The widely quoted benchmark rate is now at post-crisis highs

The last time we wrote about the US dollar London lnterbank Offered Rate (LIBOR) was in 2016, when the spread between LIBOR and the Overnight Indexed Swap (OIS) rate increased due to market dislocations leading up to US money market fund reform. Now in early 2018, we have seen LIBOR rates rise and LIBOR-OIS spreads widen again, causing us to ask the same question — what’s up with LIBOR?

In our opinion, there are three factors driving LIBOR rates higher:

- The US Federal Reserve (Fed) has continued to push monetary policy rates higher with its latest hike in March.

- Demand has fallen for short-term credit instruments due to potential corporate repatriation following last year’s tax reform.

- Given projected budget deficits, markets expect an abundant supply of US Treasury bills (T-bills) through 2019.

What is LIBOR?

LIBOR is a benchmark rate that some of the world’s leading banks charge each other for short-term, unsecured loans.1 Globally, it is considered a primary benchmark for short-term interest rates. LIBOR is also used as a barometer to gauge market expectations of future central bank policy and for measuring the health of the banking system. As such, LIBOR rates typically increase when the Fed tightens monetary policy and/or during times of market stress.

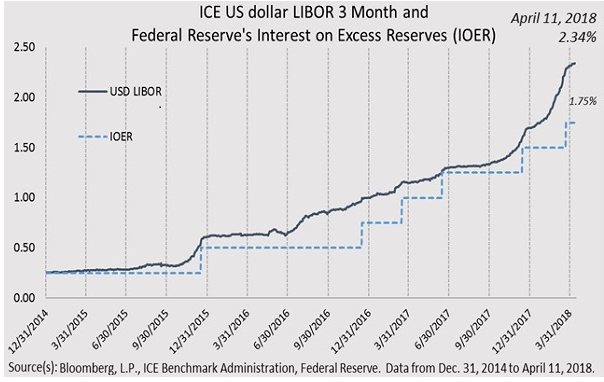

LIBOR has increased in part due to Fed policy rate hikes

The recent rise in LIBOR can be partially tied to the Fed’s removal of monetary policy accommodation. As seen in Figure 1, there has been a relatively close correlation between LIBOR and the Fed’s interest rate on excess reserves (IOER). The Fed has increased policy rates six times since 2015. Looking ahead, Invesco Fixed Income expects future Fed rate hikes to keep this trend in place.

Figure 1: Three-month LIBOR and the Fed’s IOER are Highly Correlated

What is the LIBOR-OIS spread?

The LIBOR-OIS spread is considered a key measure of investors’ perception of credit risk within the banking sector. It is the difference between LIBOR and the overnight index swap rate (OIS). OIS represents a given country’s central bank policy rate over a certain time period (the federal funds rate in the US). Unlike LIBOR, credit risk is not a major factor in determining the OIS rate.

Supply and demand have pushed the LIBOR-OIS spread wider

Current supply and demand dynamics in short-term funding markets have pushed the LIBOR-OIS spread wider. In our opinion, this is not reflective of stress or credit concerns in the banking system. This trend is similar to 2016 when assets flowed out of prime money market funds into government money market funds, disrupting supply/demand dynamics in short-term funding markets and causing the LIBOR-OIS spread to increase. Eventually, markets adjusted, banks found new sources of funding and the LIBOR-OIS spread settled down to new clearing levels (Figure 2).

Figure 2: Latest Increase in LIBOR-OIS Spread Greater than 2016

Invesco Fixed Income believes the recent increase in the LIBOR-OIS spread is due to diminished demand for short-term credit instruments, coupled with additional selling pressure created by companies seeking to repatriate and spend cash balances that are no longer “trapped” offshore. As time passes, and supply and demand adjusts, we expect the LIBOR-OIS spread to revert to lower clearing levels.

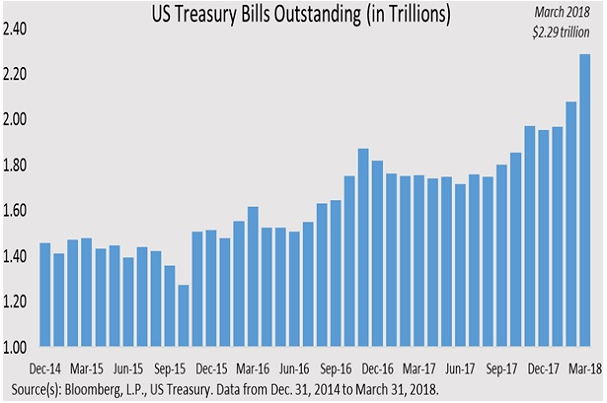

US T-bill supply higher

Adding to the technical picture is the increase in the supply of US T-bills following February’s passage of a two-year US government spending plan and the typical increase in issuance around tax season. T-bill supply was up 17% to $2.3 trillion as of March 31 (Figure 3) — an all-time high. The current abundance of T-bill supply has supported the widening of the LIBOR-OIS spread, as institutional buyers have opted for T-bills over repurchase agreements, causing T-bill yields to lag LIBOR. While T-bill supply could drop following this year’s April 17 tax deadline, we believe future US budget deficits are likely to keep overall Treasury issuance on the rise through 2018 and 2019.

Figure 3: US T-bill Supply has Increased

Who could benefit from these dynamics?

Invesco Fixed Income views the increase in LIBOR and the jump in the LIBOR-OIS spread as an opportunity. We believe short-term investment strategies may stand to benefit from higher LIBOR rates and a wider LIBOR-OIS spread.

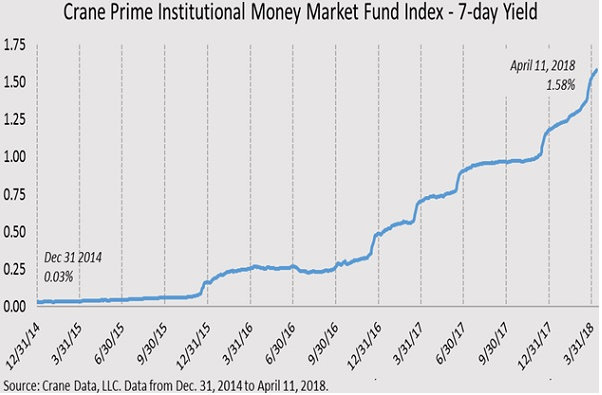

First, prime money market funds (which rely on short-term funding markets) have already benefited as yields of these types of funds have increased (Figure 4). Second, ultrashort bond funds and exchange traded funds (ETFs) that invest in LIBOR-based floating-rate securities could benefit as coupons potentially reset higher. Additionally, short-term products such as securities lending cash reinvestment pools, local government investment pools, offshore US dollar money market funds and certain separate accounts could stand to benefit.

Figure 4: Average Yield of Prime Institutional Money Market Funds has Increased

Summary

We believe Fed rate hikes and supply/demand technicals — not credit concerns in the short-term funding markets — have put upward pressure on LIBOR and the LIBOR-OIS spread. While the Fed will likely continue to hike rates in 2018, the LIBOR-OIS spread mainly reflects the current supply/demand dislocation in the short-term funding markets. We believe this could benefit short-term investors in prime money market strategies, and ultrashort bond funds and ETFs.

Investors interested in prime money market funds may want to consider Invesco Liquid Assets Portfolio, Invesco STIC Prime Portfolio and Invesco Premier Portfolio. For those looking for ultrashort bond funds and floating-rate ETFs, Invesco Conservative Income Fund, PowerShares Ultra Short Duration Portfolio and PowerShares Variable Rate Investment Grade Portfolio may also be worthy of consideration.

The interest rate on excess reserves (IOER) is determined daily by the Board of Governors of the US Federal Reserve System. This payment of interest is intended to eliminate the implicit tax imposed on depository institutions by bank reserve requirements.

1 Source: Invesco. Since 2017, there have been plans afoot among regulators to replace LIBOR by 2021. However, this effort is still in the early stages, and we believe these potential changes have not yet had an impact on LIBOR valuations.

Rob Corner

Senior Client Portfolio Manager

Robert Corner is a Senior Client Portfolio Manager for Invesco Global Liquidity, which specializes in liquidity management solutions for institutional and retail clients, including money market funds, global funds, private placement funds, fixed income products and separately managed accounts. These products include government, tax-exempt, prime, cash plus, ultrashort/conservative income and short-term strategies.

Mr. Corner entered the industry in 1989 and joined Invesco in 2013. Previously, he was a portfolio manager and director of institutional liquidity management at Edge Capital Partners. He also served as a senior portfolio manager and director of short-term fixed income management at StableRiver Capital Management, a subsidiary of SunTrust’s Ridgeworth Capital Management.

Mr. Corner earned a BS degree in business administration from Drexel University. He holds the Series 65 registration.

Important information

Blog header image: Markus Pfaff/Shutterstock.com

Past performance is not a guarantee of future results.

Fixed income investments are subject to credit risk of the issuer and the effects of changing interest rates. Interest rate risk refers to the risk that bond prices generally fall as interest rates rise and vice versa. An issuer may be unable to meet interest and/or principal payments, thereby causing its instruments to decrease in value and lowering the issuer’s credit rating.

This does not constitute a recommendation of any investment strategy or product for a particular investor. Investors should consult a financial advisor/financial consultant before making any investment decisions. Invesco does not provide tax advice. The tax information contained herein is general and is not exhaustive by nature. Federal and state tax laws are complex and constantly changing. Investors should always consult their own legal or tax professional for information concerning their individual situation. The opinions expressed are those of the authors, are based on current market conditions and are subject to change without notice. These opinions may differ from those of other Invesco investment professionals.

All data provided by Invesco unless otherwise noted.

Invesco Distributors, Inc. is the US distributor for Invesco Ltd.’s retail products and collective trust funds. Invesco Advisers, Inc. and other affiliated investment advisers mentioned provide investment advisory services and do not sell securities. Invesco Unit Investment Trusts are distributed by the sponsor, Invesco Capital Markets, Inc., and broker-dealers including Invesco Distributors, Inc. Each entity is an indirect, wholly owned subsidiary of Invesco Ltd. PowerShares® is a registered trademark of Invesco PowerShares Capital Management LLC, investment adviser. Invesco PowerShares Capital Management LLC (PowerShares) and Invesco Distributors, Inc., ETF distributor, are indirect, wholly owned subsidiaries of Invesco Ltd.

©2017 Invesco Ltd. All rights reserved.

What’s up with US dollar LIBOR? by Invesco