Italian general elections were held on March 4, 2018. The election results point to a hung parliament, with no party or coalition winning enough votes to form a government. The election came against an improving economic picture and Italian equities have performed strongly over the last year, outpacing many other developed markets including the broader eurozone and the U.S. We offer the market and political implications of the election below.

Key points:

- The strong performance of populist parties in Italy is balanced against Germany forming a new government. We see scope for pressure on Italian and peripheral eurozone bonds.

- A government involving populist parties might take a confrontational stance against the EU and loosen fiscal policy. We see an increased probability of another election this year.

- At the EU summit this month, the UK will likely seek agreement on a transition deal that avoids a cliff-edge Brexit in March 2019.

Overview

Results of the Italian election point to a hung parliament, with no party or coalition winning enough votes to form a government. The strong showing of populist parties complicates the Italian political outlook but is balanced against a new government forming in Germany.

The right-wing, euroskeptic Northern League (Lega Nord) party, led by Matteo Salvini, is emerging stronger than Silvio Berlusconi’s center-right Forward Italy (Forza Italia) party within the center-right coalition, which also includes the far-right Brothers of Italy (Fratelli d’Italia) party. The independent and also euroskeptic Five Star Movement (Movimento 5 Stelle or M5S) led by Luigi di Maio has beaten poll forecasts and won a greater share of the vote than expected – not enough to form a government, but enough to make it a linchpin in any potential government. Matteo Renzi’s center-left Democratic Party (Partito Democratico) appears to have fared the worst.

We believe it unlikely that Five Star will partner with the Northern League to form a government. The Northern League’s ambition is to lead the center-right coalition rather than be a junior partner in an unstable alliance with Five Star. At some point, an increasingly mainstream Five Star and the Democratic Party may warm up to each other.

Market implications

We see scope for pressure on Italian and peripheral eurozone government bonds but don’t see this as a sustained negative for the euro or regional equities. A new Italian parliament needs to be convened by March 23, yet negotiations are likely to drag on beyond then. Political noise is poised to remain high until a sustainable coalition emerges.

At the same time, a healthier Italian economy looks likely to cushion some of the short-term hit. The Bank of Italy’s real GDP growth estimate of 1.5% in Italy looks realistic for 2018-2019, though ongoing political uncertainty may be a drag. We consider that the debt-to-GDP ratio should start falling from this year.1 Italy’s banking sector appears to have turned the corner and is making progress in dealing with the large non-performing loans on its books.

We now see an increased probability of new elections after the summer. Any government involving the Northern League or Five Star is likely to take a confrontational stance against the European Union (EU), especially on immigration. We believe a government involving those parties would partially roll back fiscal prudence and economic reforms.

European political implications

Although we expect that Northern League or Five Star may take a more robust approach to the EU, we see lower risk of euro exit talk from the anti-establishment parties. The defeat of Marine Le Pen’s National Front in France last year spurred even the most euroskeptic parties to tone down their euro exit talk, and neither the Northern League nor Five Star campaigned on an anti-euro message, focusing more on domestic issues. Anti-European sentiment was largely absent through the election campaigns.

Indeed, weekend developments in Germany may bode well for renewed momentum behind deeper European integration, we believe. On Sunday the Social Democratic Party (SPD) membership voted in favour of a coalition with Angela Merkel’s Christian Democratic Union (CDU) and its sister party the Christian Social Union (CSU). The pro-Europe SPD will take over key ministries such as finance and foreign affairs. The outcome should boost corporate sentiment and could give the European Central Bank (ECB) more confidence in its growth and inflation forecasts.

Meanwhile, a key date on the UK’s Brexit calendar looms: the European Council meeting in Brussels on March 22-23. Expectations are high, especially in the UK, that a transition deal can be reached that would avoid a cliff-edge Brexit in March 2019. Compromise is far from certain, and we see volatility in Brexit-sensitive assets – particularly sterling – rising ahead of the March meeting. Clarity on a transition deal is a key factor for companies deciding on contingency plans. The issues around the Irish border appear likely to be kicked down the road beyond any agreement on a transition deal.

Economic backdrop

Although it lags the rest of the eurozone, the Italian economy is doing well and its recovery from its worst recession since World War II has gained pace. Evidence points to a broad recovery in the manufacturing sector, while the Bank of Italy projected recently that the economy will expand by 1.5% this year and that growth should remain above 1% over the next two years, citing rises in household income and declines in firms’ spare capacity as signals of higher consumption and investment. Public debt has stabilized at approximately 132% of GDP.2

Italy keeps running a sizeable and stable current account surplus (2.8% of GDP).3 Moreover, its net International investment position, though still negative, has improved from approximately 35% of GDP in 2008 to less than 10% in Q3 2017.4 The banking sector, though still overloaded with non-performing loans (NPLs), appears to have turned the corner: The flow of new non-performing loans in the third quarter of 2017 in proportion to total loans fell to 1.7% (even lower than pre-financial crisis level of 2006-2007) and the stock of non-performing loans (net of provisions) fell to 8.4% of total loans in June 2017 from around 9.3% at the end of 2016.5

Conclusion

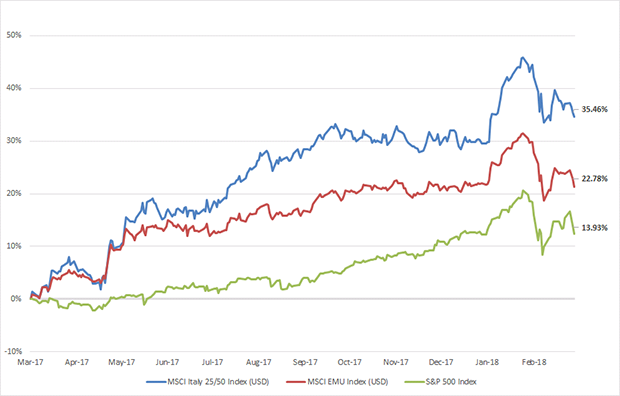

Notwithstanding the muted geopolitical risks, we are underweight European fixed income overall – across sovereigns and credit on account of the ECB’s interest rate and asset purchase policies. Although we are neutral on broad European equities, the fact that fundamentals appear to be on an improving trend may help limit the downside to risk assets. Specifically, Italian equities have outperformed both the eurozone and U.S. equities over the past 12 months, supported by the region’s above-trend economic expansion. Italian equities do not look expensive relative to their historical norms; sitting just above average at their 50th percentile ranking.6

12 Month Index Performance

The bottom line: Regional assets may come under pressure from greater near-term uncertainty, but the fact that economic fundamentals have been on an improving trend may help limit any downside for Italy in the longer term.

© iShares

Read more commentaries by iShares