We may come to view February 2018 as a turning point for the U.S. economy. For the first nine years of the current expansion, fiscal policy was constrained and trade policy was measured. During the past month, the two have moved with more force, raising important questions about the outlook.

The Tax Cuts and Jobs Act of 2017 is taking effect as employers implemented new tax withholding tables in February. Many workers saw increases to their take-home pay, which should provide a short-term stimulus to consumer spending. Meanwhile, a wave of stock repurchases is providing shareholders with a special dividend that will also boost consumption. This could stress the capacity of the economy.

The market is still digesting the new tariffs on imported steel and aluminum. While we do not anticipate a full-blown trade conflict, the U.S. economy is now at risk of greater inflation as the costs of commonly-used raw metal materials are poised to increase.

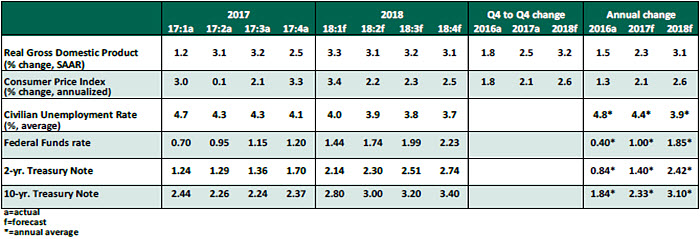

Key Economic Indicators

Influences on the Forecast

- The March employment report tallied a startlingly high 313,000 new jobs in February, far exceeding expectations. The unemployment rate was unchanged at 4.1%. Strong job growth and a low and a steady unemployment rate indicate the labor force has expanded; the absence of runaway wage inflation suggests the employment population still has room to grow. Wage growth and job availability have helped coax some labor holdouts back to work.

- Speculation continues about the return of inflation, but recent readings have been benign. Hourly wages made headlines with 2.9% year-over-year growth in February, a nine-year high. The March reading cooled to 2.6%, closer to recent averages. Meanwhile, the Consumer Price Index (CPI) rose by 2.1% year-over-year in January and 2.2% in February, in line with expectations and reflecting steady growth, not rampant inflation.

- The manufacturing sector continues to perform well. The Institute of Supply Management (ISM) Purchasing Managers’ Index rose to 60.8 (where a reading over 50 means expansion), reflecting the strongest observed growth in manufacturing in the current economic cycle. Notably, the ISM prices index climbed to 74.2, a six-year high, reflecting higher raw materials prices.

- Fourth-quarter real economic growth was revised down slightly to 2.5%. The revised reading confirmed the initial findings that consumer spending has driven much of our current economic growth. In light of tax code changes, we expect consumption to remain strong in 2018. The question will be whether business investment rises sufficiently to boost productivity growth.

- Congress passed a spending agreement lifting spending caps that had restrained federal expenditures. Gross domestic product will be further bolstered by increased government spending, and the risk of impairment due to a government shutdown has been pushed forward two years.

- New Federal Reserve Chair Jerome Powell gave his first remarks before Congress. He indicated that recent market events have caught the Board of Governors’ attention, adding that “headwinds have become tailwinds.” We continue to expect four rate increases from the Fed this year, starting with the upcoming Federal Open Market Committee meeting on March 20-21.

- January’s import tariffs on solar panels and residential washing machines foreshadowed a broader tariff announcement on all imported steel and aluminum. We view the risks of this action as being on the downside, as higher metal prices and retaliatory measures may add to inflation, curtail job creation and hinder corporate profits. Though this tariff round allows for country-by-country exemptions, the trend towards greater trade restrictions seems clear.

Information is not intended to be and should not be construed as an offer, solicitation or recommendation with respect to any transaction and should not be treated as legal advice, investment advice or tax advice. Under no circumstances should you rely upon this information as a substitute for obtaining specific legal or tax advice from your own professional legal or tax advisors. Information is subject to change based on market or other conditions and is not intended to influence your investment decisions.

© 2018 Northern Trust Corporation. Head Office: 50 South La Salle Street, Chicago, Illinois 60603 U.S.A. Incorporated with limited liability in the U.S. Products and services provided by subsidiaries of Northern Trust Corporation may vary in different markets and are offered in accordance with local regulation. For legal and regulatory information about individual market offices, visit northerntrust.com/disclosures.

© Northern Trust

Read more commentaries by Northern Trust