Weighing the Week Ahead: Will Higher Interest Rates Lead to Lower Stock Prices?

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsThe economic calendar is light, and the market week will be shortened. There is no holiday this week, but expect many participants to take off early for a long weekend. If interest remain above 3% on the ten-year note, that will be the focus. Pundits will be asking:

Will higher interest rates lead to lower stock prices?

Last Week Recap

In my last edition of WTWA I suggested that the week lacked a dominant theme. That part was right. I took the occasion to discuss which stocks might benefit from Trump policy changes. While few pundits took up the topic, it was still a useful exercise for me, and I hope for my readers as well.

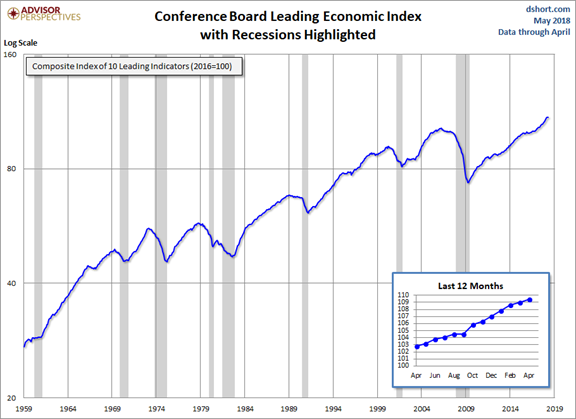

The Story in One Chart

I always start my personal review of the week by looking at a great chart. I especially like the version updated each week by Jill Mislinski. She includes a lot of valuable information in a single visual. The full post has even more charts and analysis, including commentary on volume. Check it out.

The market declined about 0.6% with a trading range of only 1.5%. This is the quietest week we have seen in a long time. I summarize actual and implied volatility each week in our Indicator Snapshot section below. As you can see, volatility has been moving lower, and is back into the long-term range.

Personal Note

Mrs. OldProf and I will be enjoying an extended holiday next weekend, so there will not be the regular WTWA installment. I’ll try to update indicators if possible. She is in withdrawal in the absence of football of any sort. She was watching some wedding on TV when I asked her for a comment.

Thanks to the Intelligent Economist for once again including me among the Top 100 Economics Blogs. Most readers know that my labor of love is fueled by the knowledge that people find the work useful.

Noteworthy

From the Visual Capitalist, where you can also see prior years for comparison.

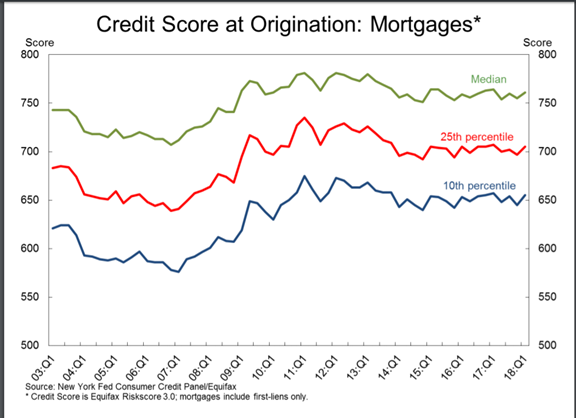

And, some updated information on debt from the NY Fed (HT GEI). The report also has information about various types of debt levels over time along with related credit scores.

The News

Each week I break down events into good and bad. For our purposes, “good” has two components. The news must be market friendly and better than expectations. I avoid using my personal preferences in evaluating news – and you should, too!

Feel free to add items that I have missed. Please keep in mind that we are looking for current news, especially from the last week or so. WTWA is not about long-term concerns like debt. These are important, of course, but not our weekly subject unless there has been some major change.

The overall picture remains positive. Economic strength is reasonable, and inflation is low. New Deal Democrat’s analysis of high-frequency indicators shows some deterioration but retains the overall outlook.

Both the nowcast remains and the short term forecast remain positive.

The long term forecast has deteriorated further, with interest rates and money supply now both generally negative. Only the continued strength in housing and credit are keeping me from switching this from positive to neutral or even negative.

The Good

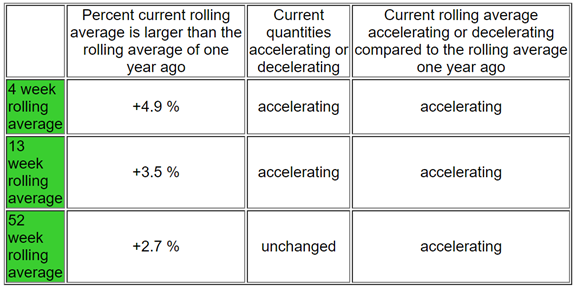

- The rail traffic growth cycle continues. Steven Hansen (GEI) does the best deep dive into this series, using his “intuitive sector” approach, rolling averages, and year-over-year comparisons. Here is just one of his summary tables and charts.

- Industrial production increased 0.7% in April slightly beating expectations and matching the upwardly-revised report from March. See Calculated Riskfor charts and analysis.

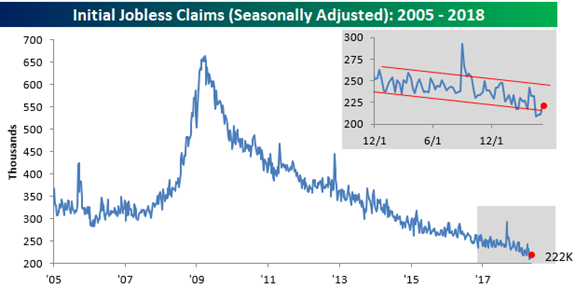

- Initial jobless claims while rising somewhat to 222K, continued lower on the less-noisy four-week moving average. Bespoke observes, “With this week’s reading of 222K, the four-week moving average dropped to 213.25K. That’s a new low for the cycle, the century, and all the way back to December 1969!”

- Leading indicators matched expectations of 0.4% and the upwardly revised 0.4% from March. (Jill Mislinski)

- Port traffic improves on both imports and exports. Steven Hansen’s (GEI) analysis suggests that the implications are stronger for global economic growth than for the U.S.

- Improvement in the US/China trade talks? Politico covers the progress, described as “positive, constructive, and fruitful” by the Chinese government.World-Grain.com reports that China has dropped sanctions against U.S. sorghum. China is the largest destination for U.S. sorghum exports. It remains difficult to get an accurate read on the progress.

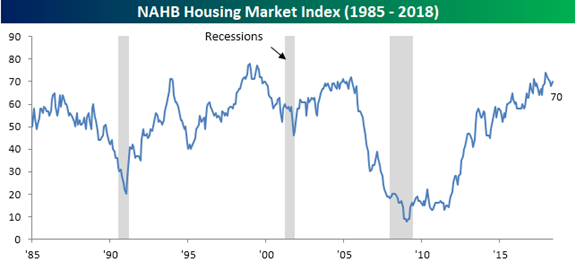

- NAHB index registered 70, a slight gain over April and beating expectations of 69. (Bespoke)

The Bad

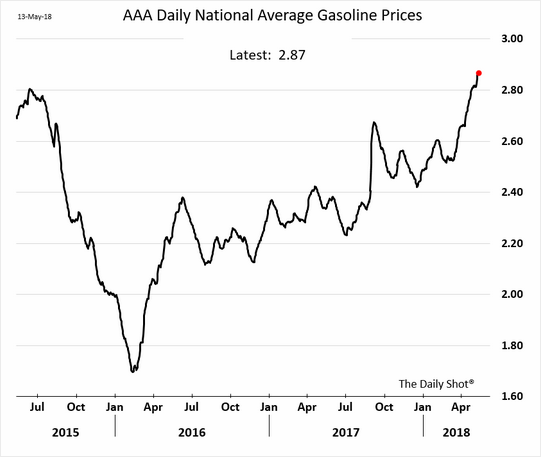

- Oil and gasoline prices move higher. The WSJ quotes Morgan Stanley estimates that gasoline at $2.96 would take an annualized $38 billion from spending elsewhere. That is about a third of the additional take-home pay from the tax cuts.

- Housing starts declined to a SAAR of 1287K, down 3.7% and missing expectations of 1325K. Building permits were in line with expectations. Calculated Risk provides analysis and charts. Bill also notes the volatility in multi-family and the continuing “wide bottom” in single-family starts. This long-standing prediction has been quite accurate.

- Mortgage rates reached a seven-year high. (Calculated Risk)

The Ugly

Santa Fe, Texas. I understand that more people die from other causes, including terrorism around the world. These high school massacres are different. Senseless. Innocent young people. A familiar environment that we all expect to be safe.

The Week Ahead

We would all like to know the direction of the market in advance. Good luck with that! Second best is planning what to look for and how to react.

The Calendar

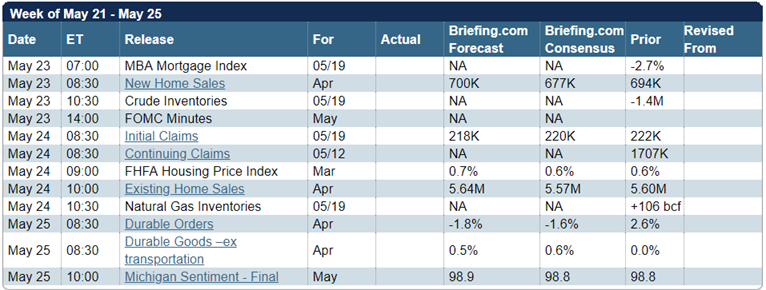

The economic calendar is light. Home sales data are most important, and many will pay careful attention to the FOMC minutes. Many participants will be taking off early to extend their holiday weekend.

Briefing.com has a good U.S. economic calendar for the week (and many other good features which I monitor each day). Here are the main U.S. releases.

Next Week’s Theme

Without much news and a quiet week on tap, it is an open field for the punditry. Home sales and the FOMC minutes will get some attention. If interest rates do not move any lower I expect many to be asking:

Do higher interest rates imply lower stock prices?

There are a few clear-cut positions.

- Interest rates have broken to new levels and may move much higher. Brian Gilmartin covers this angle.

- Don’t fight the Fed!

- Interest rates will lead to a strong dollar and lower earnings.

- Three steps and a stumble.

- It is just a return to normalcy. (Eddy Elfenbein)

As usual, I’ll save my overall personal conclusions for today’s Final Thought.

Quant Corner

We follow some regular featured sources and the best other quant news from the week.

Risk Analysis

I have a rule for my investment clients. Think first about your risk. Only then should you consider possible rewards. I monitor many quantitative reports and highlight the best methods in this weekly update.

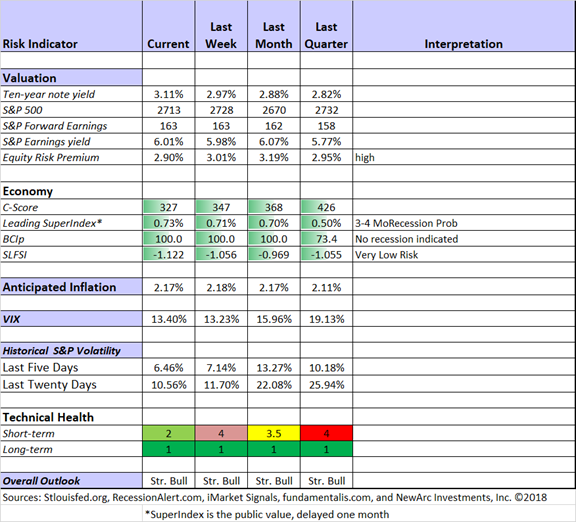

The Indicator Snapshot

Short-term trading conditions improved dramatically. Despite the recent borderline ratings suggesting “bad weather” it was not quite enough to take us out of the market. A strength of our modeling approach (Thanks, Vince!) is a touch more patience than shown by many technical systems. This has a mild cost, and can reap great rewards, as it has in the last few weeks.

A notable feature of the chart is that we recently increased the nine-month recession odds to a chance of 25%. While this is significantly higher than it has been during the long stock rally, it does not yet represent a real threat. Instead of thinking of the odds as higher than before, we must keep in mind the continuing evidence that a near-term recession is unlikely. The odds are only slightly higher than the long term average.

That said, we watch this quite closely and plan to reduce position sizes if the risk grows much larger.

The Featured Sources:

Bob Dieli: Business cycle analysis via the “C Score.

RecessionAlert: Strong quantitative indicators for both economic and market analysis.

Brian Gilmartin: All things earnings, for the overall market as well as many individual companies.

Georg Vrba: Business cycle indicator and market timing tools. None of Georg’s indicators signal recession.

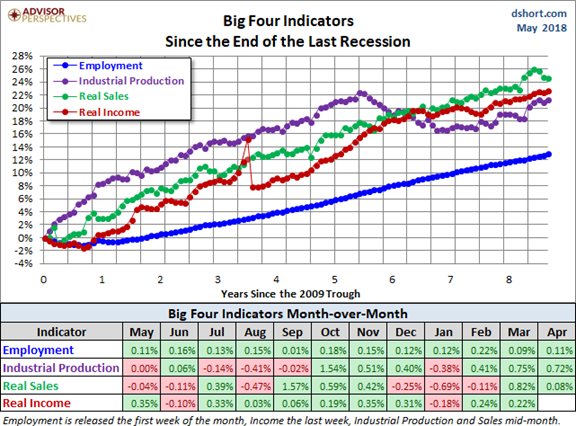

Doug Short and Jill Mislinski: Regular updating of an array of indicators. Great charts and analysis. With some crucial updates on the most important indicators, it is time for an update of their extremely helpful Big Four.

The post-January sea of green is impressive. If only we could highlight this for all the individual investors bombarded with the incessant flow of perma-bear negativity. These are not forecasts; they are facts from an objective source.

Guests:

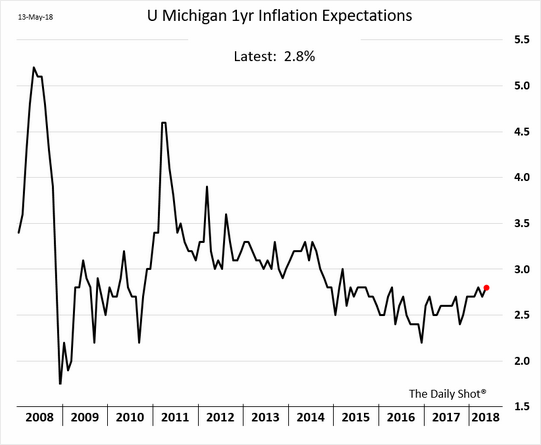

Like us, James Picerno tracks the market-implied inflation expectation.

The Daily Shot takes note of consumer inflation expectations from the University of Michigan sentiment survey, a bit higher than the market verdict.

Bill McBride explains the importance of seasonal adjustments for employment data.

The Dallas Fed (via GEI) reports that consumers respond more to negative news than positive info. This is a nice analysis of the asymmetric reaction to shocks, with a discussion of policy implications.

When do recessions accompany stock market corrections? David Rice has both an interesting approach and some useful conclusions.

Insight for Traders

Check out our weekly Stock Exchange post. We combine links to important posts about trading, themes of current interest, and ideas from our trading models. This week we asked fellow traders if their rules were too rigid.

As usual, we included varying expert opinions and a comparison with our trading models. We also discussed some stock ideas and updated the ratings lists for Felix and Oscar, this week featuring the Russell 2000. With lue Harbinger on a European jaunt (business, he insists) we were delighted that earnings expert and investment manager Brian Gilmartin was able to offer his view of the various ideas.

While I emphasize trading in the Stock Exchange series, it often has implications for long-term investors. It is worth a visit.

Insight for Investors

Investors should have a long-term horizon. They can often exploit trading volatility.

Best of the Week

If I had to pick a single most important source for investors to read this week it would be Lloyd Clucas’s colorful and accurate description of the current investment landscape. To get the setting, please consider some facts from this week’s Barron’s cover story about Jack Bogle. The story covers a lot of interesting and controversial ground, but I was drawn to this factual statement:

Bogle fears that ETFs are purely speculative, encouraging selling at the bottom and buying at the top. Bogle shared his analysis of dollar-weighted investor returns, which accounts for money flows, with Barron’s. The research shows that from 2005 to 2017, the average investor return from “Traditional Index Funds” was 8.4%. For actively managed funds, it was 7.2%. For ETFs, it was 5.5%, even worse than actively managed funds. That contains the seeds of the category’s demise. “How long are investors going to be happy with that? Sure if you double your money, why would you complain? But you could have tripled it. I am glad we continue to be primarily on the TIF horse, and not the ETF horse.” He also foresees that growth in ETFs will slow because “an awful lot of [market] niches have been populated.” Next up, “a lot of ETFs will go out of business along the way.”

The key takeaway is that individual investors do worse than they would by merely holding some asset. How could this happen?

I cannot do justice to Lloyd’s article with one quote, but here is a taste:

The media-driven issue of the day is virtually always misleading. Ignore all of them. If you insist on watching CNBC, be sure to leave the sound off. Leave it off unless you actually know the person is worth listening to. Of course that usually requires years of experience – not just your emotional preferences. Leave the latter to your evening cable show watching. And leave it entirely out of your investment decision-making.

There is no euphoria or even complacency in the U.S. equity market today. Rather, it is clear to me that investors are scared. The VIX doesn’t tell you what you might think it does. If it explodes over 40, it is worth looking at in conjunction with other psychological indicators. Recent public interpretations of it are preposterous. Bond funds have drawn ridiculous sums from individual investors. The Wall of Worry is huge.

As one who watches financial television with TIVO and mute, and who knows the players, I fully understand this description.

Please read the rest of the post for more valuable insights.

Stock Ideas

Individual investors seeking high-quality research on their stock holdings and ideas already use the many resources at Seeking Alpha. Just in case you are not following the Today’s Editors’ Picks series, take a look. You will definitely find ideas that you would otherwise have missed.

Chuck Carnevale discusses blue chip Johnson & Johnson (JNJ), asking “What can I expect to make if I invest today?” As usual, he combines a lesson about how to analyze a stock with a specific idea and conclusion. Take time to watch his video.

Blue Harbinger has a good record trading Prospect Capital (PSEC) and he has a new call.

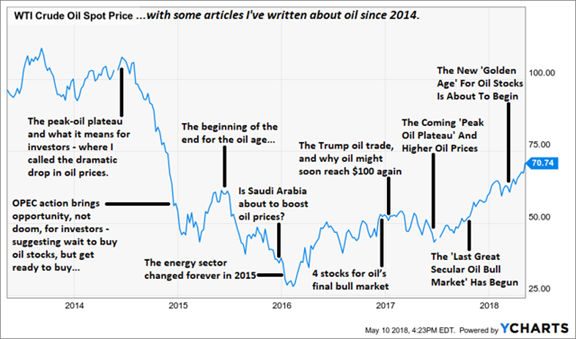

Energy stocks? Kirk Spano has had some winning ideas in the sector and still sees room to run. He suggests a “New Golden Age” for oil stocks. Check out his post for the full discussion and some ideas for how to play possible strength.

Target (TGT) might be at an attractive value point. D.M. Martins Research argues that the top line growth will be fine, although year-over-year comparisons will remain tough for a few quarters.

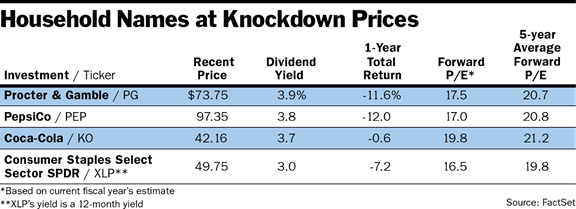

Consumer staples bargains? Barron’s takes a look.

Airline stocks? Southwest or others? Stone Fox Capital analyzes the choices. You probably cannot guess which is cheapest on a forward PE basis.

Chip stocks? Peter F. Way applies his unique methods to consider the risk and reward for the entire sector. We own one of the stocks listed, and I was quite eager to see where it was in his chart.

Aerospace and defense stocks? Peter F. Way takes on this sector as well. I am considering some candidates, and my own methods yield similar results.

Closed-end funds? Stanford Chemist has a first-rate method and covers this space carefully. Many buyers merely look for discounts without considering the risks. He provides an interesting list of choices, using various important criteria.

A high-potential REIT? Dividend Sensei has a pick that has both yield and upside.

Stone Fox Capital makes the case for Baidu – “Another Gift.”

Market Outlook

Avondale Asset Management covers earnings calls by reviewing transcripts and presentations. This is an excellent source for those of us wondering whether economic growth is reflected in corporate profits. This week’s report highlights overall optimism, solid growth, a strong labor market, and a CEO expectation that the business cycle could continue for several more years. They love tax reform but are feeling pricing pressures from capacity limits and oil price increases.

Personal Finance

Seeking Alpha Senior Editor Gil Weinreich has expanded his excellent series for financial advisors (and serious individual investors) to include some podcasts. This week I especially enjoyed his thoughtful and kind commentary on the last installment of WTWA. Gil adds his own valuable insights and points to some great posts from other contributors. He also continued his podcast series with his take on behavioral finance questions.

Abnormal Returns is always worth reading, with many links on an array of interesting topics. Wednesday the focus is on personal finance. Among many good choices, I especially appreciated the honest account of an advisor who “botched her own RMD.” There are plenty of lessons in this post. More important for most investors is the discussion from Mullooly Asset Management, Inc on why it so often right to “do nothing.”

Watch out for…

Investments in direct general-obligation bonds from the State of Illinois. David Kotok of Cumberland Advisors explains the reasons. They are all familiar to those of us who call Illinois “home.”

Non-GAAP adjustments. Paulo Santos analyzes Symantec with the earnings controversy in mind. [Jeff – I understand the value of adjusting for one-time effects in an effort to gauge a stock’s future performance. This demonstrates why it is important to do solid research on individual stocks, with this question in mind.]

Cisco Systems? (CSCO). A good company with a valuation that is too high? (D.M. Martins)

Legalized sports betting is an interesting news story. There was the typical rush to find stocks that might benefit. Vince Martin provides an interesting contrarian analysis, the reason to measure your optimism.

Zillow? Marc Gerstein has an interesting story explaining what might go wrong with the business model.

Final Thoughts

I had the great honor and privilege last week to share my thoughts with a group of top executives and financial experts from Chicago and southern Wisconsin. They were very sharp both in conversation and in their questions. My comments were centered on the noise from financial news and how to make sound decisions in that environment. It was a great audience and they even laughed at the right times.

Astute investors like this are already looking beyond the noise, but maybe I helped a little and provided examples for their own clients. The current interest rate story is mostly noise. The same sources that criticized the Fed for “punishing savers” with low rates are now worried about the gentle and gradual increase. There are so many who are selling something – and therefore on a mission!

Dale Roberts hits these same themes in his post, Fear Sells. But Why Are You Buying It?

He has an entertaining list of attention-grabbing headlines from the past. Apparently credible at the time, but costly to the readers.

A few simple facts will help us all keep perspective on the increase in rates.

- There is no magic point where things suddenly turn negative. Markets represent a distribution of participants with widely differing needs. A slightly higher rate will be marginally attractive to some investors. It is not like a light switch.

- It is completely normal for the ten-year note to yield 4 to 5%. This is a healthy range, consistent with solid economic growth and corporate earnings. Stocks normally move higher as rates increase into this range.

- The Fed is cognizant of the incipient inflation pressures. Their patient attitude is “at last.” They may react too late, but for investors that is a problem for some future time. Owning stocks is not “fighting” their policy shift.

And most importantly —

Do not base your investment decisions on slogans!

The pundit parrots are relying upon a handful of cases that are not really like our current market. A little more analysis is needed.

It is easy to get lost in the noise of the news, distracted from your goals and how to reach them. If that sounds familiar, send for my free paper on the Top Investor Pitfalls. Whether you are trying to preserve wealth or to build your assets, there are some great opportunities right now. If you are having trouble pulling the trigger, organizing your thoughts, or finding attractive stocks, send a note to main at newarc dot com. I have written papers on each of these topics. We will happily send some free resources and provide a consultation if you wish.

I’m more worried about:

- North Korea. The prospects for a constructive agreement fluctuates with the wind.

- Over-reaction to higher interest rates. It so easy to be seduced by catchy slogans.

I’m less worried about:

- China. While I understand the skepticism surrounding the talks, there are indications of progress.

- Technical market concerns. Those watching charts got further relief last week.

Membership required

Membership is now required to use this feature. To learn more:

View Membership Benefits