Summary: Trade war rhetoric is driving US equities. This week, for the third time in the past month, the start of a sustained rally was clobbered by administration threats. Conversely, every interim recovery has come on the heels of conciliatory language. Long story short, what happens next in the equity market is very much a function of which trade posture the administration adopts next. Longer term, it's unlikely much of the current rhetoric will make into actual policy as it suits no one's economic interests.

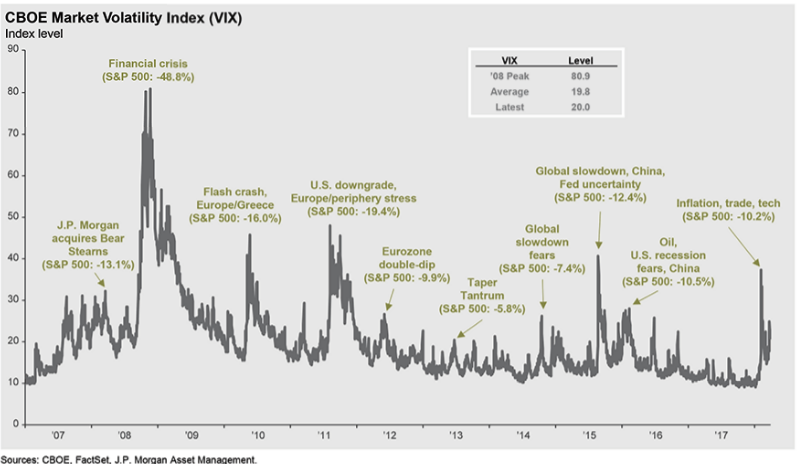

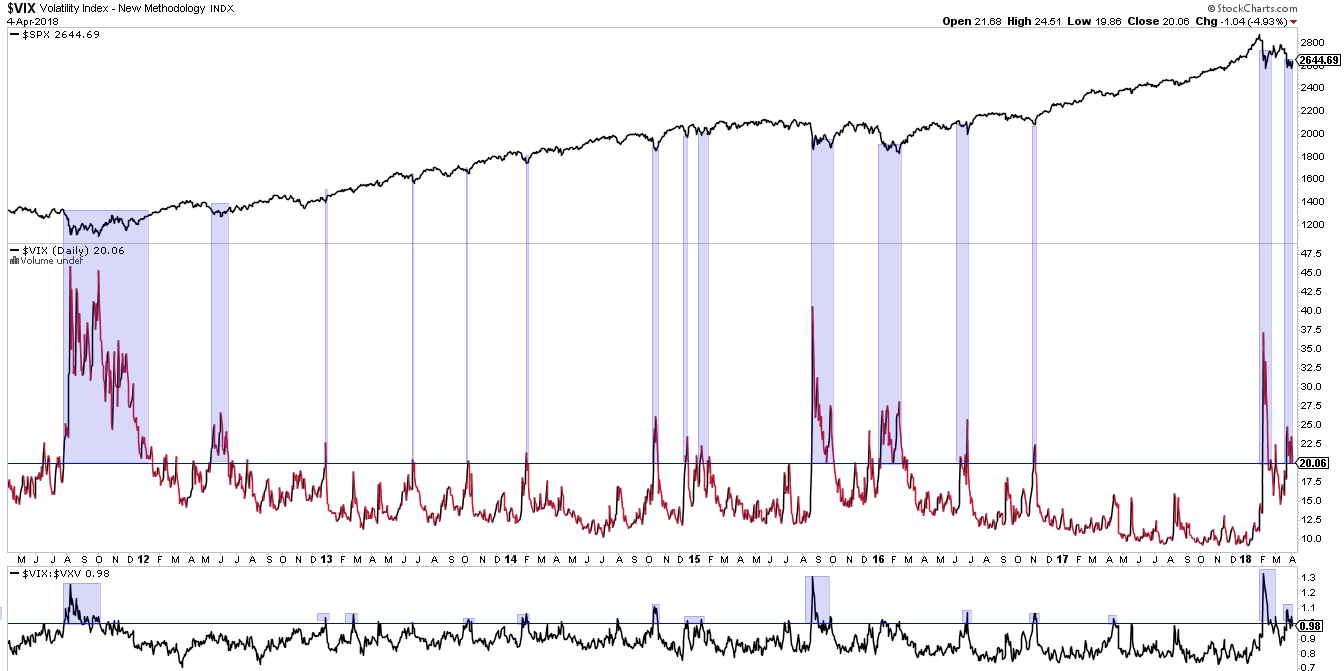

Volatility has shot up in the past two months. Remarkably, investors now view volatility as the "new safe haven" and a "dependable bet." To that end, speculators are now positioned net long Vix futures to a near record extent; in the past decade, that has reliably coincided with at least a near term top in volatility.

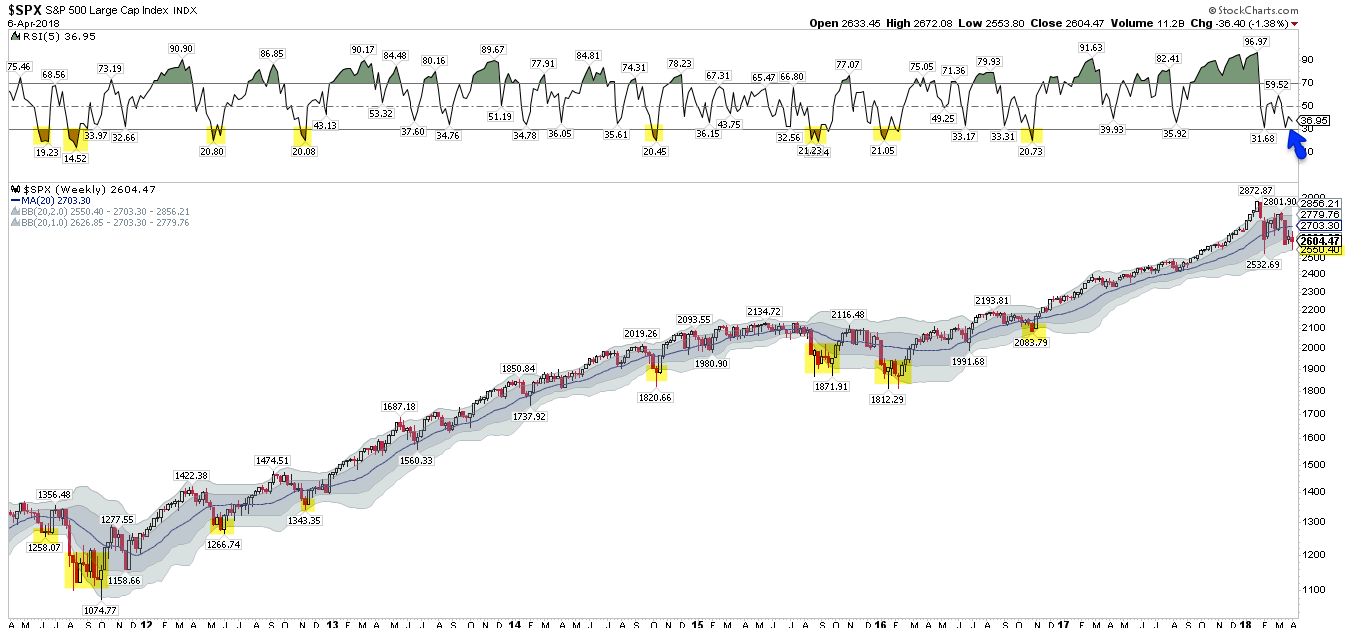

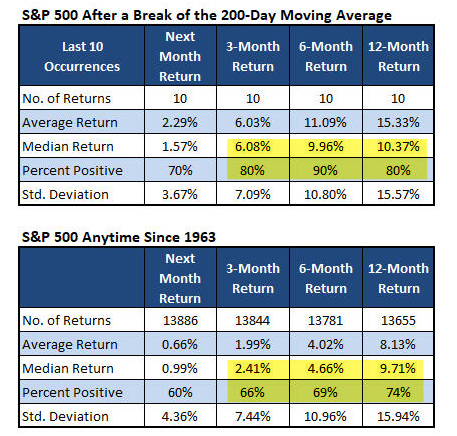

This past week, SPX closed below it's 200-dma for the first time in over 400 days. The end of prior long streaks have not coincided with the start of bear market since 1962. Returns after the end of these long streaks have been exceptionally strong.

US equities gained three days in a row last week for the first time in a month but a massive gap down on Friday and further follow through selling turned the markets negative for the week and (mostly) for the year (from Alphatrends). Enlarge any chart by clicking on it.

The culprit was trade war rhetoric once again. On Thursday evening, the administration announced its intention to levy $100b in retaliatory tariffs on China. This follows previous statements that started on February 27 (steel tariffs) and March 13 (larger tariffs).

After the 11% sell off in January and early February, every rally since then has been stopped dead by trade war rhetoric. Conversely, every interim recovery has come on the heels of conciliatory language from administration officials.

Long story short, what happens next in the equity market is very much a function of which trade posture the administration adopts next. It's unlikely much of the current rhetoric will make into actual policy - a long term positive - but the intermediate path is anyone's guess.

From a pure technical perspective, Friday's sell off is more dangerous than the ones before it as it returns price to prior lows (and the 200-dma) for at least the fourth time, implying a higher likelihood of failure. In the chart above, there is room to test intraday lows down to 2530-50. If that gives way, the next level is the June-August trading range between 2400-2500.

2550 also returns SPX to its important lower weekly Bollinger Band. SPX has a strong propensity to trade down to this level each year, especially after low volatility years (like 1995, 2013 and 2017). A long pierce with an intra-week recovery would be a common reversal pattern. That looked likely on Thursday (before the latest trade war threat) but was made null on Friday.

On a short term basis, the beginning of this week is important. SPX had regained its 5-dma and weekly pivot (WPP) on Wednesday. Thursday was a good follow through day higher, with the 5-dma inflecting upwards. This is how new uptrends start (arrows). Friday's close was back below, but an bounce early this week could still rescue the pattern.

Again, trade rhetoric predominates other considerations short term. That said, losing 2% on a Friday after also losing 2% earlier in the week (last Monday) is a pattern that typically leads to further downside in the next day or so (i.e., momentum). Equities are more often higher after 5 days (64%), but risk/reward is skewed negative over the next week (from Odd Stats).

Friday was also the sixth major distribution day (90% down volume) of the year. For comparison, there was only one in all of 2017.

Returns after the end of these long streaks have been very strong relative to all periods (from Schaeffers).

In summary, trade war rhetoric is driving US equities, meaning, what happens next in the equity market is very much a function of which trade posture the administration adopts next. Longer term, it's unlikely much of the current rhetoric will make into actual policy as it suits no one's economic interests.

Volatility has shot up in the past two months and speculators are now positioned net long Vix futures to a near record extent; in the past decade, that has reliably coincided with at least a near term top in volatility.

This past week, SPX closed below it's 200-dma for the first time in over 400 days; returns after the end of these long streaks have been exceptionally strong.

© The Fat Pitch

Read more commentaries by The Fat Pitch