On the heels of the positive surprise on the jobs front, we also received the new release of the state of U.S. households last week. The state of the U.S. household is in one the best shapes it has been in throughout history; though depending on how you look at it, it may corroborate your skepticism or optimism. At a recent discussion, a key debt figure was triggering doubt about this optimism. To ascertain if the numbers corroborate the skepticism of the U.S. consumer we wanted to offer a slideshow of the various metrics we analyze.

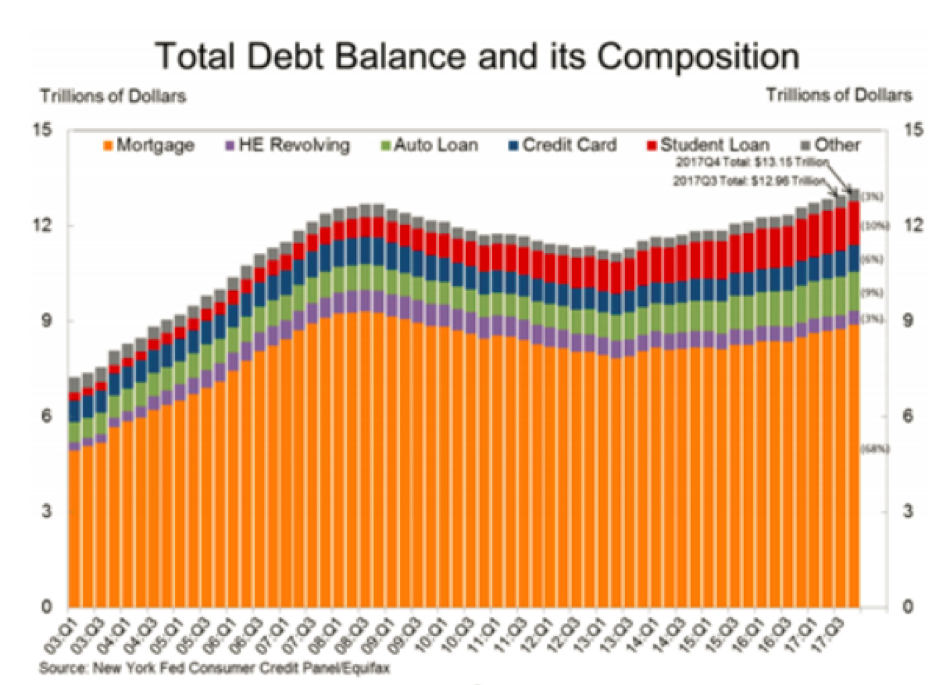

The first is to look at the metrics showing growing household debt to all-time levels. This is verified by the Federal Reserve in tabulating mortgages, auto loans, revolving and credit card debt as well as student loans. Currently, we are at all-time highs of just over $13 trillion. It’s up from the previous all-time high set in 2008 by about 10%.

By itself, this might cause great clickbait for articles; however, we need to look at the other side of the balance sheet. Since 2008 total household assets have risen from $69 trillion to just over $114 trillion. So, while debt increased 10%, total assets increased over 60%. Since the 1940s, assets have grown at an annual rate of 6.75%; yet from the bottom of the asset recovery in 2009, the annual growth of assets is at 5.95%. It seems we want to continually put the metrics behind the emotions of our fears on the back burner unless it affirms anxieties.

To put this in perspective, consider household debt compared to various other forms to corroborate this discrepancy.

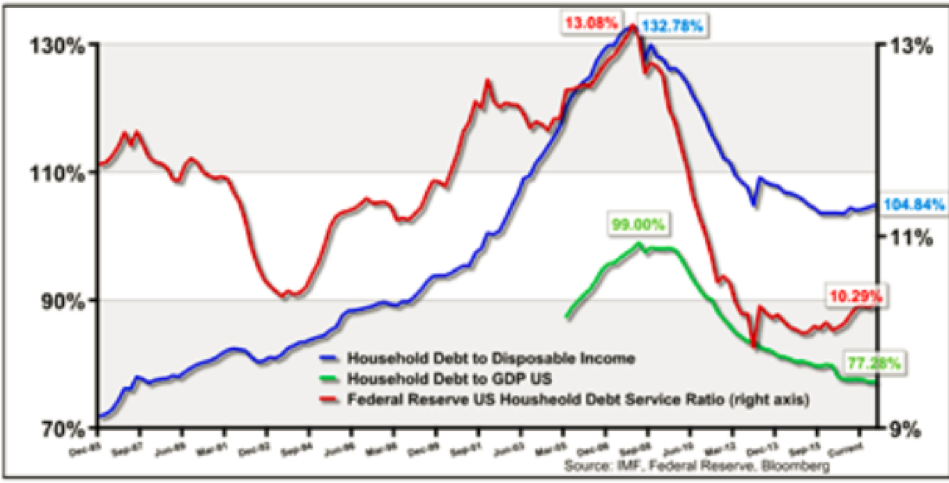

As confirmed, household debt to disposable income, debt to U.S. GDP and the U.S. household debt service ratio have all corrected and have been slow to ascend to historic averages, let alone highly leveraged metrics.

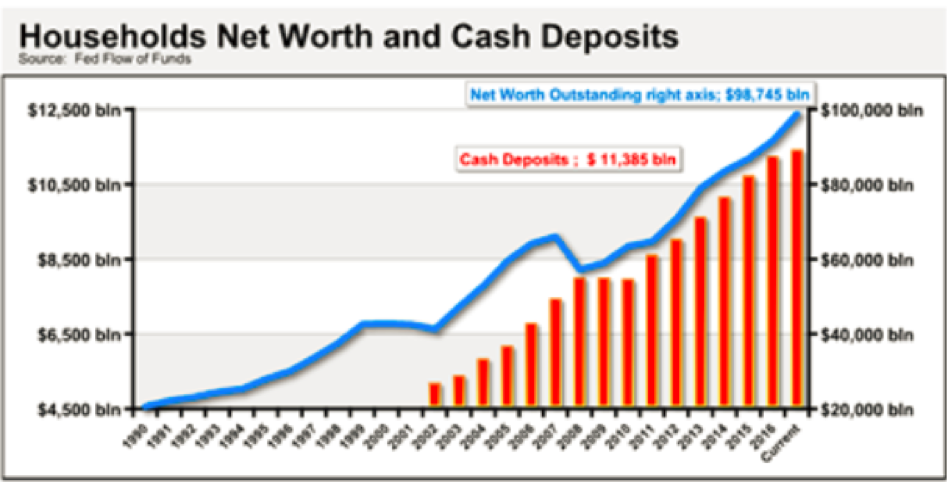

U.S. households’ net worth rose to $98.475 trillion, while total cash deposits rose to $11.385 trillion.

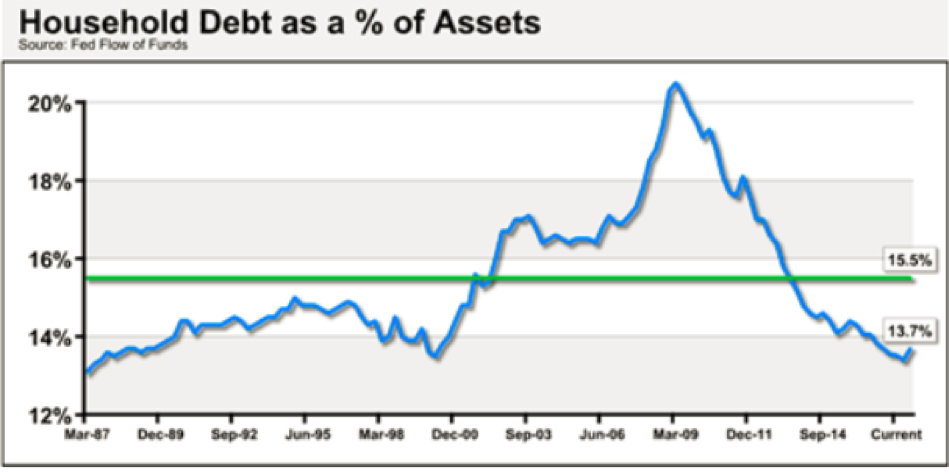

That gets us to the perspective of how the current consumer looks relative to history when comparing their total debt to total assets. Though we are under the long-term average by a measly 1.8%, it is important to note that a rise to the long-term average would constitute an increase in nominal debt by over $4 trillion from current levels. This would constitute a 20% boost to the nominal U.S. Gross Domestic Product number. This doesn’t even count if the consumer felt as robust as they did in equity bubbles of the dot-com era or The Great Recession. Those numbers would melt the most rational quantitative analyst.

One last note, the Fed Flow of Funds report has a volatile but telling number on the state of U.S. corporations and their liquidity needs. The corporate financing gap is a number in which if it is positive it denotes that broadly companies must access the capital markets or other debt lines to meet operational needs. Since it has been measured, companies have needed to access the capital markets nearly 80% of the time. Take special attention to notice the high points pointed to the last two bear markets. The current metric plummeted to negative territory, a positive in that companies are not needing capital markets and can fund operation from current cash flow. This is due to the corporate tax cut and the repatriation of upwards of what might be a trillion dollars. To affirm this metric, consider that commercial paper outstanding is half of where it peaked in 2008 and has not seen any sustained growth.

Negative events often have a more lasting impact and adjust behavior and perspective unlike positive events. We are hardwired for negative thinking, with the need of five positive events to counter one negative in the average person. We are alike in that we feel as though we are long-tailed cats in a room full of rocking chairs and it’s just a matter of time before it gets pinched. There is plenty to worry about today and the vigilance against disaster is always a good long-term frame of mind. However, it is also important to put fears and hope in proper perspective when given the chance.

The state of the U.S. consumer is strong by a multitude of metrics and currently we are not seeing one of the most important triggers in households or corporations – a liquidity crunch. This will be giving a scant signal when it is most alarming, but the signal now is more of our own making and not of the current state of affairs.

© Advisors Asset Management

© Advisors Asset Management

Read more commentaries by Advisors Asset Management