- Oil’s Rise

- The E.U. Has Its Own Concerns About China

- More Hours In The Week

The end of the academic year is approaching. For parents of college students, this means folding down the seats in your vehicle and driving to campus for departure day. All too often on these occasions, the “movers” arrive to find their student unprepared (and even, on occasion, fast asleep). What ensues is a frenzied few hours that involve stuffing a broad range of belongings into garbage bags for the trip back home.

These voyages use a lot of gasoline, which means trips to the filling station. On those occasions, motorists often feel as though they are pulling the arm of a slot machine. The dial spins for a while and finishes on a random outcome. Sometimes you’re happy; sometimes, you’re not.

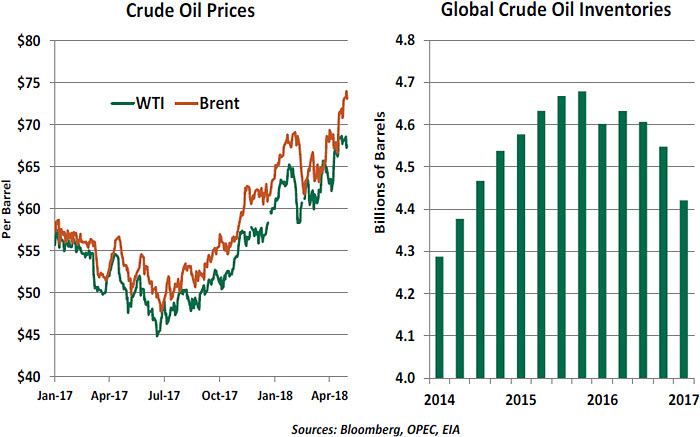

This year’s campus-homestead transitions are going to be expensive propositions. After hovering around $50 per barrel for a long while, oil prices have been rising steadily for the past six months. If the trend is sustained, it could have an important influence on global economic performance.

We last discussed oil this past October. At that time, prices were tightly range-bound. The Organization of Petroleum Exporting Countries (OPEC) was on the back foot, struggling to control its members and facing increased competition from non-OPEC providers. Global inventories were high and alternative fuels were advancing, leading key oil producers to contemplate life after petroleum.

Since then, a series of factors have conspired to push crude prices upward.

-

- Global demand has improved, thanks to accelerating growth in the United States and Europe. Vehicle ownership and usage continue to expand in developing markets (China, in particular) and shipping volumes have been rising world-wide. Global air travel continues on a sharp upward trajectory. With economic performance expected to continue growing, energy demand is unlikely to diminish.

-

- OPEC members have generally adhered to the supply reductions agreed in 2016. Production from OPEC countries and Russia has declined by about 6% since last fall; with prices rising, the cost of these restrictions has been falling. OPEC members will meet later this month to discuss renewing production ceilings, and they are widely

expected to keep the limits in place.

- OPEC members have generally adhered to the supply reductions agreed in 2016. Production from OPEC countries and Russia has declined by about 6% since last fall; with prices rising, the cost of these restrictions has been falling. OPEC members will meet later this month to discuss renewing production ceilings, and they are widely

-

- The stability of global oil supplies is a subject of concern. Venezuela’s economic collapse has hindered its production; oil workers have been leaving the country in droves, and the additives required to make its oil marketable are in short supply.

-

- Rising tensions in the Middle East, including attempted missile strikes from Yemen on Saudi oil infrastructure, could curtail production in the region. Overall, the risk premium within the price of crude has been increasing.

- Iran, whose production has been rising steadily, could be squeezed if talks over its nuclear program devolve. The White House faces a decision next week on whether to re-apply sanctions against Tehran; analysts suggest new limitations could reduce Iran’s production by 1 million barrels per day.

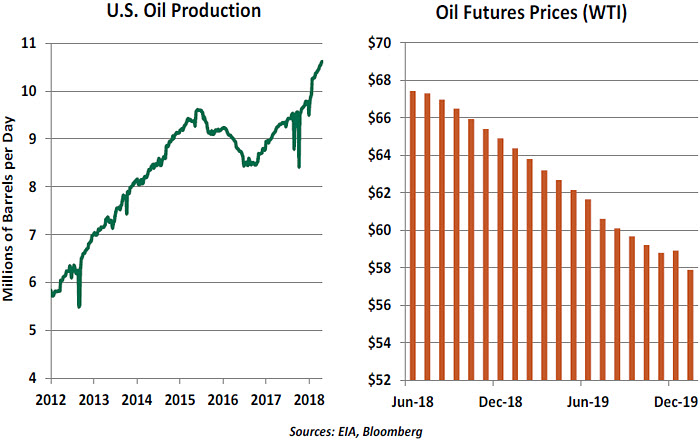

U.S. producers have responded to higher prices by opening their spigots. American output has risen by almost

1 million barrels per day so far in 2018; there are 13% more wells actively producing oil than there were last November. Analysts expected this rapid reaction, but it has not been enough to place a cap on prices.

Partly as a result of this, futures markets are anticipating that oil prices will ease in the months ahead. Contracts one year forward are priced at more than $5 per barrel less than current spot prices. This condition (called “backwardation”) may serve OPEC’s purposes very well. An outlook for lower prices may limit the expansion of U.S. production, as fields requiring higher prices to cover extraction costs may remain idle.  If oil remains expensive, it could have important effects on the global economy. Oxford Economics estimates that a rise to $85 per barrel would reduce global growth by more than 0.5% over the next two years, a substantial amount. Inflation would rise by 1% over that same interval: good for central banks trying to get inflation up to targeted levels, but bad for purchasing power in energy-consuming nations.

If oil remains expensive, it could have important effects on the global economy. Oxford Economics estimates that a rise to $85 per barrel would reduce global growth by more than 0.5% over the next two years, a substantial amount. Inflation would rise by 1% over that same interval: good for central banks trying to get inflation up to targeted levels, but bad for purchasing power in energy-consuming nations.

Any pass-through to core inflation in the U.S. could prompt the Federal Reserve to raise rates more rapidly than currently anticipated. And as we highlighted last week, oil has a powerful influence on inflation expectations. Sustained prices in excess of $65 could produce additional upward pressure on long-term interest rates.

Energy markets are notoriously difficult to forecast. So many variables can affect equilibrium, and they can shift suddenly and substantially. Experts in the field are anticipating that current prices will be sustained, but potential error around this projection is wide in both directions.

I can, however, anticipate at least one element of the energy price equation with some certainty. My collegian will undoubtedly demand automobile privileges when she returns home, which will increase our gasoline consumption considerably. To add insult to injury, she will probably be using my car. Fortunately, the walk home from the train station only takes forty minutes, and at least the price of a stroll won’t change.

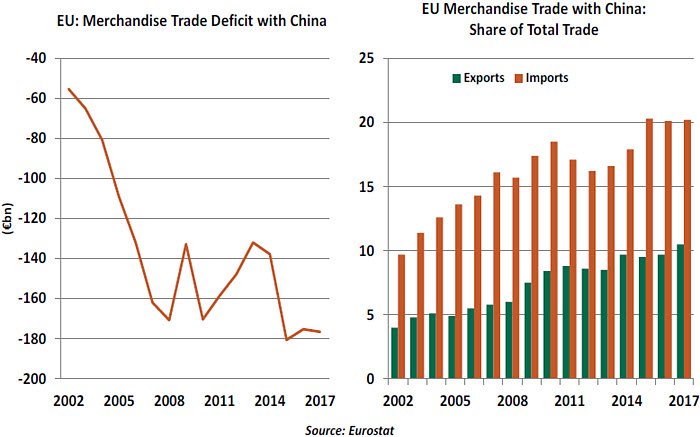

The rising trade deficit with China has caught the attention of European commissioners. As per the

The rising trade deficit with China has caught the attention of European commissioners. As per the

One explanation for this trend can be found in the part-time workforce. Some members of this group identify as part-time for economic reasons: they would prefer to work full-time but cannot find a role with sufficient hours. But not all part-time workers are necessarily seeking more hours. Some indicate they are working part-time for non-economic reasons,

One explanation for this trend can be found in the part-time workforce. Some members of this group identify as part-time for economic reasons: they would prefer to work full-time but cannot find a role with sufficient hours. But not all part-time workers are necessarily seeking more hours. Some indicate they are working part-time for non-economic reasons,