Gold and the Global Ticking Debt Bomb

Membership required

Membership is now required to use this feature. To learn more:

View Membership Benefits

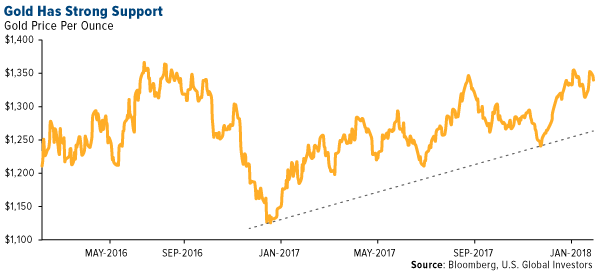

Since its recent high of $1,370 an ounce at the end of January, the price of gold has shaved off about $40 as Treasury yields continue to head north. The yield on the benchmark 10-year T-note is looking to cross above 3 percent, which would be the first time since early January 2014. This is a short-term headwind for the yellow metal that could reverse if inflation continues to rise more than expected, as it did in January. The consumer price index (CPI) increased 0.5 percent from the previous month, against forecasts of 0.3 percent.

Looking more long-term, there are mounting risks involving debt that make gold appear very attractive right now as a safe haven and portfolio diversifier.

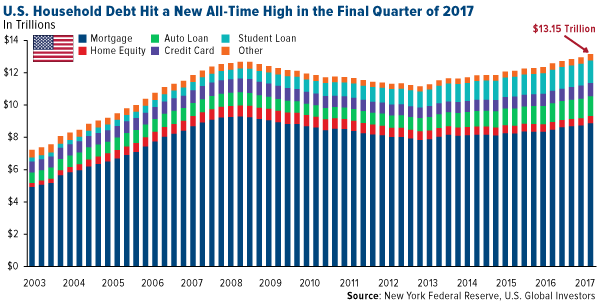

A new report from the Federal Reserve Bank of New York indicates that U.S. household debt rose to a new all-time high in the last quarter of 2017. American families now owe a jaw-dropping $13.15 trillion, or roughly $40,000 per man, woman and child. That’s up 1.5 percent, or $193 billion, from the previous quarter, and up 8.5 percent from the high during the financial crisis.

Thirteen trillion is a head-spinning sum, but we can’t place all the blame on borrowers. For nearly a decade now, the Fed has kept interest rates at historically low levels, flooding the economy with cheap money.

The good news is the rate of delinquency for all debt has fallen to prerecession levels.

But there’s one area that’s worsened since then—student debt, which now stands at nearly $1.4 trillion, the largest type of lending second only to mortgages. At the start of this year, about 11 percent of student debt was considered delinquent, or more than 90 days past due.

fA Global Credit Binge

Americans aren’t the only ones loading up on debt, though. Last month, the Institute of International Finance (IIF) reported that global debt rose to a record $233 trillion in the third quarter, up $16 trillion in only nine months.

As much as $44 trillion is owed by households alone. And in some countries—most notably Switzerland, Australia, Norway and Canada—the amount of debt families have on their balance sheets is now greater than what Americans owed soon before the housing bubble.

All of this news follows an October 2017 report from the International Monetary Fund (IMF) warning that leveraging in G-20 nonfinancial sectors—governments, nonfinancial companies and households—had exceeded pre-crisis levels, presenting “rising financial vulnerabilities.”

Combined with overstretched asset valuations, these debt loads “could undermine market confidence in the future, with repercussions that could put global growth at risk,” the IMF writes.

Time to Add to Your Gold Exposure?

I see this growing debt bomb as just the latest sign that investors might want to consider adding to their gold exposure. The yellow metal has been sought as a safe haven during times of economic and systemic market risk, and I frequently recommend a 10 percent weighting, with 5 percent in gold bullion or jewelry and the other 5 percent in high-quality gold stocks, mutual funds and ETFs.

Since the Fed raised rates in December, the price of gold has been trending up, as it did in the previous two years following December rate hikes. A declining U.S. dollar continues to support the metal, which has consistently been hitting higher highs and higher lows so far this year.

The greenback is expected to remain lower for longer, with CLSA writing in a note to investors on Tuesday that it “is a casualty of strong risk appetite that has characterized financial markets since the start of the year.”

As for the monumental debt load, I can’t say when or whether it might burst. All I can say with certainty is that the bigger it gets, the greater the risk it presents. This, in turn, underscores the need for a reliable safe haven investment, which I believe gold is.

Apple to Purchase Cobalt Directly from Miners

Turning to another metal, cobalt has made stunning moves on red hot demand, rising nearly 180 percent in the past three years. The brittle bluish-white metal is used in the production of lithium-ion batteries, which power our smartphones and electric vehicles (EV), among other things.

According to mining consultant CRU Group, cobalt demand exceeded 100,000 metric tons for the first time last year, and over the next 10 years, it’s projected to grow at a compound annual growth rate (CAGR) of 11.6 percent.

Because around two-thirds of the world’s cobalt is mined in the highly unstable Democratic Republic of the Congo, a supply shortage is likely brewing.

“There just isn’t enough cobalt to go around,” George Heppel, a CRU consultant, told Bloomberg in January. “The auto companies that’ll be the most successful in maintaining long-term stability in terms of raw materials will be the ones that purchase the cobalt and then supply that to their battery manufacturers.”

Automakers aren’t the only ones with this idea. Bloomberg reported this week that Apple, the world’s largest end user of cobalt, is in talks to buy the metal directly from miners, a move that could save the iPhone-maker many billions of dollars.

Although details are scarce at this point, Bloomberg writes that “Apple is seeking contracts to secure several thousand metric tons of cobalt a year for five years or longer.”

One of the miners the company is rumored to be speaking with is Switzerland-based Glencore, the 14th largest company in the world by revenue as of 2016, according to the Fortune Global 500. This would make sense, as Glencore—the best-performing London-listed miner last year, finishing up 41 percent—has been positioning itself as the go-to supplier of not just cobalt but other metals that are used in so-called clean tech, including copper, nickel and zinc.

Glencore Announces $2.9 Billion in Dividends in 2018

Glencore stock jumped more than 5 percent on Wednesday after the company reported phenomenal performance in 2017 that CEO Ivan Glasenberg describes as “our strongest on record.” Earnings before interest, taxes, depreciation and amortization (EBITDA) rose 44 percent year-over year, from $10.3 billion to $14.8 billion, led by higher commodity prices and “enhanced” mining margins.

Sure to make investors happy, the company also declared a distribution of $2.9 billion, or $0.20 per share, to be paid in two installments this year.

The earnings report made no mention of Apple—or smartphones, for that matter—but it did emphasize the high rate of growth in electric vehicle investment, which is expected to greatly benefit cobalt demand.

“Global automaker investments now total more than $90 billion, with at least $19 billion attributed to the U.S., $21 billion to China and $52 billion to Germany,” Glasenberg writes. “Volkswagen alone plans to spend $40 billion by 2030 to build electrified versions of over 300 models.”

Over the next three years, Glencore’s cobalt production growth is projected at 133 percent, followed by nickel at 30 percent and copper at 25 percent.

This year alone, the company believes it will produce as much as 39,000 metric tons of cobalt, up 42 percent from 27,400 tons last year.

Explore investment opportunities in mining and natural resources by clicking here!

Congratulations to Speaker Joe Straus!

|

Every year, the World Affairs Council of San Antonio (WACSA) names a local leader as the International Citizen of the Year for his or her contributions to the international community and for exemplifying global citizenship. I was honored and humbled to receive the award in 2009, and to this day I still think of it as one of my proudest accomplishments.

Last night I had the opportunity to see the award go to Joe Straus, Speaker of the Texas House of Representatives. In an age when partisan divides seem only to be widening, making it more difficult for Americans to find common ground and compromise, Joe is the rare pragmatist who truly serves his constituents rather than an ideology. He’s often been at odds with the more far-right faction of his own party, going so far as to block the consideration of a controversial “bathroom bill” similar to the one in North Carolina that was ultimately repealed.

I’d like to extend my sincerest congratulations to Joe, and I look forward to seeing what he chooses to do after the end of this term. (He announced recently that he would not seek reelection.)

Finally, I’d like to say that I thoroughly enjoyed hearing from the night’s keynote speaker, presidential historian Jon Meacham, whose biography of Andrew Jackson, American Lion, won the 2009 Pulitzer Prize. I was impressed with the scope and depth of his knowledge of not just Jackson but American politics as a whole and the ways in which the office of president has changed over time. He’s also very witty and amused the audience with his impersonation of former President George H.W. Bush, the secret to which, he told us, is to do Mr. Rogers doing John Wayne.

Have a blessed weekend!

Index Summary

- The major market indices finished up this week. The Dow Jones Industrial Average gained 0.36 percent. The S&P 500 Stock Index gained 0.55 percent, while the Nasdaq Composite gained 1.35 percent. The Russell 2000 small capitalization index was up 0.37 percent this week.

- The Hang Seng Composite gained 0.94 percent this week; while Taiwan was up 3.58 percent and the KOSPI rose 1.23 percent.

- The 10-year Treasury bond yield fell 1 basis point to 2.86 percent.

Domestic Equity Market

Strengths

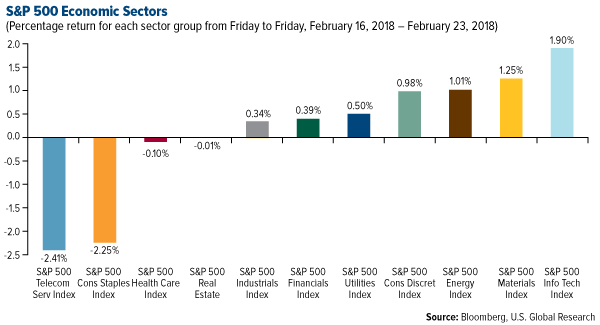

- Information technology was the best performing sector of the week, increasing by 1.90 percent versus an overall increase of 0.39 percent for the S&P 500.

- Chesapeake Energy was the best performing stock for the week, increasing 17.22 percent.

- Rite Aid's stock rose on Monday after Albertsons announced a deal to acquire the drugstore chain in a cash-and-stock deal. The resulting merger will bring in an expected $83 billion in 2018 revenue.

Weaknesses

- Telecommunications was the worst performing sector for the week, decreasing 2.41 percent versus an overall increase of 0.39 percent for the S&P 500.

- Stericycle was the worst performing stock for the week, falling 21.01 percent.

- "Angry Birds" maker Rovio's stock has fallen over 50 percent and is well below its IPO price. The revenue guidance for 2018 has been weak with a maximum of $370 million in forecasted revenue versus the $414 million predicted by analysts.

Opportunities

- The Bloomberg Intelligence Equity Strategy macro model implies a 10 percent gain for the S&P 500 in the year ahead versus bottom-up analyst forecasts for a 13 percent increase, write BI strategists Gina Martin Adams and Peter Chung. Earnings will need to be the main driver of stock performance, as valuations are likely to compress with rising interest rates.

- In the wake of the stock market's 10 percent correction and subsequent recovery, Marko Kolanovic, JPMorgan's global head of quantitative and derivatives strategy provides two main arguments why equities should continue to climb. The first is that hedge fund equity beta will most likely increase from current levels, which would involve the purchase of stocks and in turn lift major indexes. The second is he expects volatility-targeting trades to pick up once again. In fact, he believes they've already started "very slowly rebuilding their equity positions.” And that rebuilding process means more stock buying.

- Intel is partnering with several companies to launch 5G-powered Windows 10 machines in 2019. Partner firms include Microsoft, Dell, Lenovo and HP.

Threats

- Walmart's stock dropped more than 10 percent Tuesday, its biggest single-day loss in 30 years, on reports that the company experienced a sharp slowdown in its e-commerce operations over the holiday season following three quarters of booming growth.

- Shares of Roku, the maker of connected TV boxes and software for smart TVs tumbled more than 20 percent in after-hours trading Wednesday. This came after the company said it expected first-quarter revenue of $120 million to $130 million, missing the $132 million Wall Street was expecting.

- People hate Snapchat's redesign so much that another Wall Street analyst downgraded the stock. Snap plunged by more than 7 percent Tuesday after two Citigroup analysts, Mark May and Hao Yan, downgraded the company to a sell and said, "While the recent redesign of [Snap's] flagship app could produce positive long-term benefits, [there is a] significant jump in negative app reviews since the redesign was pushed out a few weeks ago, which could result in a decline in users and user engagement, and could negatively impact financial results."

The Economy and Bond Market

Strengths

- The Conference Board’s US Leading Economic Index rose 1 percent in January following increases of 0.6 percent in December and 0.4 percent in November. The index accelerated further in January and continues to point to robust economic growth in the first half of 2018, according to Ataman Ozyildirim, director of business cycles and growth research at The Conference Board.

- U.S. business activity growth accelerated markedly in February, according to the flash PMI surveys, suggesting the economy is growing at its fastest pace in over two years. The headline IHS Markit Flash US Composite PMI jumped to 55.9 in February, up from 53.8 in January and the highest reading since November 2015.

- Americans’ outlook for the U.S. economy improved in February to the second-highest level since March 2002, the Bloomberg Consumer Comfort Index showed. Further, the Bloomberg Economic Expectations gauge climbed to 54.5, up from 52.5 in January.

Weaknesses

- Sales of previously owned U.S. homes unexpectedly fell in January to a 4-month low, a National Association of Realtors report showed. Contract closings fell 3.2 to a 5.38 million annual rate, down from the month prior at 5.56 million.

- Men in their prime working years have left the labor force at an astonishing rate and they may never return if the state of the U.S. job market holds, according to a new report from the Federal Reserve Bank of Kansas City. A decline in demand for middle-skilled work, a phenomenon dubbed “job polarization” where more positions are concentrated at the higher and lower ends, has played a role in keeping prime-age men out of the job market, Didem Tuzemen, an economist at the Kansas City Fed, wrote this week. Without job polarization, Tuzemen estimated that 1.9 million more prime-age men would have been employed in 2016.

- The median price of a previously owned home in the U.S. sold in January was 41 percent higher than it was five years ago, the National Association of Realtors’ data showed on Wednesday. The acceleration in property values dwarfs the 12.6 percent advance in average hourly earnings. With home prices typically peaking in June, and mortgage rates currently the highest since 2014, housing affordability is set to worsen in coming months.

Opportunities

- American business confidence in the world economy is on the rise, adding to an uptick in overall optimism as U.S. tax cuts and looser regulation improve the outlook for domestic growth, according to a new study. 69 percent of leaders from mid-size companies across the U.S. said they were optimistic about the global economy this year, more than double the 30 percent in 2017, according to a JPMorgan survey. The results marked the highest share of confidence in the 8-year history of the report, which indicated small businesses are similarly optimistic.

- The Republican tax overhaul will broaden the income tax base in most states, boosting collections and giving elected officials options to use the revenue for growing pension costs or lowering tax rates, Moody’s Investors Service said.

- State treasurers are lobbying Congressional leaders to bring back advanced refundings to ensure that state and local governments have the tools to implement President Trump’s infrastructure plan. Congress should "maximize the use of tax-exempt bonds," the National Association of State Treasurers said in a letter.

Threats

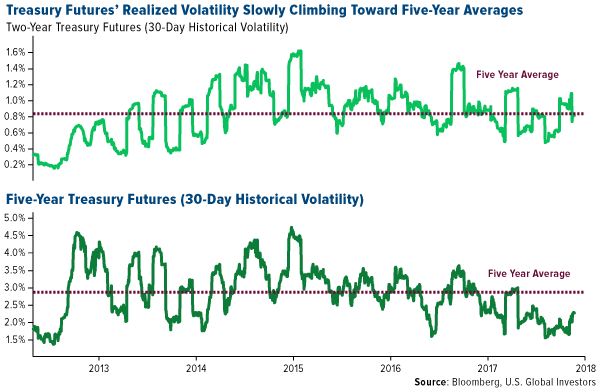

- While there’s a lack of consensus on the U.S. bond market’s next direction, the pickup in 30-day historical volatility for two- and five-year Treasury futures points to a rougher ride. This comes as greater U.S. borrowing compounds the impact of a global monetary shift to less accommodation.

- The impact of raising the gas tax by 25 cents per gallon, as the U.S. Chamber of Commerce has suggested and Trump reportedly has offered to support, would vary widely from state to state because of differences in the current tax rate and fuel consumption, the report by Americans for Prosperity and Freedom Partners shows. The top 10 states identified by the groups as facing the highest percent change increase in total gas tax liability are: Alaska, 81 percent; Oklahoma, 71 percent; Missouri, 70 percent; Mississippi, 67 percent; New Mexico, 67 percent; Arizona, 67 percent; Texas, 65 percent, Louisiana, 65 percent; South Carolina, 64 percent and Alabama, 64 percent. “Every American stands to lose under this proposal, but some would be more heavily impacted than others,” says the report from the two organizations that are part of the political network led by Charles and David Koch.

- Munis will probably perform worse than Treasuries in the “near term" as issuance starts picking up in March and April, according to Barclays municipal strategist Mikhail Foux who also said the current pace of issuance is "unsustainably low.''

Gold Market

This week spot gold closed at $1,328.75, down $18.35 per ounce, or 1.36 percent. Gold stocks, as measured by the NYSE Arca Gold Miners Index, ended the week lower by 2.85 percent. Junior-tiered stocks outperformed seniors for the week, as the S&P/TSX Venture Index came in at 0.49 percent. The U.S. Trade-Weighted Dollar strengthened this week and rose 0.88 percent.

| Date | Event | Survey | Actual | Prior |

|---|---|---|---|---|

| Feb-20 | Germany ZEW Survey Current Situation | 93.9 | 92.3 | 95.2 |

| Feb-20 | Germany ZEW Survey Expectations | 16.0 | 17.8 | 20.4 |

| Feb-22 | Initial Jobless Claims | 230k | 222k | 229k |

| Feb-23 | Eurozone CPI Core YoY | 1.0% | 1.0% | 1.0% |

| Feb-26 | New Home Sales | 650k | -- | 625k |

| Feb-27 | Hong Kong Exports YoY | 15.5% | -- | 6.0% |

| Feb-27 | Germany CPI YoY | 1.5% | -- | 1.6% |

| Feb-27 | Durable Goods Orders | -2.3% | -- | 2.8% |

| Feb-27 | Conf. Board Consumer Confidence | 126.0 | -- | 125.4 |

| Feb-28 | Eurozone CPI Core YoY | -- | -- | 1.0% |

| Feb-28 | GDP Annualized QoQ | 2.5% | -- | 2.6% |

| Feb-28 | Caixin China PMI Mfg | 51.3 | -- | 51.5 |

| Mar-1 | Initial Jobless Claims | 226k | -- | 222k |

| Mar-1 | ISM Manufacturing | 58.9 | -- | 59.1 |

Strengths

- The best performing metal this week was palladium, up 0.11 percent as hedge funds boosted their net bullish in the metal. Gold traders are split between bullish and bearish on the yellow metal after the U.S. dollar rose this week. In the prior week traders were bullish and positive sentiment sent $529 million into the VanEck Gold Miners ETF.

- According to Haywood Cheung Tak-hay, president of the Chinese Gold & Silver Exchange Society, China is in talks with Singapore, Myanmar and Dubai to set up a gold commodity corridor to promote gold trading using yuan as the main currency. This is part of Beijing’s “One Belt, One Road Initiative” and would use Hong Kong as a base for the exchange.

- The Russian Central Bank surpassed China to become the fifth-largest sovereign holder of gold, reports Bloomberg. Russia increased its holdings to 1,857 tons, topping China’s reported 1,843; however, China has not officially reported its holdings since October 2016. Switzerland’s gold imports increased 26 percent in January to 204.5 tons, the highest amount since last September with the majority exported to China and Hong Kong.

Weaknesses

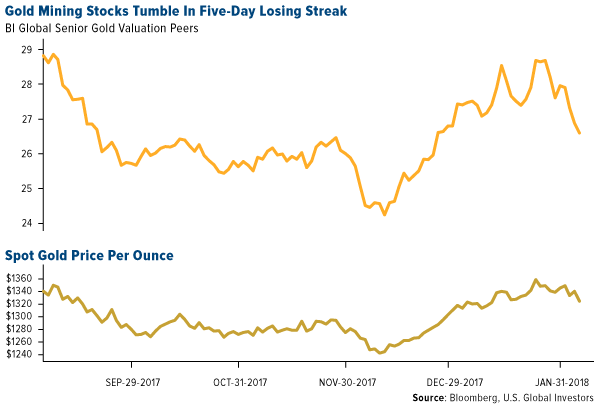

- The worst performing metal this week was gold, down 1.36 percent. Gold fell this week on the heels of a stronger U.S. dollar. UBS strategist Joni Teves writes that gold continues to be sensitive to dollar moves and that equities bouncing back have hurt the yellow metal some. Teves said that gold’s year-to-date performance “has to do with the dollar falling as much as 4 percent so far this year, and being down as much as 15 percent since early 2017.”

- The gold price fell five consecutive days, the longest stretch since last June after the Federal Reserve meeting minutes from January showed increasing confidence in economic growth, reports Bloomberg. Bullion for immediate delivery fell to $1,321 on Thursday, the lowest since February 14.

- Several gold companies experienced losses in the fourth quarter last year according to Bloomberg First World. Alamos Gold’s fourth quarter operating revenue missed the average analyst estimate, coming in at $161.7 million versus estimates of $165 million. Iamgold reported an unexpected fourth quarter loss with a loss per share of 3 cents while estimates were for a loss of 2 cents per share. Torex Gold also reported losses per share of 25 cents versus the estimate of a 12 cent loss per share.

Opportunities

- Analysts are debating how high 10-year Treasury yields will go with median forecasts compiled by Bloomberg see them rising to 3 percent by the end of this year. If history is any guide, during the last five rate hiking cycles the short end of the curve raised the most with the long end largely anchored. If long rates do indeed remain subdued, perhaps the dollar will not see renewed strength which would be positive for the price of gold.

- BMO has picked up coverage of Wesdome Gold Mines with an outperform rating and price target set to C$3.75. SilverCrest Metals has also been given a buy rating with drilling active at their high grade Mexican mine and a new larger resource statement is expected shortly.

- Northern Star Mining recently paid out a 4.5 cents per share, which is higher than estimates of 4 cents. The stock has grown from 2 cents per share up to $6 per share in the last eight years, and its executive chairman Bill Beament says that it is still a “growth stock” with their forecasted production. Newmont Mining Corp almost took over Barrick as the biggest bullion producer in the world, according to Bloomberg. Newmont was just 50,000 ounces, or 125 gold bars, away from claiming the top spot. Newmont doubled its quarterly payout to 14 cents a share and pushed itself ahead of Barrick in terms of market share.

Threats

- At Janet Yellen’s final Fed meeting, she and her colleagues received a special briefing on what had gone wrong with the computer models used to forecast price measures and inflation, reports Bloomberg. According to that briefing, the models used seemed to come up short on explaining and forecasting inflation. “Perhaps even more troubling for policy makers is that inflation appears to be anchored below the Fed’s 2 percent target,” the article reads.

- Canada, the top steel and aluminum exporter to the United States, is hopeful of being exempt of President Trump’s crackdown on foreign shipments, reports Bloomberg. Although the U.S. Commerce Department didn’t recommend giving Canada a pass during the outline of tariffs and quotas on Friday, it did single out its importance to the U.S. aluminum industry and numerous cross border manufacturing relationships, the article continues.

- Apple has become the latest major consumer to seek long-term supply deals with cobalt firms, which sent China Molybdenum’s stock surging as much as 10 percent on the news, reports Bloomberg. In fact, Apple is one of the world’s largest end users of cobalt for the batteries inside of its various gadgets, but up until now left the business of buying the metal to the companies that make its batteries. With the rapid growth in battery demand for electric vehicles threatening to create a shortage of raw material, the tech giant maker is “keen to ensure that cobalt supplies for its iPhone and iPad batteries are sufficient,” the story continues. This is almost reminiscent of when Ford started switching to a more palladium centric catalyst for emission and drove the price up ten-fold to later fall about 80 percent. However, the next generation of batteries may be cobalt free, as Nano One had developed for commercial testing a high voltage spinel (HVS) using lithium, manganese and nickel. Besides avoiding the high cost and supply chain risk of cobalt, the higher six-volt cells would mean fewer battery cells needed, less weight, less cost extending range, longer lifetime or better warranties, greater storage, faster charging and more power.

Blockchain and Digital Currencies

Strengths

- Of the cryptocurrencies tracked by CoinMarketCap, the best performing for the week ended February 23 was LendConnect, which gained 220 percent.

- For the first time since January, Bitcoin broke through the $11,000 mark on Tuesday, reports Seeking Alpha. The popular currency moved on Venezuela’s announcement of the pre-sale of its new “petro” currency. The petro is backed by oil, gas, gold and diamond reserves, and according to President Nicolas Maduro, it raised $735 million in the first day of its pre-sale this week.

- This week South Korean regulators signaled that they will actively support what they call “normal” cryptocurrency trading, reports Bloomberg. The comments made by Choe Heungsik, governor of South Korea’s Financial Supervisory Service, were quite the shift from earlier rhetoric that had hinted at an outright ban of cryptocurrency exchanges, the article continues.

Weaknesses

- Of the cryptocurrencies tracked by CoinMarketCap, the worst performing for the week ended February 23 was bitJob, which lost 26 percent.

- “For now it is difficult for the IRS to really find out on an individual basis whether you reported your virtual currency sales or exchanges,” says Ryan Losi of Virginia accounting firm PIASCIK. According to CNBC, if you sold crypto-coins or used crypto to buy anything in 2017, you probably owe the IRS taxes, and not paying can have consequences.

- A short-term system glitch at Osaka-based Zaif exchange allowed some customers to claim Bitcoin tokens for free, reports Seeking Alpha. In fact, one client “purchased” $20T worth of Bitcoin and then attempted to cash out. According to the article, the issue was fixed quickly and the exchange is in the process of resolving the issue with its customers.

Opportunities

- Prime Shipping Foundation, which is the shipping agency that struck the first freight deal settled in Bitcoin, is now seeking $150 million to launch its own digital coin, reports Bloomberg. “Using its own cryptocurrency would ease conversions into and out of traditional currencies, speeding settlement,” says Chief Executive Officer Ivan Vikulov.

- Coinbase Inc., the largest crypto exchange in the U.S., is planning to roll out an upgrade for its SegWit software, reports Bloomberg. This upgrade would aim to reduce transaction fees that customers pay when sending Bitcoin, the article continues.

- A new use for blockchain technology could save billions of dollars per year. According to the Financial Times, if the investment industry adopted blockchain to replace the current manual practices involved in buying and selling funds, based on estimated daily trade volumes, it could save $2.7 billion per year. Calastone, a UK-based firm, tested blockchain to sell funds and reported it was successful in processing transactions.

Threats

- The operator of “a now-defunct cryptocurrency investment platform” has been charged with lying to the Securities and Exchange Commission about a hack, writes Bloomberg. Jon Montroll, who operated BitFunder, tried to cover up the fact that hackers stole more than 6,000 of his customers’ Bitcoins, the article continues, lying under oath to the SEC.

- Shares of a blockchain startup company called Riot Blockchain tumbled hard in recent weeks, reports Bloomberg. On February 16 the “biotech-company-turned-blockchain-startup” lost a third of its value after CNBC broadcast an investigative story on the stock, the article continues.

- According to Bank of England’s Mark Carney, Bitcoin “has pretty much failed” as traditional money, reports MarketWatch. In a question and answer session at London’s Regent’s University, Carney continued by stating, “It is not a store of value because it is all over the map. Nobody uses it as a medium of exchange.”

Energy and Natural Resources Market

Strengths

- Lumber was the best performing major commodity this week rising 4 percent. The commodity surged to extend its rally to all-time high prices after a Canadian producer delayed the construction of a new facility, which may fuel further price hikes.

- The best performing sector this week was the S&P1500 Fertilizers and Agricultural Chemicals Index. The index rose 3.20 percent after JPMorgan surprisingly upgraded its view on fertilizer prices, arguing positive sector fundamentals are brewing after Mosaic reduced phosphate production in the U.S. through plant idling; and India, a large importer of phosphates, has low inventories, which may lift demand.

- The best performing stock for the week was Daqo New Energy Corp. The Chinese manufacturer of photovoltaic products for the solar power industry rose 11.90 percent after Steve Cohen’s famous Point72 hedge fund reported it had added shares in the company on its latest 13F filing.

Weaknesses

- Iron ore was the worst performing commodity this week. The commodity dropped 14.67 percent after China’s top steel-making city could impose further output curbs after the end of the winter season to improve air quality, according to Bloomberg. An extension of the output curbs lowers steelmakers' need for iron ore as a critical input in the steelmaking process.

- The worst performing sector this week was the S&P/TSX Composite Gold Index. The index dropped 3.40 percent after gold prices posted a third weekly decline in four as the Federal Reserve’s upbeat assessment of the U.S. economy fuels speculation that policy makers will step up the pace of monetary tightening, leading to a recovery in the U.S. dollar.

- The worst performing stock for the week was Devon Energy Corp. The major oil and gas producer dropped 7.86 percent, the most in two years after the oil explorer fell short of fourth-quarter production estimates and failed to present specific plans to boost investor returns.

Opportunities

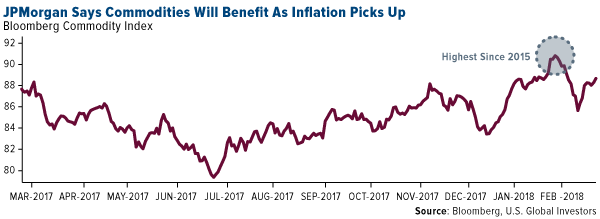

- Inflation is back and commodities will benefit, according to JPMorgan. “Inflation has come and it should be good for commodities,” the bank said in a report. Among signs of the shift, JPMorgan cited stronger US wage numbers as well as recent core consumer price inflation. Bets on gains in precious metals, copper, zinc and nickel will probably result in the highest returns over one year, the bank said.

- OPEC-led production cuts may have achieved their initial purpose of re-balancing the global crude market. Yet Saudi Energy Minister Khalid Al-Falih wants to go further. “Producers should keep cutting for the whole year, even if it causes a small supply shortage,” Al-Falih said. “If we have to overbalance the market a little bit, then so be it,” he told reporters in Riyadh last week.

- North American energy producers survived the recent oil bust in large part by selling more than $60 billion of new stock. Now they’re beginning to buy it back. Several oil and gas producers have started the year by initiating or enlarging share-repurchase programs. The buybacks reflect oil prices that have climbed enough for them to drill profitably and shareholders who have urged companies to focus more on the bottom line.

Threats

- Canada’s energy stocks drop to the lowest in two years despite better global crude prices. With pipeline, regulatory and political frustrations reaching new heights, Canadian energy companies have seen weak prices, caused by the pipeline pinch. Western Canadian Select, the main grade of oil extracted by Canadian oil-sands producers, is trading near the widest discount to West Texas Intermediate crude in almost four years.

- Gold prices dropped after a growing number of economists expect the Federal Reserve to step up the pace of its interest-rate increases this year after congressional passage of a US$300 billion government spending package that is seen lifting U.S. economic growth and inflation. “Stronger growth and higher inflation would increase the odds of four Fed rate hikes in 2018.”

- Eurozone business growth has slowed more than expected this month but remains robust. IHS Markit’s composite flash PMI for the eurozone, seen as a good guide to economic health, fell to 57.5 this month, below all forecasts in a Reuters poll, echoing the first broad-based setback in euro area PMIs; still strong, but down from their recent high.

China Region

Strengths

- Taiwan, which reopened after a lengthy Lunar New Year holiday period, jumped 3.58 percent this week. Singapore also put in a strong showing, climbing 2.61 percent after reopening.

- Hong Kong visitor arrivals from mainland China were up 15 percent year-over-year during the Lunar New Year holiday period. These numbers were in the neighborhood of gains for Macau, which saw Golden Week visitor arrivals from mainland China up 12.3 percent year-over-year.

- Materials constituted the strongest performing sector for the Hang Seng Composite this week, climbing 3.69 percent.

Weaknesses

- This week was a generally green one, but among the weakest regional performers were the Philippines Stock Exchange Index, up 22 basis points since last Thursday, and India’s SENSEX and NIFTY indices, up 26 and 40 basis points, respectively, since last Friday.

- Fourth-quarter GDP readings in Thailand missed expectations this week. Quarter-over-quarter GDP came in up 0.50 percent, shy of an anticipated 0.7 percent and down from the third quarter’s 1.0 percent rate, while the year-over-year reading clocked in at 4.0 percent, shy of analysts’ expectations for a 4.3 percent reading and down from last quarter’s pace of 4.3 percent.

- The only Hang Seng Composite sector to finish in the red this week was financials, which declined 42 basis points.

Opportunities

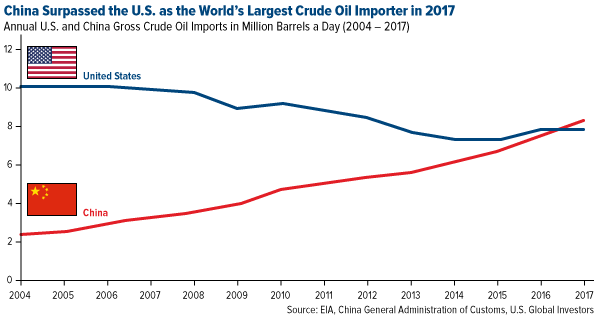

- According to the U.S. Energy Information Administration (EIA), for the first time in 2017, China imported more crude oil than the United States. Last year the Asian nation brought in an average 8.4 million barrels per day, compared to 7.9 million barrels per day for the U.S.

- According to Ministry of Commerce data released on Wednesday, Chinese shoppers stepped up spending during this year’s week-long Lunar New Year holiday, reports Reuters. The retail and catering sectors posted sales of 926 billion yuan during the holiday period that began February 15 and ended Wednesday, the article continued, with Chinese movie box office receipts also rising nearly 60 percent.

- As the South China Morning Post reports, a Chinese research team has come up with a novel design for an “ultra-fast plane” they say would travel at hypersonic speed. “It will only take a couple of hours to travel from Beijing to New York,” the researchers led by Cui Kai wrote in a paper this month published by Science China Press. Right now, it takes a typical passenger jet 14 hours to fly between the two cities, the article continues.

Threats

- A report from the Financial Times alleging that inmates of a Chinese prison made packaging used by two European fashion giants has sparked an investigation by the companies, reports Reuters. Retailers H&M and C&A, along with technology company 3M are looking into the claims. “We have a zero tolerance policy for any form of modern slavery including forced, bonded or prison labor,” C&A’s chief sustainability officer Jeffrey Hogue said in an email statement. “If we detect a case we immediately terminate our relationship with the supplier.”

- Chinese takeovers of U.S. companies may get pushed even further to the backburner, at least for the time being. Chinese authorities announced that the government seized control of Anbang Insurance Group Co., and according to Bloomberg News, “will prosecute its founder, Wu Xiaohui, for alleged fraud.” Like some other Chinese companies, Anbang had been on something of a buying binge over the last few years, fueled by debt and likely attempting to diversify away from what had been a weakening yuan. Indeed, since the start of 2015, Bloomberg notes, some $72 billion worth of outbound Chinese takeovers of U.S. companies or real estate assets have been terminated.

- U.S. President Donald J. Trump announced Friday that the administration is imposing the largest sanctions yet against North Korea in another attempt to slow or discourage the East Asian nation’s nuclear weapons program. While there was some speculation that perhaps the Kim regime might reach out informally to meet with U.S. officials (including U.S. Vice President Mike Pence) at the Winter Olympic Games in Pyeongchang, South Korea, ultimately the meeting did not materialize (at least publicly). It would seem that the ante just went up in the “maximum pressure campaign” game.

Emerging Europe

Strengths

- Russia was the best performing country this week, gaining 3.6 percent. S&P rating agency raised Russia’s sovereign debt rating to investment grade from junk. Fitch did not cut Russia to junk status after Russia annexed Crimea, and Moody’s still rates Russia below investment grade (and will review the country’s ratings later in the year).

- The Russian ruble was the best performing currency this week, gaining 30 basis points against the U.S. dollar. The currency is highly correlated with the price of oil. Brent crude oil gained 4 percent this week, closing at $67.40 per barrel.

- Consumer staples was the best performing sector among eastern European markets this week.

Weaknesses

- Hungary was the worst performing country this week, losing 2 percent. OTP Bank and MOL Hungarian Oil and Gas PLC were the worst performing equites trading on the Budapest stock exchange. MOL lost 3.9 percent and OTP Bank 2.3 percent.

- The Hungarian forint was the worst performing currency this week, losing 1.6 percent. Hungarian rate setters will meet next Tuesday and are expected to leave borrowing costs at record lows. Despite solid economic growth, the dovish central bank’s outlook is weighing on the country’s currency.

- Information technology was the worst performing sector among eastern European markets this week.

Opportunities

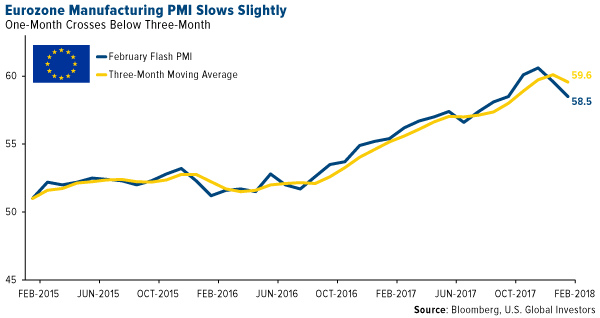

- Preliminary February manufacturing PMI for the eurozone came out slightly weaker at 58.5 versus expected 59.2; falling from the January reading of 59.6. PMI’s one month reading crossed below the three month moving average, indicating a possible trend reversal. Germany and France, the two biggest European economies, released slightly weaker manufacturing PMIs.

- Russia has overtaken China as the fifth-biggest sovereign holder of gold, increasing its holdings every month since March 2015, while China last reported buying gold in October 2016. Russia is the world’s third-largest gold producer, and most of the gold is purchased locally. Higher gold reserves offer Russia some independence from the dollar and protection from financial sanctions imposed by the U.S. and Europe.

- Fitch credit rating agency upgraded Greece by one notch to B from B- with a positive outlook. In addition, Moody’s rating agency upgraded Greece two notches to B3, saying the country looks set to return to the market-based funding following the conclusion of its current bailout program in the summer.

Threats

- Russia and Ukraine are ranked as the most corrupt countries in Europe by the latest Transparency International Corruption Perceptions Index rankings. Russia fell four places over the last year to be ranked 135 out of 180 countries in the ranking index. Ukraine is ranked at 130. The IMF delayed its last transfer of $1 billion to Ukraine on the lack of progress on the anti-corruption court. Hungary’s rating dropped more than any other European Union member in the past five years, placed at 66, just ahead of Jamaica and Belarus.

- Special counsel Robert Mueller’s team has either indicted or gotten guilty pleas from 19 people and three companies – with most of them being announced in the past week. More indictments could follow under his investigation on Russia interfering with the U.S. presidential campaign in 2016. Even more Russia-related sanctions are likely in the works.

- European Central Bank minutes from the January 22 meeting showed that the central bank is reluctant in changing its monetary stance, even if there are stronger inflation expectations. The bank could revisit its monetary policy “early in the year,” but it was too early to do so last month. Mario Draghi also said that the currency was as a “source of uncertainty.” A stronger euro could hurt European exports.

© US Global

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All