had some investors wondering if the pendulum is ready to swing back and favor EMs in coming years. After all, the alternating leadership of EMs or the U.S. tends to move in multiyear cycles.

So far in 2018, EMs have lagged. However, we think giving up on an EM allocation to equities would be a mistake due to their diversification benefits, earnings growth, relative valuations and other factors.

That said, EM equities have faced several headwinds so far in 2018, including rising U.S. Treasury bond yields, a resurgent U.S. dollar, concerns over the potential for a U.S.-China trade war and increasing geopolitical risks.

Digging deeper, markets that are most sensitive to global liquidity tightening have had it the worst in 2018 -- Turkey, Indonesia and South Africa. In Turkey, rising oil prices and the announcement of early parliamentary and presidential elections, to be held in June, also increased uncertainty. Russia was negatively impacted by the announcement of new U.S. sanctions in response to "malign activity across the globe," according to Treasury Secretary Steven Mnuchin.1

However, EM valuations relative to the U.S. look attractive. The recent weakness has brought EM equities back under their 10-year average price-to-earnings (P/E) and price-to-book (P/B) ratios. Meanwhile, profitability is relatively healthy among EM corporates.

From this, we infer the market is worried that profits will be impacted by potential trade wars and armed conflicts. These events are hard to accurately predict, but it is clear that underlying economic fundamentals are strong in both developed markets and EMs at present, and the earnings outlook is good.

Of course, it is possible that trade and military tensions escalate from here. Yet based on the fundamentals, we have a positive outlook for EM equities in general. In other words, we think the current fears about EM equities are overblown, and present buying opportunities.

Bottom line: We believe the opportunity in EM stocks has strengthened given the recent price correction, and may persist. Positive factors include a supportive macro environment, improving corporate margins and attractive valuations. EMs are increasingly home to companies at the cutting edge of innovation, particularly in the technology sector. These companies tend to exhibit a higher return on equity (ROE) and are now seen as quality, value-adding and sustainable businesses -- rather than venues for "risk-on, risk-off" trades.

1"What to Know About Trump's New Sanctions Against Russia," Time Magazine, April 6, 2018.

Investing involves risk including the risk of loss. Investing in foreign securities involves additional risks relating to political, social, and economic developments abroad; differences between the regulations that apply to U.S. and foreign issuers and markets; the potential for foreign markets to be less liquid and more volatile than U.S. markets; and currency risk associated with securities that trade or are denominated in currencies other than the U.S. dollar. The risks of investing in emerging market securities can be greater than those of investing in securities of developed foreign countries.

© Eaton Vance

© Eaton Vance

Read more commentaries by Eaton Vance