Italian general elections will be held on March 4, 2018. The key to power lies not just in forging allegiances, but navigating complex new electoral laws. The election comes against an improving economic picture and Italian equities have performed strongly over the last year, outpacing many other developed markets including the broader eurozone and the U.S. The iShares U.S. ETF Investment Strategy teams offers a pre-election primer and

considers market implications.

Key points:

- Our base case for the March 4 Italian general elections is a hung Parliament leading to a grand coalition between the major centrist parties. However, we encourage investors to follow the election in case of a surprise showing by populist parties leading to renewed questions over the future of the eurozone.

- The election occurs against a backdrop of an improving Italian economy and strong equity performance over the last 12 months.

- The fact that Italian fundamentals appear to be on an improving trend limits the material downside to risk assets from political developments.

Overview

The election will be fought between three main blocks:

-

The center-right: A coalition of parties including Forward Italy (Forza Italia), Northern League (Lega Nord) and Brothers of Italy (Fratelli d’Italia), led by former Prime Minister Silvio Berlusconi for Forward Italy and Matteo Salvini of Northern League (who do not always agree), and Giorgia Meloni for the far-right Brothers of Italy.

-

The center-left: anchored by Democratic Party (Partito Democratico or PD) with a few small parties, PD being led by Matteo Renzi.

-

Independent anti-establishment movement: Five Star Movement (Movimento 5 Stelle or M5S) led by Luigi di Maio, which has positioned itself as distinct from other parties and resistant to forming coalitions with them.

The challenge for each of these parties is a new, untested electoral law known colloquially as “Rosatellum,” which means that for the first time since 2001, voters will vote not just for a party, but for a candidate in a first-past-the-post race in their local community.1 One third of the seats are assigned by the first-past-the-post (uninominal) system and the remainder according to a full proportional system. Theoretically, even as little as 40% of the votes, depending on the performance of uninominal colleges, could be enough for a single party or coalition to get an absolute majority in Parliament.

The political landscape

Five Star is currently the largest party in Italy, PD has been in free fall in opinion polls (due to severe internal infighting and struggles to come up with a clear message) and the center-right coalition is well ahead of both. The center-right coalition is more likely to get a majority of the seats than any other coalition or party, currently polling at 37%.2 Berlusconi’s involvement has been a key driver behind this success in the polls, in spite of his inability to stand for election due to a 2013 tax fraud conviction. It currently appears that the most likely scenario is a hung Parliament – as the center-right will likely struggle to get enough votes in the south – followed by lengthy negotiations between the political parties.

Our base case, albeit with low conviction, is that a hung Parliament would most likely lead to a grand coalition between PD/Forward Italy and other centrist parties, while the possibility of a new election exists but is unprecedented during the Second Republic. Other scenarios, such as a national unity government supported by all parties, or an anti-establishment alliance with Five Star and the Northern League or PD, are less likely, in our view.

Given the new system and a high proportion of undecided voters, the polls are likely to be even less reliable than in the past. The impact of a higher turnout is unclear but on balance should favour establishment parties. A surprise showing by populist parties could lead to new questions about the durability of the eurozone.

Policies and promises

All the parties are making what are likely unrealistic electoral promises: These include a universal income proposal, a flat tax for households and companies, and the partial roll-back of labor market and pension reforms. However, even if these promises are unlikely to materialize in their current form, it is likely that the government deficit will increase and the fiscal tightening implied in the current stability plan will not take place, in our view.

Although the Northern League and Forward Italy have played to a supporter base discontent with immigration, on the key question of EU stance, the pro versus anti-Europe message does not appear to be playing a role in this campaign. As recently as January, even the anti-establishment Five Star indicated that plans for a referendum for exiting the eurozone would be seen as a “last resort”.3

Economic backdrop

Although it lags the rest of the eurozone, the Italian economy is doing well and its recovery from its worst recession since World War II has gained pace. Evidence points to a broad recovery in the manufacturing sector, while the Bank of Italy projected recently that the economy will expand by 1.5% this year and that growth should remain above 1% over the next two years, citing rises in household income and declines in firms’ spare capacity as signals of higher consumption and investment. Public debt has stabilized at approximately 132% of GDP.4

Italy keeps running a sizeable and stable current account surplus (2.8% of GDP)5. Moreover, its net international investment position, though still negative, has improved from approximately 35% of GDP in 2008 to less than 10% in Q3 20176. The banking sector, though still overloaded with non-performing loans (NPLs), appears to have turned the corner: The flow of new non-performing loans in the third quarter of 2017 in proportion to total loans fell to 1.7% (even lower than pre-financial crisis level of 2006-2007) and the stock of non-performing loans (net of provisions) fell to 8.4% of total loans in June 2017 from around 9.3% at the end of 2016.7

Investment implications

Markets have shown little reaction to Italian political risk, despite the extravagant electoral promises made by many of the campaigning parties. There may be a modest increase in volatility as the election approaches, but “tail risk” outcomes seem unlikely as no party currently looks like it will emerge with a clear mandate. Given the uncertainty around the election outcome we see reduced likelihood of fiscal tightening and even the potential for the partial rollback of structural reforms.

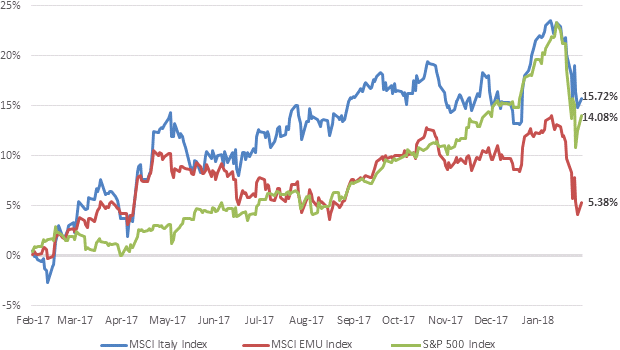

Notwithstanding the muted geopolitical risks, we are underweight European fixed income overall – across sovereigns and credit on account of ECB interest rate and asset purchase policies. Although we are neutral on broad European equities, the fact that Italian fundamentals appear to be on an improving trend limits the material downside to risk assets. Specifically, Italian equities have outperformed both the eurozone and U.S. equities over the past 12 months, supported by the region’s above-trend economic expansion. Italian equities do not look expensive relative to their historical norms; sitting just above average at their 50th percentile ranking.8

12 Month Index Performance

In the event of our base-case scenario, a hung parliament, the market response will depend on the performance of the establishment versus the anti-establishment parties. A strong anti-establishment vote has the potential to affect risk assets but the impact should be limited as the most likely eventual outcome is a PD/FI grand coalition with the explicit or implicit support of the small parties.

The bottom line: Markets are familiar with political uncertainty in the eurozone, but the fact that economic fundamentals have been on an improving trend may help limit any downside for Italy.

1 Source: Politico, January 15 2018.

2 Source: Financial Times, January 31 2018. FT Research poll-of-polls tracker ‘Voting intention, share by coalition (%)’, (https://ig.ft.com/italy-poll-tracker), retrieved 13 February 2018.

3 Source: Bloomberg, February 13 2018.

4 Source: Bloomberg, February 10 2018.

5 Source: Bloomberg, The Bank of Italy, November 2017.

6 Source: Bloomberg, National Institute of Statistics, Italy (Istat), January 18 2018.

7 Source: The Bank of Italy Central Credit Register and National Institute of Statistics, Italy (Istat), BlackRock Investment Institute, January 18 2018.

8 Source: BlackRock Investment Institute, with data from Thomson Reuters, January 31 2018 using data going back as far as 1969.

© iShares

Read more commentaries by iShares