Economic reforms remain critical for emerging economies' attempts to successfully transition from low-wage industrial economies to high-skilled, consumption-based economies.

For those economies – and investors – that transition can lead to better economic growth, stronger future earnings, and a lasting, structural improvement over peers. Here, we review the reform momentum across four countries – Brazil, Indonesia, India, and China – and preview South Africa's post-Zuma reform agenda.

- The global economic expansion, along with reasonable valuations, supports our current preference for overweighting emerging market (EM) equities.

- Economic reform is a critical component of future economic growth and development in many EMs, and warrants close monitoring.

- Our preferred EM countries include Brazil, Indonesia, India and China. We describe their reform efforts below. In addition, positive political developments in South Africa bear watching.

Brazil's swings between reformist and populist administrations demonstrate the importance of economic reforms. The prior reform cycle, which began in 1994 under succeeding President Cardoso’s leadership, ultimately stabilized the economy by breaking extreme inflationary expectations. In the following years, which also coincided with stronger commodity prices, Brazilian equity markets were a major outperformer across EM equities.1 The populist policies in Luiz da Silva's (Lula's) later years and under President Dilma Rousseff effectively wiped out these gains as market-friendly reforms were replaced with incoherent macroeconomic policies and unsustainable fiscal promises, culminating in a deep stagflationary recession. President Michel Temer offered investors hope after quickly enacting labor reforms, adopting a microeconomic reform agenda aimed at boosting productivity, and addressing fiscal sustainability with a 20 year cap on real spending growth at zero percent.2

However, the spending cap isn’t enough to fully correct Brazil’s fiscal path; that requires pension reform. Pensions account for roughly 45% of total expenditure and are growing 5% annually in real terms.3 At this pace, Brazil's pension spending will consume the entire fiscal budget by 2030.4 Brazil's positive cyclical position – accelerating economic growth, loose financial conditions, and low inflation – has offset declining market expectations for further pension reforms ahead of the October 2018 elections. However, Brazil will quickly need to address its pension system; doing so would arrest the unsustainable fiscal trajectory, possibly leading to lower neutral policy rates. It could also help increase potential GDP through higher investment and productivity increases. The October elections may complicate the timing of reforms, but certainly not their necessity nor the benefits they bring investors.

Brazil vs. Emerging Markets

Indonesia: Strong reform momentum

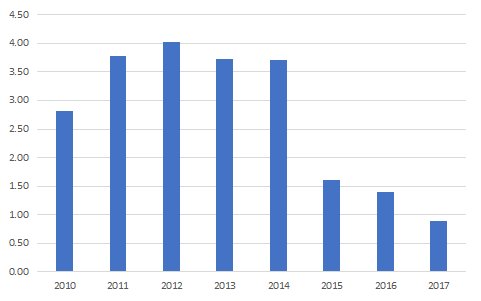

Indonesia has steadily enacted over 39 reforms in 15 years, half of which came in the last four years, a sign that reform momentum is accelerating. The World Bank labeled Indonesia one of the world's top 10 reformers, climbing 37 places after enacting more reforms than any country for a second consecutive year.5 For context, starting a business in Jakarta now takes just 22 days compared to 181 days in 2004.5 Broader macro-finance conditions are also improving. Credit access continues to deepen, while insolvency resolution has improved considerably. Cuts to energy subsidies have also helped finance infrastructure spending, which could continue to support long-run GDP growth. In short, easing regulatory burden and more efficient allocation of resources – both capital and labor – is leading to greater macro stability and stronger growth.

Indonesia is expected to push ahead with reforms intended to make it easier to do business, however greater fiscal measures are required. Indonesia remains vulnerable to swings in global liquidity and risk appetite due to a persistent budget deficit that has left foreign ownership of its debt near an EM-high of 40%.6

|

Indonesia vs. Emerging Markets

Relative Returns, USD

|

Government Spending on Subsidies

% of GDP

|

|

|

| |

India: Short-term pain, long-term gain

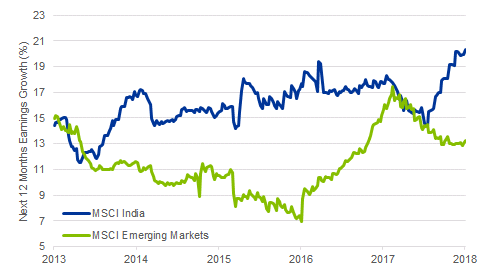

India's potential growth slowed from an estimated 7.6% (2003 – 2008) to 6.7% (2014/2015) as reform momentum slowed.7 However, the Narendra Modi government has aggressively instituted a series of reforms over the past several years including India's largest indirect tax reform, the goods and services tax (GST), adopting an inflation targeting central bank framework, financial deepening and demonetization, improving the ease of doing business, and a new bankruptcy code. India’s reform agenda should address fiscal constraints and a sluggish investment cycle next, and the renewed momentum is a good start. The reform momentum has lifted potential growth estimates to above 7% as reform momentum should lead to higher productivity and greater investment. In addition, these measures were designed to address structural weaknesses. The inflation targeting framework helped anchor inflation expectations, while the GST could raise up to $50bn in tax receipts, in turn boosting India's low tax-to-GDP ratio by 2% by 2020.8

The rapid pace of reforms weighed on corporate margins and near-term economic growth, however both are already showing signs of rebounding. India's PMI, now at 52.5, has already bounced off the 46.0 lows in July 2017.9

|

Earnings Growth

|

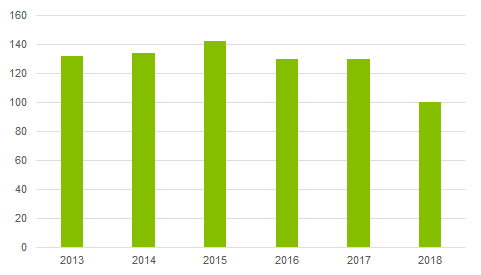

India's Ease of Doing Business Ranking

|

|

|

| |

China: Out with the old, in with the new

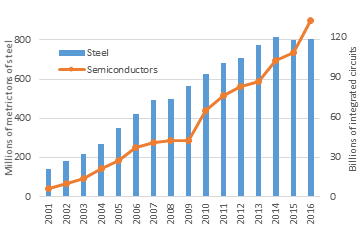

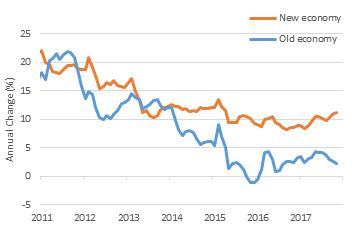

China's macro imbalances – excess capacity, excessive credit and corporate leverage, inefficient state-owned enterprises, and slowing growth – have been well documented. Yet these risks are largely concentrated in the "old" economy, not in the "new" economy, which has seen growth accelerate and accounts for an increasingly large share of China's economy. The shifting growth mix is a strong signal China is taking appropriate steps to transition from a low-cost manufacturing-based exporter to a more services-driven, consumption-based economy. The 19th Party Congress outlined an ambitious reform agenda covering internal priorities – innovation, environmental protection, reform of state-owned enterprises, supply-side capacity cuts – and external priorities – namely a more assertive foreign policy. We expect specific details to roll out in 2018 and investors should pay close attention, in our view. Having consolidated power, President Xi Jinping is well positioned to push forward an aggressive reform agenda.

|

The New vs. Old Economy

|

Chinese Steel and Semiconductor Output

|

|

|

| |

South Africa: Life after Zuma

Cyril Ramaphosa, South Africa's new president and leader of the African National Congress (ANC), offers a new beginning following Jacob Zuma’s resignation. Zuma's scandal-plagued administration cost the country dearly. Growth slowed, inflation rose, and the unemployment rate hit nearly 30%.10 Ramaphosa's goal is to kick start the reform agenda, including fiscal consolidation, and a corruption crackdown. Early indicators are positive. South Africa increased its value-added tax (VAT) for the first time since 1993 to stem its deteriorating credit outlook, and South Africa’s new budget is expected to trim the fiscal deficit from 4.2% of GDP to 3.6% next year.11GDP growth forecasts have also inched higher, climbing from 1.1% in October to 1.5%.12 A cabinet shuffle appears likely before proceeding with further reforms. Stay tuned, as this reform story may just be getting started.

1Source: Thomson Reuters. Data compare the MSCI Brazil Index against the MSCI Emerging Markets index; both are measured in USD. Past performance does not guarantee future results.

2Fiscal spending is to grow no more than the prior year’s inflation rate.

3Source: Brazilian National Treasury as of February 2018.

4Source: World Bank as of February 2018.

5Source: World Bank. Doing Business 2018: Reforming to Create Jobs.

6Source: Bloomberg, as of February 2018.

7Source: Reserve Bank of India.

8Source: BlackRock Investment Institute as of November 2017.

9Source: Thomson Reuters, I/B/E/S, as of February 21, 2018.

10Source: Bloomberg, as of February 21, 2018.

11Source: South Africa National Treasury as of February 2018.

12Source: Bloomberg, as of February 21, 2018.

©2018 BlackRock, Inc. All rights reserved.

Read more commentaries by iShares