The Case for Chinese Equities: A Shares Inclusion Update

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSummary

- We are constructive on Chinese equities despite tensions over trade. We see protectionist threats as largely negotiating tactics, while Chinese reforms, a stable growth environment and a solid earnings outlook support equities.

- MSCI’s A-Shares inclusion will begin in June 2018, kicking off a landmark event as the world’s second largest equity market is opened to foreigners.

- Global ETP flows show investors are increasingly taking a single country view on China instead of accessing it through broad EM index exposure.

Still room to run

Last year, Chinese equities were among the world’s best performing assets. The MSCI China Index was up 54% in 2017, outpacing broader emerging markets, which were up 37%, and more than double the 22% return of the S&P 500 Index.1 Despite the strong rally in 2017, we remain constructive on Chinese equities amid a stable growth environment, ambitious reform agenda, and solid earnings outlook.

To be sure, the recent tensions over trade do represent a risk. However, we view U.S. trade actions targeting China more as an opening gambit for negotiations than the start of a trade war. Moreover, China’s trade openness peaked over a decade ago as domestic growth drivers took on added importance, suggesting the economy may be relatively insulated from the effects of higher tariffs2.

We continue to see a strong reform agenda following the 19th National Party Congress supporting China’s pivot away from the “old economy” of credit-intensive, heavy industry and towards the “new economy” driven by technology, consumer spending, and healthcare. The shift towards faster-growing, less credit-intensive sectors has the dual benefit of supporting aggregate growth while letting policymakers continue their financial deleveraging campaign without overly straining growth. President Xi Jinping’s latest remarks on April 10th at the Boao Forum highlighted several reform efforts aimed at further opening China’s markets and which could help alleviate strained Sino-American relations. In particular, President Xi outlined plans to further open China through:

- Widening market access by raising foreign equity caps in the financial sector, easing restrictions on foreign financial institutions and reducing limits on foreign investment in manufacturing industries, including autos.

- Improving the investment environment by aligning domestic policies with international economic and trading norms.

- Expanding imports by lowering import tariffs on vehicles and holding the first China International Import Expo as a major policy initiative.

- Strengthening intellectual property rights (IPR) by re-instituting the State Intellectual Property Office to enforce IPR and raise the cost of violating IPR to increase deterrence.

China: Too big to ignore

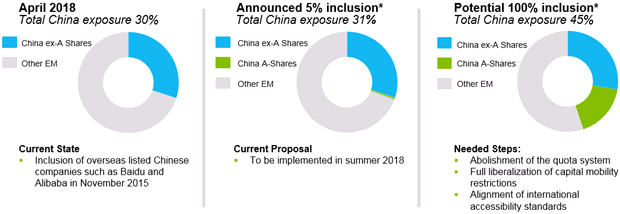

The positive outlook for China occurs against a backdrop of a significant development in the way investors can access Chinese equities. This June, MSCI will begin including a portion of the China A-shares market into the MSCI Emerging Market Index, a key index tracking emerging market (EM) equities. The MSCI EM Index currently has an approximate 30% weight to China3 by way of offshore-listed Chinese companies, the majority of them being those listed in

Hong Kong (“H-shares”).

Historically, foreign investors have had unrestricted access to only about half of China’s equities market (largely through H-shares). The remaining half is comprised of A-shares, the “onshore” stocks, which were only available to foreign institutions under strict quotas set by the Chinese government.

MSCI will gradually phase in the A-shares market, which represents the 2nd largest equity market globally by market capitalization and turnover.4 To start, a 2.5% inclusion factor will add 235 large cap A-share stocks (“MSCI-A stocks”) to the MSCI EM Index on June 1, 2018.5 The inclusion factor will then be raised to 5% of the A-share market on September 3, 2018.2 We expect the initial flow impact on markets to be relatively minimal given the small, incremental addition – at first it will translate into a less that 1% additional weight of China in the MSCI EM Index. Eventually, A-shares could account for 9% of the broad EM index after 50% of the A-shares are included, and then 17% after full inclusion. A complete, 100% inclusion of A-shares could then raise China’s MSCI EM index weight to more than 40%.2 For investors, having a view on China is moving from “nice to have” to “have to have” – it’s simply too big to ignore.

MSCI Emerging Markets Index Inclusion Roadmap

Source: BlackRock, MSCI, as of April 16, 2018. Notes: Index constituents subject to change. *The percentage number refers to the inclusion factor applied to the free float-adjusted market capitalization of China A-Share constituents in the pro forma MSCI China Index.

Implications for investors

The inclusion of A-shares provides investors with a more accurate picture of – and access to -- the Chinese market. A-shares provide access to sectors of the economy currently underrepresented in other share classes, with larger weights in sectors such as materials, industrials, consumer discretionary and healthcare. The “new economy” in China – areas such as the tech, consumer, and healthcare segments – is mostly represented in the offshore H-shares market. The fact that the onshore A-shares market is the second largest equity market globally suggests that these secular growth themes are currently underrepresented in foreign investors’ portfolios.

Fortunately, deciding between A-shares and H-shares isn’t mutually exclusive. The complementary nature of A-shares exposure can also be seen through its low correlation with global equity markets. Investors should consider holding exposure to both markets instead of picking one over the other. Given the lingering operational complexities facing foreign investors, and the breadth of A-share names, investors may want to consider investing via an ETF structure, which removes operational burdens as well as providing cost effective, liquid and broad based exposure.

Flows

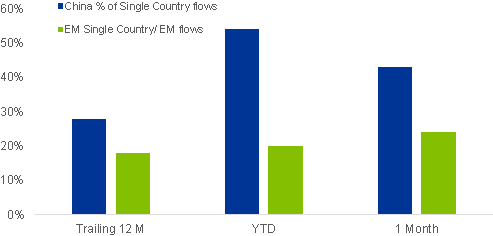

As China’s EM Index concentration grows, investors may be well served to adopt a single country focus on China and rethink EM as EM ex-China instead. Global ETP flows suggest investors are doing just that: EM equity flows have been increasingly single country focused over the past year – a notable contrast to developed market flows which have favored broad exposure. Moreover, there is a meaningful acceleration in EM single country flows led by China. EM single country flows as a percent of total EM flows have risen from 18% over the trailing one year to 20% YTD and to 24% over the last month. Over the same time, China has seen its share of single country flows rise from 28% over the trailing one year to over 50% YTD, before pulling back to 43% as trade worries hit market sentiment in March.6 However, annualizing the trailing one month and YTD China flows suggest a more than double and triple increase, respectively, over the trailing one year flows.

EM Flows are increasingly “single country” focused and Chinese flows are accelerating

Source: Global Intelligence Flash Report, as of April 12, 2018

The bottom line: Investor appetite for China is accelerating significantly and investors are increasingly accessed dedicated China exposures, not broad EM index exposure.

Conclusion

The opening of China’s A-share market and accompanying index inclusion is a landmark event for the global investor community. For long-term investors, the A-shares vs. H-shares decision is a false dilemma given complementary exposure. The real question is how much China does one need in their portfolio. As China’s concentration in broad EM indexes eventually grows north of 40%, investors should start taking a view on China and EM ex-China separately, just as investors do with U.S. and non-U.S. developed markets. Global ETP flows suggest investors are beginning to do just that.

© iShares

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All