Muhlenkamp Market Commentary 1st Quarter 2018

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsTony: Good afternoon, everybody. This is Tony Muhlenkamp, and I want to thank you for joining us for our quarterly webcast. We're here to try to bring you up to date a little bit on what we've been seeing and doing, with what we're seeing in the markets, and the economies, and sometimes the policies that are coming out of DC and central banks around the world. With me, I've got our portfolio managers, Ron Muhlenkamp and Jeff Muhlenkamp. You probably all know Ron's been doing this professionally full-time, 80 hours a week or more it seems like, since roughly 1968.

Ron: Thereabouts…

Tony: Ron started our firm in 1977. Jeff, his co-manager, came on ten years ago. Jeff started as an analyst, and is now serving as backup and co-manager for Ron. And between the two of them, I'm hoping to pick their brains a little bit on what we're seeing, what we're doing, and how we're using that to manage the portfolio you've entrusted us with if you're a client or shareholder, and what you can expect to see from us here a little bit going forward. So I want to thank you all for joining us.

Let's get Ron and Jeff started. Jeff, why don't you go ahead and take it from there.

Jeff: Thanks, Tony. Good afternoon, everybody, and thanks for joining us today.

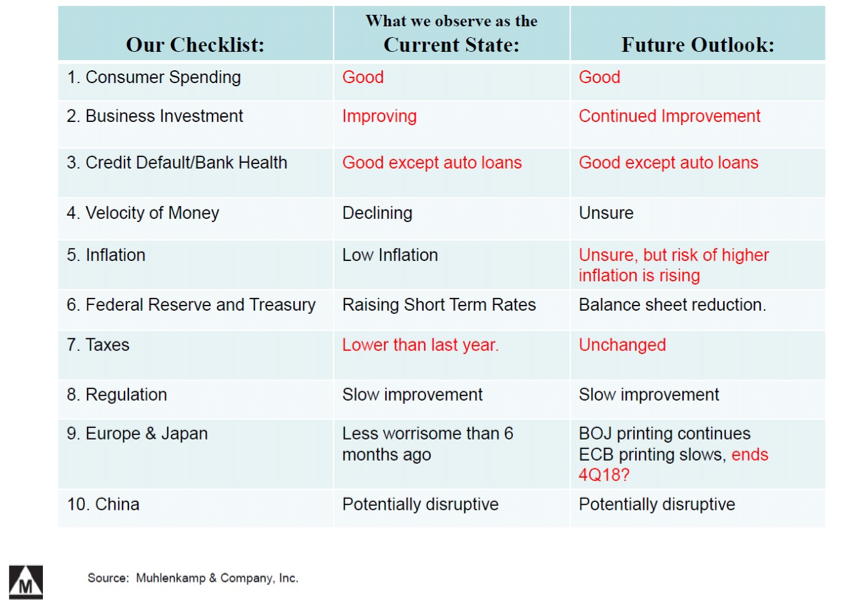

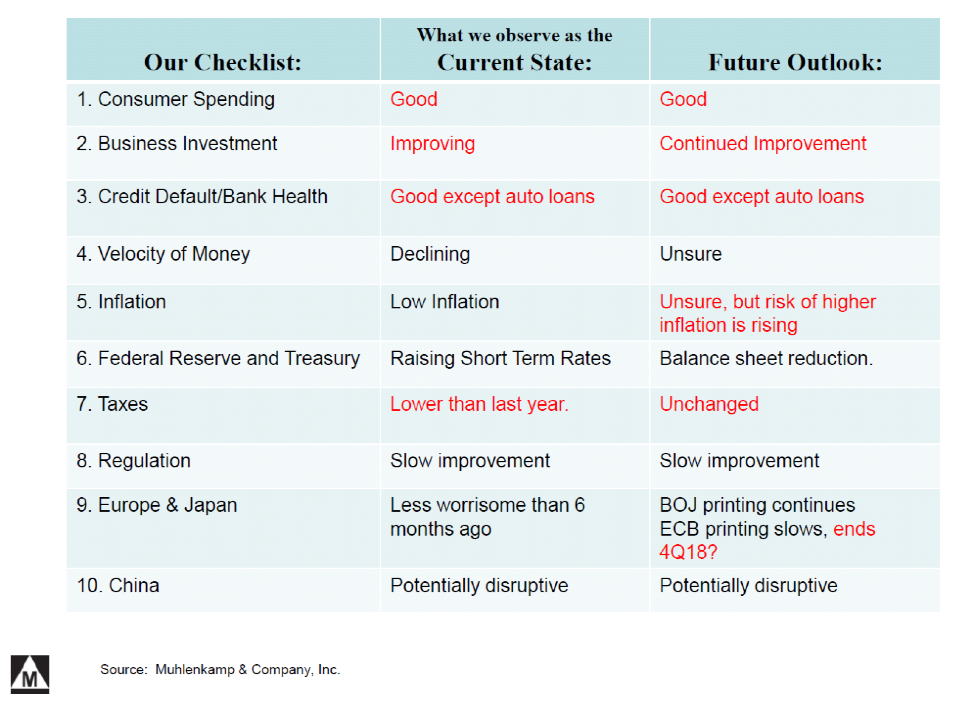

Jeff: We're going to update you today on what we see happening in the economy and the markets, and as we have for the past six quarters or so, we're going to use this checklist as a guide. You can see on this checklist the short assessments that we have for each category. I'll go over them very briefly, and then we'll explain more and give you more detail about why we come to those conclusions during the course of the presentation.

So starting at the top, we've changed our outlook for consumer spending from mixed to good, both currently and in the future. We've changed our assessment of business investment to improving, and we expect that improvement will continue in the future. When you look at credit default or bank health, we now think that the current state is good with the exception of auto loans, which continue to slowly decay. And we expect that to continue. We don't see things that will change with that in the near term.

Ron: The items in red in this list have changed since the prior quarter.

Jeff: Thank you, Ron. Yes, if it's in black, it hasn't changed since the prior quarter. If it's in red, that's to draw your attention to it because we've changed what we're saying about it. Inflation, we think the risks are to the upside in the future, although currently we're not seeing high inflation. Taxes changed right before Christmas, so we have different taxes now than we had even three months ago. But looking forward, we don't see those changing again. We think that's about as much as they're going to do with taxes for quite a while. And then, in the future outlook for Europe and Japan, we think in concert with the rest of the market, frankly, that the European Central Bank will probably end their quantitative easing program here towards the end of the year. So that's the summary, and we'll start with GDP, and we'll flesh some of this out for you.

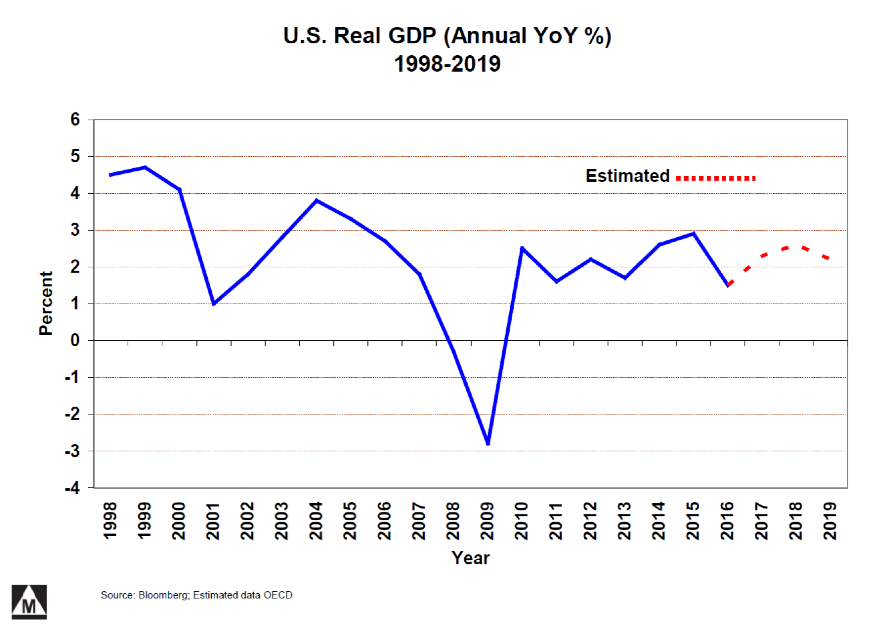

Jeff: This is a chart of U.S. Real Gross Domestic Product (GDP) growth (real—meaning inflation-adjusted) since 1998. Recessions typically involve a contraction in real GDP, which you saw in 2008 and 2009, although you really didn't in the 2001, 2002 recession. Go ahead, Ron.

Ron: You'll notice that GDP ‘real’ has been about 2% for the last eight years. On a per capita basis, it looks a little bit different. Our population tends to grow about 1% a year, as it has for a long, long time. So on a per capita basis, this would be a 1% plus instead of a two. So you don't have to be very much below average for that to have shown no growth the last eight years, and we'll say a little bit more about that going forward.

Jeff: So what we saw prior to the recession was kind of, on average, 3% growth. That took a step down to 2% growth. As we look forward, we don't specifically make growth projections for the economy, but we do have an opinion. And frankly, our opinion looking forward is maybe a little bit better than the recent past, and that's primarily driven by increased business spending, and we'll address that. But the dashed line here is a survey of economists and their projections for the future, and we are probably right in agreement with that. What we don't see is any reason for GDP growth to suddenly decline. We have no indicators of that in the near term right now.

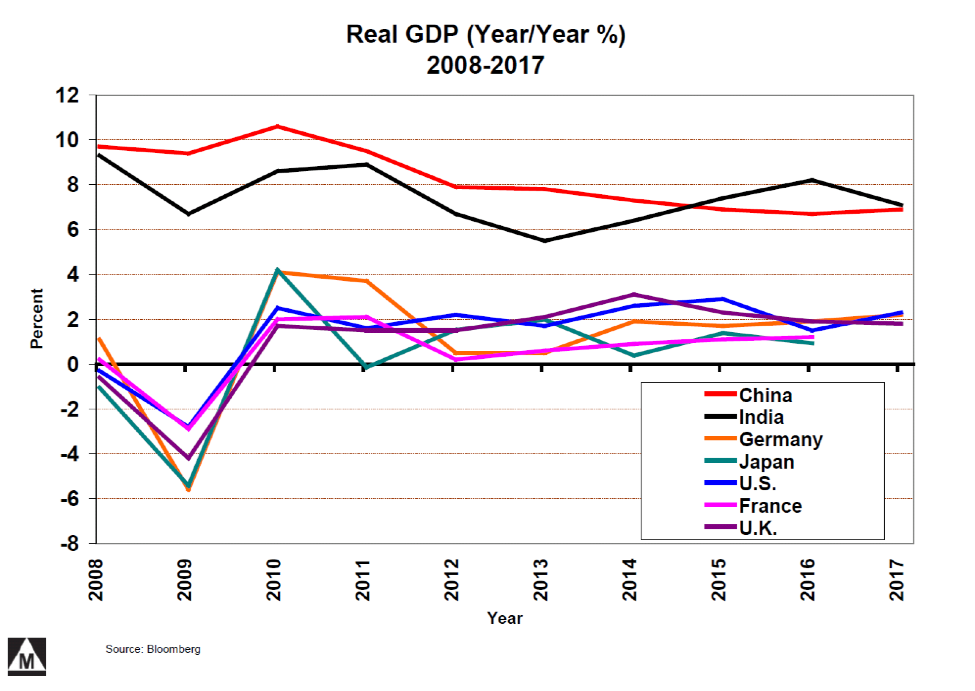

Jeff: In this chart, we're going to look at inflation-adjusted real GDP growth on a global basis (not just the United States). At the top, in red and black at about 7%, you have India and China growing quite nicely. Clustered here around the 2% level is the U.S. in blue. You've got the U.K. in purple, and you've got Germany in orange, and then down here at the 1% mark is France and Japan.

Ron: And, what's interesting about Japan is their population is not growing, so their real 1% growth looks like a 1% on a per capita basis, which is about what ours has been on a per capita basis. The point really is, the chart is the way economists look at things, but when you talk to individuals in this country, they've been saying for eight or ten years, "It doesn't feel like we're getting ahead." And that's because they're looking at it, obviously, on a per capita or on a per household basis. And we'll say a bit more on this as we go through the charts.

Jeff: You may have read headlines in the papers talking about a global expansion, and this is what they're talking about. Frankly, Japan has picked up a little bit more, and France has picked up a little bit more, but whereas since the recession, you had a number of countries take their turn in going back into recession, mostly Europe and Japan. For the last year or so, everybody's out of recession, and everybody is growing at least moderately. So this illustrates what those newspapers are talking about.

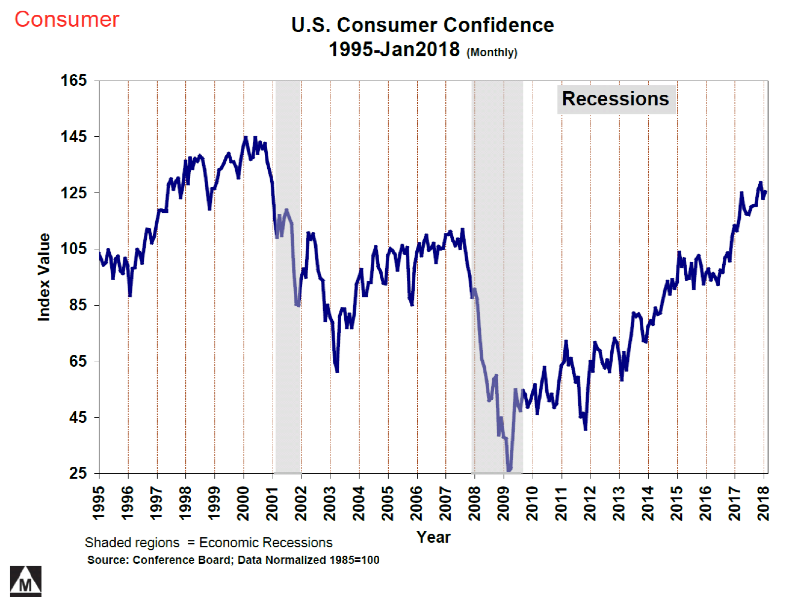

Jeff: Shifting now to consumer metrics, this is a chart of U.S. Consumer Confidence since 1995. These gray bands indicate periods of recession. You can see that in a recession, you always have consumer confidence fall. That certainly happened in 2008, 2009. You hit a trough down here at 25 [index value] in 2009. Post-recession, it took almost until 2015 to almost get back to where we were pre-recession. And then, during the election, the run-up to the election, it kind of stabilized. Post-election, it jumped big time, so now consumers are more confident than they had been during the expansion from 2003 to 2008. So when we saw particularly that pop post-election, we considered that a good thing. One of the things we were watching for was to see whether or not the consumer opened up their checkbook and started to spend and behave in accordance with this higher level of confidence.

Ron: If you've been listening to us the last three or four quarters, we told you that our observation over the years has been: when the consumer or business gets confident, they can hold that confidence for six or nine months, and then if it's not reinforced, it tends to dissipate (this is an observation, we can’t prove it). Well, we think that much of the confidence for the last year was based on the hope of a tax cut, and it got reinforced in the last few months. So, as you see, this is holding up on the consumer. A little while later, you'll see small business [Small Business Optimism slide]. It looks largely the same, but not quite.

Jeff: Well, you're jumping ahead on me, Ron. Thanks.

Ron: I do that sometimes.

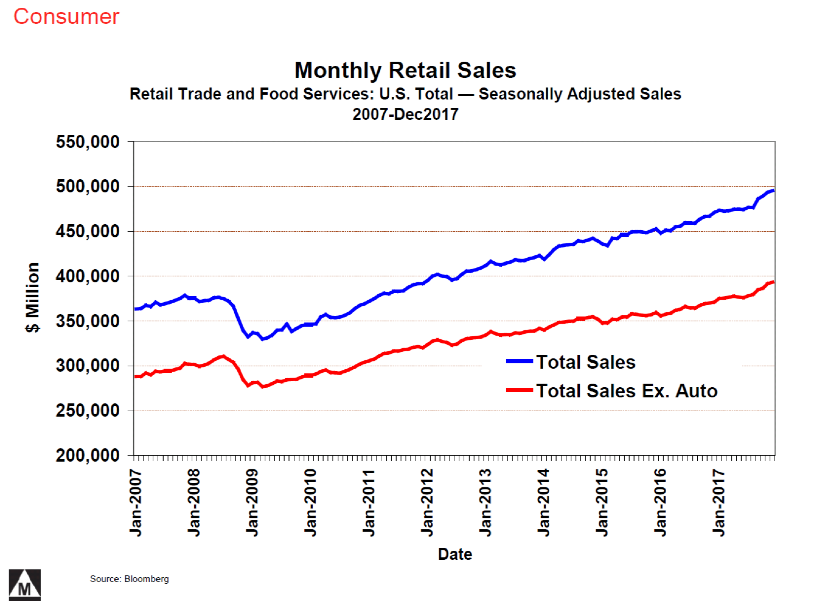

Jeff: So, did the consumer start spending? That's kind of what we're trying to address with this chart. This is monthly consumer sales since 2009. It's measured in nominal dollars. The blue line up here on top is total sales. The red line subtracts auto sales. So sometimes, since autos are such a big ticket item, you can have changes in auto sales that mask what is going on or what the consumer's doing in other areas, and so it's useful to look at them both. Six months ago, we were a little bit concerned because we saw spending, both ex autos and with autos, flattening out. But in the last six months, it started picking up again. And this is primarily what has driven our characterization of consumer spending from mixed to good. So instead of autos falling off and everything else kind of holding in there, now you've got an acceleration, once again, in growth in consumer spending.

Ron: If you look at both of these charts, today [2018] compared to '08 is up about 33%. Well, if you go 10 years, 33% happens to be 3% a year, which is in fact 2% inflation and 1% real spending. So, on a per capita basis, while the pattern looks the same, the trend doesn't look quite as impressive.

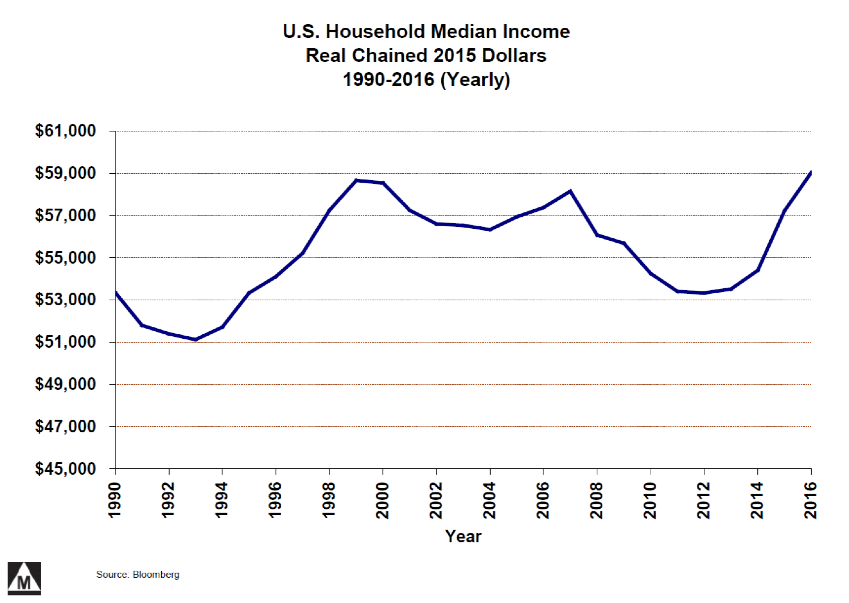

Jeff: Bringing us to median income. We haven't shown you wages lately, so we thought we'd revisit that. It's probably been two years or so since we looked at it. This is a chart of inflation-adjusted median income from 1990 to 2016. We don't quite have full-year 2017 numbers in yet, so it only goes to 2016.

Ron: Per household…

Jeff: Yes, per household.

Ron: Which is slightly different than per capita, but it comes pretty close. And as you'll see until the last maybe two years, there wasn't a whole lot to brag about on a per-household or per-capita basis.

Jeff: Exactly so. So really, per household, median wage has peaked in 2000. In 2007, you almost got back to that peak. It fell off all the way through 2013, and it's only in the last two or three years picked back up again. So we're back now to that peak. But over that 20-year period, frankly, the median wage earner has not felt all that good, and this is why. His wages have not increased on an inflation-adjusted basis.

Tony: Remind me, median versus average. Median says half the households are below this point, and half the households are above that point.

Jeff: Correct.

Tony: It's not an average by any stretch.

Jeff: It's not an average, and the reason we don't use average is it's easy for outliers (extremely high earners or extremely low earners) to skew the number. So the idea of median is that it more closely reflects what the typical wage earner sees, not necessarily the average wage earner. But there is a difference, and they can be useful for different purposes.

Tony: Thank you.

Ron: And just for one more point of perspective, look at the last 20 years compared to the prior ten. So if you weren't used to earnings or incomes going up, which is true in any number of—if you're in Cuba, they haven't gone up for 50 years. But when things were going well and then you level off and don't do well for 20 years, you see where some of the frustration comes from in the American public.

Jeff: Well, frankly, if you look at this part [the trough and the decline on the chart], it’s not too hard to imagine why people might be frustrated and looking for a change in political leadership, to be honest.

Ron: All kinds of changes…

Jeff: All kinds of changes.

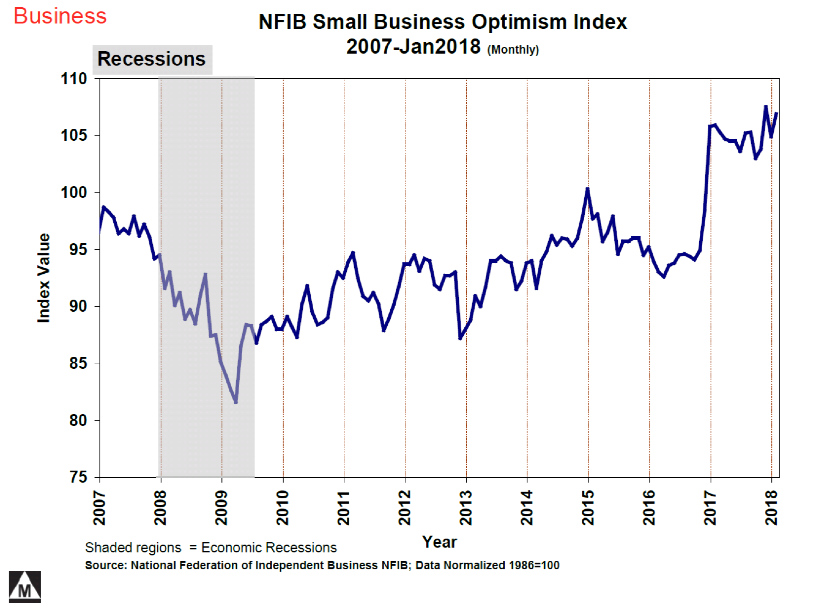

Jeff: Moving on to businesses. We're going to look now at small business optimism as expressed by the National Federation of Independent Business (NFIB) survey that they conduct monthly. So the idea is they survey independent businesses and ask them about their satisfaction or projections both for the current and future state. And this is their metric for establishing how optimistic businesses are feeling. So what you saw (gray bar is a recession) is optimism tanked in the recession, then very gradually came back. And it didn't make pre-recession highs until 2015 and then declined a little bit as the economy slowed down. If you remember, late '15, early '16, the economy was in fact slowing. Then you've got the run up to the election here in 2017. Post-election, it popped. It traded off just a little bit. But now, it's starting to climb again. So this gave us, frankly, a very interesting perspective post-election when we said, "If business starts spending--" again, just like we thought with the consumer. "If business starts translating that optimism into spending and investing, then that's going to be good for the economy." And that was something we highlighted to you a little over a year ago, something we've been watching very closely since then.

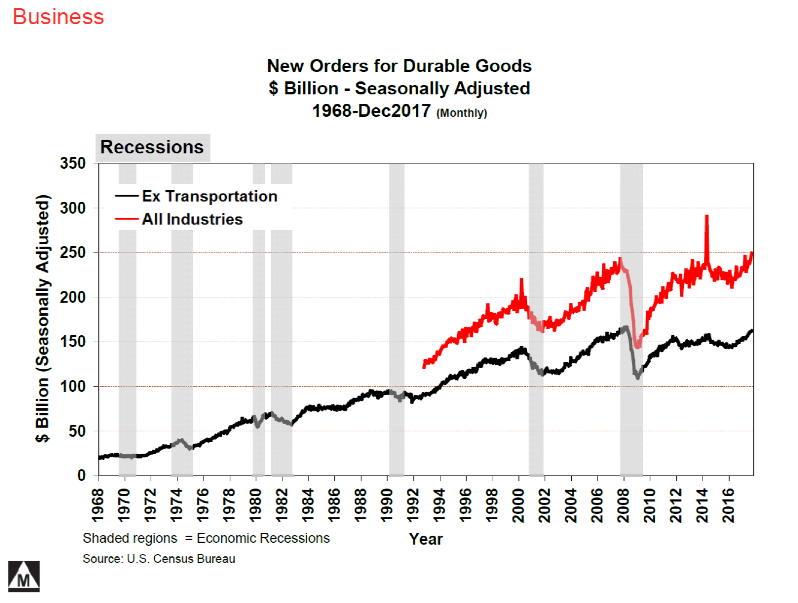

Jeff: So, how has business spending gone? This is a chart of new orders for durable goods since 1968, and it's measured in nominal dollars. Again, the gray bars are recessions, the red line is all goods and the black line backs out aircraft. So much like for the consumer, it's sometimes useful to back out autos. For businesses, because aircraft is such a big ticket item—they can hide things, mask things—it's also useful to look at it ex aircraft. So what you saw is, of course, investment in capital goods declined in the recession and it slowly recovered. But then, unlike previous recoveries where you had a nice, steady growth all the way through the recovery, this time, it flattened out in about 2011. Whether you look at with aircraft or without aircraft, it doesn't matter much. And so, for a period of three or four years, businesses were not investing more in their business, and this was not growing. And this contributed to the slow recovery that we saw. Ron?

Ron: Even in nominal dollars, if you take 2% inflation out of this, you would've seen a gradual decline.

Jeff: So what we were interested in seeing was, when business optimism jumped in late 2017, was that going to translate into increased spending? And in fact, we've seen a little bit here at the tail end of this chart, which ends in 2017. And anecdotally, we're hearing more of that from businesses as we listen to them on their earnings calls here recently. So this is an encouraging chart, and we're kind of pleased to see this come about.

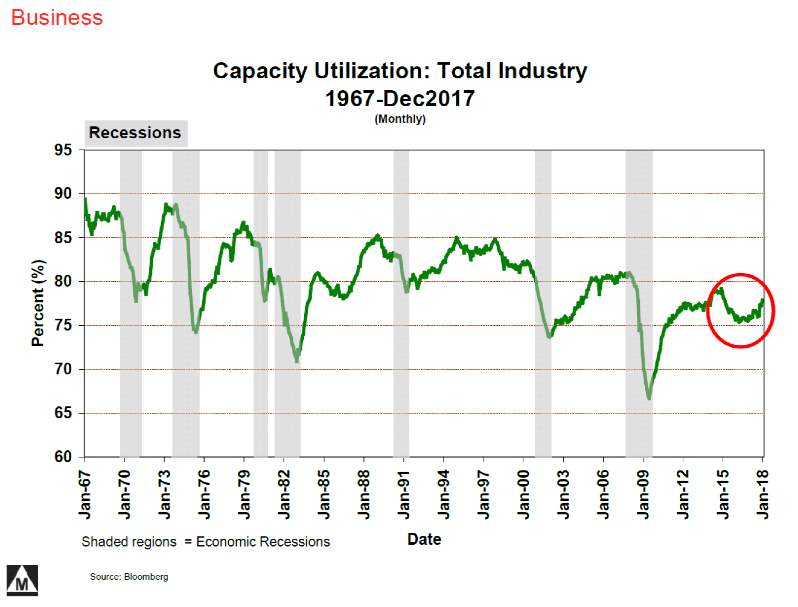

Jeff: And this is a graph of Capacity Utilization: Total Industry in the U.S. since 1967. And as usual, gray bars mark recessions. Capacity utilization picked up if you look way out here at the tail end. Normally, what happens is capacity utilization falls in a recession. Coming out of the recession, it picks back up. But it's not until you get to about 80% utilization that companies start to invest in their businesses again because they don't need to before then. They've got ample personnel and ample equipment to meet the demands of their clients, their customers. We never got there [to 80% utilization], which explains why businesses never started investing in their business, which was that flat line we just talked about a minute ago. And in 2016, it fell off again, but down to this trough here and declined. So we were looking for: is that going to start picking up, and is that going to cause businesses to have a need now to start expanding capacity? And the answer is: it's starting to, but it's still not to that kind of almost magical 80% level where it starts to become even more critical for that business. But this is an encouraging sign, and we're happy to see it.

Let's reflect a little bit on what we've said on this business spending topic over the last year. Nine months ago, we said we were seeing a disconnect between measures of business and consumer sentiment (which were both rising), and business activity and spending (which wasn't doing much). So the optimism was going up, but the spending wasn't. We told you then that we didn't know how that disconnect was going to reconcile itself. Six months ago, we kind of opined that it was more likely that the optimism would pull back than that the spending would pick up because we weren't seeing, as Ron highlighted, the facts on the ground starting to support that optimism. But we were wrong in that assessment. So what we finally saw in December was we had the changes in tax policy and we had kind of a cumulative effect of changes in regulations. So now business is confident that, in fact, the rules have changed to allow them to start expanding again, and they're doing that. So you've started to see business spending pick up to match the optimism which has remained high, and that's why we changed our characterization of what we thought business spending was going to do both currently and in the near future. But that's kind of what we've told you about that very important topic over the last year or so, and where we've been right, and where we were not quite right.

Ron: We'll call it wrong.

Jeff: Wrong. Well, a little doubtful.

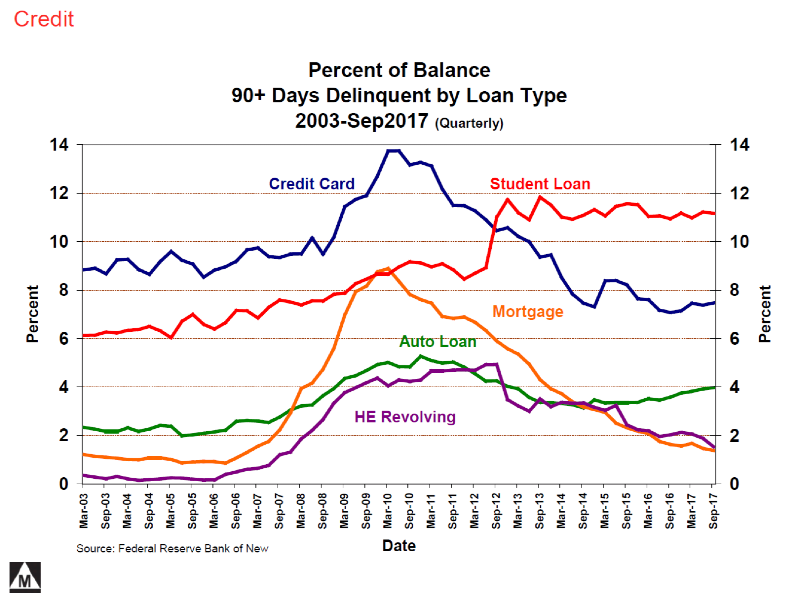

Jeff: Now, looking at credit metrics. We like to look at credit metrics. Sometimes you can get an early read on what's going on. This is a chart from the Federal Reserve Bank of New York. They update it quarterly and it shows the percentage of loans by category 90 days or more delinquent since 2003. So if the line goes up, that's bad because you have more delinquencies. If the line's coming down, that's good, you have fewer. So in one picture, you can see where the delinquencies are declining, and that's mortgage loans and home equity lines of credit; you can see where they're steady, which is pretty much here in credit cards and student loans - so even though student loans jumped up big time in 2012, they've remained steady since then; and where delinquencies are increasing, so credit is deteriorating, and that's here in auto loans. And that's kind of gradual. But frankly, it's at a higher level than it was pre-recession, and the trend is not encouraging. So six months ago, we were a little bit worried about credit cards because they came up a little bit, but now they seem to have leveled off. So it looks like they're just wiggling a lot in this range. We'll be watching to see if that changes, but auto loans still have us a little bit concerned. But that's the credit picture, if you will, for the consumer, and it's not bad.

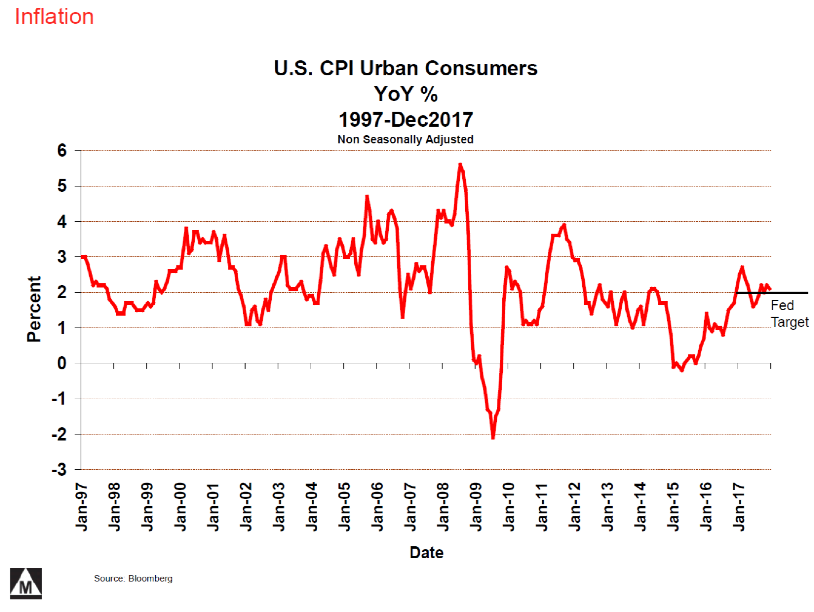

Jeff: Shifting to a discussion of inflation, the direct measurement of inflation is by pricing a basket of goods and services and seeing how that changes over time. Here we have a graph of the Consumer Price Index (CPI), Urban Consumer, since 1997. That's a data set kept by the federal government. You can see that since the recession, it's averaged probably 1.5%, maybe two percent. Here we've put in the Federal Reserve Bank's target, which is 2%. So in 2015, 2016, we almost got to deflation. We had no inflation for about a year. We're back up in the 2% range.

Ron: When we talk about 2% inflation in the last eight years, these are the numbers we're talking about.

Jeff: But what the Fed has said is we want to see 2% inflation. They're getting 2% inflation, so they're starting to withdraw some of the very extraordinary measures they had put in place to support the economy (their term, not my term) prior to that. And we'll talk about what the Fed is doing here in a moment.

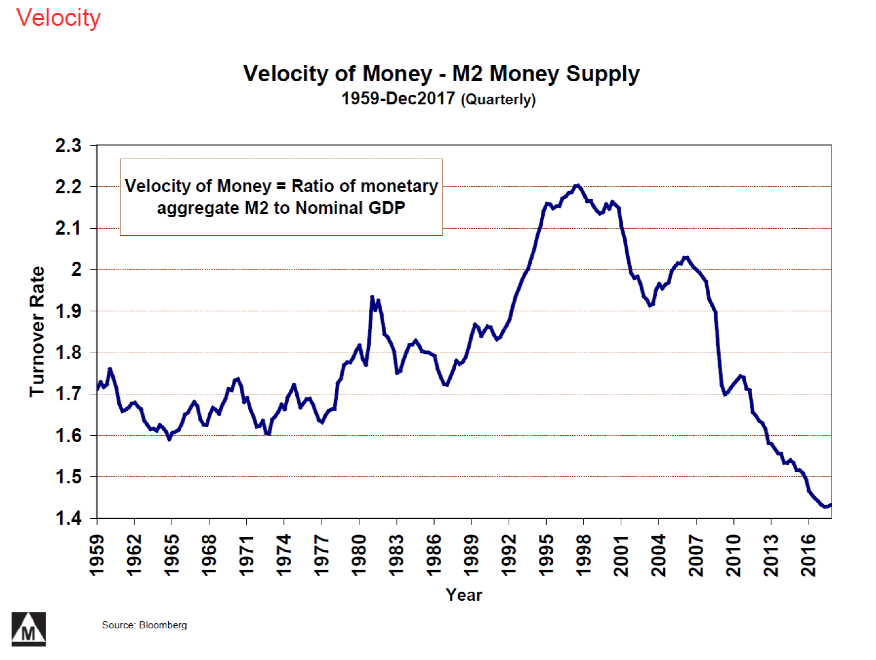

Jeff: We also keep an eye on the velocity of money to help us keep an eye on inflation. And velocity of money really became interesting post-2009 when it collapsed. At a conceptional level, velocity of money is the turnover of money in the economy, but you really can't measure that directly. So what we end up measuring is the quantity of money in the economy and the quantity of goods produced, and then you calculate the number. So it's not an observed phenomenon, it's a calculated number. As long as you have declining velocity, it's going to be very difficult to get inflation, even if you keep printing money. And that's the situation we've seen for the last eight years. And to a certain extent, the surprise for a lot of folks is the fact that we have collectively, both in the United States and overseas, printed so much money and yet gotten so little inflation. And so, all the central banks desired inflation, printed lots of money, and yet have been disappointed with the level of an inflation they got.

Ron: If you recall in '09 and all the various QEs (Quantitative Easings) when the Fed printed money. A lot of commentary and lot of markets assumed that inflation would run up. On this chart, you'll see going back in the ‘60s and the ‘70s, velocity was pretty much constant. If velocity had stayed constant, we would have gotten inflation from that printing of money, but what happened was the velocity collapsed. The money sat in bank vaults because, frankly, the business and consumers weren't interested in borrowing, and the banks, having had bad loans come home to roost in '08 and '09, weren't interested in lending. So despite the fact that the Fed put all the money out there, the visual representation of what happened is this velocity of money. But it was a surprise to a whole lot of people, I think, to some extent, or to a large extent, including us. So this is a way of trying to monitor what's happening with that money that's been put out there.

Jeff: If we started to see velocity level off or picked up in a meaningful fashion, that would increase our expectation for higher inflation. So that's, frankly, why we're watching.

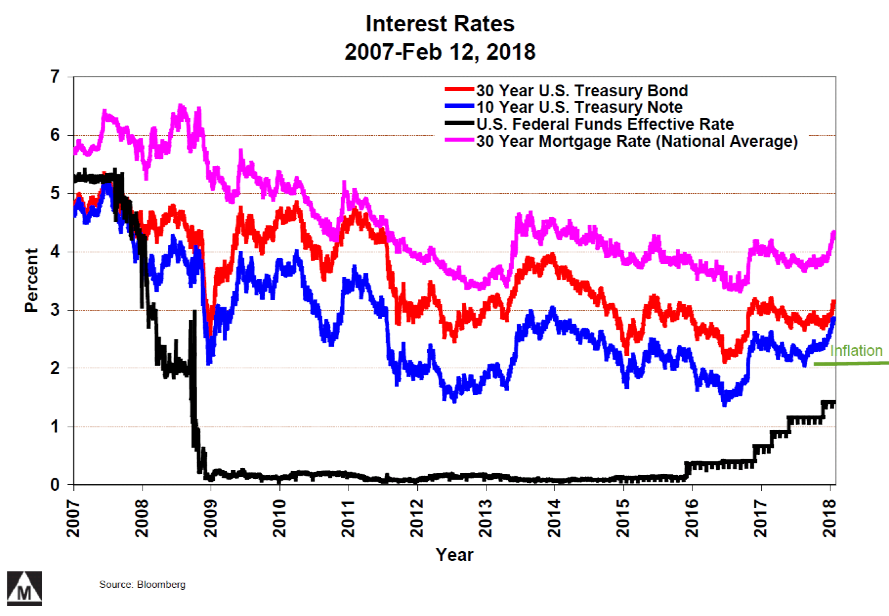

Jeff: Moving on to interest rates. This is a chart of the U.S. Federal Funds Effective Rate which is directly set by the Fed, and you see it here in black at the bottom. So the federal funds rate which they set has started to go up in late 2015. It's currently at about 1.5%. We and the markets expect that it's going to go up about three more times this year. Above that, is the 10-year U.S. Treasury Note rate in blue. You can see that, frankly, really since about 2011, it's been more or less 2%. Although, very recently, it has started to march upward pretty significantly joined by the 30-year U.S. Treasury Bond rate in red right above it and the 30-year mortgage rate in pink above that. So the concern had been, really from about 2016 through the middle of 2017, that short-term rates were coming up and yet long-term rates were not. And so towards the later end of that period, you started to get a lot of concern in the financial media about the flattening yield curve and about the potential for an inverted yield curve because the spread between short and long term was declining. Well, what you've seen here recently is the long-term rates have started to pick up, so you're no longer concerned about inverting the yield curve as much. But what has happened is you've got a new concern that everybody is talking about: Gee, inflation is imminent, and long-term rates are going up. And because inflation is running, we're going to see the Fed start to tighten even more quickly and choke off the economy because they're afraid of inflation. And so you have one fear replaced by another fear. Frankly, I'm not sure either, based on the inflation chart, that you're seeing a big ramp in inflation yet because, frankly, we saw this in '10, we saw this in '12, and we saw this in '13. Here we are in '17, I'm not sure that indicates a big ramp in inflation.

And, it's our opinion that, historically, long rates have normally been two to three percent above inflation. Well, if that's the case, if inflation is here at two percent (highlighted for you in green in the chart), you ought to see the 30-year in the neighborhood of four to five. And that would be historically normal.

Ron: Specifically, the short-term rates, historically, have equaled inflation. So the short-term rate at the bottom can come up another 75 basis points to equal inflation. Long-term, the 30-year rate had been 3% above, but that was also a time when the economy was growing at 3% real. Some economist believe that, going forward, we can only grow at 2%. They believe we can't do better than 1% productivity, which I disagree with. But the argument is: if the economy can only grow at 2% real, then the 30-year should be at inflation plus two. If we got back to a 3% real, by that theory, it should be 3 plus 3. Now, as I say, those have been the numbers historically. So there's a whole lot of economic theory that says that that is fair. Once you get a new set of numbers that defy the old theory for 5 or 10 years, people start treating that as a new theory. But there's a whole lot of economic theory that says short-term rates should be equal to inflation. You should be able to offset inflation in treasury bills, pre-tax. And that, long-term, the interest rate should be roughly what the growth in the economy is. Otherwise, the borrower makes out at the expense of the lender. The point of all this discussion is that rates can go up another three-quarters of a point to a point to get back to a normal. We do not view that as tightening by the Fed, we view that as allowing rates to get back to normal. If they start moving above that, then we kick into the mode of “gee, the Fed is tightening,” and that has different implications for us. And we'll talk about that if it occurs in the future.

Jeff: And with the point being, people are seeing the move in rates as a sign of inflation. We're not sure. In fact, we're skeptical of that. We see the move in rates as going back to the historical-normal spread over inflation. So you had a 10-year period of rates that were too low by design. That's simply going back to normal. That doesn't have us concerned yet.

Ron: Frankly, that would allow the individual to make some return on their savings account, and it would allow pension funds to make some return on their bonds, which have been hard to come by the last seven or eight years.

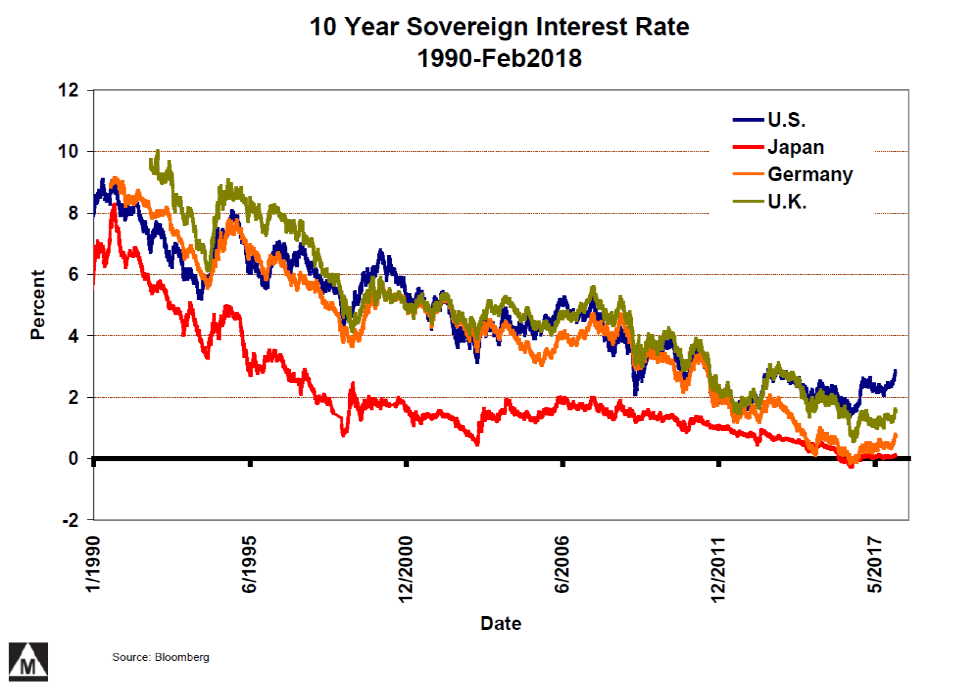

Jeff: Looking at the same topic from a global perspective, this is a chart of the 10-year interest rate on sovereign bonds since 1990 from a global perspective. So you've got the United States here in blue, Japan all the way at the bottom in red at zero, Germany in orange at about .5%, and the United Kingdom in green at about 1.5%. So the phenomenon of rising rates is not unique to the United States. With the exception of Japan, everybody in the last six months or so has seen a pretty rapid increase in rates. But that's from a repressed level. And so the European Central Bank and, to a certain extent, the British Central Bank have intentionally kept rates abnormally low, and they're starting to move up. Nonetheless, that is a big change, and investors shifted over the last 10 years how they invested based on those abnormal rates. So as they come back to "normal", you should expect to see shifts again, and so it could be turbulent.

Ron: Why do we care about foreign rates? For instance, Japan, two years ago, took their rates to zero, and it changed what their insurance companies and banks invested in. They started investing to a greater degree outside the Japanese markets—read that as: they started investing to a greater degree into the U.S. bond and stock markets. And, of course, that affects our prices as well. So you can no longer ignore what foreign countries and companies are doing if you're trying to figure out what's going on in the U.S. market.

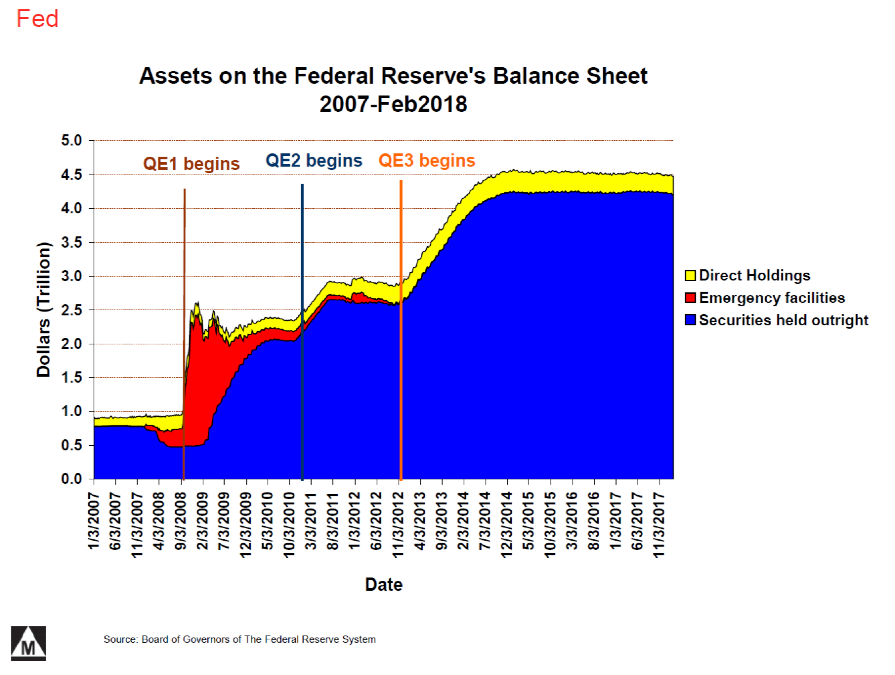

Jeff: So the Fed is raising short-term rates, which they've been doing since the end of 2015, and so far, it has not affected the markets or the economies too much. In June of 2017, they announced a plan to reduce the size of their balance sheet by not purchasing replacement bonds when their existing holdings mature. They're going to allow a portion of their bond portfolio to “run off” going forward. They started in October by allowing $10 billion in bonds to run off that month, and that will accelerate to $50 billion a month in 2018. So what they had done, as a result of the great recession, is they printed money, and bought bonds, and expanded their balance sheet from one trillion to four and a half trillion dollars over the course of about four and a half or five years. And now, we think that was part of what was responsible for the rise in prices of stocks, and bonds, and real estates, and frankly, a whole lot of assets. So they unleashed a wave of money that bid up prices in a whole bunch of different markets. That's not the only thing that contributed to it, but we think it was a contributor. So now they're saying, "We are going to start to shrink that supply of money that we have pushed out into the banking system and the economy. We're going to do that by not re-investing bonds as they mature." So the expectation kind of has to be that, as they start pulling money back, isn't that going to affect the prices of all these markets that they helped kind of inflate over the last five or six years? Isn't that going to deflate or decrease the prices? That is the risk. So far, you can't see a decline in the size of the balance sheet at all. At some point, we think it will probably have an impact. They expect to get down to $2 trillion out here in 2020, so they're going to do a slope about like that, is what they've said they're going to do. So that's a risk. What we just told you, really, over the last eight or ten slides is that we have reasons to be more confident about the growth in the economy than we were nine months to a year ago. And mostly, that has to do with regulations in tax policy and the response of both consumers and businesses to those changes. So we're a bit more optimistic, Ron probably a bit more than I am, but we're a bit more optimistic about economic growth.

Ron: And corporate earnings…

Jeff: And corporate earnings. What we are more pessimistic about is the price of the markets because now you have this countervailing force, if you will, as the central bank shrinks the dollars that are available out there to be invested in these sorts of things. And so, again, when you reverse that flow, instead of pushing money into the system, you're now pulling money out. Our expectation is that's going to have a dampening effect at best on the price of assets. Now, what the Fed has said is, "Well, we're going to tell you exactly how we're going to do it. We're going to tell you when we're going to do it." And they're trying very, very hard to reduce the size of their balance sheet without creating problems in the markets. And maybe they'll be successful with that, but maybe they won't. And it's not at all clear how much pain they are willing to tolerate in the bond and the stock markets before they change their plan and do something a little different. So you saw them, in the taper tantrum in 2015, change their plan. You saw them, in 2016, change their plan. You saw in February, when we had a 10% correction in their market, they reaffirmed the plan. So apparently, 10% doesn't meet that threshold. My guess is they have a threshold. I have no idea what that threshold is, but I think it's there.

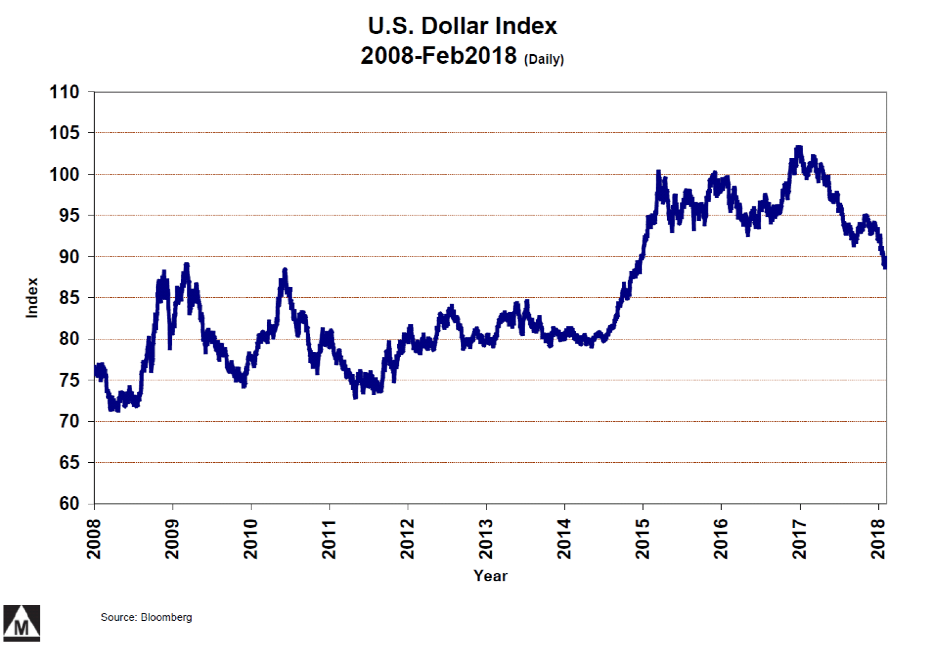

Jeff: Although it's not on the checklist, we’re going to talk very briefly about currencies and exchange rates. This is a chart of the dollar versus a basket of other currencies, chiefly the euro, the pound, and the yen. When the line goes up, that's when the dollar is strong versus other currencies. When it goes down, that's when it's weak. So what you've seen is a fairly stable dollar versus those currencies from '09 till about 2014. Then you had a strong dollar, which was beneficial for the U.S. consumer of imported goods, but any U.S. exporter saw a reduced earning power based on translating this foreign sales back into dollars. That stabilized for two or three years, and now it's coming back down. Ron?

Ron: Well, and so now, there's a couple things going on. The change in the tax law, the change in regulations, and the weaker dollar means that it benefits U.S. producers of goods, particularly those who are selling to other countries. If the dollar comes down 10%, it means our goods are 10% cheaper in Japan, or Europe, or what have you. So don't be too surprised if you see further moves by companies to build plants in the U.S. rather than foreign. It does squeeze the American consumer and, of course, anytime the dollar moves, you hear from the people who are getting squeezed. When the dollar goes up, the businesses complain. When the dollar goes down, you will start to hear consumers complain. The other part of this is you saw the spread between interest rates between U.S. treasury bonds and foreign sovereign bonds. When the dollar, at some point, will cease to go down. That means that the U.S. treasuries will look much better than domestic yen bonds or domestic eurobonds to the people in those countries. So you always have this—it's very seldom that there's one thing that's driving any given part of the market. And the major things here for the currencies is the inflation, and the flows, and the relative interest rates. Right now, U.S. rates are higher than others. While the dollar is going down, that discourages people from buying our treasury bonds. When the dollar levels off, or if it begins to go up, that will encourage them to buy our treasury bonds.

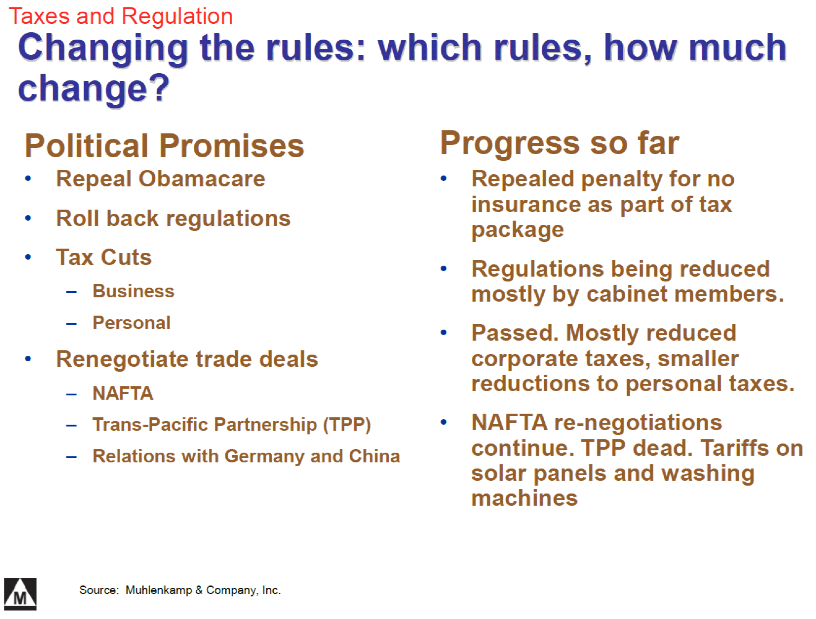

Jeff: Finally, we're going to kind of summarize what's been going on with taxes and regulation. We've used this slide for about a year to keep track of the differences between what was promised in the 2017 election and what we're actually getting. What we've seen so far is that there has been some progress made on reducing regulations. Mostly, that's a personnel-equals-policy kind of a thing. The folks that President Trump has put into cabinet positions have pretty uniformly been interested in reducing senseless regulation, and streamlining what the government does, and getting it out of businesses that it should not be in. And so that's having a gradual effect that we think is largely beneficial. The only portion of the repeal & replace Obamacare initiative that actually made it into law was the end of the penalty for not carrying healthcare. That was the individual mandate, and that got bolted into the tax reform that we saw in December.

Of course, we got tax reform in December. On an international basis, there was a lot of concern early on that Trump would be protectionist and would bail out of NAFTA. He did, of course, end the Trans-Pacific Partnership deal that was never signed into law, and it's dead. And NAFTA is being renegotiated. It's not quite clear what's going to come out of that. That's an ongoing process, and we have no predictions for you on that. What we have seen is a couple of tariffs get enacted. So there's been a tariff enacted on imported washing machines, imported solar panels, and there's now kind of teed up for the president a decision on whether or not there's going to be tariffs on aluminum and steel imports. So he had asked the Commerce Department to look at that. They have made some recommendations. He has 60 or 90 days to make a decision, and that's on his desk.

Tony: We actually have a question on that, on the tariffs, in terms of the implications that have been suggested. We wrote a paper when I first started here titled ”How We Benefit From Free Trade.”

Ron: Right. One, we think it would be a mistake. If there's a tariff on washing machines, it means the price of washing machines just went up. Now, if you're a producer of washing machines in the United States, you're probably in favor of that. But if you're a consumer, the price of washing machines just went up. Price of solar panels just went up. If you get tariffs on aluminum and steel, of course, they get pretty broadly spread throughout. So the steel industry would like it, but the auto industry would not because the auto industry's a consumer of steel. We continue to think that tariffs are detrimental in general. They're designed to help individual industries, and we understand why those industries would like them, but we think it's a mistake.

Jeff: And if we get into a tariff war—which is to say that our tariffs prompt other people to run up their tariffs, and you get this back-and-forth kind of a Hatfield and McCoy kind of feud, then it gets truly dysfunctional from an international trade perspective and that is a risk.

Ron: One of the things that happened in the Great Depression was that various countries put on tariffs and ran their tariffs up, and international trade, within a three-year period, dropped by two-thirds. So the price of domestic goods went up. Of course, your income didn't, so things got a whole lot more expensive and, simply, buying shut down. The one thing that's out there that economists agree on, is that free trade benefits the consumer. Any restriction on trade, whether it's a tariff, or a quota, or anything like that, is designed to benefit a particular producer, but it will always cost the consumer. And whether we put tariffs on or whether it's someone else, it still raises the price to the consumer. And, of course, the great advantage of free markets is the consumer's in charge, the producer is not.

Tony: To the extent that markets are free. Right?

Ron: …to the extent that markets are free, the consumer benefits.

Tony: Good. Thank you

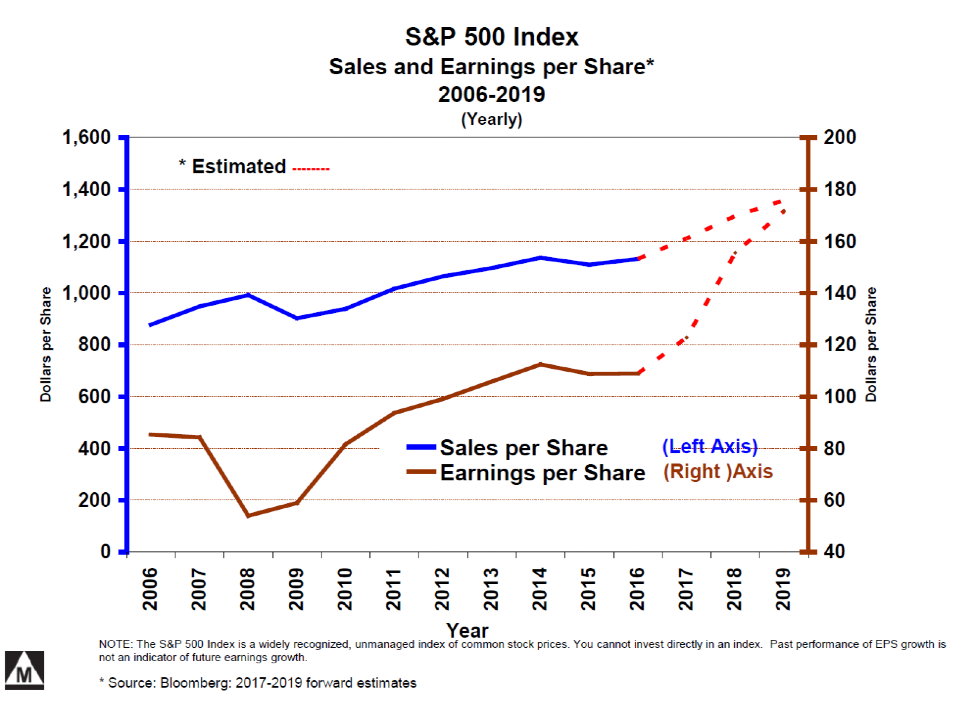

Jeff: Okay. Moving on. Now we are at the end of fourth-quarter earnings from 2017, so we'll give you an update on that. This is a plot of aggregate sales per share in blue and earnings per share in brown for the S&P 500 companies since 2006. The estimates for both earnings per share and sales per share are the dashed lines. And, since we just haven't quite gotten the end of 2017 in there, you'll see 2017 is a dashed red line for both of those even though they're pretty solid because we know about 99% of the numbers at this point. So what you saw for the last couple of years here in 2014 when oil prices declined and the dollar ran up, you saw sales per share and earnings per share decline. So that was both the pain in the energy industry and a decline in the profits of exporters (guys like Microsoft, and Intel, and those sorts of folks). And that leveled off in 2015, early 2016, and started to reverse in 2017. A lot of that, again, was energy. This big ramp here is the impact of the tax law changes. So what we've seen as a result of the changed law is everybody that had money parked overseas took an 8% hit to their earnings because that was the immediate impact from an accounting basis on that overseas money. Now, on a cash basis, they've got six or eight years to actually pay that 8% tax on it, but from an accounting perspective, it hit immediately. So all of the companies reported that, and then they reported what their lower tax rate going forward was. Typically, we saw a decline of something on the order of 5-10% in the tax rate for most companies. Some of them were very tax efficient, only saw a little bit of improvement.

Others that were much more domestically oriented had a larger improvement, but that's kind of what you've seen.

Ron: A couple observations on this chart. First, you'll notice that on the solid line, sales per share were about $1,100, which is the left-hand margin, and earnings per share are about $110. So earnings to sales is about 10%. The second thing you notice, of course, is estimates for the next two years are up in sales and up dramatically in earnings. If you believe this, it's still time to buy cyclical stocks. I don't believe these numbers. These are kind of what happens if nothing hits the fan, and anybody over five years old knows that something always hits the fan. So I don't believe, particularly, the earnings numbers even if I believe the sales numbers. This is part of what got priced in the market in the last year, is that the next couple years will look pretty good. And the ongoing thing is: we believe that what's happening on the fiscal side with lower tax rates and somewhat lower regulation, that it will extend this expansion. The whole question is how long and how far. Wall Street always expects sales and earnings to be up, well, it was 2% inflation, 1%, so you expect 2-3% growth, but I don't believe the earnings numbers. And the whole difficulty of the next several quarters, or year, or two, is: at what point does that roll over? But this is a pretty good proxy for what the estimates are at the present time.

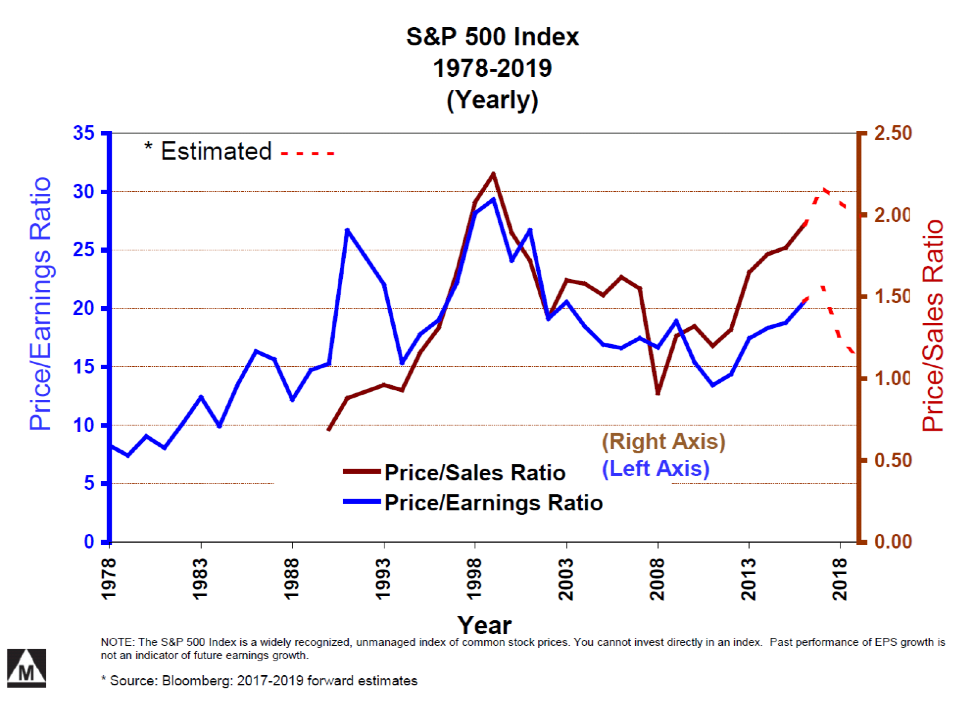

Jeff: What you've probably been hearing, really, for the last year or so is that the market is expensive. And this chart is designed to allow us to talk about that. So the blue line here is the P/E ratio of the S&P 500. The brown line is the price-to-sales ratio. What you saw, of course, is that they hit a peak back there in 1998 with the dot com bubble. And if we'd have showed you the version of this from three months ago, we'd have been back at that peak. But what's happened since then, of course, is you've had a 10% correction in the market, and you had a big jump in earnings compliments of the tax law changes, both the actual 2017 earnings, because that was a little bit of it, and then the 2018 earnings estimate. So this doesn't look quite as scary particularly going forward as it did. But you're still at historically elevated prices relative to both sales and earnings.

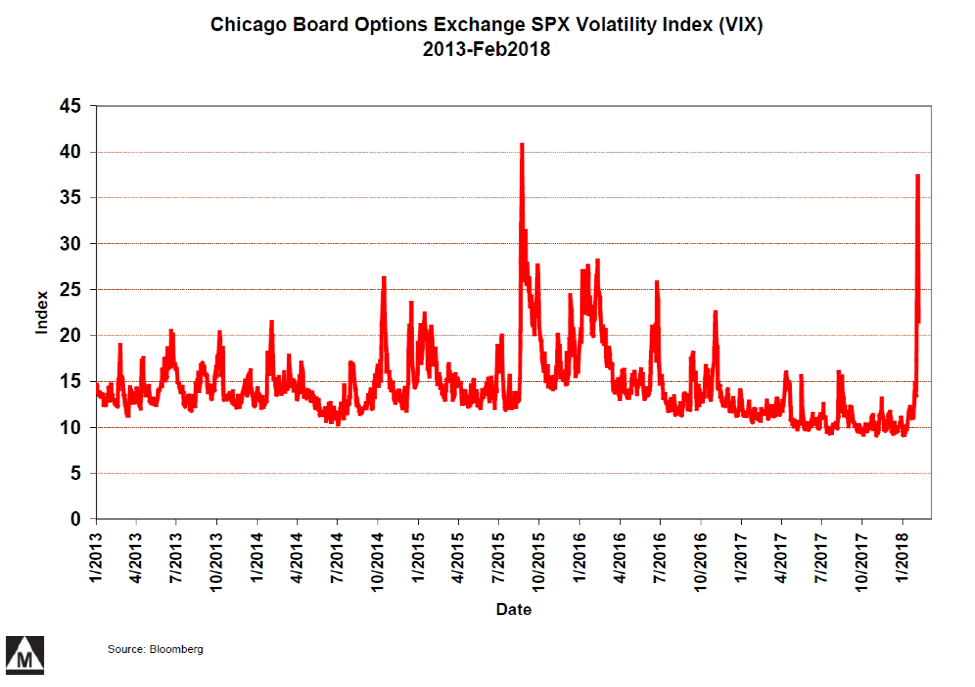

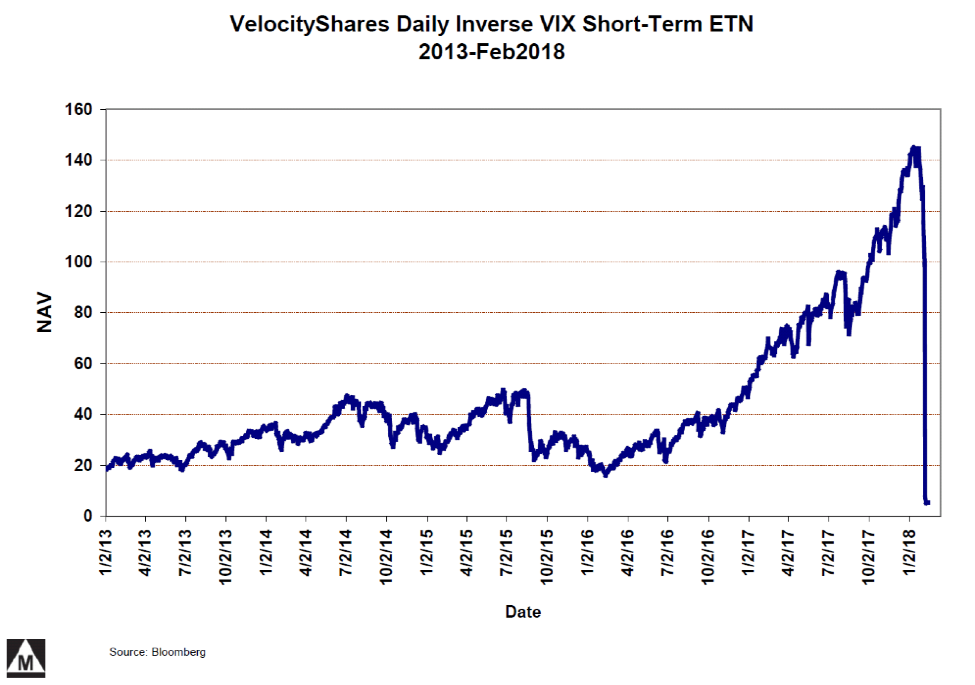

Jeff: I'm going to talk about something that happened in February a little bit, and that was the demise of some financial products that sold volatility. So this is a chart of the Chicago Board of Options VIX index, which is their measure of volatility in the market. A number of financial firms created products that allowed investors to buy investments that either matched the performance of the VIX (so you could be long volatility), or tried to match the inverse performance of the VIX (so you could be short volatility). What you saw was the long products had a structural problem in that, over longer periods of time, they always lost money no matter what the VIX was doing and the short products tended to gain money no matter what the VIX was doing, whether it was steady or just going up a little bit. And so there developed a very popular trade of being short the VIX because you made a little bit of money all the time, particularly since 2015 as volatility came down. But what you saw in early February is a big spike in volatility, and what that did to these short-volatility products is it killed them.

Jeff: And so this is a chart of the inverse VIX exchange traded note, which is similar to an ETF, and the differences aren't too important for this discussion. And you can see that if you were short-volatility, you had a great run there from '13 to '15. You had a great run from '16 right up until about a month ago, and then you literally lost all your money to the point that the price of this product declined so much that it triggered clauses in its foundational documents that forced it to go out of business and fold. And that happened to a couple of different instruments.

There were a number of similar strategies that weren't necessarily so extreme that had been adopted by hedge funds and others that made them short volatility. So as volatility ran up, they were now too exposed to it, and they ended up selling. One of the things you could do to reduce your exposure to volatility is to just sell stocks. And so we think that there was some bleed-over into the equity markets from what was going on in the volatility aspect of things. And what we always watch for is any sign that that's going to take on kind of a reinforcing aspect and start to accelerate kind of for mechanical reasons. So while you wouldn't expect it to, sometimes you can get forced selling (we've talked about that in the equities before) triggered by things that aren't necessarily germane to the equity market, but we did not see that. And so we think that what happened to these volatility products probably played a little bit in how dramatic the downturn in the market was in February, but it's kind of washed itself mostly out, and we don't think it's going to be much going forward. Ron, did you want to talk about that?

Ron: We've got a couple of questions on ETFs. We did work years ago when it became popular, and what we concluded was that an ETF that approximates an existing market, whether it's an S&P 500, or individual stock, or something, tended to act in reasonable fashion to the extent that they made what I call artificial ETFs, something that was either inverse, an inverse ETF, or a multiple. You can get ETFs that are designed to track two or three times a given index or a given stock on a daily basis. Those, over time, eat their young. And as you saw here, if you were short-volatility, that is artificial. There is no short-volatility market. It was an artificial thing set up by brokers, frankly, just to satisfy customers who wanted to make a bet on this. What you saw in early February was volatility went up 100%. The short went down 100%, which is what this blue line's all about. It looked pretty good. There's an old saying of picking up nickels in front of a steamroller. Well, if you were short-volatility for the last five years, you picked up a lot of nickels. And then you got steamrolled in the first week of February '18. We've also been asked whether we use ETFs. In the past, and to some extent the present time, we've used a few. We've used one when we wanted to invest in gold. We simply bought a gold ETF rather than, for instance, a spread of gold stocks. We own one in a number of accounts that only owns stock in companies that are repurchasing their shares at a fairly rapid rate. We think that's a rational strategy, so we own an ETF there. We have, on occasion, owned one that is an MLP (Master Limited Partnership), except to the investor, you don't end up having to file the K-1. So it takes some of the IRS or the tax aggravation out of owning MLPs. We looked at one for China, and decided we found a couple of Chinese stocks that we own or prefer in lieu of that. If we wanted to buy in India today—you saw earlier that China and India economies are growing faster than ours—that would be a place that we would look. So where we see a particular desire for a strategy and an ETF that matches that, we will own them. We see no reason to own those that are artificial because, as they say, they eat their young. And most of the time, we'd rather simply own a stock in a company or a bond of a company rather than be one step removed, which means you pay one more fee for something that Wall Street has created to help the gambler’s fixing.

Jeff: Let me expand on that a little bit. So when you talked about when we were interested in investing in China, we had looked at an ETF. And the reason we didn't go with the ETF is because whenever we look at an ETF, we look at what's in it. And what was in it was a lot of Chinese banks, which were completely uninteresting to us. So when we get a new client, and sometimes they'll come in with assets, and those assets will be in ETFs, the very first thing I do is I go run a sheet. What's in this thing? That's my first question. What's in this thing, and do I like what's in it? And the second question I always have is, what is it charging me? So some ETFs are quite cheap, and they're charging a couple basis points. Some of them are fairly expensive, and they're charging you a percent or a percent and a half. You can't just look at the title of the ETF and know what's in it. Sometimes you look at the title, and then you start digging into what their actual holdings are, and you get really surprised. So to me, whenever you start talking about ETFs, the first thing is, well, what's in it? And that's always the first thing that we look at.

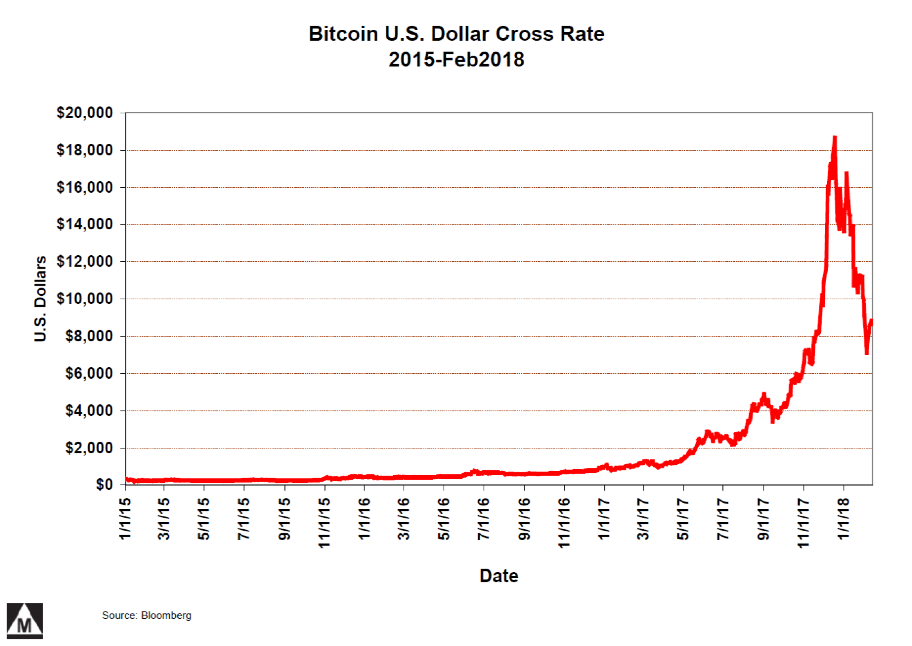

Jeff: So, the other very popular trade that just blew up, of course, was cryptocurrencies. This is a chart of the price of Bitcoins in U.S. dollars since January of 2015. And you can see that it created a lot of billionaires, and Forbes just featured a whole bunch of crypto-billionaires in their latest edition. And they're probably half as wealthy as they were after the last couple of months. But you had a classic bubble.

Bubbles happen in cryptocurrencies, and it's probably about halfway towards being done. We view the popping of the Bitcoin bubble, the crypto-currency bubble, and the popping of the volatility bubble as positive because there was this excess, this speculative excess in the markets, and it blew up. And it didn't really affect the broader or bigger markets, which is always kind of a concern. There are linkages sometimes between them that you don't expect, and so you're a little bit nervous when one blows up, well, gee, is it going to have a knock-on effect in the market that I'm personally invested in and cause me problems? And so we think things did get way too frothy in both of those markets. We think it's a positive that they blew up. We think it's really positive that it didn't have much of an impact on the equity or bond markets.

Ron: The Bitcoin was obvious to everybody. The VIX was a little less so. We were aware of it and, of course, there could be some other things out there that are getting speculative money. There are none quite as obvious to us as Bitcoin was, but that always remains true. But when you pop a bubble and it doesn't kill the rest of the market, that's a healthy thing.

Jeff: If you're one of those folks that bought Bitcoin at cents on the dollar and got out at anything above $1,000, our hat's off to you. Congratulations. Hope you enjoy it.

Ron: If you can demonstrate how you did that, we would be interested in hiring you.

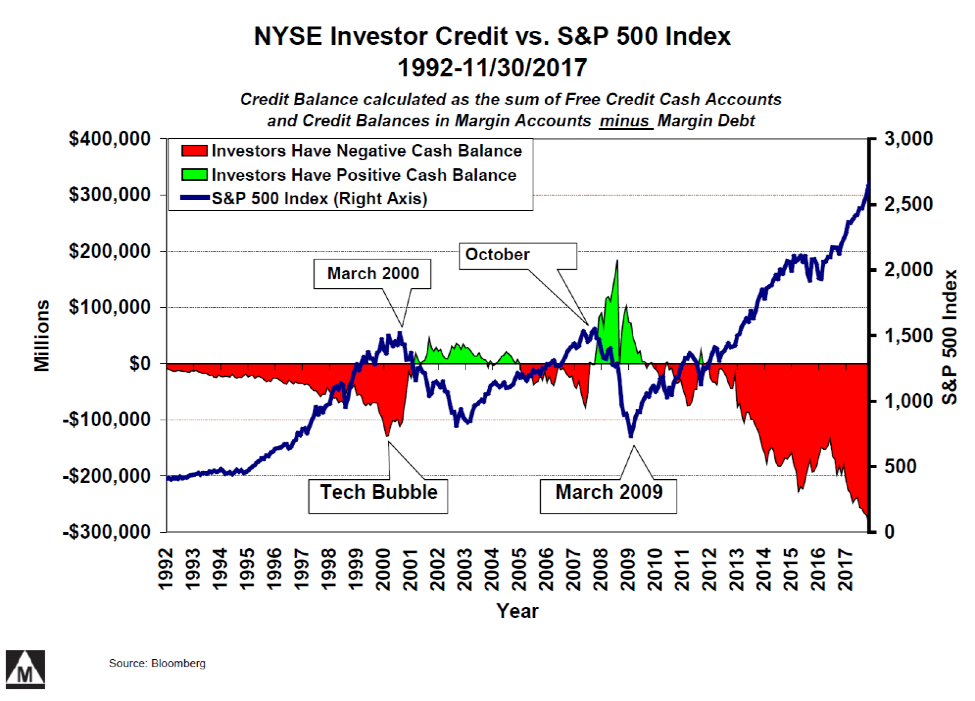

Jeff: And then, finally, this is a net margin chart that we periodically put up here. We find it useful to keep tabs on whether the market is net in debt or net in cash. You've got two lines here. The blue one is the S&P 500 since 1992. This other narrower line [in black] is the net margin line. So when the shaded area under the line is red, that means investors have borrowed against their stock holdings. When it's green, they are net in cash, and so it's a pretty good indicator, really. As the margin starts to come out, of course, you're going to drive the market down. When you start borrowing again, you're starting to drive the market up again. And the timing of that isn't perfect, but what we theorize in '08, '09 was that there were a lot of people that were on margin and whether they wanted to or not, as the price of their stocks declined, they were forced to either post more collateral or to sell their stocks to keep their lender, the bank or the brokerage happy. So it's a mechanical function. The media will talk about, "Well, there's fear in the market." Well, this mechanism has nothing to do with hope or fear. It has nothing to do with that. It has to do with covenants, and agreements, and making your lender whole. So we keep an eyeball on that. If you're in a green period, particularly later in the green periods, those are great times to buy. If you're in a red period, you're not going to get any warning that it's about to decline, but it does give you kind of a cautionary signal, if you will. How much forced selling might there be if something else causes stocks to start to decline? That's a little bit of what this gives a feel for.

Ron: Well, if the decline in the first week of February had hit 15% instead of 8 percent, my guess is some margin calls would have started to tick off, and it could cascade. So it's a vulnerability.

Jeff: Right. And unfortunately, it's lagged by three months, so you don't even see. It is entirely possible that some of the margin came off in February. We won't see it for a little while yet.

So, Tony, before I sum up, why don't you give the instructions for questions, and they can be coming in, and I'll give a quick summary, and then we'll get to whatever questions you’ve got.

Tony: You should be seeing on your screen, ladies and gentlemen, a box or a tab where you can type in a question and send it to us. We're happy to respond and reply to the best of our ability. We've already had one question come in, of course, about the tariffs. In the meantime, I do have some questions here that we can address, Jeff, after you do your summary. We're pretty good at ending at an hour, though, so get right on it.

Jeff: Well, I kind of gave you the summary already, and it was in the annual letter if you got that. But at a very high level, we see two big pressures on the market. Number one is we have some pretty solid reasons, we think, for believing that the economy will continue to do well and perhaps a little better than it had in the recent past. And that's the improvement in regulations in taxes. But we're also seeing, certainly, our Fed is starting to withdraw money from the system, if you will. We've also got the European Central Bank, which has decreased the amount they are putting into their system every month, and they may end that this year. So to the extent that our central bank money printing has fueled prices across asset classes. It's our expectation, and we don't think it's unreasonable, that as that money is withdrawn, and you’re going to see downward pricing pressure on those same asset classes. And how those two pressures interact, we don't yet know. But that's the tension, the conflict we see.

Ron: So what we're doing in the meantime is what we always do. We look for good companies at cheap prices. Our phrase is “we like to buy Buicks when they go on sale.” The average company today has a return on equity of about 13%. Ours are between 18 and 20. The average company is selling 20 times current earnings. Ours is selling about 16 times earnings. So we've got better than average in terms of profitability. We like profitability, and we like growth in sales and earnings. And ours are better than average, at below average price.

Tony: Are there certain areas of the market that you see are undervalued today?

Ron: Large areas? No, it' more of an individual picking.

Tony: There isn't a sector across the board where we can say is cheap, or an industry, or a market, or anything like that?

Ron: No. There are a couple areas that are overpriced, we believe, which is what everybody talks about, whether you're talking about the Amazons of the world. Now, the good growth areas should be tech and healthcare, and we're fairly heavy in those. Microsoft had an 18 times earnings and Apple had a 14 times earnings instead of some of the things…

Tony: Sort of a Facebook, or a Netflix, or a Google at an umpteen times earnings.

Ron: If they get hit, they'll probably all get hit. But in the meantime, we have a little more confidence in the prices of the things we own than some of the other stuff out there.

Jeff: And what we've been telling you for a long time is we don't like bonds. We think they're mispriced relative to inflation. We told you three months ago that we expected rates to go up. They have. We told you that when they went up, bonds would get hit in terms of the price of bonds, they have. We still think that they're mispriced. Not as mispriced, but they're still mispriced relative to inflation. So we're still not in favor of bonds as a way to grow wealth over the long term. And as a holding spot over the near term, that's kind of a different purpose. That's a different story.

Tony: We have had some people ask us about how they should be allocating between stocks and bonds, and frankly, that is not a conversation to have on a webcast, but it's one we're happy to have with you privately. So give us a call and you and I will talk because that's an excellent question. But, man, there's a whole lot of “it depends” that goes into that. So ladies and gentlemen I want to thank you for your attendance and reassure you. We do have questions here we didn't get to, but I will call and see if your questions were answered. And if we've raised new questions, please send us an email, give us a call. My email is [email protected] or you can get in touch with us over the website. We look forward to it. Ron, Jeff, I want to thank you both. Interesting, fascinating. I learned some things, as usual. Ladies and gentlemen, I hope that was true for you as well. Thank you.

Jeff: Thanks, everybody. Have a good night.

GLOSSARY

Central Banks are nationalized institutions, given privileged control over the production and distribution of money and credit. A central bank is generally responsible for the formulation of monetary policy and the regulation of member banks. Central banks conduct monetary policy by manipulating the money supply and interest rates. They regulate member banks through capital requirements, reserve requirements, and deposit guarantees. The central bank of the United States is the Federal Reserve System, or “the Fed,” which Congress established with the 1913 Federal Reserve Act.

Consumer Price Index (CPI) measures the prices of consumer goods and services purchased by households. CPI is used as a measure of price inflation.

Exchange-Traded Fund (ETF) is an investment fund that tracks a commodity, a basket of securities, or an index (e.g. S&P 500, MSCI EAFE), but trades like a stock on an exchange. ETFs experience price changes throughout the day as they are bought and sold.

Gross Domestic Product (GDP) is the total market value of all goods and services produced within a country in a given period of time.

Quantitative Easing is a government monetary policy used to increase the money supply by buying government securities or other securities from the market. Quantitative easing increases the money supply by flooding financial institutions with capital in an effort to promote increased lending and liquidity. Central banks tend to use quantitative easing when interest rates have already been lowered to near 0% levels and have failed to produce the desired effect. The major risk of quantitative easing is that although more money is floating around, there is still a fixed amount of goods for sale. This may eventually lead to higher prices or inflation.

S&P 500 Index is weighted by market value and its performance is considered to be representative of the U.S. stock market as a whole. You cannot invest directly in an index.

Taper tantrum was the term used in 2013 when the U.S. Federal Reserve began winding down its asset purchase program and U.S. Treasury yields surged.

Velocity of Money is the rate of turnover of money in the economy.

The opinions expressed are those of Muhlenkamp & Co. and are not intended to be a forecast of future events, a guarantee of future results, nor investment advice.

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All