Growth, momentum factors prevail after a volatile start to the year

Equities experienced heightened volatility during the first quarter of 2018, with the S&P 500 Index surging 7.55% from Dec. 31 2017, through Jan. 26, 2018, before dropping nearly 8% through quarter-end.1 Early in the quarter, market activity was buoyed by upward revisions to corporate profit outlooks following federal tax cuts in December, coupled with a squeeze on short volatility positions.

However, this momentum eased in the final two months of the quarter as investors became uneasy over a number of developments:

- The prospect of Internet regulations in the wake of Facebook privacy issues

- President Trump’s tweets about “anti-competitive” practices by online retailing giant Amazon

- Proposed US tariffs on steel and aluminum imports from China

- European Union threats to impose a 3% tax on online advertising revenues, goods and services

- A downgrade to the outlook for iPhone sales

- Concerns over tighter US monetary policy

The confluence of these events caused the CBOE Volatility Index (VIX) to spike nearly 81% during the first quarter, although high yield spreads were more contained — rising just 4.23% and hinting at a more benign risk picture.1 Despite market jitters, economic activity was robust during the quarter — albeit somewhat late cycle in nature, given strong manufacturing numbers in the form of the ISM Manufacturing index, and a drop in the Citigroup Economic Surprise Index from near-record highs (detailed in the second table below).

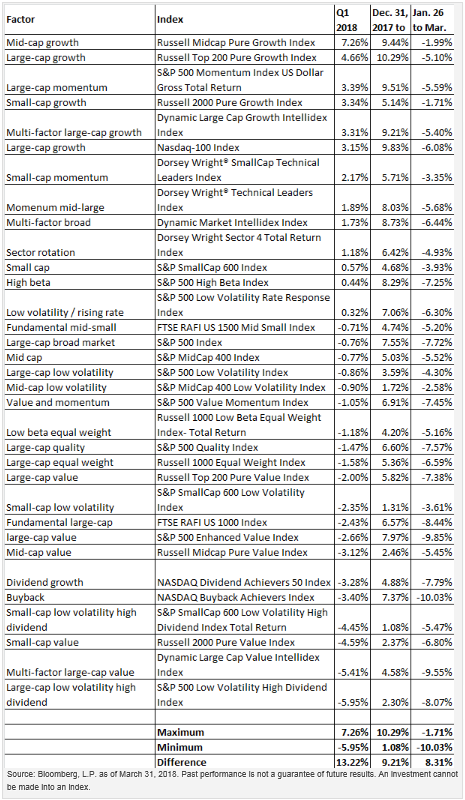

Growth, small size, momentum factors outperform

Aided by the strong US economy, growth, momentum and small size were the best-performing factors during the quarter. Many investors expected tax cuts to benefit smaller stocks, which were viewed as less likely to be affected by a potential trade war. Mid-cap shares performed especially well during the quarter. The Russell Midcap Pure Growth Index outpaced the S&P 500 Index on the strength of overweight positions in health care — particularly biotech — and technology.

Dividend yield, value factors underperform

On the other end of the spectrum, the value and dividend yield factors were among the worst performers during the quarter. Value was hurt by the poor performance of consumer staples companies and insurers, while dividend yield strategies were pressured by exposure to real estate — a sector not expected to benefit from tax reform — and an underweight position in consumer discretionary and technology shares.

Investment factor return dispersion was again notable during the quarter, with a 13.22% return spread between the best performer (mid-cap growth) and worst performer (large-cap low vol high dividend).

Low volatility factor provide cushion amid escalating volatility

The low volatility factor helped cushion the market’s decline late in the quarter. From Jan. 26 through quarter-end, the S&P 500 Low Volatility Index retreated 4.30%, while the S&P 500 Index fell 7.72%. The relative strength of low volatility was due in part to the overall drop in the equity market, and in part to heightened risk measures. VIX — a barometer of equity market volatility — jumped from 11.08 on Jan 26, 2018, to 19.97 at quarter-end, while high yield spreads, as defined by the Barcap US High Yield to Worst – 10-Year Treasury Spread Index, rose from 2.95% to 3.45% — underscoring a moderate increase in risk aversion.1

Yield spreads narrowed later in the quarter, as the US 10-year Treasury yield rose from 2.66% on Jan 26. to 2.74% at quarter-end. Despite an increase in short-term rates, low volatility provided 55.7% down capture during the quarter — meaning that it avoided nearly half of the broader market’s decline.1 This underscores my theory that interest rates are a not a primary driver of low volatility returns. In my view, risk levels and the overall direction of the equity market are far more relevant to the performance of low volatility.

Utilities, mid-cap performance pace low volatility returns

Because utilities are an important component of the S&P 500 Low Volatility Index, their performance was reflected in low volatility performance. Early in the quarter, utilities earnings estimates trended to the downside, while lower corporate tax rates diminished the value of the tax shield provided by debt financing. I believe rising interest rates hurt both the utilities and real estate sectors, which are sometimes viewed as bond proxies because of their yield potential. However, utilities gained ground after the market peaked on Jan. 26.

Low volatility’s relative outperformance wasn’t just contained to large-cap stocks. The S&P 400 MidCap Low Volatility Index outpaced the S&P MidCap 400 Index by roughly 3% during the quarter, while the S&P 600 SmallCap Low Volatility Index was marginally stronger than the S&P SmallCap 600 Index.

Looking ahead

Looking ahead, I believe low volatility strategies could provide a path for diversifying risk and reducing concentration risk present in market-cap-weighted indexes and momentum strategies. Despite recent market volatility, the underlying strength of the US economy and expected profit growth within the information technology sector are both positives for the momentum factor, and may play against technology’s inherent risks. Moreover, investors are still digesting quarterly earnings results. With the bar to beat earnings estimates set low, we could see upside surprises.

I believe the outlook for technology companies remains bright. Based on consensus earnings estimates, the S&P 500 technology sector could see growth in excess of 26% in 2018.1 That’s potentially significant, as technology accounts for nearly 40% of the S&P 500 Momentum Index and nearly one quarter of the S&P 500 Index. More specifically, Apple, Microsoft, Facebook, Alphabet, Amazon and Intel account for 14.8% of the S&P 500 Index, while Microsoft, Facebook, Alphabet, and Amazon account for 24.5% of the S&P 500 Momentum Index.1 Importantly, the S&P 500 Low Volatility Index holds none of these names. For that reason, a low volatility strategy could potentially provide a different return and risk profile and may generate diversification benefits when combined with either the S&P 500 Index or a momentum strategy.

1 Bloomberg L.P., March 31, 2018

Nick Kalivas

Senior Equity Product Strategist

PowerShares by Invesco

Nick Kalivas is a Senior Equity Product Strategist representing the PowerShares family of exchange-traded funds (ETFs). In this role, Nick works on researching, developing product-specific strategies and creating thought leadership to position and promote the smart beta* equity line up.

Prior to joining Invesco PowerShares, Mr. Kalivas spent the majority of his career in the futures industry, delivering research, strategy and market intelligence to institutional and high net worth clients centered in the equity and interest rate markets. He was a featured contributor for the Chicago Mercantile Exchange, and provided research services to a New York-based global macro commodity trading advisor where he supplied insight on equities, fixed income, foreign exchange and commodities. Nick has been quoted in the Wall Street Journal, Financial Times, Reuters, New York Times and by the Associated Press, and has made numerous appearances on CNBC and Bloomberg.

Nick has a BBA in accounting and finance from the University of Wisconsin – Madison and an MBA from the University of Chicago Booth School of Business with concentrations in economics, finance, and statistics. He holds the Series 7 and Series 63 registrations

Important information

Blog header image: Heather Bradley/Shutterstock.com

Downcapture refers to the amount of downside in the broader market that is captured by an index.

Spread represents the difference between the yield on a corporate bond and a similar maturity US Treasury bond.

Volatility is a statistical measurement of the magnitude of up and down asset price fluctuations over time.

The Barcap US Corporate High Yield to Worst―10-Year Treasury Spread Index, which displays the yield spread between a portfolio of high yield notes as defined by Barclays Capital and the 10-year Treasury yield, measures risk in the high yield market.

The CBOE S&P 500 Implied Correlation Index measures the expected average correlation of price returns of S&P 500 Index components, implied through S&P 500 Index option prices and prices of single-stock options for the 50-largest largest components of the S&P 500 Index.

The CBOE Volatility Index (VIX) is a key measure of market expectations of near-term volatility conveyed by S&P 500 stock index option prices. VIX is the ticker symbol for the Chicago Board Options Exchange (CBOE) Volatility Index, which shows the market’s expectation of 30-day volatility.

The Citigroup Economic Surprise indexes are quantitative measures of economic news, defined as weighted historical standard deviations of data surprises; a positive reading of the Economic Surprise Index suggests that economic releases have on balance been beating consensus estimates.

The CRB BLS Spot Index measures price movements of 22 sensitive basic commodities from markets presumed to be among the first to be influenced by changes in economic conditions.

The Dorsey Wright Sector 4 Total Return Index selects up to four exchange-traded funds from the PowerShares DWA Momentum Sector lineup of ETFs with the objective of gaining exposure to the strongest relative strength sectors in the US equity space on a monthly basis.

The Dorsey Wright SmallCap Technical Leaders Index includes securities pursuant to a Dorsey, Wright & Associates, LLC proprietary selection methodology that is designed to identify companies that demonstrate powerful relative strength characteristics. Approximately 200 companies are selected for inclusion from a small-cap universe of approximately 2,000 of the smallest US companies selected from a broader set of 3,000 companies.

The Dorsey Wright Technical Leaders Index includes approximately 100 US companies from a broad mid- and large-capitalization universe. The index is constructed pursuant to Dorsey, Wright & Associates, LLC’s proprietary methodology, which takes into account, among other factors, the performance of each of the approximately 1,000 largest companies in the eligible universe as compared to a benchmark index, and the relative performance of industry sectors and sub-sectors.

The Dynamic Large Cap Growth Intellidex Index seeks to provide capital appreciation while maintaining consistent stylistically accurate exposure. The Style Intellidexes apply a rigorous 10-factor style isolation process to objectively segregate companies into their appropriate investment style and size universe.

The Dynamic Large Cap Value Intellidex Index is designed to provide capital appreciation while maintaining consistent stylistically accurate exposure. The Style Intellidexes apply a rigorous 10-factor style isolation process to objectively segregate companies into their appropriate investment style and size universe.

The Dynamic Market Intellidex Index seeks to identify and select companies from the US marketplace with superior risk-return profiles.

The FTSE RAFI US 1000 Index is designed to track the performance of the largest US equities, selected based on the following four fundamental measures of firm size: book value, cash flow, sales and dividends. The 1,000 equities with the highest fundamental strength are weighted by their fundamental scores.

The FTSE RAFI US 1500 Small-Mid Index is designed to track the performance of small and medium-sized US companies. Companies are selected based on the following four fundamental measures of size: book value, cash flow, sales and dividends. Each of the equities with a fundamental weight ranking of 1,001 to 2,500 is then selected and assigned a weight equal to its fundamental weight.

The ISM Manufacturing Index, which is based on Institute of Supply Management surveys of more than 300 manufacturing firms, monitors employment, production inventories, new orders and supplier deliveries.

The NASDAQ US BuyBack Achievers Index is designed to track the performance of companies that meet the requirements to be classified as BuyBack Achievers. It is composed of US securities issued by corporations that have effected a net reduction in shares outstanding of 5% or more in the trailing 12 months.

The NASDAQ US Dividend Achievers 50 Index is composed of 50 stocks selected principally on the basis of dividend yield and consistent growth in dividends.

The Purchasing Managers Index (PMI), a commonly cited indictor of the manufacturing sector’s economic health, is calculated by the Institute of Supply Management.

The Russell 1000 Equal Weight Index captures the risk and return performance of an equal weight investment strategy for US large-cap stocks.

The Russell 1000 Low Beta Equal Weight Index tracks US large-cap stocks that exhibit low beta, with all index constituents weighted equally within the index.

The Russell 2000 Pure Growth Index is composed of securities with strong growth characteristics selected from the Russell 2000 Index. Securities are weighted based on their style score.

The Russell 2000 Pure Value Index is composed of securities with strong value characteristics selected from the Russell 2000 Index. Securities are weighted based on their style score.

The Russell Midcap Pure Growth Index is composed of securities with strong growth characteristics selected from the Russell Midcap® Index. Securities are weighted based on their style score.

The Russell Midcap Pure Value Index is composed of securities with strong value characteristics selected from the Russell Midcap® Index. Securities are weighted based on their style score.

The Russell Top 200 Pure Growth Index is composed of securities with strong growth characteristics selected from the Russell Top 200 Index. Securities are weighted based on their style score.

The Russell Top 200 Pure Value Index is composed of securities with strong value characteristics selected from the Russell Top 200 Index. Securities are weighted based on their style score.

The S&P 500 Enhanced Value Index is designed to measure the performance of the top 100 stocks in the S&P 500 Index with attractive valuations based on “value scores” calculated using three fundamental measures: book value-to-price, earnings-to-price and sales-to-price.

The S&P 500 High Beta Index consists of the 100 stocks from the S&P 500 Index with the highest sensitivity to market movements, or beta, over the past 12 months. Beta is a measure of relative risk and is the rate of change of a security’s price.

The S&P 500 Low Volatility High Dividend Index is composed of 50 securities traded on the S&P 500 Index that historically have provided high dividend yields and low volatility.

The S&P 500 Low Volatility Index consists of the 100 stocks from the S&P 500 Index with the lowest realized volatility over the past 12 months.

The S&P 500 Low Volatility Rate Response Index is designed to measure the performance of the top 100 companies of the S&P 500 Index that have exhibited low volatility and are less sensitive to changes in interest rates.

The S&P 500 Momentum Index is designed to measure the performance of securities in the S&P 500 Index universe that exhibit persistence in their relative performance.

The S&P 500 Quality Index screens holdings based on three fundamental measures of quality — profitability, earnings quality and financial robustness — which help to assess a company’s potential future profitability, as well as the financial risk each company faces.

The S&P MidCap 400 Index is an unmanaged index considered representative of mid-sized US companies.

The S&P MidCap 400 Low Volatility Index consists of 80 out of 400 medium-capitalization range securities from the S&P MidCap 400 Index with the lowest realized volatility over the past 12 months.

The S&P SmallCap 600 Index is a market-value-weighted index that consists of 600 small-cap US stocks chosen for market size, liquidity and industry group representation.

The S&P SmallCap 600 Low Volatility High Dividend Index seeks to measure the performance of the 60 least-volatile high dividend-yielding stocks in the S&P SmallCap 600 Index.

The S&P SmallCap 600 Low Volatility Index consists of 120 out of 600 small-capitalization range securities from the S&P SmallCap 600 Index with the lowest realized volatility over the past 12 months.

The US Dollar Index measures the value of the US dollar relative to majority of its most significant trading partners.

The Global Industry Classification Standard was developed by and is the exclusive property and service mark of MSCI, Inc. and Standard & Poor’s.

About risk

Many products and services offered in technology-related industries are subject to rapid obsolescence, which may lower the value of the issuers.

Investments in real estate related instruments may be affected by economic, legal, or environmental factors that affect property values, rents or occupancies of real estate. Real estate companies, including REITs or similar structures, tend to be small and mid-cap companies and their shares may be more volatile and less liquid.

To the extent the fund invests a greater amount in any one sector or industry, there is increased risk to the fund if conditions adversely affect that sector or industry.

Factor investing is an investment strategy in which securities are chosen based on certain characteristics and attributes.

Securities tied to the utilities sector are subject to a variety of industry specific risk factors that may adversely affect their business or operations, including those due to production, volumes, commodity prices, weather conditions, etc. They are also subject to significant federal, state and local government regulation.

Investing in securities of large-cap companies may involve less risk than is customarily associated with investing in stocks of smaller companies.

Low volatility cannot be guaranteed.

Momentum style of investing is subject to the risk that the securities may be more volatile than the market as a whole, or that returns on securities that have previously exhibited price momentum are less than returns on other styles of investing.

Stocks of small and mid-sized companies tend to be more vulnerable to adverse developments, may be more volatile, and may be illiquid or restricted as to resale.

A value style of investing is subject to the risk that the valuations never improve or that the returns will trail other styles of investing or the overall stock markets.

Commodities, currencies and futures generally are volatile and are not suitable for all investors.

This does not constitute a recommendation of any investment strategy or product for a particular investor. Investors should consult a financial advisor/financial consultant before making any investment decisions. Invesco does not provide tax advice. The tax information contained herein is general and is not exhaustive by nature. Federal and state tax laws are complex and constantly changing. Investors should always consult their own legal or tax professional for information concerning their individual situation. The opinions expressed are those of the authors, are based on current market conditions and are subject to change without notice. These opinions may differ from those of other Invesco investment professionals.

All data provided by Invesco unless otherwise noted.

Invesco Distributors, Inc. is the US distributor for Invesco Ltd.’s retail products and collective trust funds. Invesco Advisers, Inc. and other affiliated investment advisers mentioned provide investment advisory services and do not sell securities. Invesco Unit Investment Trusts are distributed by the sponsor, Invesco Capital Markets, Inc., and broker-dealers including Invesco Distributors, Inc. Each entity is an indirect, wholly owned subsidiary of Invesco Ltd. PowerShares® is a registered trademark of Invesco PowerShares Capital Management LLC, investment adviser. Invesco PowerShares Capital Management LLC (PowerShares) and Invesco Distributors, Inc., ETF distributor, are indirect, wholly owned subsidiaries of Invesco Ltd.

©2017 Invesco Ltd. All rights reserved.

How did factors perform during a roller coaster first quarter? by Invesco