New York - The Tax Cuts and Jobs Act of 2017 included a number of changes that have directly impacted the $3.7 trillion municipal bond market.

Two changes in particular -- the capping of state and local tax (SALT) deductions and the elimination of tax-exempt advanced refunding’s -- are making it more challenging for investors and financial advisors who are "going it alone" when managing portfolios of muni bonds.

Higher demand and lower issuance

Why exactly is it getting more difficult for individuals to oversee muni portfolios after tax reform?

First, by capping SALT deductions at $10,000, the changes raise an investor's effective state income tax rate. However, income from an in-state muni bond remains exempt from this (higher) state income tax. Therefore, we expect demand for in-state bonds will increase -- especially in states with high income tax rates.

Higher demand is likely to result in lower yields relative to those available from out-of-state bonds. Investors and advisors who build their own muni portfolios in high-tax states may already find this task challenging because of reduced dealer inventories and limited access to new issues. The recent tax changes are likely to make it even more difficult to implement a state-specific muni mandate.

Additionally, the elimination of tax-exempt advanced refunding’s should result in less issuance. New issue volume is down over 40% so far in 2018 when compared to the average volume of the last five years.

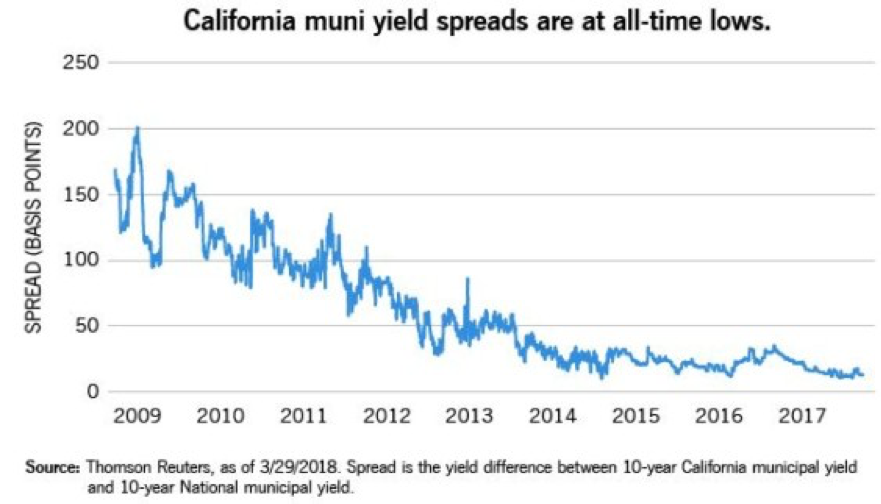

For example, California has the highest top marginal state income tax rate in the country at 10.85%. At the same time, California new-issue volume is down 45% year to date. This has brought California muni spreads to all-time lows.

State vs. national munis

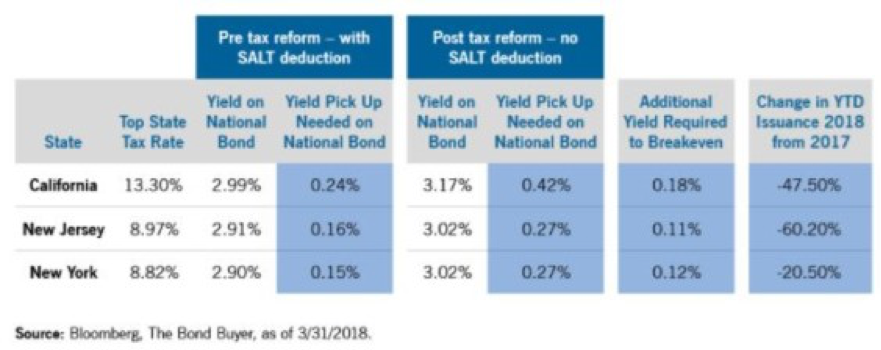

Since effective state income tax rates have gone up, there is an even greater incentive to own in-state bonds. While the added yield pick-up required on a national bond to compensate for the state income tax has increased, that yield hurdle is not as large as many investors think. It is often easily achieved. Even after tax reform, a national portfolio may still yield more after taxes, compared to an in-state portfolio.

Below is a table of the states that are among the highest in both income tax rates and annual issuance. In each case, it is assumed investors can buy a 10-year bond in that state at a yield of 2.75%. The table shows additional yield necessary to compensate for the in-state tax, in order to break even both pre- and post-tax reform.

For example, before tax reform, assuming a New York resident could have bought an in-state bond at a yield of 2.75%, he or she would have required a 2.9% yield on a national bond to break even. After tax reform, the investor would require a 3.02% yield. While the breakeven hurdle has increased, it may still be achieved by accessing a broad dealer network.

Bottom line: Using a professional muni manager lets investors access a broader dealer network, and may provide access to attractive new-issue deals and secondary inventories of muni bonds. Managers may also purchase bonds free of price markups, which might otherwise reduce yield. Whether investors are implementing state-specific muni portfolios or seeking additional yield national, we believe the value-add of professional muni managers has only become more important in the wake of tax reform.

Eaton Vance does not provide tax or legal advice. Prospective investors should consult with a tax or legal advisor before making any investment decision.

An imbalance in supply and demand in the municipal market may result in valuation uncertainties and greater volatility, less liquidity, widening credit spreads and a lack of price transparency in the market. There generally is limited public information about municipal issuers. As interest rates rise, the value of certain income investments is likely to decline. Rising interest rates could reduce the value of the bonds in the portfolio, thus adversely affecting the value of the overall investment.

©2018 Eaton Vance Distributors, Inc. • Member FINRA/SIPC Two International Place, Boston, MA 02110 • 800.836.2414 • eatonvance.com

© Eaton Vance

Read more commentaries by Eaton Vance