Equity volatility, the prospect of rising interest rates and an uptick in issuance may bode well for the asset class

After trailing US stocks in 2017,1 US convertible securities outperformed during the volatile first quarter of 2018. Given the prospect of further market volatility, the expectation for rising interest rates and a recent pickup in convertible issuance, the Invesco Convertible Securities team has a favorable outlook for this asset class in the near to medium term.

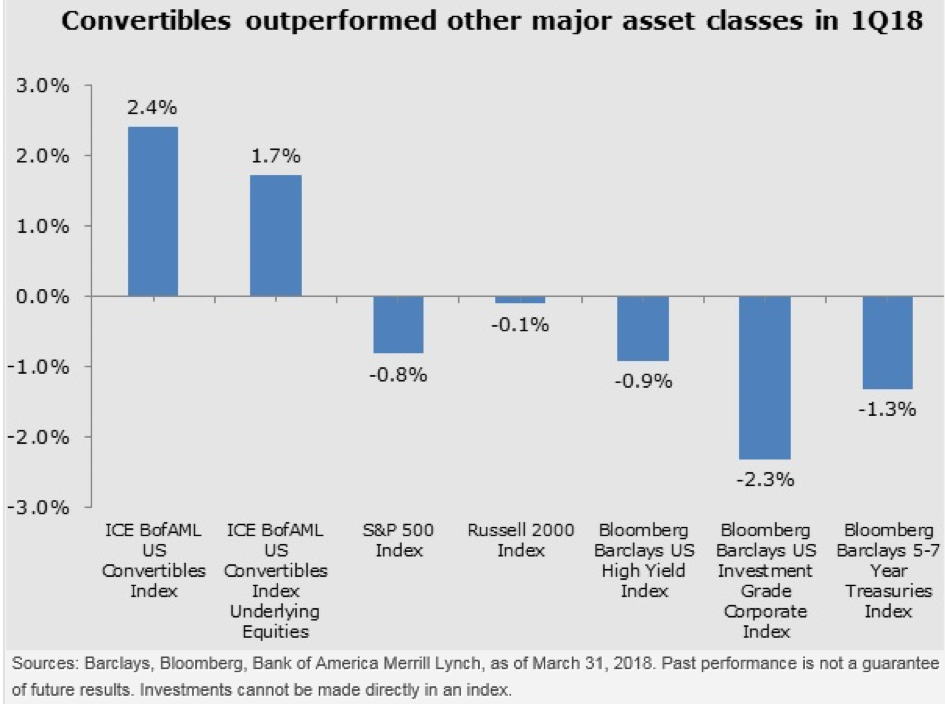

Convertibles may withstand equity volatility

A convertible security is a corporate bond that has the added feature of being converted into a fixed number of shares of common stock. Therefore, convertibles have the ability to capture some of the upside in their underlying equities. Because of their bond-like features, they may trail stocks on the way up (as we saw in 20171), but they may potentially decline only a fraction of the amount of their underlying equities in the event of a pullback (as we saw in the first quarter of 2018, illustrated in the chart below). In a highly volatile equity market — like the one we’ve experienced in recent weeks — we believe the unique qualities of convertibles may be of interest to investors.

Through the first quarter of the year, US convertible securities, as per the ICE BofAML US Convertible Index, returned 2.4%. That compares favorably to the returns of the S&P 500 Index and the Russell 2000 Index, which finished the quarter in negative territory, as well as the performance of debt categories like investment grade, high yield and Treasuries, all of which also finished the quarter with negative returns.

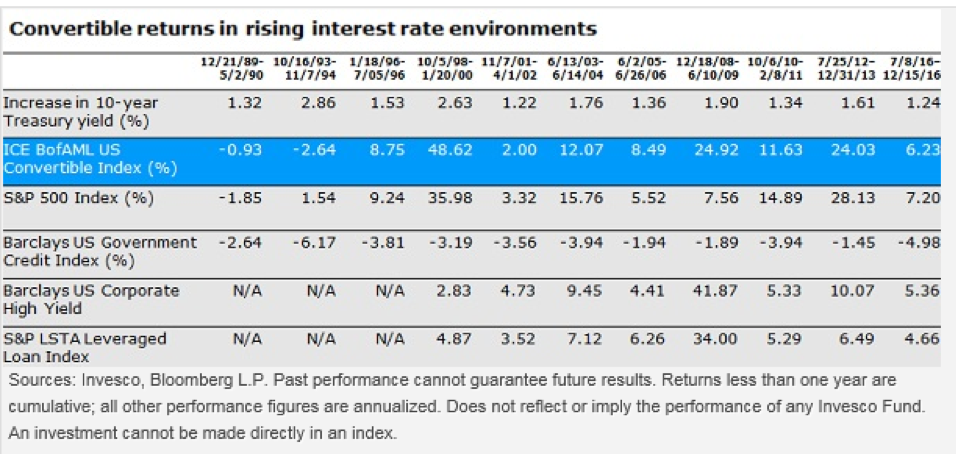

Convertibles have performed well in rising rate environments

In addition to their relatively good performance in the choppy equity market of the first quarter, the asset class has historically outperformed during periods of rising interest rates, due to their embedded equity component and their relatively short duration. (As of March 31, convertibles have a duration of less than three years on average, compared to around four years for high yield and seven years for investment grade debt).2 In fact, during the last 11 periods of time in which US interest rates rose by at least 120 basis points, or 1.2%, (going back nearly 30 years, as shown below), convertibles consistently outperformed government bonds and also outperformed high yield debt and floating rate loans in a majority of those periods.

Issuance of convertibles is rising

Also worth noting is the recent pickup in the pace of convertible issuance. In March 2018, there were 18 new convertibles issued in the US market with a principal value of more than $5 billion, compared to 11 new issues in March 2017 (approximately $4.7 billion in proceeds).3 We see this as an opportunity to be more selective in our fund’s exposures and to potentially adjust the fund’s level of exposure to moves in the underlying equities.

We see several reasons why the brisk pace of issuance could continue.

- Companies may be motivated to issue convertibles right now given the high level of volatility in stock prices, which may enhance the value of a convert’s embedded call option.

- The prospect for rising interest rates could translate into expensive terms for companies that wait to issue debt, motivating companies to issue convertible bonds sooner rather than later.

- Recent changes in the federal tax code limit the tax deductibility of corporate debt interest expense, which may lead convertibles to be viewed as a cost-efficient option for companies to consider rather than higher coupon, nonconvertible bonds.

- If interest rates do increase, converts may become cheaper to issue given what is likely to be a wider spread between coupons on nonconvertible debt compared to convertible debt, due to the call option on convertibles. This could lead larger companies with strong credit ratings to step up their issuance of convertibles.

Learn more about Invesco Convertible Securities Fund.

1 Source: Lipper. In 2017, the ICE BofAML US Convertible Index returned 13.7%, versus 21.83% for the S&P 500.

2 Sources: Bloomberg L.P., ICE Data Services/BofA Merrill Lynch. Convertibles represented by the ICE BofAML US Convertible Index.

3 Source: Barclays

Stuart Novick, CFA Senior Analyst

Stuart Novick is a Senior Analyst working with the Invesco Convertible Securities team.

Mr. Novick joined Invesco in 2014 and entered the industry in 1989. He was previously a senior credit analyst at Bloomberg, covering special situations in the Bloomberg Industries research group. Prior to that, he was a credit analyst at the Financial Times Group. Mr. Novick started in the industry in 1989 and spent 17 years at Citigroup, where he was a director in the convertible securities group.

Mr. Novick earned a BS degree from the University of Albany and an MBA from Columbia Business School. He holds the CFA designation.

Important information

Blog header image: K. van Velthuijsen/Shutterstock.com

A basis point is one hundredth of a percentage point.

The Barclays US Government Credit Index includes Treasuries and agencies that represent the government portion of the index, and it includes publicly issued US corporate and foreign debentures and secured notes that meet specified maturity, liquidity and quality requirements to represent the credit interests.

The ICE BofAML US Convertible Index is an unmanaged index that measures performance of US dollar-denominated convertible securities not currently in bankruptcy with a total market value greater than $50 million at issuance.

The Barclays US Corporate High Yield Index is an unmanaged index considered representative of fixed-rate, noninvestment-grade debt.

The S&P/LSTA Leveraged Loan Index is a weekly total return index that tracks the current outstanding balance and spread over LIBOR for fully funded term loans.

The Russell 2000® Index, a trademark/service mark of the Frank Russell Co.®, is an unmanaged index considered representative of small-cap stocks.

The Bloomberg Barclays US Corporate High Yield Index measures the USD-denominated, high yield, fixed-rate corporate bond market. Securities are classified as high yield if the middle rating of Moody’s, Fitch and S&P is Ba1/BB+/BB+ or below.

The Bloomberg Barclays 5-7 Year US Treasury Bond Index measures the performance of the US Government bond market and includes public obligations of the US Treasury with a maturity of between five and up to (but not including) seven years. Certain special issues, such as state and local government series bonds (SLGs), TIPS and STRIPS are excluded. Securities must be fixed rate and rated investment grade, as defined by the Index methodology.

The Bloomberg Barclays US Corporate Bond Index measures the investment grade, fixed-rate, taxable corporate bond market. It includes USD denominated securities publicly issued by US and non-US industrial, utility and financial issuers.

Invesco Convertible Securities Fund Risks:

Convertible securities may be affected by market interest rates, the risk of issuer default, the value of the underlying stock or the issuer’s right to buy back the convertible securities.

An issuer may be unable to meet interest and/or principal payments, thereby causing its instruments to decrease in value and lowering the issuer’s credit rating.

Derivatives may be more volatile and less liquid than traditional investments and are subject to market, interest rate, credit, leverage, counterparty and management risks. An investment in a derivative could lose more than the cash amount invested.

The risks of investing in securities of foreign issuers, including emerging markets, can include fluctuations in foreign currencies, political and economic instability, and foreign taxation issues.

Junk bonds involve a greater risk of default or price changes due to changes in the issuer’s credit quality. The values of junk bonds fluctuate more than those of high quality bonds and can decline significantly over short time periods.

Interest rate risk refers to the risk that bond prices generally fall as interest rates rise and vice versa.

Preferred securities may include provisions that permit the issuer to defer or omit distributions for a certain period of time, and reporting the distribution for tax purposes may be required, even though the income may not have been received. Further, preferred securities may lose substantial value due to the omission or deferment of dividend payments.

The Fund is subject to certain other risks. Please see the current prospectus for more information regarding the risks associated with an investment in the Fund.

This does not constitute a recommendation of any investment strategy or product for a particular investor. Investors should consult a financial advisor/financial consultant before making any investment decisions. Invesco does not provide tax advice. The tax information contained herein is general and is not exhaustive by nature. Federal and state tax laws are complex and constantly changing. Investors should always consult their own legal or tax professional for information concerning their individual situation. The opinions expressed are those of the authors, are based on current market conditions and are subject to change without notice. These opinions may differ from those of other Invesco investment professionals.

All data provided by Invesco unless otherwise noted.

Invesco Distributors, Inc. is the US distributor for Invesco Ltd.’s retail products and collective trust funds. Invesco Advisers, Inc. and other affiliated investment advisers mentioned provide investment advisory services and do not sell securities. Invesco Unit Investment Trusts are distributed by the sponsor, Invesco Capital Markets, Inc., and broker-dealers including Invesco Distributors, Inc. Each entity is an indirect, wholly owned subsidiary of Invesco Ltd. PowerShares® is a registered trademark of Invesco PowerShares Capital Management LLC, investment adviser. Invesco PowerShares Capital Management LLC (PowerShares) and Invesco Distributors, Inc., ETF distributor, are indirect, wholly owned subsidiaries of Invesco Ltd.

©2017 Invesco Ltd. All rights reserved.

Three reasons to consider convertibles now by Invesco